So you’re self-employed in Canada. Welcome! While the freedom is fantastic, you’ve also just become your own accounting department. The biggest shift? You’re now responsible for handling your own income taxes and Canada Pension Plan (CPP) contributions.

Unlike a traditional job where your employer deducts taxes from each paycheque, every dollar you earn as a business owner is yours to manage. That means you need to calculate, save for, and pay your taxes to the Canada Revenue Agency (CRA) yourself. This guide will walk you through everything you need to know.

Understanding Your Self-Employment Tax Responsibilities in Canada

Making the leap from employee to business owner can feel like a big deal, especially around tax time. But it really just boils down to understanding a few key responsibilities. Staying on top of your finances isn't just a good habit—it's essential for keeping your business healthy and avoiding stress down the road.

What Taxes Are You Responsible For?

When you work for yourself, you're taking on the tax duties an employer would normally cover. Here’s a quick rundown of what’s on your plate:

Income Tax: You'll owe federal and provincial income tax on your net business profit. That’s your total income minus all your eligible business expenses.

Canada Pension Plan (CPP): This is a big one that catches many new freelancers off guard. As an employee, you pay half the CPP contributions, and your employer pays the other half. When you’re self-employed, you have to pay both portions.

Goods and Services Tax (GST/HST): The moment your business brings in more than $30,000 in revenue over four consecutive quarters, you’ll generally need to register for a GST/HST number. From that point on, you have to collect it from your Canadian clients and send it to the CRA.

Key Tax Deadlines for the Self-Employed

Missing tax deadlines is a recipe for penalties and interest charges that can pile up fast. Mark these dates in your calendar right away:

The two most important deadlines for self-employed Canadians are April 30th for paying any tax you owe and June 15th for filing your tax return. Yes, you get a little extra time to file, but the payment is still due at the end of April.

If you miss that April 30th payment deadline, the CRA will start charging you interest on whatever you owe, starting from May 1st.

Paying Your Taxes in Instalments

To help you avoid a massive tax bill at the end of the year, the CRA expects many self-employed people to pay their estimated taxes in quarterly instalments. This usually kicks in if your net tax owing is more than $3,000 for the current year and was also over $3,000 in either of the two previous years.

This is where planning ahead makes all the difference. Instead of scrambling to figure out what you owe, a tool like NeoSpend can be a lifesaver. It helps you track your income and expenses in real-time, giving you a clear picture of your cash flow.

You can create a digital "tax jar" by automatically setting aside a percentage of every payment you receive. This ensures the money is ready and waiting when your quarterly due dates roll around, turning a stressful task into a simple, automated habit.

How to Calculate Federal Income Tax and CPP

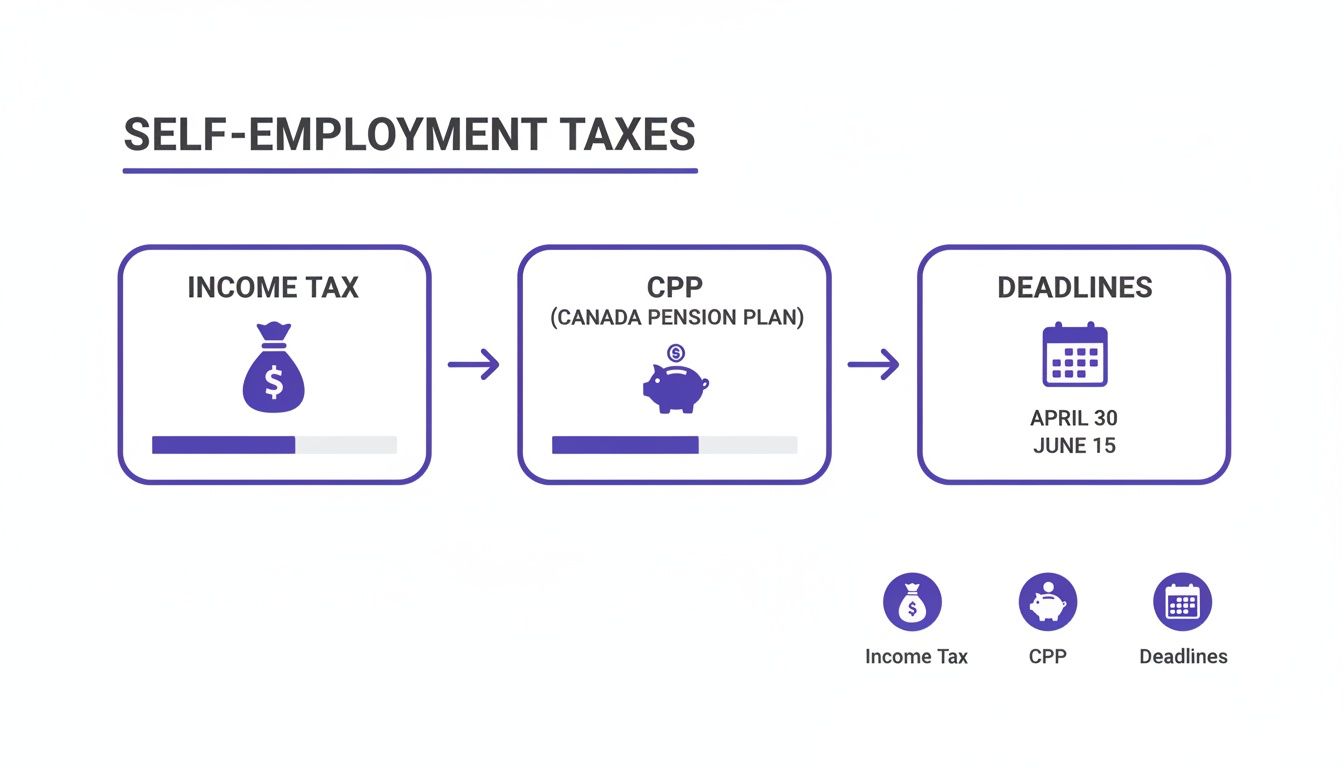

When you make the leap to self-employment, you suddenly become your own payroll department. Two of the biggest line items you'll now manage are your federal income tax and Canada Pension Plan (CPP) contributions. It's a big shift from a traditional job where this is all handled for you. Understanding how they work is the first step to staying on top of your finances.

This flowchart lays out the core financial duties of being your own boss, from income tax and CPP to the key dates you can't afford to miss.

As you can see, earning money is only half the battle. The other half is having a solid game plan for setting cash aside for taxes and investing in your own retirement through CPP.

How Federal Income Tax Brackets Work for Canadians

Canada's tax system is "progressive," which is a fancy way of saying the more you earn, the higher your tax rate gets—but only on the money you earn above certain amounts. Think of it like filling up a series of buckets. The first bucket gets filled at the lowest tax rate. Once it's full, the overflow spills into the next bucket, which has a slightly higher rate, and so on.

Let's imagine you're a freelance graphic designer in Toronto earning $70,000 in net income. For 2024, the first $55,867 of your income is taxed at 15%. The income you earn above that—the next $14,133—is taxed at the next bracket rate of 20.5%.

This is exactly why smart financial tracking is so crucial. With a tool like NeoSpend, you can see your income and categorized expenses in real-time, helping you project which tax bracket you're heading for so there are no nasty surprises. You can find more great insights in these self-employment tax tips.

Key Takeaway: Moving into a higher tax bracket is a good thing! It means you're earning more. Crucially, only the income within that new, higher bracket gets taxed at the higher rate, not your entire income.

The Canada Pension Plan: Your New Double-Duty

The other big financial reality check is the Canada Pension Plan (CPP). When you worked for someone else, you paid a portion of your paycheque into CPP, and your employer kicked in a matching amount. Simple.

But now that you're self-employed, you wear both hats: you're the employee and the employer. That means you’re on the hook for paying both halves of the CPP contribution.

The Employee Part: This is the standard amount every worker in Canada pays.

The Employer Part: This is the matching contribution you now have to cover yourself.

This "double contribution" can be a surprise at first. For 2024, the self-employed CPP rate is 11.9% on your pensionable earnings, up to an annual maximum. It’s a significant amount, but remember, every dollar is going directly toward building your own retirement pension.

Dealing with these bigger, less frequent payments requires a plan. You can tuck away a percentage of every payment you receive into a virtual "tax jar." When you treat your tax and CPP savings like any other non-negotiable business expense, you’ll have the cash ready and waiting when the CRA expects it. No more year-end panic.

Navigating GST/HST and Quarterly Tax Instalments

Beyond income tax and CPP, two other major financial hurdles appear as your business grows: sales tax and quarterly tax instalments. These aren't just suggestions from the Canada Revenue Agency (CRA)—they're mandatory. Get them wrong, and you'll face some hefty penalties.

Getting a handle on these obligations is crucial for keeping your cash flow healthy and avoiding heart-stopping tax surprises.

When Do You Need to Register for GST/HST?

One of the biggest milestones for any freelancer in Canada is hitting the small supplier threshold. The moment your business brings in over $30,000 in gross revenue—either in a single calendar quarter or across four consecutive quarters—you must register for, collect, and remit Goods and Services Tax (GST) or Harmonized Sales Tax (HST).

This isn't negotiable. If you're late to register, the CRA will expect you to pay all the GST/HST you should have collected from your clients, along with penalties and interest.

Understanding Your GST/HST Obligations

Once you're no longer a "small supplier," your first step is to get a GST/HST number from the CRA. From that day forward, you must add the correct sales tax to every invoice you send to Canadian clients. The rate depends on the province or territory where you’re providing the service.

For example, a consultant in Alberta charges 5% GST. A web developer in Ontario charges 13% HST.

Here's a critical mindset shift: the GST/HST you collect is never your money. You're just holding onto it for the government. A common mistake is letting this tax mix with your business income. It makes your bank account look bigger than it is, creating a massive cash crunch when it’s time to pay the CRA.

A practical approach is to use a tool like NeoSpend to view all your transactions in one place. By automatically sweeping the GST/HST from every payment into this separate space, you protect it from your day-to-day operating cash and know it'll be there when it's time to pay.

The Reality of Quarterly Tax Instalments

As your business finds its footing and starts earning more, the CRA won't wait until April 30th to get paid. If your net tax owing is more than $3,000 this year (and it was also over that amount in either of the past two years), you'll be required to pay your estimated taxes in quarterly instalments.

These payments are an advance on your estimated federal and provincial income tax, plus your CPP contributions for the year. The deadlines are firm, falling on the same four dates every year:

March 15

June 15

September 15

December 15

Missing a payment isn't like being late on a phone bill. The CRA charges instalment interest, compounded daily, at a high rate—often near 10%. For someone self-employed, like a consultant in Vancouver, these payments are essential for staying onside with the government. You can get a deeper look at how contributions work for the self-employed by exploring these insights from NerdWallet.

Planning is everything. With NeoSpend, you can view all your transactions in one place, including those related to your income tax and CPP. By regularly tucking away a set percentage of your earnings, you methodically build up the funds you need. What could have been a quarterly financial shock becomes just another predictable business expense.

Maximizing Deductions: How to Lower Your Self-Employed Tax Bill

When you're self-employed, tax time isn't just about paying what you owe—it's about smart strategy. This is where business expenses become your best friend. Every legitimate dollar you spend to earn your income can be subtracted from your total revenue, which directly lowers your taxable profit. Less profit means a smaller tax bill.

This is how you keep more of your hard-earned money right where it belongs: in your pocket.

The Canada Revenue Agency (CRA) lets you deduct any reasonable expense you incur to earn income. That word "reasonable" is key. It means you probably can't write off a luxury sports car, but you can absolutely claim the costs of a practical vehicle you use for client meetings. The one non-negotiable? You need proof for every single claim, so tracking your expenses is essential.

Claiming Home Office Expenses

For countless Canadian freelancers, the home office is mission control. The CRA allows you to deduct a portion of your household expenses, but first, you have to meet one of two conditions: your home is your main place of business, or you use the space exclusively for work and regularly meet clients there.

If you meet one of those conditions, you can claim a percentage of your home costs based on how much of your home's total square footage your workspace occupies. For example, if your office is 10% of your home's total area, you can deduct 10% of these eligible costs:

Rent or Mortgage Interest: Deduct a portion of your rent or the interest on your mortgage payments.

Utilities: A percentage of your hydro, heat, and water bills are fair game.

Home Insurance: You can claim part of your insurance premiums.

Property Taxes: A portion of your annual property tax bill is also an eligible expense.

Vehicle Expenses and Mileage Tracking

Do you use your personal car for business? Driving to client meetings, grabbing supplies, or heading to a conference? You can deduct a portion of what it costs to run that vehicle. This is a huge deduction for many self-employed people, but it’s one the CRA watches closely.

The golden rule for vehicle expenses is to keep a detailed mileage log. Seriously. Without one, the CRA can easily deny your claim. Your log needs to show the date, destination, purpose of the trip, and odometer readings for every business drive.

At year-end, you'll calculate what percentage of your total driving was for business. You then apply that percentage to all your vehicle costs, including fuel, insurance, repairs, and even lease payments or depreciation (known as Capital Cost Allowance).

Other Common Business Deductions You Shouldn't Miss

Beyond your home and car, a whole world of other expenses can lower your taxable income. Here are some of the most common deductions for Canadian freelancers. Remember to always keep detailed receipts.

Common Deductible Expenses for Canadian Freelancers

| Expense Category | Description & CRA Rules | Example |

|---|---|---|

| Office Supplies | Anything you use to run your office day-to-day, including physical items and digital tools. | Pens, paper, printer ink, planners, accounting software subscriptions (like QuickBooks), and project management tools (like Asana). |

| Professional Development | Costs for courses, workshops, or industry conferences that maintain or improve your professional skills. | A photographer taking an advanced course on lighting techniques or a writer attending a digital marketing conference. |

| Advertising & Promotion | Any money spent to market your business and attract clients. | Costs for running social media ads, printing business cards, website hosting fees, or hiring a branding consultant. |

| Meals & Entertainment | You can claim 50% of the amount spent on food, beverages, or entertainment for business purposes. | Taking a potential client out for lunch to discuss a project. If the bill is $80, you can claim $40 as a business expense. |

| Business Travel | Expenses for travel required to earn income, like visiting an out-of-town client or attending a trade show. | The cost of your flight, hotel stays, and taxi fares. Meals on the trip are subject to the 50% limit. |

This is where a tool like NeoSpend can be a total game-changer. Instead of drowning in a shoebox of receipts, NeoSpend automatically tracks and categorizes your spending. You can tag a coffee shop purchase as a "Client Meeting" once, and it learns for next time. It helps build a clean, accurate, audit-proof record that makes tax time feel a lot less stressful.

A Step-by-Step Guide to Filing Your Self-Employment Taxes

Alright, you’ve figured out your obligations and which deductions you can claim. Now for the main event: actually filing your taxes. This part can feel intimidating, but with a bit of organization, it’s a completely manageable process.

Think of it like assembling a puzzle. Once you have all the pieces laid out, they fit together logically.

The secret to a stress-free tax season is preparation. When you treat record-keeping as a year-round habit instead of a last-minute scramble, tax time just becomes a simple review of your business's financial story.

Step 1: Gather Your Essential Documents

Before you even open your tax software, get all your financial paperwork in one place. Doing this first will save you a massive headache later.

Here’s a quick checklist of what you'll need:

Income Records: Every invoice you sent, your bank statements showing client deposits, and any T4A slips you received from clients who paid you more than $500.

Expense Receipts: All receipts and statements for business expenses you’re planning to deduct, from software subscriptions to home office utility bills.

GST/HST Information: If you're a registrant, you’ll need your total sales figures and the total GST/HST you collected and paid on expenses.

Previous Year's Tax Return: Your Notice of Assessment from last year is gold. It’s super helpful for carrying forward any relevant amounts.

This is exactly where being proactive all year really pays off. If you’ve been using a tool like NeoSpend, this step is practically done. Instead of hunting through a shoebox of crumpled receipts, you can just view a clean, categorized summary of your income and expenses.

Step 2: Complete Form T2125, Statement of Business Activities

This form is the heart of your self-employment tax return. The T2125, Statement of Business or Professional Activities, is where you officially report your business’s financial performance to the CRA. You'll then attach it to your personal T1 General tax return.

Think of the T2125 as your business's annual report card. It’s broken down into a few key parts:

Business Identification: The basics—your business name, address, and industry code.

Income: This is where you report your gross business income, the total amount of money you brought in before any expenses.

Cost of Goods Sold (if applicable): If your business sells physical products, this is where you’ll calculate the cost of your inventory.

Business Expenses: This is the big one. You'll enter all your categorized expenses—advertising, office supplies, vehicle costs—on the designated lines.

Net Income (or Loss) Calculation: The form subtracts your total expenses from your gross income to find your net business income.

That final number—your net income—is the most important figure on the form. It represents your actual profit, and it's the amount you'll be taxed on.

Step 3: Transfer Your Net Income to Your T1 General Return

With the T2125 complete, the final move is to carry that net business income figure over to your personal income tax return (the T1 General). You’ll enter this number on line 13500 (Business income).

From there, your business income gets added to any other income you might have, like from investments or a part-time job. After your personal tax credits and deductions are applied, the tax software (or your accountant) will calculate your total tax bill for the year.

The Takeaway: Make Smart Tax Habits a Year-Round Routine

Let’s be honest: nobody enjoys the frantic, last-minute scramble to get their taxes done in April. Real financial peace of mind comes from building a simple, year-round system that makes tax prep feel less like a crisis and more like a routine.

It all starts with getting a handle on the fundamentals. Know what you’re responsible for: federal and provincial income tax, your double portion of CPP, and potentially GST/HST. Then, get smart about your business deductions. Every legitimate expense, from your home office to client lunches, directly lowers your taxable income.

Your Financial Co-Pilot

Staying on top of your finances and quarterly tax instalments is a must if you want to avoid a nasty surprise from the CRA. Keeping clean, continuous records goes from being a good idea to being your best friend. This is where a tool like NeoSpend can be a total game-changer.

Think of NeoSpend as more than just an expense tracker—it's your command centre for your business finances. It gives you a clear, real-time snapshot of your cash flow, helping you get ahead of the game. You can:

Save on Autopilot: Set up dedicated virtual jars to automatically stash away a percentage of every payment you receive for income tax, CPP, and GST/HST. No more guesswork.

Make Deductions a Breeze: Tag and categorize business expenses the moment they happen. When tax season rolls around, you’ll have a clean, audit-proof record ready to go.

Plan with Clarity: See your entire financial picture in one place, making it easier to budget for tax instalments while still having the confidence to invest in growing your business.

When you shift tax prep from an annual ordeal to a simple daily habit, you free up the mental space to focus on what actually matters—doing great work and building your business.

Ready to take control of your self-employed finances? Explore how NeoSpend can simplify your taxes and give you a clearer view of your money.

Burning Questions About Self-Employment Taxes in Canada

Stepping into the world of self-employment taxes can feel like learning a new language. Let's clear up some of the most common questions from Canadian freelancers and small business owners.

Do I Have to Issue a T4A Slip to Every Contractor I Pay?

Not necessarily. The CRA only requires you to issue a T4A slip to an unincorporated Canadian contractor if you've paid them $500 or more for their services within the calendar year. If the total is less than that, you don't need to issue a T4A. But remember, that payment is still a legitimate business expense, so always keep the invoice for your own records.

What Happens if I Don't File My Self-Employment Taxes?

Ignoring your taxes is one of the most expensive mistakes you can make. The CRA has steep penalties designed to get your attention.

For starters, you'll be hit with a late-filing penalty of 5% of your balance owing, plus another 1% for every full month your return is late (up to a maximum of 12 months). On top of that, the CRA charges compound daily interest on the overdue taxes and the penalties. It's a financial snowball you definitely want to avoid.

Can I Write Off My Phone Bill?

Yes, you can write off the business portion of your phone bill. If you use your personal cell phone for work, you can deduct the percentage of the bill that relates directly to your business.

You'll need to determine a reasonable percentage of your phone use that’s for earning income. For example, if you estimate that 60% of your calls, texts, and data are for your freelance business, you can claim 60% of your monthly bill as a business expense. Just be prepared to justify your calculation if the CRA ever asks.