So, you've maxed out your TFSA and your RRSP. What's next for your savings? That's where a non-registered account comes in. Think of it as a flexible, general-purpose investment account with no contribution limits but also no special tax protection. It’s the perfect place for your after-tax dollars to keep working for you once you've filled up your other registered accounts, helping you reach your financial goals faster.

Your Flexible Investment Account Explained

Here's a simple way to picture it: if your TFSA is a special tax-free treasure chest and your RRSP is a locked-up retirement vault, then a non-registered account is the big, open storage space where everything else can go. It’s a foundational tool for any Canadian investor looking to build wealth beyond the limits of registered plans.

The biggest difference you need to understand is how it’s taxed. With a TFSA, your investment growth is tax-free. With an RRSP, you defer taxes until retirement. But in a non-registered account, any money you make—like interest, dividends, or profits from selling an investment—is taxable in the year you earn it. This is why it's often called a "taxable account."

Why Do Canadians Use Non-Registered Accounts?

The biggest draw of a non-registered account is its freedom. The government doesn't cap how much you can put in each year, making it the natural next step for investors who have hit their TFSA and RRSP contribution ceilings but still have money to invest.

Often called an unregistered or taxable investment account here in Canada, it's a super flexible spot to hold investments like stocks, bonds, and ETFs. You can invest as much of your after-tax money as you want, which is a game-changer for those who've maxed out their TFSA room (which could hit a cumulative $102,000 by 2025 for some) or their RRSP limits (set to reach $32,490 for 2025). You can dig into more details on these 2025 financial figures for tax planning insights.

This flexibility isn't just for contributions. You can pull your money out whenever you want, for any reason, without penalties. That makes it a great option for medium-term goals, like saving for a down payment on a home or a major renovation in five years.

What Can You Hold Inside a Non-Registered Account?

Just like your TFSA and RRSP, a non-registered account can hold a wide variety of investments. The options depend on your financial institution, but you'll almost always find the usual suspects:

- Stocks from Canadian and global companies.

- Bonds from governments or corporations.

- Mutual Funds run by professional portfolio managers.

- Exchange-Traded Funds (ETFs) that track different market indexes.

- Guaranteed Investment Certificates (GICs) which offer a set rate of return.

This variety means you can build a diversified portfolio that fits your personal risk tolerance and financial goals. Of course, managing these different income streams can get tricky. This is where a smart money management tool like NeoSpend really helps. It lets you see all your financial activity in one place, making it easier to track your dividend payments and interest income when tax season rolls around.

How You're Taxed on Investment Gains in Canada

The word "taxable" might sound intimidating, but the rules for a non-registered account are straightforward once you understand them. The key is that the Canada Revenue Agency (CRA) treats different types of investment earnings differently.

Your gains will fall into one of three categories, each with its own tax rules. Understanding these differences is a game-changer for making smart investment choices that let you keep more of your hard-earned money.

The Three Types of Investment Income

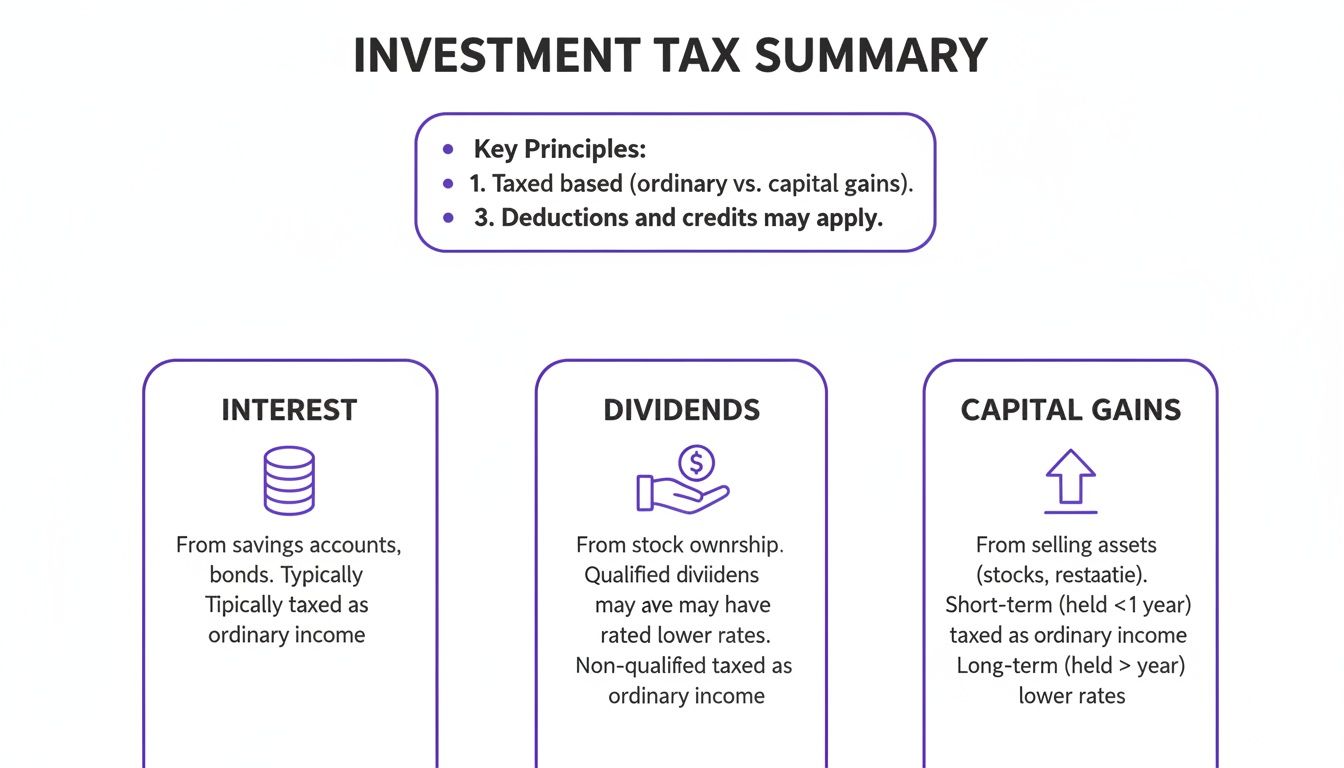

Whenever you make money in a non-registered account, it’s classified as interest, dividends, or capital gains. How each one is taxed can make a huge difference to your bottom line.

- Interest Income: This is what you earn from GICs, savings accounts, or bonds. It's the least tax-friendly because 100% of it is added to your taxable income for the year.

- Dividend Income: If you own shares in eligible Canadian companies, they might pay you dividends. Thanks to the dividend tax credit, this income gets preferential tax treatment from the CRA, meaning you'll pay less tax on it compared to interest.

- Capital Gains: This is the profit you make when you sell an investment for more than you paid. Capital gains get the best deal—only 50% of the gain is taxable. The other half of your profit is completely tax-free.

A common mistake is assuming all investment growth is taxed the same. By being strategic about what you hold in your non-registered account—like focusing on assets that generate capital gains or Canadian dividends—you can significantly lower your tax bill over the long run.

A Real-World Canadian Example

Let's make this practical. Imagine an investor in Ontario with a $70,000 salary. This year, they earned exactly $100 from each of the three income types in their non-registered account.

Here’s a rough idea of how much tax they'd owe on each $100 of earnings:

- Interest Income: The full $100 is taxable, leading to a tax bill of about $29.65.

- Eligible Canadian Dividends: With the dividend tax credit, the tax is only around $6.94.

- Capital Gains: Only half ($50) is taxed, so they’d pay roughly $14.83.

The difference is clear. The same $100 profit can leave you with more (or less) in your pocket depending on how you earned it. This is why tax efficiency is a core part of any savvy Canadian's investment plan.

Of course, keeping these different income streams straight is crucial for tax season. An app like NeoSpend can be a huge help by giving you a clear picture of your accounts, making it easier to spot dividend payments and other investment income all in one place.

Comparing Non-Registered Accounts With TFSAs And RRSPs

Picking the right investment account is like choosing the right tool for a job—each one is built for a specific purpose. For most Canadians, the toolbox contains three main options: the Tax-Free Savings Account (TFSA), the Registered Retirement Savings Plan (RRSP), and the non-registered account. Understanding how they differ is the foundation of a solid financial plan.

Think of it this way: a TFSA is designed for tax-free growth. Any money you put in grows completely shielded from the taxman, and when you pull it out, it’s still tax-free. An RRSP is for retirement; you get a tax deduction when you contribute, but you’ll pay tax on withdrawals later in life.

The non-registered account is the flexible powerhouse with no contribution limits, but every bit of investment growth is taxable.

How Each Account Fits Your Canadian Financial Goals

To see these differences in action, let's walk through a few common Canadian financial goals.

Let's say you're saving for a down payment on a house you want to buy in the next five years. A TFSA is a fantastic choice. Your money can grow without being taxed, and when you're ready to make an offer, you can withdraw the full amount without paying a dime in taxes or penalties.

Now, let's talk retirement. If you're looking to lower your taxable income today while saving for your golden years, contributing to an RRSP is a classic move. Your contribution gives you a tax break now, and the funds grow tax-deferred until you retire—when you’re likely in a lower tax bracket.

So, what happens when you've maxed out both your TFSA and RRSP for the year but still have cash to invest? That’s the perfect time to open a non-registered account. It gives you unlimited room to keep building wealth without being held back by annual contribution limits.

A Side-by-Side Comparison for Canadians

To make things even clearer, here’s a breakdown of how the three accounts stack up.

Comparing Investment Accounts: TFSA vs. RRSP vs. Non-Registered

| Feature | TFSA | RRSP | Non-Registered Account |

|---|---|---|---|

| Main Purpose | Tax-free savings for any goal | Tax-deferred retirement savings | Flexible, unlimited investing |

| Contribution Limit | Annual limit set by the government | 18% of previous year's earned income, up to a maximum | None |

| Tax on Growth | None. All growth is tax-free. | Tax-deferred until withdrawal | Taxable in the year it's earned |

| Withdrawal Rules | Tax-free, anytime | Taxable as income | Can withdraw anytime, but may trigger capital gains tax |

As you can see, each account brings something unique to the table. The right strategy for you will likely involve a mix of all three, depending on your personal financial situation and goals.

This infographic gives a quick summary of how different investment earnings are taxed inside a non-registered account.

The big takeaway is that not all investment income is treated the same by the CRA. Capital gains get the friendliest tax treatment, making them a very efficient way to grow your money in a taxable account.

Balancing these accounts is where the magic happens. A tool like NeoSpend helps you get a single, consolidated view of all your investments. Seeing everything in one place makes it much easier to track your performance and make smart decisions about where to put your next dollar.

When Should a Canadian Use a Non-Registered Account?

Most people think of a non-registered account as what you use after you’ve maxed out your TFSA and RRSP. While that’s true, thinking of it as just an overflow container misses the point. It’s a powerful tool with unique strengths, especially when you need flexibility and unlimited contribution room.

Knowing when to use it can seriously accelerate your wealth-building journey.

One of the most common reasons to open one is to save for a medium-term goal. Think about something that's too far off for a high-interest savings account, but too close to lock up in an RRSP. A classic Canadian example? Saving for a cottage down payment or a big kitchen reno you’re planning for five years down the road.

A non-registered account lets you invest that money for potentially better growth, but without the stiff penalties or tax hits you’d face for pulling from an RRSP early. When you're ready, you can access your funds, paying tax only on the gains you’ve made.

Building a Tax-Efficient Portfolio in Canada

Beyond specific goals, a non-registered account is the perfect place for certain investments if you want to be smart about minimizing your tax bill. In Canada, only 50% of capital gains are taxed, and dividends from Canadian companies get a valuable tax credit. This makes a non-registered account the ideal home for assets that generate these types of returns.

Here’s a practical strategy:

- Hold Growth Stocks or ETFs: If you’re investing in assets focused on long-term appreciation, you don't pay tax until you sell. This lets your money compound more powerfully.

- Invest in Canadian Dividend-Paying Stocks: Thanks to the dividend tax credit, you’ll pay less tax on this income than you would on interest, making it a smart choice for a taxable account.

This strategy frees up the precious, limited room in your TFSA and RRSP for investments that are less tax-friendly, like bonds or GICs that generate fully taxable interest income.

Unlocking Smarter Financial Strategies

A non-registered account also opens the door to more advanced financial planning. For instance, it’s a great vehicle for income splitting with a lower-income spouse.

If you’re in a high tax bracket, you can loan money to your spouse (at the CRA's prescribed interest rate) to invest in a non-registered account in their name. The investment income is then taxed at their lower rate, which can seriously reduce your family’s total tax bill. It’s a powerful way to make your household’s investment plan more efficient.

By understanding these specific use cases, a non-registered account transforms from a simple investment holder into a dynamic part of your financial plan. It provides the flexibility needed for life's medium-term goals and the tax efficiency required for long-term wealth.

Keeping track of different income types—dividends here, interest there—can get complicated. This is where a tool like NeoSpend really proves its worth. It gives you a clean, simple view of your cash flow, dividend payments, and interest, making it so much easier to manage your investments and prepare for tax time.

How to Manage Your Account for Tax Season

The flexibility of a non-registered account comes with one key responsibility: great record-keeping. It might sound like a chore, but staying organized is the secret to a stress-free tax season and ensuring you don't pay a penny more in tax than you owe.

The most important concept here is the Adjusted Cost Base (ACB). Think of it as the master receipt for your investments. It’s not just the purchase price; it’s the total cost, including any commissions or fees you paid to buy the asset.

When you sell, your capital gain (or loss) is the sale price minus your ACB. Without an accurate ACB, you could make a costly mistake on your tax return.

Tracking Your Adjusted Cost Base (ACB)

For anyone with a non-registered account, tracking your ACB is essential. It’s a living number. Every time you buy more of the same stock or reinvest your dividends to get more shares, your ACB changes. You have to update your records with every transaction.

For example: you buy 100 shares of a company at $10 each and pay a $10 commission. Your starting ACB is (100 x $10) + $10 = $1,010. A few months later, you buy another 50 shares at $12 each (with another $10 commission). You now have to recalculate your total ACB to account for this new purchase.

One of the best ways to manage this is with a simple spreadsheet. Log the date, transaction type (buy/sell), number of shares, price, and commission for every transaction. This diligence pays off massively at tax time.

Practical Tips for Flawless Record-Keeping

Getting organized doesn't have to be a headache. Building a few good habits now can make tax prep a smooth process.

Here are a few actionable tips:

- Keep All Trade Confirmations: Your brokerage sends a confirmation for every transaction. Save these digitally in a folder dedicated to your non-registered account.

- Track Reinvested Dividends: If you use a DRIP (Dividend Reinvestment Plan), each automatic reinvestment is a new purchase that alters your ACB. It’s easy to forget these, but they count.

- Document Return of Capital: Some investments, like certain ETFs, might give you a "return of capital" (RoC). This isn't taxable income right away, but it reduces your ACB, which is crucial to track for when you eventually sell.

Let Technology Do the Heavy Lifting

Manually tracking every transaction can get old fast, especially as your portfolio grows. This is where a smart financial tool can save the day. A platform like NeoSpend can simplify the process by connecting to all your different accounts.

With NeoSpend, you get a single dashboard showing your entire financial world. It helps you see dividend payments and other investment cash flow in one spot. This consolidated view can turn tax prep from a puzzle into a manageable task. Instead of digging through a dozen statements, you have a complete picture ready to go, making it easier to manage your what is a non registered account and stay on top of your tax obligations.

Your Key Takeaway on Non-Registered Accounts

So, you’ve maxed out your TFSA and RRSP. First, congratulations—that’s a huge milestone for any Canadian. Now you know that a non-registered account is your next powerful tool for building serious wealth.

Think of it as the wide-open field of investing. Once you’ve filled the sheltered spaces of your registered plans, a non-registered account gives you unlimited room to grow your after-tax dollars. There are no contribution ceilings, giving you total freedom to invest as much as you want. For it to be most effective, fill it with tax-efficient assets like Canadian dividend stocks or investments geared toward capital gains, which get friendlier tax treatment.

If there’s one thing to remember, it’s this: keeping a meticulous record of your Adjusted Cost Base (ACB) is absolutely essential for filing your taxes correctly and avoiding overpayment.

Juggling different accounts can feel like a lot. To get a bird's-eye view of how these taxable investments fit with your day-to-day spending and savings, a tool like NeoSpend can be a game-changer. It pulls everything together in one place, so you can see your entire financial picture at a glance. This makes tracking your progress simpler and helps you make smarter decisions, keeping you firmly in control.

Common Questions from Canadian Investors

Diving into non-registered accounts can bring up a few questions. Let's clear up some of the most common ones Canadians have so you can invest with confidence.

What Happens If I Lose Money on an Investment?

Selling an investment for less than you paid creates a capital loss. While never ideal, it has a silver lining at tax time.

You can use that loss to offset any capital gains you’ve made in the same year, which directly lowers your tax bill. If your losses are greater than your gains, the CRA lets you carry the net capital loss back to offset gains from the past three years or carry it forward indefinitely to use against future gains.

Can I Move Investments into My TFSA or RRSP?

Yes, you can transfer investments "in-kind" from your non-registered account into a TFSA or RRSP, provided you have enough contribution room. However, the CRA considers this a deemed disposition.

This means it's treated as if you sold the investments for their market value on the day of the transfer. If they’ve gone up in value, you’ll have to report a capital gain and pay tax on it. On the other hand, if the investment has lost value, you are not allowed to claim that capital loss on an in-kind transfer to a registered account.

What Happens When the Account Owner Passes Away?

When someone with a non-registered account passes away, another deemed disposition occurs. It’s as if all the assets were sold at their market value on the date of death. Any resulting capital gains must be reported on the deceased's final tax return.

From there, the assets become part of the estate. The major exception is if the assets are being transferred to a surviving spouse or common-law partner. In that case, the investments can often "roll over" at their original cost, delaying the capital gains tax until the surviving partner sells them or passes away.

Keeping track of all these moving parts is easier when you can see your entire financial picture at once. NeoSpend gives you a single dashboard to monitor all your accounts, helping you connect your investment performance with your everyday spending. See how NeoSpend can bring clarity to your finances.