"Financial literacy" might sound like something from a stuffy economics textbook, but it's not about jargon or complex theories. It’s simply about understanding how to make your money work for you, so you can build the life you want with confidence and less stress.

What Is Financial Literacy, Really?

Think of financial literacy as learning your way around a new city. You wouldn't just start wandering aimlessly. You’d want a map (your budget), a sense of the local transit (like knowing the difference between a TFSA and an RRSP in Canada), and a clear destination (your goals, whether that’s a down payment on a condo or just feeling less anxious when the bills arrive).

It's the knowledge and skills you need to manage your money effectively. It’s having the confidence to handle whatever life throws at you, from soaring grocery prices in Vancouver to finally buying your first home in Halifax.

And let's be honest, many of us feel like we could use a better map. A staggering 60% of Canadians wish they were more financially literate. While most of us (86%) feel okay with day-to-day money management, that number drops to just 53% when it comes to understanding topics like investing. That's a huge gap between managing today and building for tomorrow. You can see the full story in a recent CIBC poll.

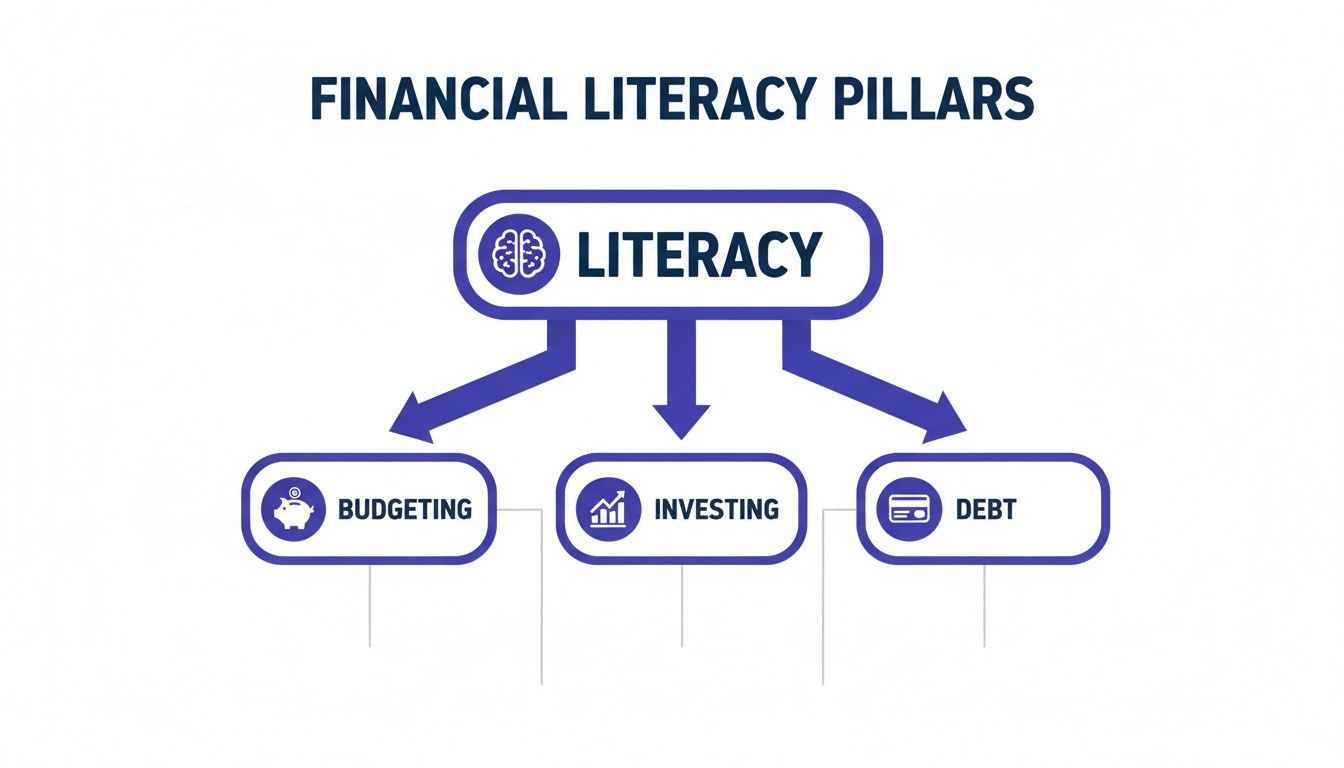

The Four Pillars of Financial Literacy

To make it less intimidating, let's break financial literacy down into four core areas. Getting a handle on these is the foundation for making smart money decisions.

| Pillar | What It Means for You | Everyday Canadian Example |

|---|---|---|

| Budgeting & Saving | Knowing what’s coming in and what’s going out. It’s the starting point for any financial goal. | Setting up an automatic transfer of $50 to your TFSA every payday before you can spend it. |

| Managing Debt | Understanding the difference between good debt (like a mortgage) and bad debt (like high-interest credit cards), and having a clear plan to pay it off. | Making more than the minimum payment on your credit card to crush that high-interest debt faster and save money. |

| Credit | Building and protecting your credit score so you can get approved for things like a mortgage or car loan with a better interest rate. | Checking your credit report for free once a year with Equifax or TransUnion to make sure there are no errors. |

| Investing | Making your money grow over time instead of just letting inflation eat away at its value in a chequing account. | Contributing to your company’s RRSP matching program to get the “free money” and build your retirement fund. |

Mastering these pillars isn’t about becoming a stock market expert overnight. It's about making small, consistent, and smart moves. The goal is to build a financial system that supports your life, not one that adds stress to it.

Why This Matters More Than Ever for Canadians

Every day, you make financial decisions—from your morning double-double to choosing a new cell phone plan. Without a solid understanding of your finances, it's easy to get sidetracked and make choices that don't align with your goals.

A lack of financial know-how can lead to some tough outcomes:

- Piling on Debt: Not understanding how credit card interest works can bury you in high-interest debt that feels impossible to escape.

- Constant Money Stress: Lying awake worrying about bills is draining. It takes a serious toll on your mental and physical health.

- Missing Out on Growth: Without a plan, you might miss huge opportunities to grow your wealth through smart saving or investing in tax-advantaged accounts like the TFSA.

This is where having the right tools makes a huge difference. An app like NeoSpend acts as your financial co-pilot. It takes the guesswork out of budgeting by showing you exactly where your money goes in real-time. It turns confusing bank statements into clear, simple insights, so you can spot where to save and stay on track with your goals, making your financial journey feel much more manageable.

Mastering Your Everyday Money Skills

Knowing the definition of financial literacy is one thing, but putting it into practice is where the real magic happens. This is how you build a solid financial foundation—not with complicated stock picks, but with simple, consistent daily habits. Mastering your everyday money skills means getting a handle on your cash flow so you can make deliberate choices that turn your income into a tool for building the life you want.

The bedrock of financial confidence comes down to budgeting, saving, and managing credit. These skills aren't about restricting yourself; they're about empowering yourself. When you know exactly where your money is going, you can finally direct it where you want it to go, whether that's a down payment on a home in Calgary or a stress-free trip to the East Coast.

Budgeting That Actually Works for Canadians

Forget complicated spreadsheets and tracking every single coffee. A modern budget is simply a plan for your money. Think of it as a roadmap that aligns your spending with your priorities, helping you avoid that end-of-month panic when you wonder where all your money went.

A good budget for a Canadian has to be flexible. Someone living in downtown Toronto with a monthly rent of $2,500 has a very different financial reality than someone in Saskatoon where rent might be closer to $1,400. The point is to create a plan that fits your life.

Here’s a simple, actionable way to start:

- Track Your Spending: For one month, get a clear picture of where your money is going. You don't need a notebook; technology can do the heavy lifting for you.

- Categorize and Analyze: Group your expenses into buckets like "Housing," "Groceries," "Transportation," and "Fun Money." This is where you’ll spot surprising spending patterns.

- Set Your Priorities: What matters most to you right now? Is it paying off student loans, saving for a car, or just building a safety net? Your budget should be built around those goals.

This is where a tool like NeoSpend becomes your secret weapon. It securely connects to your Canadian bank accounts and automatically sorts your transactions. The AI-powered dashboard shows you exactly where your money is going, so you can see if your daily Timmies run is actually costing you more than your hydro bill. It does the tedious work for you, so you can focus on making smarter money moves.

Saving with a Purpose

Saving money can feel like a chore until you give it a clear mission. Instead of vaguely saving "for the future," create specific, tangible goals. Suddenly, saving goes from being a chore to an exciting project.

In Canada, we have powerful, tax-advantaged accounts designed to help us hit our goals faster. Getting to know them is a key part of financial literacy.

A goal without a plan is just a wish. Your savings strategy is the plan that turns your financial dreams into reality by giving every dollar a specific job to do.

Consider these common Canadian savings goals:

- Emergency Fund: This is your financial safety net. Aim to save 3-6 months of essential living expenses in a high-interest savings account. It’s what keeps an unexpected car repair or job loss from derailing your long-term plans.

- First Home Purchase: The First Home Savings Account (FHSA) is a game-changer for aspiring homeowners in Canada. It combines the best features of an RRSP (tax-deductible contributions) and a TFSA (tax-free withdrawals for a home), giving your down payment a serious boost.

- Retirement: It might feel far away, but contributing to your Registered Retirement Savings Plan (RRSP) or Tax-Free Savings Account (TFSA) early is the single most effective way to build wealth over the long term.

NeoSpend helps you see your progress clearly. You can set up specific savings goals right in the app—like "Trip to Banff Fund"—and watch the progress bar fill up. That visual feedback is incredibly motivating and keeps you focused on the finish line.

Understanding Your Canadian Credit Score

Your credit score is one of the most important numbers in your financial life. It’s a three-digit score that tells lenders how reliable you are with borrowed money. In Canada, scores typically range from 300 to 900—the higher your score, the better your chances of getting approved for loans with lower interest rates.

It's not just for big things like mortgages. Landlords, insurance companies, and even some employers might look at your credit. Your score is calculated by Canada's two main credit bureaus, Equifax and TransUnion, based on a few key factors.

Here’s what goes into that all-important number:

- Payment History (Approx. 35%): This is the biggest factor. Always pay your bills on time. Even one late payment can cause your score to drop.

- Credit Utilization (Approx. 30%): This is how much of your available credit you're using. A good rule of thumb is to keep your balances below 30% of your limit on each credit card. Maxing out your cards can be a red flag for lenders.

- Length of Credit History (Approx. 15%): A long, positive credit history is beneficial. This is why it’s often a good idea to keep your oldest credit card account open, even if you don't use it much.

- Credit Mix (Approx. 10%): Lenders like to see that you can responsibly manage different types of credit, like a credit card, a car loan, and a line of credit.

- New Credit Inquiries (Approx. 10%): Applying for several new credit cards or loans in a short period can temporarily lower your score. Each application triggers a "hard inquiry" on your report.

Building good credit is a marathon, not a sprint. By consistently paying your bills on time and keeping your balances low, you’re building a strong financial reputation. NeoSpend can help by tracking your bills and subscriptions in one place and sending you smart alerts before due dates. It’s a simple feature, but it’s a powerful way to protect and build your credit score over time.

Growing Your Wealth Through Investing

Once you’ve mastered the day-to-day flow of your money, it's time to shift your focus from managing today to building for tomorrow. That’s where investing comes in. It’s all about putting your money to work for you, so it can grow and create more wealth over time.

For many Canadians, the world of investing feels like an exclusive club, full of confusing jargon and scary market predictions. But the core idea is simple. Think of it like planting a tree: you start with a small seed (your initial investment), and with time, patience, and the right conditions, it grows into something much larger.

The Power of Compound Interest

The magic behind investing is compound interest. This is the snowball effect of your money. Your investments earn a return, and then that return starts earning its own return.

Let's say you invest $1,000. If it earns a 7% return in one year, you have $1,070. But the next year, you’re not just earning 7% on your original $1,000—you’re earning it on the whole $1,070. It might not seem like much at first, but over decades, this is the single most powerful wealth-building tool you have. The earlier you start, the more time you give your money to work its magic.

Your Personal Investing Style

Before you start investing, it's important to figure out your risk tolerance. This is just a way of asking, "How comfortable are you with the stock market's natural ups and downs?" Your age, goals, and general comfort level with money all play a role.

- Low Risk Tolerance: If you’re saving for a down payment in two years, you’ll likely want safer, more stable investments. Protecting your initial investment is more important than chasing huge returns.

- High Risk Tolerance: If you’re in your 20s saving for retirement, you have decades to ride out market volatility. You can afford to be more comfortable with investments that have higher growth potential, like stocks, even if they are more volatile.

There’s no right or wrong answer. Financial literacy is about knowing yourself and making choices that let you sleep soundly at night.

Investing isn't about timing the market; it's about time in the market. The most important step is getting started, even with a small amount, to let the power of compounding begin its work.

Smart Investing Tools for Canadians

In Canada, we have special investment accounts that offer significant tax advantages. Getting to know them is a huge part of financial literacy. The two most common are the TFSA and the RRSP.

Tax-Free Savings Account (TFSA)

The TFSA is a flexible account where your investment growth is completely tax-free. You contribute with after-tax dollars, but you never pay tax on the interest, dividends, or capital gains you earn inside it.

- Best For: Short- to medium-term goals like buying a car, saving for a wedding, or a home down payment. It’s also a fantastic retirement tool, especially for lower-income earners.

- Example: You put $5,000 into your TFSA and invest it. It grows to $7,000 over five years. When you withdraw that money, the $2,000 profit is all yours, tax-free.

Registered Retirement Savings Plan (RRSP)

The RRSP is designed for retirement savings. Its main feature is that your contributions are tax-deductible, which means you can subtract the amount you contribute from your taxable income for the year, often resulting in a tax refund.

- Best For: Long-term retirement planning, especially for those in their peak earning years when the tax deduction is most valuable.

- Example: You earn $80,000 a year and contribute $5,000 to your RRSP. You’ll only be taxed on $75,000 of income that year. This could mean getting a significant tax refund in the spring.

See Your Entire Financial Picture

One of the biggest challenges with personal finance is that everything can feel disconnected. Your chequing account is with one bank, your TFSA is with a robo-advisor, and your RRSP is somewhere else. It’s hard to know if you’re on track when your money is scattered.

This is where seeing the whole picture is a game-changer. Tools like NeoSpend are built to solve this problem by bringing all your accounts—spending, saving, and investing—into one clear dashboard. By securely linking your different financial institutions, you can see your total net worth at a glance.

This big-picture view helps you connect the dots. You can see how your investment contributions are moving the needle on your long-term goals and make smarter, more informed decisions. It makes investing feel like an integrated part of your overall financial plan, turning knowledge into real, measurable progress.

Navigating Debt with Confidence

Debt can feel like a heavy weight, but learning how to manage it is one of the most empowering skills you can develop. Not all debt is created equal. Some debt, like a mortgage, can be a tool for building long-term wealth. Other kinds, like a credit card balance with a high interest rate, can hold you back. The key is to stop reacting to debt and start acting with a clear plan.

Good Debt vs. Bad Debt

First, it’s important to understand the difference between good and bad debt. A simple way to think about it is that good debt helps you acquire assets that can grow in value or increase your earning potential, while bad debt is typically used for things that lose value and comes with high interest costs.

- Good Debt Examples: A mortgage on a home, a student loan that leads to a higher-paying career, or a loan to start a business. These are investments in your future.

- Bad Debt Examples: High-interest credit card balances from everyday spending, payday loans, or financing a new car that depreciates the moment you drive it off the lot.

Making this distinction is critical. It helps you prioritize what to pay off first. The goal isn't necessarily a zero-debt life; it's about using debt strategically and eliminating the expensive "bad" debt that drains your finances.

Proven Strategies for Paying Down Debt in Canada

Once you've identified which debts to target, it's time to choose your repayment strategy. Two of the most popular and effective methods for Canadians are the debt avalanche and the debt snowball.

- The Debt Avalanche: This method is purely mathematical. You make minimum payments on all your debts but put every extra dollar towards the debt with the highest interest rate. This approach saves you the most money on interest over time and helps you get out of debt faster.

- The Debt Snowball: This strategy is based on psychology and motivation. You focus on paying off the smallest debt first, regardless of the interest rate. Once that's paid off, you "roll" that payment amount onto the next-smallest debt. The quick wins build momentum and keep you motivated.

The best debt repayment strategy is the one you’ll actually stick with. Whether you prefer the math of the avalanche or the motivation of the snowball, consistency is the key to reaching the finish line.

Taking Control with Smarter Tools

Juggling due dates for credit cards, student loans, and lines of credit can be overwhelming. Household debt is a major issue in Canada, with Canadians owing nearly $1.75 for every dollar of disposable income. What's worse, many of us don't fully understand the terms of our loans, meaning we often underestimate their true cost. You can learn more about these findings on financial literacy from the FCAC.

This is where technology can help. A tool like NeoSpend simplifies everything by putting all your bills and subscriptions in one clear dashboard. By securely syncing your accounts, it can help you:

- Track Due Dates: NeoSpend sends smart alerts before your bills are due, helping you avoid painful late fees and protect your credit score.

- Spot Savings Opportunities: The app’s AI analyzes your spending patterns and identifies areas where you could cut back, freeing up more cash to put toward your debt.

- Monitor Subscriptions: It also tracks all your recurring charges, making it easy to cancel services you forgot about and redirect that money to your financial goals.

By automating the tedious parts of debt management, NeoSpend lets you focus on what really matters: executing your plan, paying down your balances, and building a more secure financial future.

How to Improve Your Financial Literacy Today

Getting smarter with your money isn't about memorizing financial jargon. It’s about taking small, practical steps that build your confidence over time. The journey starts with an honest look at your own habits to see which skills could use a little attention.

Think of it like learning to cook. You wouldn't try to make a five-course meal on day one. You'd start by learning how to chop vegetables or follow a simple recipe. The same principle applies to your finances—master one small thing at a time, and you'll build momentum for bigger wins.

Start With a Simple Self-Assessment

Before you dive into finance podcasts or blogs, take a moment to see where you stand. Ask yourself a few simple questions to identify your strengths and areas for improvement.

- Budgeting: Do I know where my money goes each month, or is my bank balance always a surprise?

- Saving: Do I have an emergency fund? Am I putting money away for specific goals?

- Debt: Do I have a clear plan to pay off high-interest debt, like my credit card balance?

- Investing: Is my money working for me in accounts like a TFSA or RRSP, or is it just sitting in a chequing account?

It’s perfectly fine if your answer is "I'm not sure" to any of these. That’s a great starting point, because now you know exactly what to focus on first.

Financial progress starts with awareness. You can't improve what you don't measure, and a quick personal check-in is the first step toward building a stronger financial life.

Find Your Go-To Canadian Learning Resources

Once you’ve identified what you want to work on, it's time to find trustworthy information. The good news is there are more high-quality, free Canadian resources available than ever before.

For many Canadians, especially younger ones, the biggest hurdle is feeling overwhelmed and not knowing where to begin. Studies show that while 88% of us know that budgeting would reduce financial stress, 49% of people aged 18-34 don't know where to turn for reliable advice. This is exactly where great tools and resources can help. Learn more about the barriers Canadians face from the 2025 Financial Stress Index.

Build your personal finance toolkit with resources like:

- Trusted Blogs and Websites: Look for Canadian-focused personal finance blogs that explain concepts simply.

- Engaging Podcasts: Find a show that discusses money in a way that resonates with you for your commute or workout.

- Government Tools: The Financial Consumer Agency of Canada (FCAC) offers unbiased calculators, guides, and resources that are genuinely helpful.

Turn Knowledge Into Action With Technology

Reading about financial literacy is one thing, but actually doing it is another. This is where the right technology can be a game-changer, helping you apply what you've learned to your real life.

Instead of just showing you numbers, an app like NeoSpend acts as your personal finance coach. Its AI-powered insights don't just present data; they teach you about your own spending habits in real time.

By automatically categorizing where your money goes, showing you how close you are to your goals, and giving you personalized tips, NeoSpend helps you connect the dots between your daily decisions and your long-term ambitions. It turns passive knowledge into active skill-building, one transaction at a time.

A Final, Helpful Takeaway

Financial literacy isn't an intimidating, all-or-nothing test. It's the ongoing practice of making informed and effective decisions with your money. When you understand the four pillars—budgeting, saving, investing, and managing debt—you transform money from a source of stress into a tool for building the life you want. It all begins with small, consistent actions that build confidence and lead to significant long-term success.

The most important first step is simply getting a clear, honest picture of where you stand today.

We know it's one thing to read about all this, and another to actually do it. That's why we built a tool to help you connect the dots. NeoSpend gives you an intelligent, secure way to see your entire financial picture, all in one place, so you can stop guessing and start tracking your progress for real.

Once you connect your accounts, you can see where every dollar is going, spot opportunities to save, and manage your bills without the constant anxiety. NeoSpend is designed to help you apply what you're learning in real-time, turning knowledge into confident action.

Ready to take that first step toward mastering your money? See how NeoSpend can help you manage your money smarter, and explore our other articles to continue building your financial skills.

Your Top Financial Literacy Questions, Answered

Even with the fundamentals down, it's natural to have a few more questions. Here are answers to some of the most common ones we hear from Canadians.

How Long Does It Take to Become Financially Literate?

Financial literacy is a journey, not a destination. You can start feeling more in control and making smarter choices within just a few weeks by focusing on one skill at a time, like creating your first budget or setting up a plan to tackle credit card debt.

True mastery, however, is a lifelong practice. Think of it like fitness—you don't just work out for a month and then stop. It’s about building healthy, sustainable habits that support you as your life and financial goals evolve over time.

Do I Need a Lot of Money to Start Investing?

Absolutely not. This is one of the biggest myths holding Canadians back. You can open an investment account like a TFSA or RRSP with many robo-advisors or banks for as little as $25.

The most powerful ingredient for investment growth isn't a large initial sum; it's time. By starting early, even with small, consistent contributions, you allow the magic of compounding to work for you. Over the years, those small contributions can grow into something truly significant. The most important step is simply to start.

Is It Better to Pay Off Debt or Save Money?

This is a classic financial dilemma, and the answer usually comes down to simple math: comparing interest rates.

Most financial experts in Canada agree that you should prioritize paying off any high-interest debt first. This includes things like credit card balances, which often have interest rates of 19.99% or higher. This type of debt actively works against your financial progress.

A great rule of thumb for Canadians is to compare the interest rate on your debt to the potential return you'd get from investing. If your debt's interest rate is higher (and with credit cards, it almost always is), paying it off is your guaranteed best return on investment.

However, you shouldn't put saving completely on hold. While you tackle high-interest debt, try to build a small emergency fund. Having even $1,000 saved can prevent a minor unexpected expense from forcing you into more debt. Once the expensive debt is gone, you can direct that extra cash flow toward your bigger savings and investment goals.

How Can an App Actually Help Me Improve My Financial Literacy?

It's a fair question. Reading articles provides knowledge, but an app like NeoSpend is designed for action. It bridges the gap between knowing what you should do and actually doing it.

Instead of just telling you to make a budget, it connects to your accounts and shows you exactly where every dollar went last month. Rather than just explaining the concept of a savings goal, it lets you create one, name it, and watch your progress in real-time.

It transforms financial management from a passive chore into an interactive experience based on your own life. With smart alerts and personalized insights, you start to see the direct connection between your daily habits and your future goals, building real financial skill with every transaction you make.

Ready to turn knowledge into action? Try NeoSpend today to get a clear, intelligent view of your entire financial world and start managing your money smarter. Explore more at https://neospend.com.