A self-directed TFSA is a powerful financial tool that puts you in the driver's seat of your investments. Instead of being limited to the savings products your bank offers, a self-directed account lets you choose from a wide range of assets—like stocks, ETFs, and bonds—all while your money grows completely tax-free. This guide will walk you through how to use one to build wealth smarter.

What a Self-Directed TFSA Is and Why It Matters

Think of a standard TFSA at a big bank like a pre-set menu. The options are simple and safe—usually high-interest savings accounts or GICs—but they offer limited potential for growth. A self-directed TFSA, on the other hand, is like having a fully stocked kitchen. You're the chef, free to build a portfolio that perfectly matches your financial goals, whether you're saving for a down payment or building a retirement fund.

The real power of a self-directed TFSA is the control it gives you. By actively investing your money, you can unlock the potential for much higher returns than a basic savings account can offer. And because it’s a TFSA, every dollar of growth is yours to keep, completely tax-free. This tax-free compounding is one of the most significant advantages available to Canadian investors.

A self-directed account isn't just about picking stocks; it's about building a strategy based on your own goals and research. That kind of independence is what turns lofty financial goals into achievable milestones.

Unfortunately, many Canadians aren't making the most of this opportunity. A recent TD survey revealed that while 65% of Canadians have a TFSA, a staggering 39% aren't investing the cash inside it. That money is just sitting idle, losing purchasing power to inflation instead of growing. You can read more about this TFSA usage gap on stories.td.com.

Smart Tools Make It Simple

Diving into investing might seem intimidating, but modern tools have made it incredibly straightforward. This is where an app like NeoSpend can make a real difference. By connecting your self-directed TFSA, you can track your contributions and monitor your investments in the same place you manage your daily spending. NeoSpend gives you a complete, bird's-eye view of your entire financial life, making it easy to see how your portfolio is performing and ensuring you're using your contribution room effectively. It simplifies managing a powerful tool like a self-directed TFSA into a seamless part of your money routine.

Getting a Handle on TFSA Contribution Rules

To make a self-directed TFSA work for you, you need to understand the contribution rules set by the Canada Revenue Agency (CRA). These rules are designed to help you save, but knowing your limits is essential to avoid penalties.

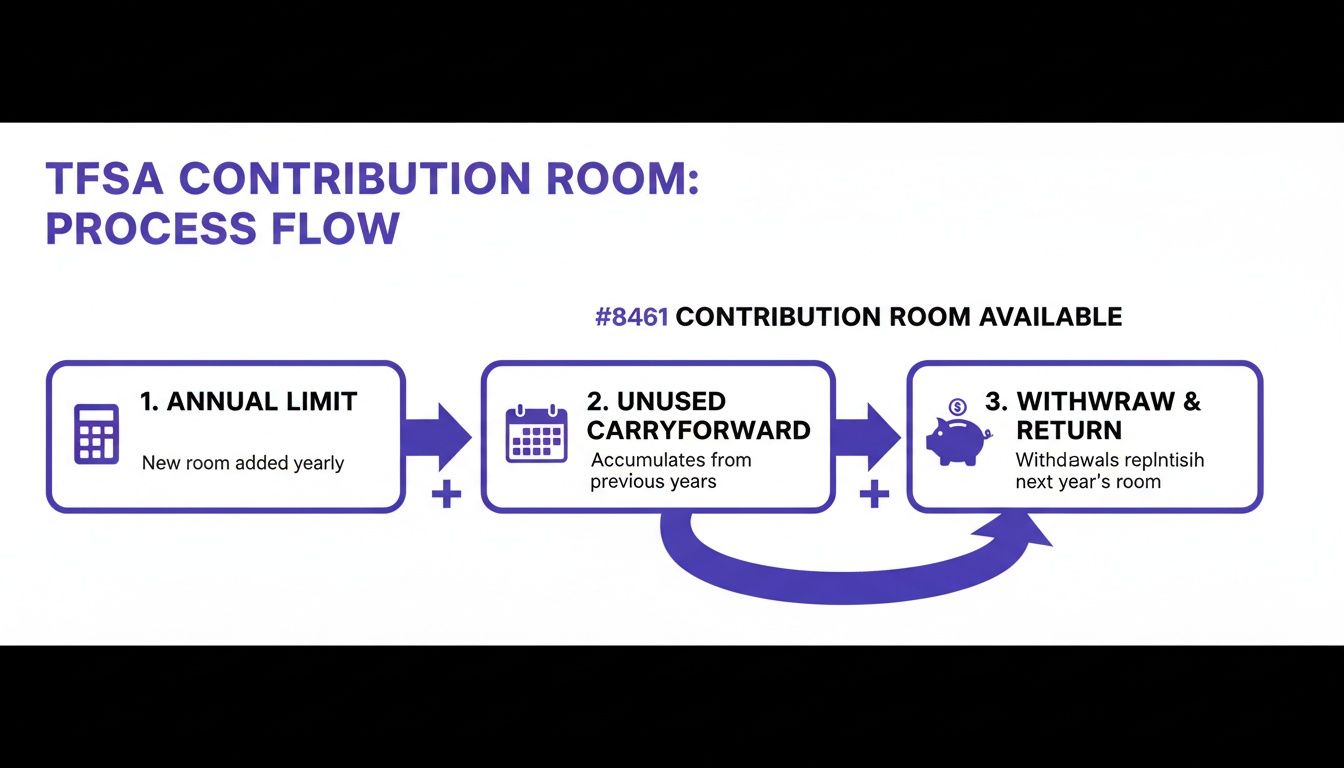

Your TFSA contribution room is the total amount you can put into all your TFSAs combined. Think of it as a running total that grows each year you're an eligible Canadian adult.

How Your Contribution Room is Calculated

Your total contribution room is the sum of three key components:

- The annual TFSA limit: This is the new contribution room you get each year. For 2024, the limit is $7,000.

- Unused room from past years: If you haven't maxed out your TFSA in previous years, that unused room carries forward indefinitely.

- Withdrawals from the previous year: In a fantastic feature, any amount you withdrew last year is added back to your contribution room on January 1st of the current year.

This carry-forward rule is a game-changer. For someone who has been eligible since the TFSA was introduced in 2009, their total cumulative contribution room has now surpassed $95,000. That’s a huge amount you can invest and grow tax-free. You can see a breakdown of these figures in the 2024 financial planning facts from Scotia Wealth Management.

Let's break it down with an example:

Imagine Liam turned 18 in 2021 but has never opened a TFSA. His total contribution room for 2024 is the sum of the annual limits from 2021 to 2024. If he deposits $15,000 this year and later withdraws $3,000 for a trip, his contribution room for next year will be his remaining room, plus the new annual limit, plus the $3,000 he took out.

The Danger of Going Over Your Limit

The CRA is strict about over-contributions. If you put in more than your available room, you'll be hit with a penalty tax of 1% per month on the excess amount. This penalty can quickly erode your investment returns. For instance, over-contributing by $2,000 would cost you $20 every month until you fix it—that's $240 a year.

To stay on track, you can check your official contribution room on the CRA's "My Account" portal. However, this number isn't updated in real-time, so you still need to track your deposits and withdrawals yourself. This is where a smart money tool like NeoSpend comes in handy. Linking your accounts to NeoSpend gives you a clear, up-to-date picture of your contributions, helping you avoid costly mistakes and invest with confidence.

Exploring Your Investment Options in a Self-Directed TFSA

This is where a self-directed TFSA truly shines. Instead of being confined to a bank’s limited selection, you get access to a vast universe of investments. You become the architect of your own portfolio, choosing assets that align with your goals, timeline, and risk tolerance.

The CRA allows a wide range of "qualified investments" within a TFSA, empowering you to go beyond a simple savings account and put your money to work in a meaningful way.

The Core Building Blocks of Your Portfolio

A solid portfolio is typically built on a foundation of proven asset classes. A self-directed TFSA lets you buy and sell these assets on your terms, with all growth remaining tax-free.

Here are the most common investment options for Canadians:

- Stocks (Equities): Buying a stock means owning a small piece of a publicly traded company. If the company does well, the value of your shares can grow, and you may also earn dividends.

- Canadian Example: You could invest in a major bank like TD, a tech leader like Shopify, or an energy company like Enbridge.

- Exchange-Traded Funds (ETFs): An ETF is like a basket holding hundreds or even thousands of different stocks or bonds. ETFs offer instant diversification, allowing you to own a piece of an entire market—like the S&P/TSX 60—in a single, low-cost transaction.

- Canadian Example: An ETF like XIC (iShares Core S&P/TSX Capped Composite Index ETF) gives you broad exposure to the Canadian stock market.

- Bonds: When you buy a bond, you're essentially lending money to a government or a corporation, which agrees to pay you back with interest. Bonds are generally considered a more stable part of a portfolio than stocks.

- Canadian Example: You could purchase a Government of Canada bond, which is among the safest investments available, or a corporate bond from a stable company.

- Guaranteed Investment Certificates (GICs): A GIC is a secure investment where you lock in your money for a set term (e.g., one to five years) in exchange for a guaranteed interest rate. Your principal investment is protected.

- Canadian Example: You can purchase GICs from various financial institutions directly through your self-directed brokerage account.

To make these investments, you need to know your TFSA contribution room. This visual breaks down how your annual limit, unused room, and withdrawals all come together.

The best part? Withdrawing money isn't a "use it or lose it" situation. The amount you take out gets added right back to your contribution room on January 1st of the next year, giving you amazing flexibility.

What You Cannot Hold in Your TFSA

While the list of qualified investments is long, the CRA has strict rules about what you can't hold. Holding a "prohibited" or "non-qualified" investment can result in severe penalties.

As a general rule, you can't hold shares of a private company in which you or a relative own 10% or more. Other prohibited assets include personal property like art or jewellery, land, or personal debts.

To stay on the right side of the rules, stick to publicly traded investments available on major stock exchanges. This ensures your focus remains on building wealth, not navigating complex tax issues. Seeing all your accounts in one place makes this easier, which is where a tool like NeoSpend can be really helpful by giving you a complete financial picture.

How to Open and Fund Your Self-Directed TFSA

Ready to get started? Opening a self-directed TFSA is surprisingly easy and can be done online in minutes. Following these steps will help you set up your tax-free investment engine for long-term success.

Step 1: Choose the Right Online Brokerage

Your online brokerage is your gateway to the investment world. While you could use your bank, many dedicated online brokerages offer lower fees and better tools. The "best" brokerage depends on your needs—a new investor might prioritize a user-friendly app and zero commissions, while an experienced one may seek advanced research tools.

To find your perfect match, compare platforms on a few key factors:

- Fees: Look for commission-free ETF purchases and low (or $0) stock trading fees. Watch out for inactivity or administration fees that can eat into your returns.

- Ease of Use: A clean, intuitive platform makes investing feel less complicated.

- Account Types: Ensure the brokerage offers a self-directed TFSA.

- Investment Selection: Confirm they provide access to a wide range of Canadian and U.S. stocks, ETFs, and other assets you want.

Checklist for Choosing a Brokerage

Use this checklist to compare different online brokerages and find the best fit for your self-directed TFSA needs.

| Consideration | What to Look For | Why It Matters |

|---|---|---|

| Trading Fees | Commission-free ETFs, low or no fees for stock trades. | High fees directly reduce your investment returns over time. |

| Account Fees | No annual, quarterly, or inactivity fees. | These fees drain your account, even when you’re not trading. |

| User Experience | An intuitive website and a well-rated mobile app. | A good platform makes managing your money easier, not harder. |

| Investment Options | Access to Canadian/U.S. stocks, ETFs, GICs, etc. | Ensures you can build the diversified portfolio you want. |

| Customer Support | Accessible phone, chat, or email support. | You want help to be available when you have questions or issues. |

| Promotions | Cash bonuses or free trades for new accounts. | A nice perk that can give your new account a small boost. |

Step 2: Gather Your Documents and Open the Account

Once you've chosen a brokerage, the online sign-up process is quick. You'll typically need:

- Your Social Insurance Number (SIN) for tax reporting.

- Personal Information (full name, date of birth, address).

- Government-Issued Photo ID (like a driver's licence or passport).

You'll also answer some standard questions about your income and investment knowledge to ensure the account is suitable for you.

Step 3: Fund Your Account and Place Your First Trade

After your account is open, it's time to add money. Most brokerages allow you to link your chequing account and transfer funds electronically. Once the funds arrive, you can make your first investment. Simply search for a stock or ETF by its ticker symbol (e.g., VCN), enter the number of shares you want to buy, and confirm the trade. Congratulations, you're officially a self-directed investor.

Transferring an Existing TFSA

If you already have a TFSA at another institution, you can move it without starting over. The key is to request a direct transfer. This official process, handled between your new and old brokerage, moves your cash and investments without affecting your contribution room. Do not withdraw the money yourself to move it, as that will be counted as a regular withdrawal. Many brokerages will even reimburse any transfer-out fees your old bank charges.

Once you’re set up, connect your new account to an app like NeoSpend. This lets you see your investments, track your contributions, and monitor performance alongside your daily spending, giving you a complete financial overview in one place.

Comparing a Self-Directed TFSA and an RRSP

In Canadian personal finance, the TFSA vs. RRSP debate is a classic. Both are fantastic tools for building wealth, but they operate differently. Understanding these differences is key to creating a financial plan that works for you. A self-directed TFSA and a self-directed RRSP both offer the freedom to invest in a wide range of assets; the main difference lies in their tax treatment.

Tax Treatment: The Core Difference

The biggest distinction between a TFSA and an RRSP is when you get your tax break.

TFSA (Tax-Free Savings Account): This is a tax-free account. You contribute with after-tax dollars, but all investment growth and withdrawals are 100% tax-free, forever.

RRSP (Registered Retirement Savings Plan): This is a tax-deferred account. Your contributions are made with pre-tax dollars, meaning you get a tax deduction that lowers your taxable income for the year. The catch is that you must pay income tax on all withdrawals in the future.

Simply put: with a TFSA, you pay tax on the seed, not the harvest. With an RRSP, you get a tax break on the seed, but you owe tax on the entire harvest when you collect it.

Contributions and Withdrawals

Their different purposes are also reflected in how you contribute and withdraw money.

A self-directed TFSA offers maximum flexibility. You can withdraw funds at any time for any reason, tax-free. Plus, the amount you withdraw is added back to your contribution room the following year.

An RRSP is designed for long-term retirement savings. Contributions provide an immediate tax refund, which is especially valuable for high-income earners. However, withdrawals are taxed as income, and you permanently lose that contribution room.

For most Canadians, the question isn't TFSA or RRSP. It's about how to use them together. A smart combination is often the most powerful way to build wealth and manage your taxes throughout your life.

Which Account Should You Prioritize?

The best choice often depends on your income and financial goals.

Scenario 1: The Young Professional Saving for a Home

Meet Chloe. She’s 27, earns $60,000 a year, and is focused on saving for a down payment. Her priority should be her self-directed TFSA. Why? Her income is in a lower tax bracket, making the RRSP deduction less impactful. More importantly, when she’s ready to buy a home, she can withdraw her entire down payment tax-free.

Scenario 2: The High-Income Earner Planning for Retirement

Now consider Mark. He’s 42, earning $140,000 a year, and his main goal is retirement. For him, the RRSP is a clear winner. The tax deduction at his income level is substantial, saving him thousands each year. He anticipates being in a lower tax bracket in retirement, meaning he'll pay less tax on withdrawals later than he would today.

Juggling both accounts can be complex. This is where a smart tool like NeoSpend becomes your co-pilot. By linking all your accounts, you can see your TFSA and RRSP contributions in one dashboard, making sure you never over-contribute and can make smart calls about where your money will work hardest for you.

Common Mistakes to Avoid With Your Self-Directed TFSA

Taking control of your investments with a self-directed TFSA is a smart financial move. However, this power comes with the responsibility to avoid common pitfalls that can cost you money and attract penalties from the CRA.

Over-Contributing and Ignoring Penalties

This is the most frequent and costly mistake. It's easy to lose track of contributions, especially with multiple TFSA accounts. The CRA imposes a penalty tax of 1% per month on any amount over your limit. To avoid this, always confirm your contribution room on the CRA website before making a large deposit. An even better solution is to use a tool like NeoSpend. By linking your accounts, its dashboard provides a real-time view of your contributions, helping you stay safely under your limit.

Letting Cash Sit Idle

Faced with thousands of investment choices, some people experience "analysis paralysis" and leave their contributions as uninvested cash. This defeats the purpose of the account, as cash earns little to no return and loses value to inflation over time. Your TFSA is a growth engine, not a piggy bank. Make a plan to invest your money shortly after depositing it. Even starting with a simple, diversified ETF is a great first step.

"The biggest risk of all is not taking one." - Mellody Hobson

Engaging in Day Trading

Your TFSA is designed for long-term investing, not active day trading. If the CRA determines you are operating your account like a business—characterized by frequent, speculative trades—they can revoke its tax-free status. This would make all your gains fully taxable. Focus on building a diversified portfolio for the long haul rather than trying to time the market.

Other Critical Oversights to Avoid

- Forgetting to Name a Beneficiary: This simple step is crucial. Designating a beneficiary (or a successor holder for a spouse) ensures your TFSA assets pass to your loved ones smoothly and tax-free, outside of your estate.

- Holding Non-Qualified Investments: Stick to publicly traded stocks, ETFs, bonds, and GICs. Venturing into prohibited assets like private company shares can trigger severe tax penalties.

Your Top Self-Directed TFSA Questions, Answered

Here are answers to some of the most common questions about managing a self-directed TFSA.

Can I Have More Than One TFSA Account?

Yes, you can open as many TFSA accounts as you wish at different financial institutions. However, your annual contribution limit is a single, total amount shared across all of your accounts. It's your responsibility to track your total contributions to avoid penalties.

What Happens if I Move Out of Canada?

You can keep your existing TFSA if you become a non-resident of Canada, and the investments will continue to grow tax-free from a Canadian perspective. However, you cannot contribute any more money to it. Any contributions made while you are a non-resident will be subject to a 1% penalty tax per month. Be aware that your new country of residence may have its own tax rules for the income earned in the account.

Is the Money in My Self-Directed TFSA Protected?

Yes, in most cases. If your brokerage is a member of the Canadian Investor Protection Fund (CIPF), your assets are protected up to $1 million in the event the firm becomes insolvent. This coverage applies to your cash and securities across all your general accounts (like your TFSA and RRSP). It's important to know that CIPF does not protect you from market losses if your investments decrease in value.

Managing a self-directed TFSA, tracking your budget, and hitting your savings goals can feel overwhelming. NeoSpend simplifies your financial life by bringing everything together in one powerful app. Get a clear, real-time picture of your investments, spending, and progress. Explore how NeoSpend can help you manage your money smarter by visiting https://neospend.com or checking out our other financial guides.