Think of a Tax-Free Savings Account (TFSA) as a powerful financial tool for any Canadian looking to grow their money. In a nutshell, it's a special savings and investment account where whatever you earn—interest, dividends, or capital gains—is completely tax-free. That’s right. The government doesn’t take a cent, even when you withdraw your money.

More Than Just a Savings Account

It’s easy to get tripped up by the name. The "Savings Account" part is a bit misleading because a TFSA is so much more. The best way to picture it is as a special basket you can fill with all sorts of different investments.

What goes inside that basket is entirely up to you. You could keep it simple with cash, but the real power comes from filling it with assets that grow over time, like:

- Guaranteed Investment Certificates (GICs) for safe, predictable returns.

- Mutual funds and ETFs to get diversified growth without having to pick individual stocks.

- Individual stocks and bonds if you’re aiming for higher potential returns.

The magic is that everything happening inside this basket is shielded from taxes. Forever. This tax-free environment lets your money compound much faster, helping you reach your financial goals sooner.

Key Takeaway: The TFSA isn't an investment on its own. It's a registered account that acts as a tax shelter for the investments you hold within it. This tax-free growth is its biggest superpower.

For a quick overview, here are the core features of a TFSA.

TFSA Key Features at a Glance

This table breaks down the essentials of what makes a TFSA such a valuable tool for Canadians.

| Feature | Description |

|---|---|

| Tax-Free Growth | All investment income (interest, dividends, capital gains) earned inside the account is never taxed. |

| Tax-Free Withdrawals | You can take money out at any time, for any reason, without paying any tax on the withdrawal. |

| Contribution Room | The government sets an annual limit. Unused room carries forward indefinitely to future years. |

| Re-Contribution | Any amount you withdraw is added back to your contribution room starting the next calendar year. |

| Eligibility | Available to Canadian residents aged 18 or older with a valid Social Insurance Number (SIN). |

| Investment Options | Holds a wide range of investments, including cash, GICs, stocks, bonds, mutual funds, and ETFs. |

These features combined make the TFSA an incredibly flexible and powerful account for nearly any financial goal.

A Flexible Tool for Every Goal

This unique blend of tax-free growth and flexibility makes the TFSA a perfect fit for almost any financial plan. Let's say you're saving for a down payment on a condo in Toronto, planning a dream trip to the Rockies, building an emergency fund, or saving for retirement—a TFSA can help you get there faster.

Since its launch back in 2009, the TFSA has become a cornerstone of personal finance in Canada. By the end of 2022, nearly 18 million Canadians held TFSAs, with the total assets sitting around a whopping $519 billion. That says a lot about its value. You can dig into more TFSA statistics on the Government of Canada website.

Of course, making the most of this account means keeping track of it. This is where tools like NeoSpend help you manage your money smarter. It lets you connect all your accounts, including your TFSA, so you get a single, clear view of your entire financial world and can track your progress without any hassle.

Who Can Open a TFSA in Canada?

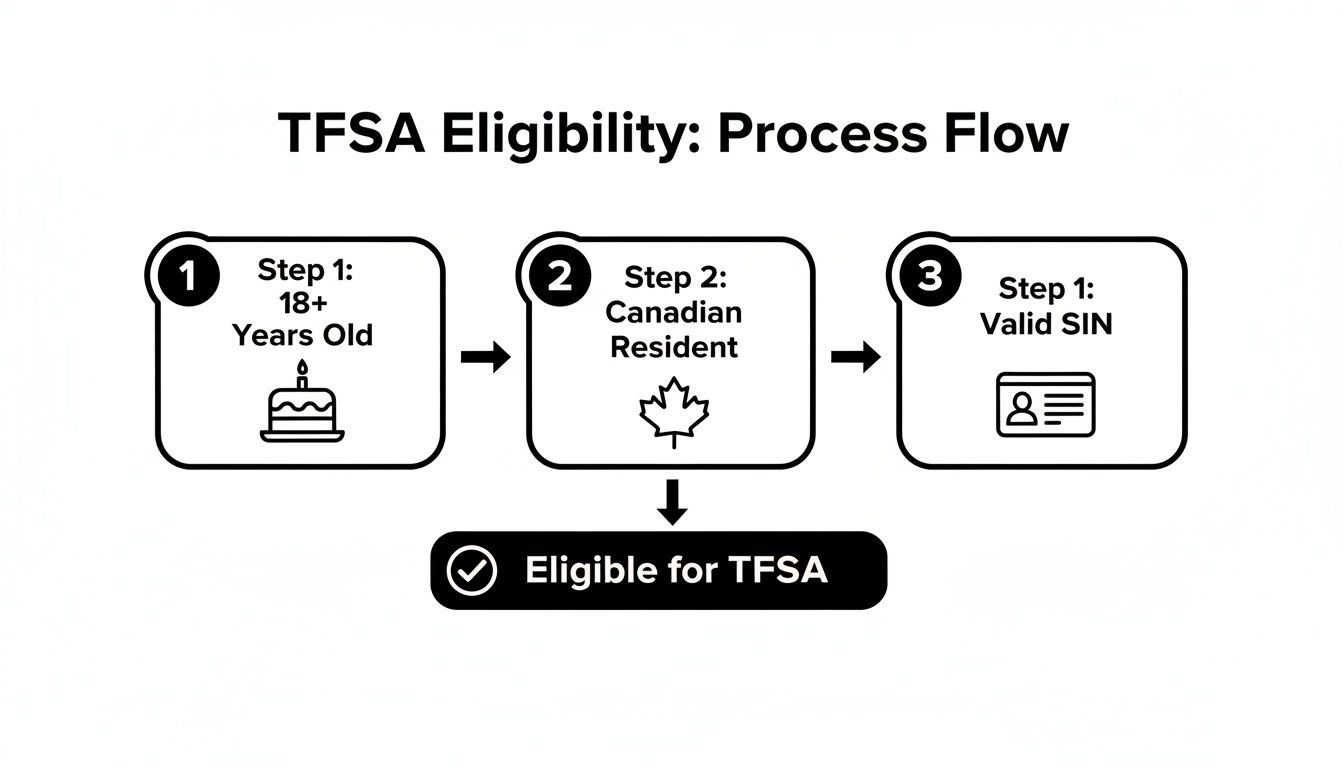

The Tax-Free Savings Account is one of the most popular investment tools for Canadians, but you need to check a few boxes before you can start. The good news is, the eligibility rules are simple and designed to let most adult residents in Canada get in on that tax-free growth.

To open and contribute to a TFSA, you just have to meet three basic criteria set by the Canada Revenue Agency (CRA). Think of them as the three keys you need to unlock the account.

The Three Core Eligibility Rules

These rules are non-negotiable, and any financial institution will confirm them before opening a TFSA for you.

You must be 18 or older. Your TFSA journey officially begins the year you turn 18, and your contribution room starts building up from that point on—even if you don't open an account right away.

You need a valid Social Insurance Number (SIN). To open any registered account in Canada, including a TFSA, you need a valid SIN. It’s how the government tracks your contributions.

You must be a Canadian resident. Specifically, a resident of Canada for tax purposes. While someone who isn't a resident can technically hold a TFSA, they can't contribute. If they do, they'll be hit with a penalty tax of 1% per month on anything they put in while living abroad.

Here’s an important point: There’s no income requirement to open a TFSA. This makes it an amazing tool for students, retirees, or anyone who isn't earning an income but has some savings they want to grow tax-free.

Once you’ve confirmed you meet these three conditions, you’re ready to start. And if you’re worried about keeping track of a new TFSA on top of everything else, a tool like NeoSpend can help by pulling all your financial accounts into one clean view.

Understanding Your TFSA Contribution Room

One of the best features of a TFSA is its contribution room—the total amount you're allowed to put into your account. Think of it as a financial backpack that gets bigger every year. The government adds more space annually, giving you more room to shelter your investments from taxes.

This room starts building up the year you turn 18, and it keeps growing whether you’ve opened a TFSA or not. The real magic is that any space you don't use simply carries forward to the next year. So, if you can’t contribute one year, that room isn't lost. It just waits for you.

How Contribution Room Carries Forward

Let’s look at a real-world Canadian scenario. Imagine Maya, from Calgary, who turned 18 when the annual TFSA limit was $6,000. She was focused on school and didn't open an account. The next year, the limit was $6,500.

- Year 1: Maya gained $6,000 in contribution room but put in $0.

- Year 2: That unused $6,000 carried over, and she gained another $6,500 in new room.

- Total Room: Suddenly, Maya has a total of $12,500 ($6,000 + $6,500) available to her.

This carry-forward system is incredibly forgiving. The annual limit does change; it started at $5,000 back in 2009, and for 2024, it’s $7,000. If you've been eligible since day one, your total cumulative room could be as high as $95,000 as of 2024. You can always check the history of the annual limits to see how it all adds up.

This infographic shows just how simple it is to start accumulating your TFSA room.

As you can see, hitting these three basic milestones is all it takes. Once you do, your tax-free savings potential starts growing every year.

How to Check Your Official TFSA Contribution Limit

While you can try to track your contributions on your own, there's only one source of truth: the Canada Revenue Agency (CRA). Your bank only knows what you’ve put in with them, but the CRA sees the whole picture across all your accounts.

To get the official number for your TFSA contribution room, you must log in to your CRA My Account. This is the only number that matters, and checking it is the best way to avoid over-contributing. Getting it wrong is costly—the penalty is a steep 1% per month on the excess amount.

Keeping an eye on this limit is crucial. An app like NeoSpend can be a great sidekick, helping you consolidate your financial accounts to see where your money is going. This makes it much easier to track what you're contributing alongside the official numbers you get from the CRA.

Choosing the Right Investments for Your TFSA

A common mistake Canadians make is treating their TFSA like a regular savings account. They let cash pile up, earning very little interest. While it’s better than no savings at all, this misses the point of what a TFSA can do for you.

Think of it less like a piggy bank and more like a high-performance investment vehicle. The real power of a TFSA is unleashed when you fill it with assets that can grow, because all that growth is 100% tax-free. What you put inside this powerful container is what will determine how fast your money compounds.

It all comes down to aligning your investments with your financial goals, your timeline, and how much risk you can handle.

Investments for Cautious Savers

If your main goal is to keep your original investment safe while earning a predictable return, you’ll want to stick to the basics. These options are perfect if you’re saving for a short-term goal, like a down payment on a house in the next year or two.

Guaranteed Investment Certificates (GICs): A GIC is exactly what it sounds like—guaranteed. You lock in your money for a set period, from a few months to several years, and in return, you get a fixed interest rate. Your initial investment is safe.

High-Interest Savings Accounts (HISAs): Yes, you can hold a HISA inside a TFSA. It gives you a much better interest rate than a standard savings account, but your money is still accessible when you need it.

These won't make you rich overnight, but they offer stability and peace of mind.

Investments for Balanced Growth

If you have a bit more time—say, five years or more—and you’re okay with some market fluctuation, then a balanced, diversified approach is probably your sweet spot. The goal here is to capture market growth while smoothing out the bumps along the way.

Key Insight: The secret to long-term success is rarely about picking one winning stock. It's about spreading your money across different types of assets so you're not putting all your eggs in one basket.

One of the best tools for this is an Exchange-Traded Fund (ETF). An ETF is like a basket that holds hundreds or even thousands of different stocks or bonds. With a single purchase, you can own a tiny piece of the entire Canadian or U.S. stock market. It’s instant diversification at a very low cost.

Investments for Higher Growth Potential

If you're investing for a long-term goal like retirement and you have a higher tolerance for risk, you might consider buying individual stocks. When you buy a stock, you're buying a small ownership slice of a specific company. This approach offers the highest potential for growth, but it also comes with the highest risk.

No matter which path you choose, you can't manage what you don't measure. This is where NeoSpend is a valuable partner. It brings all your accounts, including your TFSA, into one clean dashboard, making it easier to track how your investments are performing and ensure you're on course to hit your financial goals.

TFSA vs. RRSP: Which Is Better for Your Goals?

In Canadian personal finance, the TFSA vs. RRSP debate is a classic. Both are fantastic tools for building wealth, but they work in completely different ways. Figuring out which one is right for you comes down to your income, your goals, and when you plan to use the money.

Think of it this way: a Registered Retirement Savings Plan (RRSP) gives you a tax break right now. Every dollar you contribute is tax-deductible, which lowers your taxable income for the year. The catch? You pay income tax on everything you take out later, hopefully in retirement when you're in a lower tax bracket.

The TFSA flips that script. You contribute with money you've already paid tax on (no upfront deduction), but every penny of growth and every withdrawal is completely tax-free.

Key Differences at a Glance

So, how do you choose? Seeing them side-by-side helps. This comparison breaks down the core features of each account to help you match your savings strategy with your financial reality.

Comparing TFSA and RRSP Features

| Feature | TFSA (Tax-Free Savings Account) | RRSP (Registered Retirement Savings Plan) |

|---|---|---|

| Tax on Contributions | None. You contribute with after-tax money. | Tax-deductible. Contributions reduce your taxable income. |

| Tax on Growth | Tax-Free. All investment gains are yours to keep. | Tax-Deferred. Growth is tax-sheltered until withdrawal. |

| Tax on Withdrawals | Tax-Free. You can take money out anytime, for any reason. | Taxable. Withdrawals are taxed as regular income. |

| Withdrawal Impact | None. Withdrawals don't affect government benefits. | Can impact benefits like OAS and GIS. |

| Re-Contribution | Room is added back the following calendar year. | Room is permanently lost after withdrawal (except for HBP/LLP). |

| Primary Use Case | Flexible for any goal (short-term, long-term, retirement). | Primarily for long-term retirement savings. |

This table lays out the technical differences, but the real decision comes down to your life circumstances.

When a TFSA Is Often the Better Choice

For many Canadians, especially if you're early in your career or in a lower income bracket, the TFSA is usually the smarter first move. If you think you'll be earning more (and paying more in taxes) down the road, it makes sense to save your RRSP deduction for those higher-earning years when it will have a bigger impact.

A TFSA is ideal for short-term goals like saving for a car or a house down payment. The ability to withdraw funds tax-free without penalty gives you incredible flexibility that an RRSP can't match.

The TFSA isn't just for young people. In 2023, about 7.5 million Canadians put money into a TFSA, from young adults to seniors. What's telling is that half of these contributors had incomes under $60,000, which proves its value for everyday Canadians who benefit more from tax-free growth than an immediate tax deduction. You can find more insights about TFSA usage across Canada.

When an RRSP Might Be the Winner

On the other hand, an RRSP really starts to shine when you're in your peak earning years. If you're in a high tax bracket now, the immediate tax deduction from an RRSP contribution is a powerful tool that can lead to a significant tax refund.

The strategy is to contribute when your income is high and withdraw in retirement when your income (and therefore your tax rate) is likely much lower. That difference in tax rates is the magic of the RRSP.

In the end, you don’t have to pick just one. Most savvy Canadians use both a TFSA and an RRSP. A tool like NeoSpend can help you see your contributions to both accounts in one spot, making it easier to manage your overall savings strategy.

Getting Your TFSA Started and Keeping It on Track with NeoSpend

Ready to start your tax-free growth journey? Opening a TFSA is easier than you might think. Just about every bank, credit union, and online brokerage in Canada offers them.

All you really need to get started is some basic personal info and your Social Insurance Number (SIN).

Your Step-by-Step Guide to Opening a TFSA

Getting your account up and running is a quick process. Here’s how it usually works:

- Choose Your Institution: First, decide where to open your account. Are you looking for a simple high-interest savings TFSA at your bank, or do you want a self-directed investment TFSA from a brokerage?

- Gather Your Documents: You’ll need your SIN and a piece of government-issued ID, like a driver’s licence or passport.

- Complete the Application: Most applications are online and only take a few minutes. You’ll just fill out a form with your personal details.

- Fund Your Account: Once your account is open, you can transfer money in and start saving or investing immediately. It’s that simple.

Simplify Your Financial Life with NeoSpend

Opening a TFSA is a great first step, but managing it well is what really counts. That’s where NeoSpend comes in—think of it as your financial command centre. Instead of juggling different apps, you can link your new TFSA, bank accounts, and credit cards all into one clean dashboard.

With NeoSpend, you get a complete, real-time look at your entire financial world. This bird's-eye view helps you see exactly how your TFSA contributions fit into your bigger budget and savings goals.

Our tools make it easy to see how you're doing. You can watch your investments grow, set savings goals to consistently build up your TFSA balance, and check how close you are to maxing out its tax-free potential. By bringing your whole financial life into one place, NeoSpend helps you stay organized, motivated, and on track.

Your Top TFSA Questions, Answered

Once you get the hang of TFSAs, a few specific questions almost always come up. Knowing the answers is key to managing your account like a pro and avoiding simple, yet costly, mistakes.

Let’s answer the questions we hear all the time.

What happens if I over-contribute to my TFSA?

This is a big one. If you contribute more than your available room, the Canada Revenue Agency (CRA) will charge a penalty tax. It’s a steep 1% per month on the highest excess amount.

To stop the penalty, you have to withdraw the extra cash right away. The best way to handle this is to avoid it altogether. Before you deposit money, log into your CRA My Account online and check your official contribution room. It's the only way to be 100% sure.

Can I have more than one TFSA?

Yes. You can open as many TFSA accounts as you want across different financial institutions. You might want one at your bank for a GIC and another with an online broker to trade ETFs. That's totally fine.

But here’s the catch: your contribution limit is a single, combined total for all of your accounts. It's not a separate limit for each one. That means it’s on you to track every dollar you put in across all your accounts.

Pro Tip: Juggling multiple accounts can be a headache. Using an app like NeoSpend lets you link all your TFSAs into one dashboard. You get a clear view of your total contributions, which helps you stay organized and on track.

Do I lose my contribution room if I take money out?

No, you don't lose the room permanently, but timing is key. Any amount you withdraw from your TFSA gets added back to your contribution room—but not until January 1st of the next year.

For example, if you take out $5,000 in July to fix your car, that $5,000 of contribution room is "returned" to you, but you have to wait until the new year to use it again. If you're already maxed out for the year and try to put that $5,000 back in October, you'll trigger an over-contribution penalty.

Is my TFSA money guaranteed to be safe?

The safety of your money depends entirely on what you’re holding inside your TFSA. Think of the TFSA as a container; what matters is what you put in it.

- Cash and GICs held at a Canada Deposit Insurance Corporation (CDIC) member institution are generally protected. If the bank fails, your deposits are insured up to $100,000.

- Investments like stocks, ETFs, and mutual funds are different. They are not insured against market ups and downs. Their value can fall, and you could lose money. That’s the risk you take for the potential of higher growth.

Your Takeaway: A TFSA is one of the most powerful tools available to Canadians for building tax-free wealth. By understanding the rules and choosing investments that match your goals, you can make your money work harder for you. Ready to stop guessing and start managing your savings with real clarity? NeoSpend pulls all your accounts into one simple view, making it effortless to track your TFSA, see your progress, and build wealth the smart way. Try NeoSpend today and finally see your full financial picture.