Ever get to the end of the month and wonder, "Where did all my money go?" Zero-based budgeting provides a clear, powerful answer. At its core, it's a simple idea: you give every single dollar a job to do. Your income minus your expenses should equal exactly zero. It’s about starting fresh every single budget period, ensuring your money is working for you.

What Is Zero-Based Budgeting and How Does It Work?

Imagine instead of buying the same groceries out of habit, you sit down and plan every meal from scratch for the week. That’s the essence of zero-based budgeting (ZBB). You don’t just tweak last month’s numbers; you start with a blank slate and justify every single expense, every single time.

This approach is all about being intentional. Every dollar you earn gets a purpose, whether it's for rent in Toronto, groceries in Halifax, building your savings, or chipping away at debt. There’s no "miscellaneous" fund or money left floating around without a plan.

By assigning every dollar a job, you gain a firm grip on your financial life. This process shines a light on where your money is actually going, helping you make sure your spending truly lines up with your priorities.

Zero-based budgeting isn't about restriction. It's about empowerment. It’s about understanding exactly how your money can work for you, month after month.

How ZBB Differs From Traditional Budgeting

The biggest difference is the reset. With a traditional budget, you might just adjust last month's spending by a certain percentage. ZBB makes you start fresh every time. It’s this switch from passive tweaking to active planning that helps so many Canadians finally feel in control of their finances. This is where a tool like NeoSpend can be a game-changer, automatically tracking your spending so you have a clean slate of real numbers to work with each month.

To put it simply, the two approaches are worlds apart. Here’s a quick look at how they stack up.

Zero-Based Budgeting vs. Traditional Budgeting at a Glance

This table breaks down the fundamental differences between ZBB and the budgeting methods most of us are used to.

| Feature | Zero-Based Budgeting (ZBB) | Traditional Budgeting |

|---|---|---|

| Starting Point | Starts from zero each budget period. | Uses the previous period's budget as a baseline. |

| Focus | Justifies every single expense. | Focuses on incremental changes (e.g., "increase food by 5%"). |

| Awareness | High awareness of all spending habits. | Can overlook wasteful or unnecessary spending. |

| Effort Required | More detailed and time-intensive initially. | Quicker and simpler to create each month. |

As you can see, ZBB demands more upfront effort but delivers a much deeper understanding of your financial habits in return. It’s a proactive strategy for anyone tired of passively watching their money disappear.

How to Create Your First Zero-Based Budget in 4 Steps

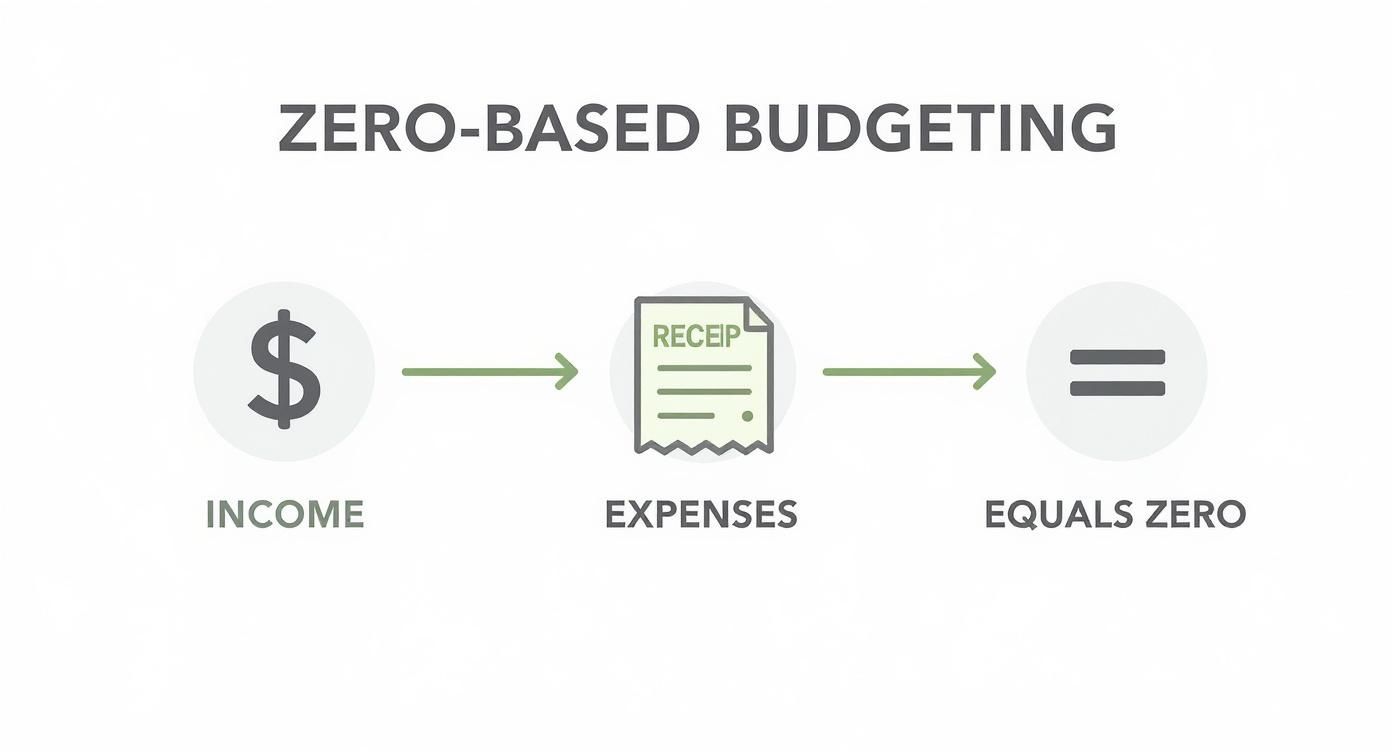

Ready to build your budget from the ground up? Getting started with zero-based budgeting is a simple process that puts you back in the driver's seat. It all comes down to one powerful formula: Income - Expenses = Zero.

We’ll walk through the four main steps. Think of it less as a chore and more as a strategy—a way to see exactly where your money is going so you can start telling it where to go instead.

This chart shows the basic idea perfectly.

You start with your total income, account for everything you spend, and aim for that perfect balance of zero. Every single dollar gets a job.

Step 1: Pinpoint Your Total Monthly Income

First, you need a clear number for how much money is coming in each month. We're talking about your total net income—the actual amount that lands in your bank account after taxes and deductions.

If you're a salaried employee in Canada, this is usually the straightforward number on your pay stub. But for freelancers or anyone with a variable income, look at your average earnings over the last few months to get a realistic baseline. Don't forget to include income from any side hustles, like driving for a ride-share service or selling crafts online.

Step 2: Track Every Single Expense

Next, it's time to play detective and figure out where your money has been going. This part takes a little digging. Pull up your bank and credit card statements from the last month or two to get a real, honest look at your spending habits.

To make sense of it all, start sorting your spending into categories. Most of your expenses will likely fit into one of these buckets:

- Fixed Costs: Predictable bills that don't change month to month. Think mortgage or rent, car payments, and insurance premiums.

- Variable Costs: This is the stuff that fluctuates, like how much you spend on groceries, gas for the car, dinners out, or entertainment.

- Irregular Costs: Don't let these catch you by surprise! These are expenses that only pop up now and then, like an annual subscription renewal, holiday gifts, or car maintenance. It’s crucial to plan for these.

Step 3: Assign Every Dollar a Job

This is where the magic happens. With your income and expenses laid out, you can now give every single dollar a specific purpose until your income minus your expenses equals zero.

Start with your needs—all those fixed costs and essential variable spending. Once those are covered, direct your money toward your financial goals. This could be paying down a student loan faster, beefing up your TFSA or RRSP, or saving for a down payment. Whatever is left over can then be assigned to your wants, like hobbies or a travel fund.

For example, if your monthly take-home pay is $4,000, you might assign $1,500 to rent, $500 to groceries, $400 to debt repayment, and $600 to savings. You’d keep going like this, assigning every dollar, until you've accounted for the full $4,000.

Step 4: Review and Adapt Monthly

A zero-based budget isn’t something you set once and forget. It's a living document. Life happens, things change, and your financial priorities will probably shift. At the end of every month, take some time to compare your spending against what you had planned. Did you overspend on takeout? Did you manage to save more than you expected?

This monthly check-in is your chance to tweak and adjust for the month ahead. It’s this flexibility that makes ZBB so effective over the long run. Using an app like NeoSpend makes this process much smoother by automatically categorizing your expenses and tracking your spending in real-time. It gives you the clarity you need to adapt your budget and stay on track with your goals.

The Pros and Cons of Zero-Based Budgeting

Is zero-based budgeting (ZBB) right for you? Like any money management style, it has its pros and cons. For many Canadians, making the switch brings a ton of clarity to their finances, but it’s definitely not a magic wand. It takes work.

The biggest win is the heightened awareness it forces on you. When you build your budget from scratch every month, you can't just go on autopilot. You have to actively justify every dollar you plan to spend. It’s this intentionality that helps connect your spending to what you truly value.

This hands-on planning often puts you on the fast track to your financial goals. Whether you’re trying to save for a down payment on a condo in Vancouver or pay off student loans from your time in Montreal, ZBB makes sure your goals get paid first, not just with whatever’s leftover.

The Upsides of Going Zero-Based

Adopting a ZBB approach can seriously change how you handle your money. It's less of a tracking system and more of a total mindset shift.

Here are some of the biggest perks:

- Total Financial Control: You know exactly where every dollar is going. No more wondering where your paycheque vanished to. It helps you stop wasteful spending before it even starts.

- Intentional Spending: ZBB makes you evaluate every purchase. This naturally helps you cut back on things that don't really add value to your life.

- Faster Goal Achievement: By assigning money directly to savings or debt repayment first, you can make real, measurable progress on the financial milestones that matter most.

- Built-in Accountability: This method holds you accountable for your decisions, which builds discipline and helps you create money habits that actually stick.

At its heart, zero-based budgeting turns your budget from a boring report on past spending into an active, forward-looking game plan for your money.

And it’s not just a trick for personal finance. Big organizations use this same strategy to get their spending under control. For instance, the City of San Diego used ZBB to completely overhaul its budget, rein in costs, and cut out waste by making every department justify its expenses from scratch.

The Potential Downsides of ZBB

While the benefits are compelling, you have to be realistic about the downsides. ZBB isn't a "set it and forget it" kind of deal; it demands your attention and a bit of grunt work.

The biggest hurdle for most people is that it can be time-intensive, especially when you’re just getting started. Sitting down to review every expense category and build a new plan each month takes more effort than just glancing at a traditional budget.

On top of that, the level of detail required can feel a bit much. You really need to keep a close eye on your spending throughout the month to make sure you’re sticking to the plan. This is where a tool like NeoSpend can be a lifesaver by automatically categorizing your transactions and taking the pain out of tracking.

Finally, ZBB can be a challenge for anyone with an unpredictable or fluctuating income—think freelancers, gig workers, or people who rely on commissions. When you don't know exactly what you'll earn, creating a precise plan from a "zero base" requires more guesswork and flexibility.

Zero-Based Budgeting Examples for Canadians

Theory is one thing, but seeing zero-based budgeting in action is where it really clicks. To understand what this method is all about, let’s look at how it plays out in the real lives of Canadians. The basic formula never changes: Income - Expenses = $0.

Here are a few simplified monthly budgets for different Canadian scenarios, showing how you can give every dollar a job, no matter your goals.

University Student in Toronto

For a student juggling a part-time job and classes, the margins are thin. Their ZBB is all about covering essentials while trying to keep student debt from piling up.

Monthly Net Income: $2,100

- Housing:

- Rent (shared apartment): $900

- Utilities & Internet: $100

- Education & Living:

- Groceries: $300

- Transit Pass (TTC): $130

- Phone Bill: $50

- Textbooks/Supplies Savings: $70

- Financial Goals:

- Tuition Savings Fund: $300

- Emergency Fund Contribution: $50

- Personal Spending:

- Entertainment/Social: $150

- Subscriptions: $20

Total Assigned: $2,100

Remaining: $0

Freelance Designer in Vancouver

A freelancer’s income can be unpredictable, so they have to be proactive about business costs and saving for taxes. Their ZBB is built on a conservative income estimate to stay safe.

Monthly Net Income (Conservative Estimate): $5,000

- Housing & Utilities:

- Rent: $2,200

- Hydro & Internet: $150

- Business & Financial:

- Tax Savings (Set aside 30%): $1,500

- Business Software/Tools: $100

- Living Expenses:

- Groceries & Dining Out: $500

- Transportation (Compass Card & Car Share): $150

- Phone Bill: $80

- Goals & Personal:

- RRSP Contribution: $200

- Personal Savings (Travel): $120

Total Assigned: $5,000

Remaining: $0

Any income earned above the $5,000 baseline can be strategically assigned to accelerate goals, such as making a larger RRSP contribution, paying down debt, or topping up their emergency fund.

Young Family in Calgary

For a young family, the budget is a balancing act between covering today's costs and planning for big-picture goals like their kids' education and their own retirement.

Monthly Net Income (Combined): $7,500

- Housing:

- Mortgage Payment: $2,500

- Property Tax & Insurance: $450

- Utilities (Gas, Electricity, Water): $350

- Family & Living:

- Groceries & Household Supplies: $1,200

- Childcare: $1,000

- Car Payment & Insurance: $600

- Gasoline: $300

- Financial Goals:

- RESP Contribution: $250

- TFSA Savings: $500

- Personal:

- Family Activities/Entertainment: $350

Total Assigned: $7,500

Remaining: $0

Young Professional in Montreal

A young professional is often laser-focused on crushing debt while still trying to build savings and enjoy city life. Their budget reflects that hustle.

Monthly Net Income: $4,200

- Housing & Bills:

- Rent: $1,400

- Hydro & Internet: $120

- Debt Repayment:

- Student Loan (Extra Payment): $800

- Living Expenses:

- Groceries: $450

- Transit Pass (STM): $97

- Phone Bill: $70

- Financial Goals & Savings:

- TFSA (Investment): $500

- Emergency Fund: $200

- Personal & Lifestyle:

- Dining Out & Social: $400

- Gym Membership: $63

- Shopping/Miscellaneous: $100

Total Assigned: $4,200

Remaining: $0

Each of these scenarios shows how zero-based budgeting creates a crystal-clear roadmap for your money. Using a tool like NeoSpend makes it even easier by automatically sorting your expenses, so you can see exactly how your spending lines up with your plan in real time.

Common Mistakes to Avoid When Starting Your Budget

Making the jump to zero-based budgeting is a fantastic move, but it's easy to stumble out of the gate. Knowing a few common hurdles ahead of time can mean the difference between a budget that empowers you and one that just adds stress.

One of the biggest mistakes people make is getting too strict. Yes, ZBB is all about precision, but if you create a plan with zero wiggle room, you’re setting yourself up for burnout. Life is messy, and a budget that can’t bend will eventually break.

Another classic oversight is completely forgetting about irregular expenses. You know the ones—the costs that pop up a few times a year and throw a wrench in your plans if you're not ready. Think annual subscriptions, car repairs, or holiday spending.

Building Flexibility Into Your Budget

To keep from getting discouraged, you must build some breathing room into your plan. This doesn't mean leaving cash unassigned—that would go against the ZBB philosophy. Instead, you create specific jobs for your money that cover flexibility and those surprise costs.

An easy way to do this is with a small ‘Miscellaneous’ or ‘Buffer’ category. Assign a modest amount to it, maybe $50 or $100, to handle small, unexpected things without blowing up your entire budget. Think of it as your financial shock absorber.

The point of zero-based budgeting isn’t to suffocate your spending; it’s to give you a clear, intentional plan. The best budget is one you can actually stick with, and that always requires a little bit of flexibility.

For those bigger expenses you know are coming but aren't monthly, a little trick called sinking funds is a game-changer.

Planning for Irregular and Emergency Costs

A sinking fund is a dedicated savings pot for a specific future expense. You contribute a small amount each month, so when the bill arrives, the cash is sitting there waiting. It turns a potential financial panic into just another planned payment.

Here’s how you could put sinking funds to work:

- Annual Car Insurance: If your premium is $1,200 a year, you’d tuck away $100 each month into its own fund.

- Holiday Gifts: Planning to spend $600 on presents? Start saving $50 a month in January, and you're all set.

- Vehicle Maintenance: Put aside a set amount every month for things like new tires or oil changes so it never feels like a surprise hit.

It's important to remember that sinking funds are not the same as your emergency fund. Your emergency fund is your safety net for true, unforeseen crises, like a sudden job loss or a medical bill. Sinking funds are for costs you can see coming. Having both is what makes your financial plan truly resilient. With NeoSpend, you can set up specific savings goals that act as digital sinking funds, making it super easy to track your progress.

How NeoSpend Makes Zero-Based Budgeting Effortless

The idea behind zero-based budgeting is fantastic for gaining control, but let's be real—the day-to-day manual tracking can feel like a part-time job. Having the right tool can make all the difference. We built NeoSpend to smooth out the trickiest parts of this powerful budgeting method.

For most Canadians, the biggest hurdle is keeping up with every single transaction. NeoSpend tackles this head-on with automatic expense categorization. It securely syncs with your Canadian bank accounts and credit cards, sorting your spending on the fly so you don't have to wade through receipts and statements.

Align Your Budget with Your Life

A budget is useless if it doesn't fit your life. NeoSpend lets you build fully customizable budget categories that mirror your ZBB plan.

- Create Your Categories: Set up budgets for everything, from the big stuff like your mortgage and groceries to specific savings goals, like an RESP for the kids or that dream trip to Banff.

- Track in Real-Time: Instantly see how much you've spent in each category. No more guesswork or waiting until the end of the month to see where you stand.

- Adjust on the Fly: Life happens, and your budget needs to be able to roll with it. NeoSpend makes it simple to tweak categories and amounts as your priorities change.

With NeoSpend, you're not shoehorned into a rigid template. You build a budget that makes sense for you, and the app does the heavy lifting to keep you on track.

Best of all, NeoSpend helps you sidestep the overspending that can derail a good plan. You'll get real-time spending alerts that give you a gentle nudge when you’re getting close to a category limit—before you go over. This small feature transforms ZBB from a time-consuming chore into a streamlined, achievable habit, putting you back in control of your money.

Your Top Questions, Answered

Got a few more questions about zero-based budgeting? Let's clear them up. Here are the answers to some of the things we hear most often from Canadians trying this method for the first time.

What if I’m a Freelancer or Have a Fluctuating Income?

This is a big one, and the short answer is: yes, you absolutely can. The trick is to build your budget around your most conservative, rock-bottom monthly income estimate. Think of it as your baseline.

Then, in those amazing months when you earn more, you’re not just spending it blindly. You get to intentionally decide where that extra cash goes—maybe it’s an extra payment on your student loan, a boost to your TFSA, or finally starting that emergency fund.

Isn’t This Just the Same as Tracking My Expenses?

Not at all. Tracking your expenses is like looking in the rearview mirror; it shows you where your money already went. It’s a passive activity.

Zero-based budgeting is like using a GPS. It’s a proactive plan that tells every single one of your dollars where to go before the month even starts. You’re in the driver's seat, not just along for the ride.

How Long Until This Doesn't Feel Like So Much Work?

Fair question. Give yourself about three months to really get the hang of it.

Your first month is going to be a bit of a learning curve. You'll be figuring out your real spending habits and where your money actually goes. By month three, the process will feel much more natural. It stops being a chore and starts feeling like an seriously empowering habit.

Your Takeaway

Zero-based budgeting is a proactive way to manage your finances that puts you in complete control. By giving every dollar a job, you ensure your spending aligns with your goals, helping you save more and reduce debt faster. While it takes more effort upfront than traditional budgeting, the clarity and control it provides can be life-changing for your financial well-being.

Ready to put your money to work? NeoSpend makes giving every dollar a job surprisingly simple with its automatic expense tracking and easy-to-tweak budgets. See how NeoSpend can help you master your money.