Ever feel like your money needs a GPS? That's exactly what a financial advisor does for Canadians. Think of them as a personal trainer for your finances—someone who helps you navigate the world of TFSAs, RRSPs, mortgages, and investments to map out a clear path to your financial goals.

Your Financial Guide in a Complex World

Let's be honest: managing money in Canada can feel overwhelming. Between TFSAs, RRSPs, soaring interest rates, and the climbing cost of living, it's easy to feel like you're guessing. A financial advisor steps in to provide personalized, expert guidance that can make a real difference.

Their main job is to build a roadmap tailored to your life, leading you toward your biggest goals. It doesn't matter if you're trying to buy your first home in Calgary, retire comfortably in the Maritimes, or finally get a handle on your debt. An advisor brings clarity and a solid strategy to your financial life, and they’re not just for the wealthy—they offer valuable direction for anyone who wants to make smarter money moves.

Why Canadians Are Seeking Professional Financial Advice

The financial world is getting trickier to navigate alone. According to FP Canada's 2024 Financial Stress Index, a surprising 37% of Canadians now work with a financial professional. Specifically, one in seven (16%) rely on a financial advisor to help guide their decisions.

What’s really interesting is the clear link between getting professional advice and feeling better about your finances. The data shows that Canadians without a financial planner are more than twice as likely to see their disposable income drop compared to those who have one. You can read more about the findings on financial stress in Canada to see just how much of an impact professional advice can have.

A financial advisor’s role is to translate your goals into a structured, actionable plan. They act as your strategist, accountability partner, and expert guide, helping you make informed decisions and stay on track through life's inevitable ups and downs.

Preparing for Your Financial Journey

Before sitting down with an advisor, getting your financial house in order is a huge first step. Using a tool like NeoSpend brings all your accounts into one dashboard, giving you a clear picture of your income, expenses, and savings. This simple prep work helps you walk into your first meeting with confidence, ready to build a strategy that works for you.

Core Services Canadian Financial Advisors Provide

When you ask, "what does a financial advisor actually do?", the answer is much more than just picking stocks. A great advisor is the architect of your financial life, drafting a comprehensive blueprint that connects every piece of your money puzzle.

They offer a suite of services that work together, ensuring a decision about your investments also supports your retirement goals. This integrated approach is critical because your money doesn’t live in separate boxes. Your retirement dreams influence your investment choices, and both are shaped by smart tax strategies.

Let's look at the key services you should expect from a Canadian financial advisor.

Key Services Offered by Financial Advisors in Canada

Here’s a breakdown of the most common services advisors offer, with real-world Canadian examples.

| Service Area | What They Do for You | Example Canadian Scenario |

|---|---|---|

| Investment Management | Build and manage a portfolio that fits your goals and risk tolerance. They help you understand different investment types and avoid emotional market decisions. | A young professional in Toronto might build a portfolio of growth-oriented ETFs in their TFSA, while someone nearing retirement in Halifax might focus on dividend stocks and bonds for steady income. |

| Retirement Planning | Help you figure out how much you need to save for the retirement you want. They strategize the best use of accounts like your RRSP and TFSA. | An advisor helps a 40-year-old determine the optimal split for their savings between their RRSP (for the immediate tax break) and TFSA (for tax-free growth). |

| Tax Planning | Structure your finances to be as tax-efficient as possible, letting you keep more of your money. | They might advise placing high-income investments (like bonds) in your RRSP to defer taxes, while keeping Canadian dividend stocks in a non-registered account to benefit from the dividend tax credit. |

| Insurance & Risk Management | Analyze potential financial risks (like illness or death) and recommend the right type and amount of insurance to protect you and your family. | After a new baby arrives, an advisor helps a couple secure a term life insurance policy that would cover their mortgage and future education costs if something happened to one of them. |

| Estate Planning | Work with you (and often a lawyer) to create a plan for how your assets will be distributed after you’re gone, minimizing taxes and ensuring your wishes are followed. | An advisor helps a business owner structure their will and set up trusts to ensure a smooth and tax-efficient transfer of their company to their children. |

As you can see, their job is to build a cohesive strategy where every part of your financial plan is working in harmony.

Investment Management and Strategy

This is what most people think of first. An advisor helps you build an investment portfolio aligned with your life goals and comfort with risk. They aren't just order-takers; they're strategists. They demystify the world of investing—ETFs, mutual funds, GICs—and help you build a diversified portfolio designed for long-term growth. A huge part of their value is acting as a calm voice of reason when the market gets shaky.

Comprehensive Retirement Planning

Saving for retirement in Canada means making the most of powerful accounts like the Registered Retirement Savings Plan (RRSP) and the Tax-Free Savings Account (TFSA). An advisor’s job is to turn these tools into your personal wealth-building engine.

They help you:

Do the math: Figure out exactly how much you’ll need to save to live the life you want in retirement.

Optimize your savings: Decide whether it’s better to contribute to your RRSP or TFSA this year based on your income.

Create a retirement paycheque: Map out a plan to turn your nest egg into a reliable income stream, factoring in CPP and OAS.

This kind of planning isn’t just about saving—it’s about saving smarter.

Tax Planning and Efficiency

This is one of the most underrated services an advisor provides. They work to minimize your tax bill, which means more of your hard-earned money stays in your pocket. This involves concrete strategies, like placing certain investments inside a tax-sheltered account like your RRSP or TFSA to reduce the tax you pay on growth.

A key part of financial advice isn't just about what you earn, but what you keep. Smart tax planning can feel like getting an extra return on your investments.

Insurance and Risk Management

Growing your wealth is exciting, but protecting it is just as crucial. An advisor takes a hard look at your life to spot potential financial risks and recommend the right kind of insurance to guard against them. This could mean life insurance to protect your family, disability insurance to replace your income if you get sick, or critical illness insurance to provide a tax-free lump sum. They ensure your financial plan is protected from life’s curveballs.

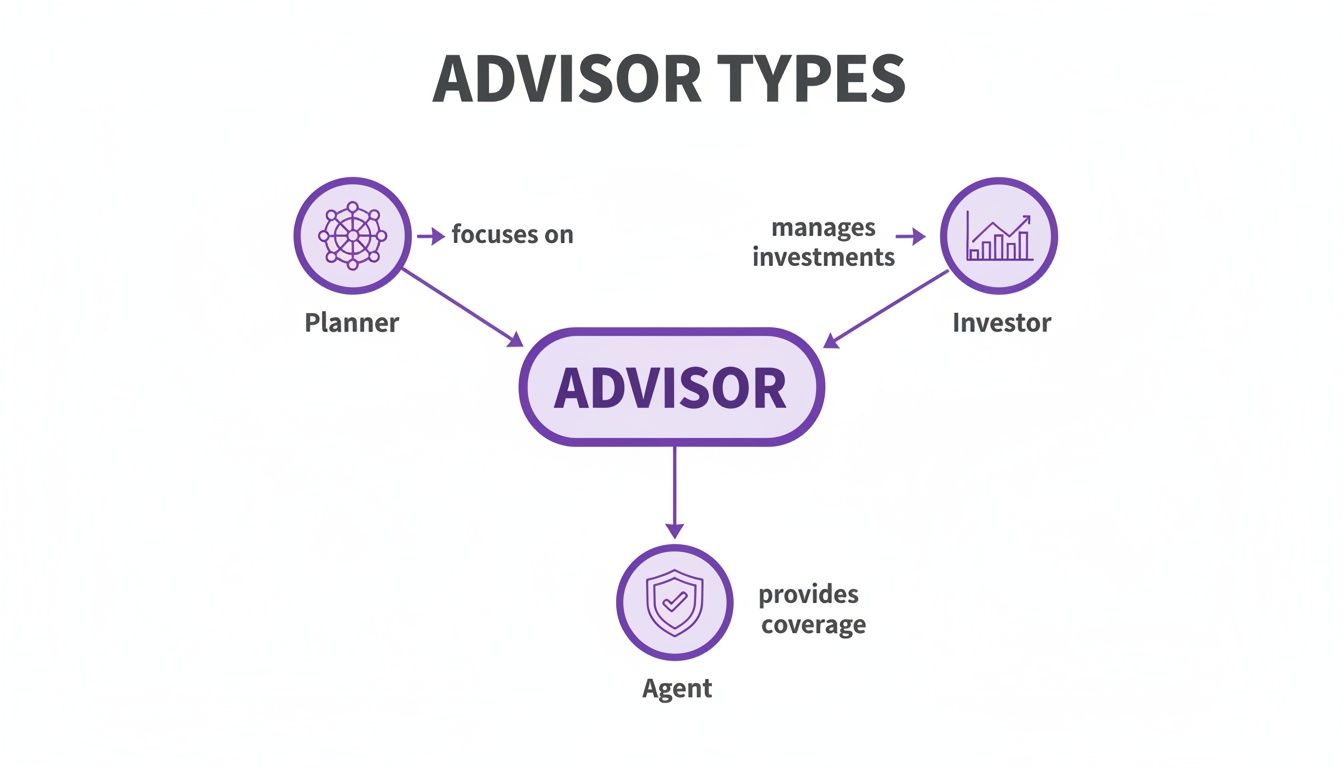

Different Types of Financial Advisors Explained

Not all financial pros wear the same hat. In Canada, "financial advisor" is a broad term, so understanding the different specialties is key to finding the right person for you. Think of it like building a house: you hire an architect for the design, a contractor to manage the project, and specialists like plumbers for specific jobs.

Let’s break down the most common types of financial advisors you'll find in Canada.

Certified Financial Planner (CFP)

A Certified Financial Planner (CFP) is like the architect of your financial world. They look at the whole picture—your retirement goals, insurance coverage, tax strategy, and estate plan—to pull it all into one cohesive strategy.

Who they're for: Anyone who needs a comprehensive, long-term financial roadmap. If you're juggling big goals like saving for retirement, a child's education, and paying down a mortgage, a CFP is a great choice.

How they help: They build a detailed plan where every financial decision works together to get you where you want to go.

Investment Advisor

An Investment Advisor (or Registered Representative) is licensed to buy and sell investments like stocks, bonds, and mutual funds. Their main job is to grow your wealth through the market, ensuring your portfolio matches your comfort with risk. While some offer broader advice, their expertise is in managing investments.

Insurance Agent

An Insurance Agent focuses on one thing: protecting you from financial risk. Their role is to look at the "what ifs" in life—illness, injury, or death—and recommend products like life, disability, or critical illness insurance to build a financial safety net for you and your family.

An insurance agent’s job is to build a financial safety net. They make sure an unexpected event doesn't derail the financial plan you’ve worked so hard to build.

Robo-Advisors

Robo-advisors are digital platforms that use algorithms to build and manage an investment portfolio for you, usually for a very low fee. They’re fantastic for straightforward, goal-based investing. They're perfect for new investors or anyone comfortable with a digital-first approach. While you don't get personalized human advice, they offer an accessible and affordable way to get your money into the market. Getting a clear view of your spending with a tool like NeoSpend can help you figure out how much to set aside for these automated investments.

How Financial Advisors Get Paid in Canada

Understanding how your advisor gets paid is critical for building a trusting relationship. When you know where their paycheque comes from, you can better understand their advice. In Canada, there are three main ways advisors are compensated.

This image helps visualize how different financial pros specialize, which is often tied to how they are paid.

Commission-Based

In this traditional model, a commission-based advisor earns money by selling you financial products, like a mutual fund or an insurance policy. The product company pays the advisor a commission. The upside is that you don't pay a direct fee. The downside is a potential conflict of interest, as an advisor might be tempted to recommend a product that pays them a higher commission.

Fee-Based (AUM)

A fee-based advisor charges a percentage of the total assets they manage for you. This is often called an "Assets Under Management" or AUM fee. For example, if an advisor manages $200,000 of your investments and charges a 1% AUM fee, you’d pay them $2,000 a year. This model aligns their success with yours—when your portfolio grows, so does their pay.

When an advisor’s pay is tied to your portfolio's growth, their main incentive is to help your money grow. This creates a partnership focused on long-term success.

Fee-for-Service

The fee-for-service model is the most straightforward. You pay an advisor directly for their time or for a specific task, like an hourly rate for a consultation or a flat fee for a comprehensive financial plan. This is a fantastic option if you need specific advice without ongoing management. Because the advisor is paid only for their expertise, it’s widely seen as the most transparent and conflict-free model.

Comparing Financial Advisor Fee Structures

This table breaks down the fee structures to help you decide what's right for you.

| Fee Model | How It Works | Best For... | Potential Conflict |

|---|---|---|---|

| Commission-Based | Advisor earns a commission from selling specific products (e.g., mutual funds, insurance). | Those who prefer not to pay an upfront or ongoing fee and are comfortable with the product-based model. | The advisor may be incentivized to recommend products with higher commissions, not necessarily what's best for you. |

| Fee-Based (AUM) | You pay a percentage of the assets the advisor manages for you (e.g., 1% of your portfolio). | Investors with larger portfolios who want ongoing management and a partnership approach. | Since fees are based on asset size, there's less incentive for advice on things like debt management. |

| Fee-for-Service | You pay a flat fee for a specific project (like a financial plan) or an hourly rate for consultation. | People who need a one-time plan or specific advice without ongoing investment management. | None. This model is considered the most transparent and conflict-free. |

The key is to find an advisor whose compensation structure you understand and feel comfortable with.

How to Choose the Right Financial Advisor for You

Finding an advisor you click with is a huge part of getting your finances on track. Think of it less like hiring someone to crunch numbers and more like finding a long-term partner who understands your life goals.

It all starts with knowing where to look and what to ask.

Finding Potential Advisors

Doing a little homework now will save you headaches later.

Ask for Referrals: Chat with friends, family, or colleagues who seem to have their finances in order. A recommendation from someone you trust is a great starting point.

Check Professional Organizations: Reputable groups like FP Canada have directories of certified professionals, ensuring they meet strict ethical and educational standards.

Look at Your Bank: Your own bank often has in-house advisors or planners, which can be a convenient option.

Your goal is to get a shortlist of two or three candidates you can interview to compare their approaches and see who you connect with.

Essential Questions for Your First Meeting

Remember, you’re interviewing them, not the other way around. Come prepared with a list of questions to make an informed choice.

Here are a few must-asks:

What are your qualifications and credentials? (Listen for designations like CFP, PFP, or CIM).

How do you get paid? (This gets straight to the fee structures we talked about).

What is your investment philosophy? (Are they an active trader, or do they prefer passive, long-term strategies?).

Who is your typical client? (This helps you see if they have experience with people in a similar financial situation as you).

How often will we communicate? (Set expectations for meetings and check-ins from the start).

Before your meeting, organize your finances in an app like NeoSpend. Having a clear view of your accounts, debts, and spending makes the conversation incredibly productive.

Red Flags to Watch Out For

Knowing what to avoid is just as important as knowing what to look for. Be cautious of anyone who:

Promises guaranteed high returns. No one can predict the market.

Pressures you to make quick decisions. A true professional gives you time to think.

Is vague about how they get paid. Transparency is non-negotiable.

Doesn't give you straight answers.

Trust your gut. If something feels off, it’s okay to walk away and keep looking.

Your Partner in Building Financial Confidence

Ultimately, a great financial advisor does more than manage your money—they build your confidence. They are your financial strategist, accountability partner, and expert guide, helping you make smart decisions through all of life's ups and downs.

They turn the complex world of finance into a clear, actionable plan that makes sense for you. This partnership is becoming even more essential as Canadians grapple with market volatility, economic slowdowns, and persistent inflation. The desire for a single, go-to 'essential advisor' has shot up 59% since 2018, showing how much people value comprehensive guidance. You can read more about how Canadian advisors are adapting in 2025 to meet this growing need.

The journey to financial well-being starts with clarity. A solid advisor helps you navigate uncertainty, turning abstract goals into concrete achievements.

By taking a simple first step, like organizing your accounts with NeoSpend, you create the perfect foundation. This clarity lets you start a relationship with an advisor on solid ground, ready to turn your financial goals into reality.

Takeaway

A financial advisor acts as your personal guide, helping you create a strategy for everything from investing and retirement to taxes and insurance. They provide the expertise and discipline needed to navigate Canada's complex financial landscape with confidence. By understanding what they do and how to choose the right one, you can build a partnership that empowers you to achieve your most important life goals.

Ready to gain clarity on your finances? Start managing your money smarter with NeoSpend today.