Think of financial planning as creating a personalized roadmap for your money. It's the process of figuring out how to manage your finances so you can hit your life goals, whether that’s buying a home in the suburbs or finally retiring with enough to be comfortable. In simple terms, it's about telling your money where to go, instead of wondering where it went.

Why a Financial Plan is Your Blueprint For Life

You wouldn't build a house without a blueprint, right? You’d probably end up with crooked walls and a leaky roof. The same logic applies to your money. Without a plan, it's easy to feel lost or make choices that don't get you closer to where you want to be.

Financial planning is that blueprint. It’s like a GPS for your finances. You plug in your destination—maybe buying a condo in Vancouver or funding your kid's education—and the plan maps out the best route to get there. It shows you where you stand now, where you're headed, and the specific turns you need to make along the way.

Why Financial Planning Matters For Canadians

This isn't just a "nice-to-have" anymore, especially for Canadian households. Money is a huge source of stress for many people, and financial worries consistently top the list of anxieties.

Research from FP Canada’s Financial Stress Index shows this anxiety has been climbing since 2021. The study also uncovered a harsh reality: 51% of Canadians say they don’t have enough left over after bills to save or invest. This is exactly why having a plan has gone from a luxury to a necessity. You can dive into the full research from FP Canada to see more of these trends.

A solid financial plan cuts through the noise. It gives you clarity and the confidence to handle economic pressures with a real strategy.

Financial planning isn’t about cutting out all the fun. It’s about making your money work for your values, so you can spend intentionally on what actually matters to you.

Who Needs A Financial Plan?

There's a persistent myth that financial planning is only for the super-wealthy. That's simply not true. It’s for anyone who wants to make the most of what they have.

Whether you're a recent grad in Halifax navigating your first real paycheque, a growing family in Calgary juggling new expenses, or someone in Montreal starting to think about retirement, a plan helps you:

- Gain Control: Finally understand where your money is actually going every month.

- Reduce Stress: Stop guessing and start making financial decisions with confidence.

- Achieve Goals: Build a clear, actionable path toward your biggest life milestones.

- Build Security: Prepare for life’s curveballs and create a stable long-term future.

The good news is, modern tools like NeoSpend make it easier than ever to build and manage your own financial blueprint. By pulling all your accounts into one place and tracking your progress, NeoSpend helps turn those big financial goals from dreams into reality.

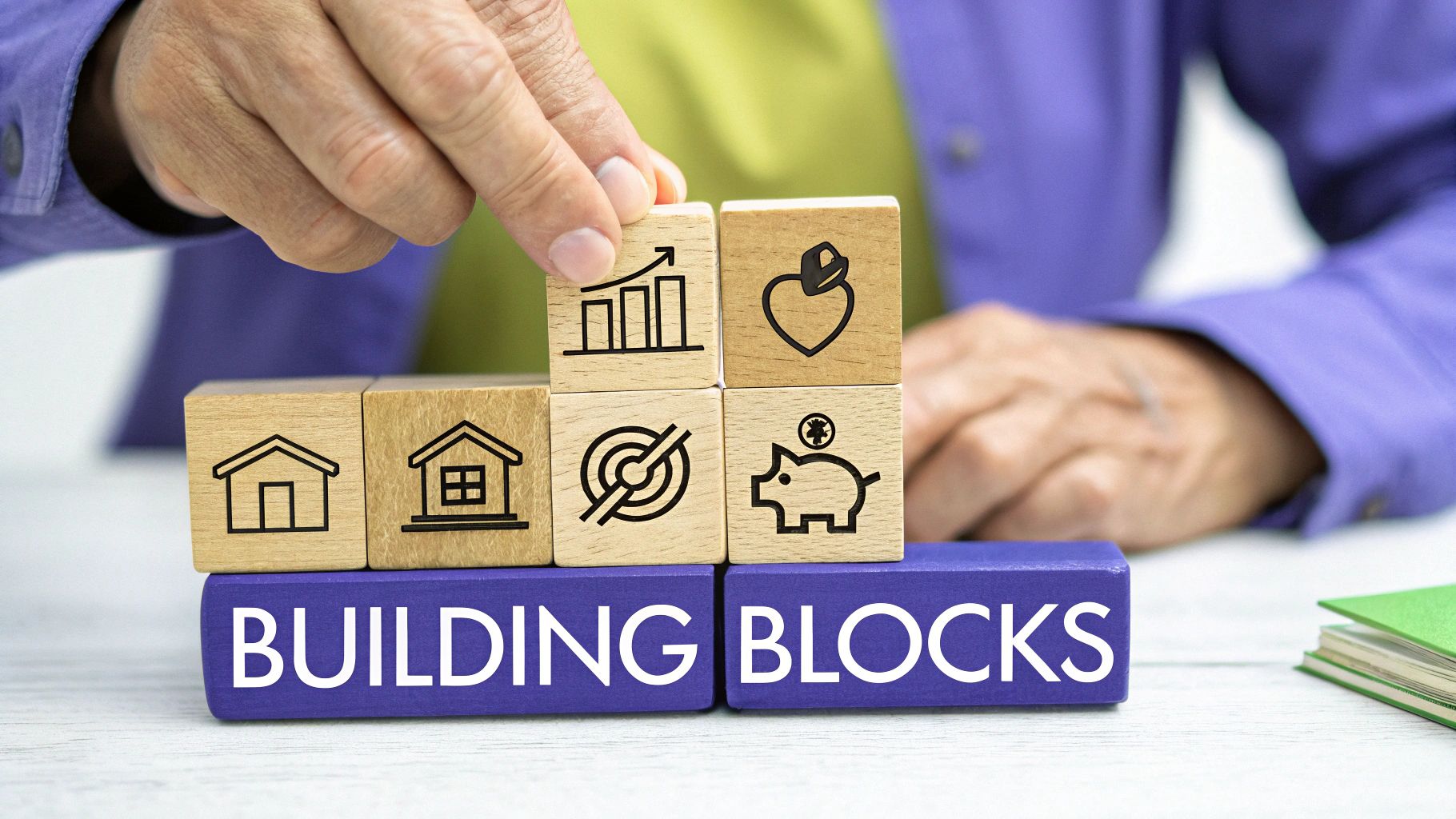

The Building Blocks Of a Solid Financial Plan

A solid financial plan isn’t some complicated, secret document. It’s more like a recipe, where every ingredient plays a crucial part. Once you understand these individual components—the building blocks—the whole idea of financial planning becomes a lot less intimidating. Each block supports the others, creating a sturdy foundation for everything you want to achieve.

Let’s break down the six pillars that create a complete and powerful financial picture for any Canadian.

The Six Pillars of Your Financial Plan

Every strong financial house is built on six core pillars. Miss one, and the whole structure can get wobbly. Nail all six, and you're building something that will last a lifetime.

| Pillar | What It Means for You | Your First Actionable Step |

|---|---|---|

| Cash Flow Management | Knowing exactly what money comes in and where it goes out each month. | Track your spending for 30 days using an app to see your real numbers. |

| Financial Goals | Defining what you're working toward, from a vacation to a down payment. | Write down one short-term (1-2 years) and one long-term (5+ years) money goal. |

| Debt Management | Creating a smart strategy to pay down what you owe, especially high-interest debt. | List all your debts, their interest rates, and minimum payments to see the full picture. |

| Investing | Making your money work for you to build wealth over the long haul. | Open a TFSA and set up a small, automatic monthly contribution. |

| Insurance & Protection | Shielding yourself and your family from life's unexpected financial shocks. | Review any insurance coverage you have through your employer to understand your baseline. |

| Retirement & Estate Planning | Ensuring you have enough to live comfortably when you stop working. | Check your latest RRSP statement to see where you stand. |

These aren't just separate tasks to check off a list; they're interconnected parts of a single, powerful strategy.

Pillar 1: Managing Your Cash Flow

This is ground zero. Your cash flow is simply the movement of money in and out of your life. It’s about getting crystal clear on what you earn versus what you spend. If you don't have a handle on your cash flow, setting realistic goals is pure guesswork.

For example, a software developer in Toronto needs to see her full picture—not just her salary, but her freelance income, set against real-world costs like rent, TTC passes, and student loan payments. That clarity is the first step to taking back control.

Pillar 2: Setting Meaningful Financial Goals

Your plan needs a destination. Without goals, you’re just saving money for the sake of it. Goals give your plan a purpose and turn vague wishes into real, achievable targets. They are the why behind every financial choice you make.

They can be short-term, like saving for a dream trip to Banff next winter, or bigger, like pulling together a down payment for a house in Calgary. The trick is to make them specific, measurable, and genuinely important to you.

A goal without a plan is just a wish. Financial planning turns your wishes into an actionable strategy by attaching real numbers and timelines to them.

Pillar 3: Handling Debt Strategically

Debt isn’t automatically a bad word. But when it’s unmanaged, it can derail your financial progress. A huge piece of any financial plan is having a smart strategy to manage and shrink your debts, especially high-interest kinds like credit cards.

This means you need to know what you’re working with—from credit cards and lines of credit to a mortgage or student loans. Figuring out which debts to attack first can save you thousands of dollars in interest and free up cash to pour into your other goals.

Pillar 4: Understanding Basic Investing

Saving is step one, but investing is how you put your money to work. This pillar is all about moving your savings into assets that can grow, helping you beat inflation and build real, long-term wealth. For most Canadians, the journey starts with our two main tax-advantaged accounts:

- Tax-Free Savings Account (TFSA): An incredibly flexible account where all your investment growth and withdrawals are 100% tax-free. It’s perfect for almost any goal.

- Registered Retirement Savings Plan (RRSP): Designed for your golden years. Your contributions are tax-deductible (which means a lower tax bill today), and your investments grow tax-deferred until you take the money out in retirement.

Pillar 5: Protecting Yourself With Insurance

Financial planning isn't all about offence; you need a good defence, too. Insurance is your financial safety net, built to protect you and your family from life’s curveballs. A single unexpected event could wipe out years of hard work. This pillar covers things like life, disability, and critical illness insurance. A solid plan is about both growing your wealth and protecting it.

Pillar 6: Planning For Retirement

Finally, all these other pieces come together to support the ultimate long-term goal: a retirement you can actually enjoy. This is all about figuring out what your future life will cost and building a roadmap to make sure you have the income to cover it when you stop working. It means making regular contributions to your RRSP, TFSA, and any workplace pension plan, and making investment choices that match your timeline.

How To Build Your First Financial Plan in 5 Steps

Knowing the building blocks is one thing, but actually putting them together to create your own financial roadmap is where the magic happens. Building your first financial plan can feel like a massive undertaking, but it's really just a series of small, manageable steps.

To make this practical, let’s follow the story of Alex, a recent graduate from Montreal who just landed their first full-time job. Alex is excited but also a bit overwhelmed by new responsibilities like student loans and figuring out how to save.

Step 1: Gather Your Financial Information

Before you can map out where you're going, you need to know exactly where you're starting from. This first step is all about gathering your key financial information in one place.

Alex sits down and pulls together:

- Recent pay stubs to see their net (after-tax) income.

- The last three months of bank statements.

- The latest statements for their Quebec student loan and credit card.

- Login information for the group RRSP their new employer set up.

Apps like NeoSpend simplify this part by securely connecting your accounts to automatically pull all your transactions and balances into a single dashboard, giving you a complete, real-time financial snapshot.

Step 2: Calculate Your Net Worth

This sounds more intimidating than it is. Your net worth is just a snapshot of your financial health: what you own (your assets) minus what you owe (your liabilities). Calculating it gives you a clear baseline to measure your progress against.

For Alex, the math is straightforward:

- Assets: Chequing ($1,500) + Savings ($3,000) + Work RRSP ($500) = $5,000

- Liabilities: Student Loan ($18,000) + Credit Card ($1,000) = $19,000

Alex’s net worth is $5,000 - $19,000 = -$14,000. Seeing a negative number might feel discouraging, but for a recent grad with student loans, it's completely normal! The important thing is that Alex now has a starting number to improve upon.

Step 3: Define Your Financial Goals

Now for the fun part: deciding where you want to go. Vague goals like "save more" are hard to act on. You need clear, specific, and achievable targets with a timeline.

Alex thinks about what’s most important and lands on three key goals:

- Short-Term (1-2 years): Build a $5,000 emergency fund to cover unexpected expenses.

- Mid-Term (3-5 years): Pay off that $1,000 high-interest credit card debt, then start saving $10,000 for a down payment on a future condo.

- Long-Term (10+ years): Consistently contribute to their RRSP to get the full employer match and get a head start on retirement.

Step 4: Create A Realistic Budget

Your budget is the engine of your financial plan. It’s the tool that directs your money toward your goals. The key is to create a budget that’s realistic and sustainable, not one so restrictive you ditch it after a month. A great starting point for many Canadians is the 50/30/20 rule.

The 50/30/20 rule is a simple framework: allocate 50% of your after-tax income to Needs (rent, groceries), 30% to Wants (dining out, hobbies), and 20% to Savings & Debt Repayment.

Using this guide, Alex maps out their monthly take-home pay of $3,500:

- Needs (50% = $1,750): Rent, hydro, groceries, transit pass, and minimum loan payments.

- Wants (30% = $1,050): Restaurants with friends, weekend trips, and subscriptions.

- Savings & Debt (20% = $700): Extra payments on the credit card, contributions to the emergency fund, and RRSP savings.

Suddenly, every dollar has a job.

Step 5: Build Your Action Plan

This is the final piece of the puzzle. It’s where you turn your budget and goals into a concrete to-do list.

Alex’s action plan is simple but powerful:

- Automate Savings: Set up an automatic transfer of $400 every month to a high-interest savings account for the emergency fund.

- Tackle Debt: Schedule an automatic payment of $300 per month to their credit card to clear the balance quickly.

- Invest for the Future: Ensure their payroll deduction for the RRSP is high enough to get every dollar of their employer’s matching contribution. It's free money!

Remember, a financial plan is a living document. Life will change—you’ll get a raise, move cities, or dream up new goals. Your plan should evolve right along with you.

Common Financial Planning Mistakes To Avoid

Knowing what to do is important, but knowing what not to do can save you from serious headaches. Many Canadians get tripped up by the same small group of mistakes. If you know what they are ahead of time, you can steer clear and keep your financial plan on track.

Getting Stuck in "Analysis Paralysis"

The single biggest mistake? Never actually starting. It’s easy to get bogged down by all the information out there, leading to analysis paralysis—that feeling you need to know everything before you can do anything. A simple, "good enough" plan you start today is infinitely better than a "perfect" plan you keep putting off.

Confusing Saving with Investing

People often use these terms interchangeably, but they play very different roles.

- Saving is stashing money in a safe, easy-to-access place (like a high-interest savings account) for short-term goals or emergencies.

- Investing is using your money to buy assets like stocks or funds to grow your wealth over the long term, which involves taking on some risk for a higher potential return. A Leafs fan saves for playoff tickets next spring but invests in their RRSP for retirement decades away.

Setting Wildly Unrealistic Goals

It’s great to be ambitious, but setting goals that are too aggressive is a fast track to burnout. If your budget is so tight there’s zero room for a single coffee out with a friend, you’re setting yourself up to fail. Your plan needs to work for your actual life. Instead of vowing to pay off a $20,000 student loan in one year on a modest income, a better goal might be to knock out $5,000. Hitting smaller targets builds momentum and confidence.

Skimping on Your Emergency Fund

Life happens. A surprise car repair or a sudden job loss can pop up when you least expect it. Without an emergency fund, these costs often go on a high-interest credit card, wrecking your progress. A solid rule of thumb is to have at least three to six months' worth of essential living expenses tucked away.

Your emergency fund isn't an investment; it's insurance. It’s the buffer standing between you and a financial crisis, protecting your long-term goals from short-term problems.

Letting High-Interest Debt Stick Around

Not all debt is created equal. A mortgage helps you build equity, but high-interest credit card debt does the exact opposite—it actively works against you. With interest rates often climbing past 20%, this kind of debt can snowball out of control. Making only the minimum payments is like trying to bail out a sinking boat with a teaspoon. A key part of any good plan is an aggressive strategy to crush this costly debt.

How NeoSpend Simplifies Your Financial Planning

Knowing the theory of financial planning is one thing, but actually putting it into practice can get messy. Juggling spreadsheets, remembering passwords for a half-dozen banking apps, and manually logging every purchase is often where good intentions fizzle out.

NeoSpend cuts through that complexity. Think of it as your financial command centre, turning the tedious work of managing money into a seamless, insightful process. By giving you one clear view of your entire financial world, NeoSpend helps you manage your money smarter.

See Your Full Financial Picture Instantly

The starting point for any good plan is knowing where you stand. NeoSpend delivers this clarity by securely pulling all your Canadian bank accounts, credit cards, loans, and investments into a single dashboard. No more bouncing between apps to check your chequing at CIBC, your TFSA at Wealthsimple, and your credit card at Scotiabank. You get a real-time overview of everything you own and owe, all in one spot.

Make Budgeting Effortless and Automatic

Let’s be honest: sticking to a budget is tough. NeoSpend tackles this with automatic transaction categorization. When you make a purchase, the app intelligently sorts it into categories like groceries, transit, or entertainment. Suddenly, you have a precise, up-to-the-minute breakdown of your spending habits without lifting a finger. This automation turns budgeting from a dreaded chore into a simple process that helps you make better decisions.

Stay Motivated With Clear Goal Tracking

A financial plan is fueled by your goals, but motivation can fade when progress feels slow. NeoSpend’s goal-tracking features are designed to keep you focused. Whether you're saving for a down payment on a home in Halifax or building an emergency fund, you can set up a specific goal in the app. NeoSpend helps you monitor your progress, visually showing you how your savings are stacking up.

Seeing your goals get closer every month provides a powerful psychological boost. It transforms saving from a sacrifice into an exciting journey toward a tangible reward.

Gain Control Over Your Debts and Bills

Managing debt is a huge piece of the financial puzzle. Canadian households often face unique debt challenges. Data from Statistics Canada, for example, shows that households aged 35-44 carry the highest debt service ratio. You can dig into the latest household financial statistics to learn more. NeoSpend gives you a consolidated view of all your debts—from student loans to credit cards—so you know exactly what you owe. The app also tracks recurring bills and sends you reminders, helping you dodge costly late fees.

Plan Confidently With Bank-Level Security

Handing over financial data requires trust. NeoSpend was built with security as its foundation. The app uses bank-level 256-bit encryption and connects to your accounts through a secure, read-only link. This means NeoSpend can display your financial information but never has the access or ability to move your money. We are committed to a strict privacy policy and will never sell your personal data.

Your Financial Planning Questions Answered

Even with the best roadmap, a few questions always pop up. We’ve pulled together the ones we hear most from Canadians to give you clear, no-nonsense answers.

Do I Need a Professional Financial Planner?

It depends. There’s no single right choice for everyone. A professional planner brings deep expertise for complex situations, like owning a business or managing intricate investments. They offer an objective viewpoint and can be a lifesaver when you’re navigating major life changes. On the flip side, going the DIY route gives you total control and is easier on the wallet. Tools like NeoSpend empower you to manage your own financial life by pulling all your accounts into one place, automating your budget, and tracking your goals—giving you the clarity to make smart moves on your own.

How Often Should I Review My Financial Plan?

Your financial plan shouldn't be a "set it and forget it" document. Think of it as a living guide that needs regular check-ins. A good rule of thumb is to sit down for a full review at least once a year. It’s the perfect time to see how you’re tracking against your goals and make sure your budget still makes sense. You’ll also want to review your plan after any major life event, like getting a new job, getting married, welcoming a child, or buying a home.

Is Financial Planning Only For Wealthy People?

Absolutely not. This is a common myth. Financial planning is for anyone who wants to be more intentional with their money, no matter their income. In fact, it’s arguably more critical when you're working with a modest income. A clear plan ensures every dollar is working as hard as you are to build security and help you get what you want out of life.

Financial planning isn't about how much money you have. It’s about creating a clear path for the money you do have, no matter the amount.

What Is the Difference Between a TFSA and an RRSP?

Getting a handle on the Tax-Free Savings Account (TFSA) and the Registered Retirement Savings Plan (RRSP) is a game-changer for Canadians. They both offer amazing tax advantages but work in different ways.

- TFSA (Tax-Free Savings Account): Think of this as your flexible powerhouse. You put in after-tax dollars, but all growth and withdrawals are 100% tax-free, forever. This makes it perfect for a huge range of goals, from a new car to supplementing your retirement.

- RRSP (Registered Retirement Savings Plan): This one is designed for retirement. You contribute with pre-tax dollars, which means you get a tax deduction now, lowering your tax bill for the year. Your money grows tax-deferred, and you only pay tax when you take it out in retirement—when you’re likely in a lower tax bracket.

The simple version? A TFSA gives you tax-free withdrawals later, while an RRSP gives you a tax break now. A solid financial plan for a Canadian will almost always use a combination of both.

Key Takeaway: Financial planning isn't about restricting your life; it's about empowering it. By creating a simple roadmap for your money, you reduce stress, gain control, and build a clear path to achieving your most important life goals. The best plan is one you can start today.

Ready to take control of your financial roadmap? NeoSpend simplifies everything by bringing your accounts, budgets, and goals into one easy-to-use app. Get the clarity you need to build your plan with confidence by visiting https://neospend.com to get started.