A Spousal RRSP is a smart retirement savings strategy designed for Canadian couples, especially when one partner earns significantly more than the other.

Here’s the simple version: the higher-earning spouse contributes to a Registered Retirement Savings Plan (RRSP) that is set up in the lower-earning spouse’s name. The person who contributes the money gets the immediate tax deduction, but the funds grow in an account owned by their partner.

The main goal is to balance out your retirement incomes down the road. This teamwork approach, known as income splitting, can significantly lower your family's overall tax bill in retirement.

Unlocking a Smarter Retirement Strategy for Couples

Let’s use an everyday Canadian scenario. Imagine you and your partner each have a bucket to fill for retirement. If you're a high-income earner, your bucket might be overflowing, pushing you into a high tax bracket now and, eventually, in retirement. Meanwhile, your partner’s bucket may have more room, perhaps because they earn less or took time off work to raise your family.

A Spousal RRSP lets you pour some of your savings directly into your partner's bucket. It's a simple act of financial teamwork that leads to a much more tax-efficient retirement for your household.

The end game is to split your future retirement income more evenly. When it's time to withdraw your savings, drawing from two balanced accounts instead of one massive one means you’ll likely pay a lot less tax to the Canada Revenue Agency (CRA). We're talking about potentially thousands of dollars in tax savings over your retirement years.

The Two Key Roles in a Spousal RRSP

To understand how a Spousal RRSP works, it’s essential to know the two people involved. The CRA has clear definitions for these roles:

- The Contributor: This is the spouse or common-law partner who puts money into the account. They use their own RRSP contribution room and get the tax deduction on their income tax return.

- The Annuitant: This is the spouse or common-law partner whose name is on the account. They are the legal owner of the account and all the investments inside it. The contributions made by their partner do not affect their personal RRSP contribution limit.

So, the contributor gets the short-term win (a tax break now), while the annuitant owns the long-term retirement asset.

This strategy really shines when there's a significant income gap between partners. By shifting future retirement income—and the associated tax—to the lower-income spouse, you effectively lower your combined tax bill when you finally start enjoying your savings.

To help you see the difference more clearly, here’s a quick breakdown.

Spousal RRSP vs. Individual RRSP: What's the Difference?

This table highlights the fundamental differences between a regular RRSP and a Spousal RRSP to clarify roles and benefits.

| Feature | Individual RRSP | Spousal RRSP |

|---|---|---|

| Account Owner (Annuitant) | You | Your spouse/partner |

| Who Contributes? | You | You (the contributor) |

| Whose Contribution Room is Used? | Yours | Yours (the contributor's) |

| Who Gets the Tax Deduction? | You | You (the contributor) |

| Who Owns the Investments? | You | Your spouse/partner |

| Who is Taxed on Withdrawals? | You | Your spouse/partner (after the 3-year attribution period) |

This side-by-side view makes it clear: with a Spousal RRSP, you're using your contribution room to build your partner's nest egg, all while getting a tax break for yourself.

Managing these contributions requires planning. The contributing spouse needs to know their available contribution room and budget accordingly. Keeping a close eye on your finances with a tool like NeoSpend can be a huge help. It helps you track your spending and see where you can free up cash for retirement savings, giving you a clear picture of your financial future and helping you manage your money smarter.

How Spousal RRSP Contributions and Tax Deductions Work

So, how does the money get into the account and who gets the tax break? This is where the real power of a Spousal RRSP comes into play, and it’s surprisingly straightforward. The higher-income spouse makes the contribution, but it uses up their own RRSP contribution room—not their partner's.

That’s a key point. The spouse who owns the account (the annuitant) doesn’t need any of their own contribution room. The entire strategy depends on the contributor's available deduction limit, which you can find on your latest Notice of Assessment from the CRA.

The Immediate Power of the Tax Deduction

The biggest and most immediate benefit of a Spousal RRSP is the tax deduction for the person putting the money in. Since the contributor is usually in a higher tax bracket, their deduction results in a much larger tax refund than if the lower-income spouse had contributed the same amount to their own RRSP.

It's a seriously smart tax-planning move for any Canadian couple with a significant income gap. For instance, with the maximum RRSP contribution limit for 2024 at $31,560, a higher earner could direct that entire amount into their partner's Spousal RRSP. This is a huge advantage in Canada's progressive tax system, where every extra dollar you earn is taxed at a higher rate. This strategy is popular for a reason—3.8 million Canadians contribute to RRSPs, with a median contribution of $3,420. You can find more Canadian financial planning insights on theseanwhitegroup.ca.

The bottom line is you get more cash back from the government right away, which you can reinvest or use for other financial goals.

A Real-World Canadian Example

Let's break it down with an everyday Canadian scenario to see how it works.

- Meet Liam and Chloe: Liam is a software developer in Calgary earning $150,000 a year, putting him in a high tax bracket. His partner, Chloe, is a freelance artist earning $45,000, placing her in a much lower bracket.

- The Contribution: Liam has plenty of RRSP contribution room. He decides to contribute $10,000 into a Spousal RRSP for Chloe.

- The Tax Deduction: When he files his taxes, Liam claims that $10,000 contribution as a deduction. Because of his high income, that deduction could easily result in a tax refund of $4,000 or more, depending on provincial tax rates.

By contributing to Chloe's account, Liam gets a substantial tax refund based on his high income. If Chloe had contributed that same $10,000 herself, her refund would have been much smaller because she's in a lower tax bracket.

This immediate financial boost is what makes the strategy so compelling. You're putting money back into your family’s budget today while building a more balanced and tax-efficient retirement fund for tomorrow. Tracking your contribution room and seeing these savings is easy with an app like NeoSpend, which helps you see your whole financial picture without the headache and manage your money smarter.

Navigating The Critical Three-Year Attribution Rule

When you use a Spousal RRSP, there's one golden rule you absolutely need to know: the three-year attribution rule. Think of it as a waiting period the Canada Revenue Agency (CRA) created to ensure these accounts are used for their intended purpose—long-term retirement savings, not short-term tax avoidance.

Here’s what it means: if your spouse withdraws money from their Spousal RRSP, the CRA looks back to see when you last contributed. If you made any contributions in the year of the withdrawal or in the two calendar years before it, that withdrawal gets "attributed" back to you.

This means you, the contributor, must claim that withdrawal as income on your tax return. You'll pay tax on it at your higher marginal rate, which defeats the entire purpose of the income-splitting strategy.

How The Three-Year Clock Works

It all comes down to timing. The "three-year" window includes the year the money is withdrawn, plus the two full calendar years immediately before it.

Once three full calendar years have passed since your last contribution, your spouse is in the clear. Any money they withdraw after that is taxed in their hands, at their lower rate. That's the tax-saving win you're aiming for.

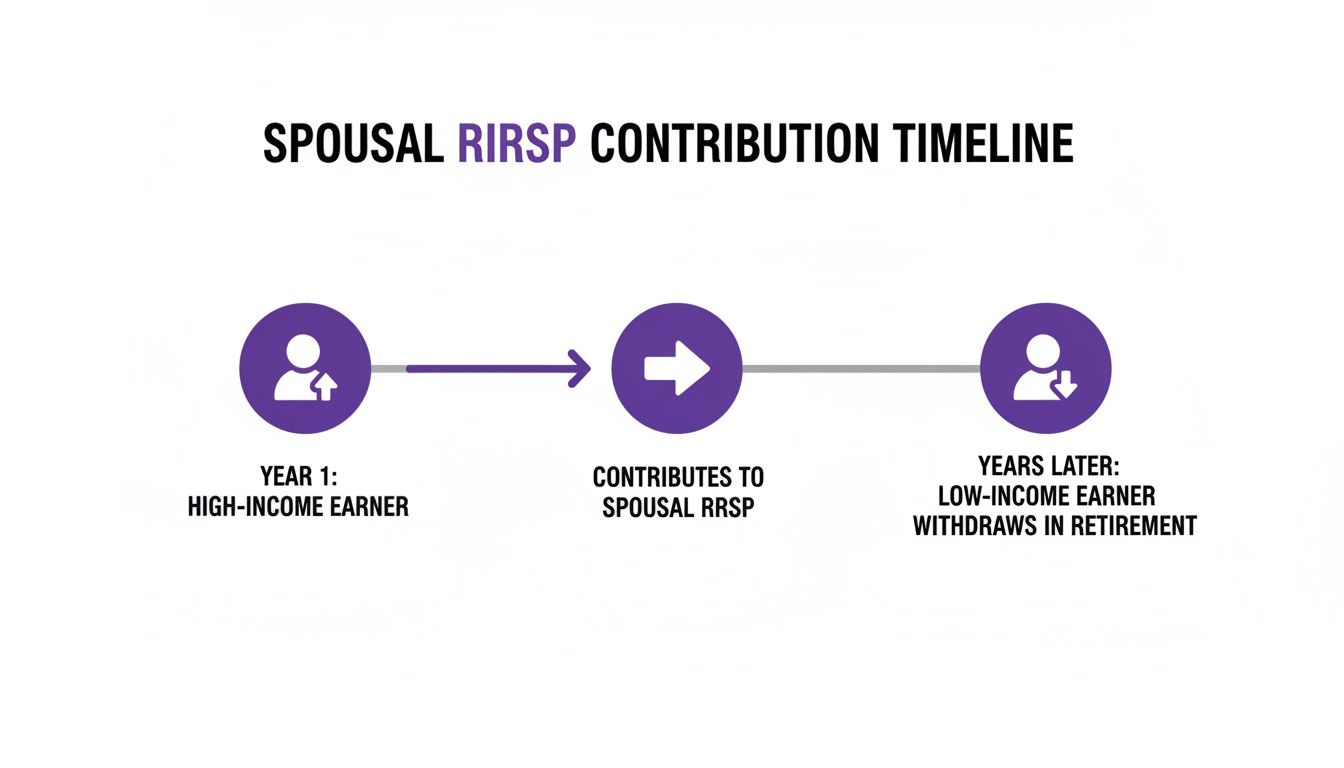

This timeline shows how the money flows from the higher-income earner to the lower-income spouse, paving the way for tax-smart withdrawals in retirement.

The key takeaway is to be strategic. Proper timing is what unlocks the tax savings for the lower-income partner in retirement.

A Practical Example Of The Attribution Rule

Let’s walk through a quick scenario to see this rule in action.

Meet Marc and Stephanie. Marc has been contributing to a Spousal RRSP for his wife, Stephanie.

- 2023: Marc contributes $2,000.

- 2024: Marc contributes another $2,000.

- 2025: Marc contributes $1,000 in January.

Later in 2025, Stephanie needs to withdraw $4,000 from the account for an emergency. Because Marc contributed in 2025 (the year of the withdrawal) and the two prior years (2023 and 2024), the attribution rule is triggered.

The result? The full $4,000 withdrawal is treated as Marc's income for the 2025 tax year, not Stephanie's. For a closer look at these rules, this wealth planning guide from BMO offers more detailed examples.

Once you understand this rule, you can plan around it. If you anticipate your spouse may need to make a withdrawal, you can simply stop contributing for at least three full calendar years beforehand. This ensures the withdrawal is taxed at their lower rate, just as planned.

Keeping track of contribution dates is crucial. A financial tool like NeoSpend can be a lifesaver here. By creating a specific tag for "Spousal RRSP Contributions," you can log every deposit. This makes it easy to check your history and plan withdrawals without accidentally triggering the attribution rule, turning a tricky tax rule into a manageable part of your financial plan.

When a Spousal RRSP Is a Smart Financial Move for Canadians

Understanding the rules of a spousal RRSP is one thing, but seeing how it helps real Canadian families is where it clicks. This isn't just an abstract financial tool; it's a practical solution for common life situations.

Let's explore a few scenarios where this strategy can make a huge difference in building a more secure and tax-smart retirement.

The Significant Income Gap Scenario

Picture a couple, Maya and David, from Toronto. Maya is a surgeon earning $220,000 a year, putting her in a high tax bracket. David is a teacher making $65,000. If they only used their own RRSPs, Maya's retirement withdrawals would be taxed heavily.

By contributing to a spousal RRSP in David's name, Maya gets an immediate and significant tax deduction at her higher income level. In retirement, they can draw income from both her RRSP and David’s spousal RRSP. David's withdrawals will be taxed at his much lower rate, which slashes their combined tax bill and leaves more money for their retirement lifestyle.

The Stay-at-Home Parent or Caregiver Scenario

Now, let's consider Sarah and Tom from Vancouver. Sarah left her career to raise their children and currently has little to no income. Tom has a steady, well-paying job and is maxing out his own RRSP, but Sarah’s retirement savings have stalled.

This is a classic case for a spousal RRSP. Tom can use his contribution room to fund an RRSP for Sarah. This ensures both partners are actively building a nest egg, even when one isn't earning an income. It’s a powerful way to recognize the non-monetary value a stay-at-home parent brings and guarantee they have financial security in retirement.

Planning for an Earlier Retirement

What if one partner wants to retire earlier? Let's say Ben, age 60, plans to retire in two years, while his partner, Anna, age 55, wants to work for another decade. Ben has always been the higher earner.

For years, Ben contributed to a spousal RRSP for Anna. Now, as Ben prepares to retire, they can start withdrawing from Anna's account to supplement his income. As long as they respect the three-year attribution rule, these withdrawals are taxed in Anna's hands at her lower rate. This strategy creates a tax-efficient income stream to bridge the gap until they’re both fully retired.

A spousal RRSP isn't just a savings plan; it's an active financial tool that provides flexibility for major life events, ensuring both partners are on solid financial ground.

If you see your family's situation in any of these examples, a spousal RRSP might be the right move. To make it work, you need a clear handle on your finances to determine how much you can contribute. Using an app like NeoSpend gives you that complete picture, making it easier to set goals and track your contributions toward a shared, prosperous retirement.

Managing Withdrawals and Retirement Income

After years of strategic contributions, you finally reach retirement. This is where the spousal RRSP truly shines, as your long-term income-splitting plan comes to life. All that careful planning now turns into real tax savings that can significantly boost your retirement cash flow.

It all comes down to timing and respecting the attribution rule. Once you're past that three-year waiting period, any money withdrawn from the spousal RRSP is taxed as income for the annuitant spouse—the one whose name is on the account. That income is taxed at their lower marginal rate, not yours. This is the big win.

Converting Your Spousal RRSP to a RRIF

Just like a personal RRSP, a spousal RRSP must be closed by the end of the year the account holder (the annuitant) turns 71. At that point, it is typically converted into a Registered Retirement Income Fund (RRIF) or used to purchase an annuity.

This is a standard step in the Canadian retirement process. A spousal RRIF operates just like a regular one, requiring you to withdraw a minimum amount each year, starting the year after you open it.

The great news is that the income-splitting benefit continues. Those mandatory annual payments from the spousal RRIF are still considered the annuitant spouse's income and are taxed in their hands. This creates a predictable and highly tax-efficient income stream throughout retirement.

Navigating Major Life Events

A solid financial plan must account for life's changes. It’s important to know how a spousal RRSP is treated during major events like a separation or death.

- In case of divorce or separation: A spousal RRSP is usually considered a family asset. Like other marital property, it is typically divided between partners according to your provincial family law.

- If the contributor spouse passes away: The spousal RRSP remains the property of the annuitant spouse. They own the account outright and will be taxed on any future withdrawals they make.

- If the annuitant spouse passes away: The remaining value of the spousal RRSP or RRIF is typically included in their income on their final tax return, unless it can be rolled over tax-free to a qualified survivor, such as their spouse.

Understanding these rules provides a complete picture of how this account functions from start to finish. It’s designed to provide security not just for a comfortable retirement, but through all of life's transitions.

Managing these details requires organization. Using a tool like NeoSpend can help you tag contributions and monitor account balances, giving you a clear financial snapshot at all times. This makes it easier to manage your retirement income and adjust your strategy as your family's needs evolve.

Bringing Your Spousal RRSP Strategy to Life

A spousal RRSP strategy is powerful, but making it work comes down to knowing your numbers. The first crucial step is figuring out exactly what you can afford to contribute without straining your budget. This requires a clear view of your finances.

Modern tools like NeoSpend give the contributing spouse a unified picture of their money, taking the guesswork out of finding a sustainable contribution amount.

It’s also smart for both partners to track these contributions carefully. You can set up a specific savings goal in your finance app—call it ‘Spousal RRSP Contributions’—to keep everything organized.

By tagging every deposit, you create a clean record of your contributions. This is essential for respecting the three-year attribution rule and planning future withdrawals without getting hit by an unexpected tax bill.

Seeing a complete dashboard of all your investment accounts—from your own RRSP to your TFSA and the spousal plan—allows you to coordinate your entire financial picture as a couple. With the right tools like NeoSpend, you can manage your money smarter and turn a tax-savvy strategy into a real, tangible plan for the future you’re building together.

Common Questions About Spousal RRSPs in Canada

Even after understanding the basics, a few specific questions often come up. Let's tackle some of the most common ones we hear from Canadian couples.

Can I contribute to both my RRSP and a Spousal RRSP?

Yes, absolutely. You can contribute to your personal RRSP and a spousal RRSP in the same year.

The key is that all contributions come out of your single annual RRSP contribution room. For example, if your contribution limit for the year is $20,000, you could put $12,000 into your own plan and $8,000 into your spouse's. The Canada Revenue Agency (CRA) only cares that your total contributions do not exceed your limit.

Does my spouse need to have an income to have a Spousal RRSP?

No, and this is one of the biggest advantages of a spousal RRSP. The entire strategy is based on the contributor's income and their available contribution room.

This makes it an excellent tool for couples where one partner has stepped back from their career—perhaps to raise kids, go back to school, or care for a family member—and isn't earning an income to generate their own RRSP room.

How do Spousal RRSPs work if we get divorced?

In the event of a separation or divorce, a spousal RRSP is typically treated as a family asset. Like other shared property, the funds in the account are usually divided between both partners according to provincial family law.

It’s important to remember that while one person contributes, the account legally belongs to the annuitant spouse. This ownership is a key factor during asset division.

Can we use a Spousal RRSP for the Home Buyers' Plan?

Yes. The annuitant (the spouse who owns the account) can withdraw funds from their spousal RRSP for the Home Buyers' Plan (HBP), as long as they meet all the standard HBP eligibility rules.

The withdrawal doesn't trigger the 3-year attribution rule, which is a great feature. However, the responsibility for repaying the withdrawn amount back into the RRSP belongs to the annuitant spouse—the one who took the money out.

A Spousal RRSP is a powerful tool for Canadian couples to build a tax-efficient retirement together. By strategically splitting income, you can lower your overall tax bill and keep more of your hard-earned money. The key is careful planning and tracking your contributions. To manage your money smarter and stay on top of your financial goals, explore how NeoSpend can give you a clear view of your entire financial picture. Take control of your retirement planning and download the NeoSpend app to get started.