When it comes to managing your money, the difference between a savings and a chequing account comes down to one simple idea: purpose.

A chequing account is your daily financial hub—it’s for paying bills, buying groceries with your debit card, and handling your day-to-day cash flow. Think of it as your digital wallet. A savings account, on the other hand, is for setting money aside for your future goals. It’s your modern piggy bank, but better, because it earns interest and helps your money grow.

Chequing vs Savings Accounts: At a Glance

Understanding how to use these two accounts is the first step toward building a solid financial foundation in Canada. Your chequing account is your financial command centre, designed for a high number of transactions. It’s where your paycheque lands and where you pull money from for everything life throws at you, from your morning Tims run to your monthly rent payment.

Your savings account is your goal fund. Its main job is to keep your money safe while it quietly earns interest, helping you save for something specific. That could be an emergency fund, a down payment on a condo in Toronto, or a dream family vacation to Banff.

The core idea is simple: money for today lives in your chequing account, and money for tomorrow lives in your savings. Keeping them separate is the easiest way to make sure you don't accidentally spend your future on today's expenses.

To really nail down the differences, let’s break it down feature by feature. This table gives you a quick snapshot of how each account is designed to handle a different part of your financial life.

Chequing vs Savings Accounts At a Glance

| Feature | Chequing Account | Savings Account |

|---|---|---|

| Primary Purpose | Daily transactions and bill payments | Storing money for future goals |

| Interest Earnings | Typically 0% or very low interest | Earns interest to grow your money |

| Typical Fees | Monthly maintenance, e-Transfer fees | Fewer fees, but transaction limits |

| Access to Funds | High (debit card, cheques, e-Transfers) | Lower (fewer free withdrawals) |

| Best For | Managing monthly cash flow, paying bills | Building an emergency fund, saving for a car |

When you use both accounts the right way, you can keep your daily finances running smoothly while still making steady progress on your big-picture goals. An app like NeoSpend makes this even easier by showing you both accounts in one place, so you always know where your money is and how it’s working for you.

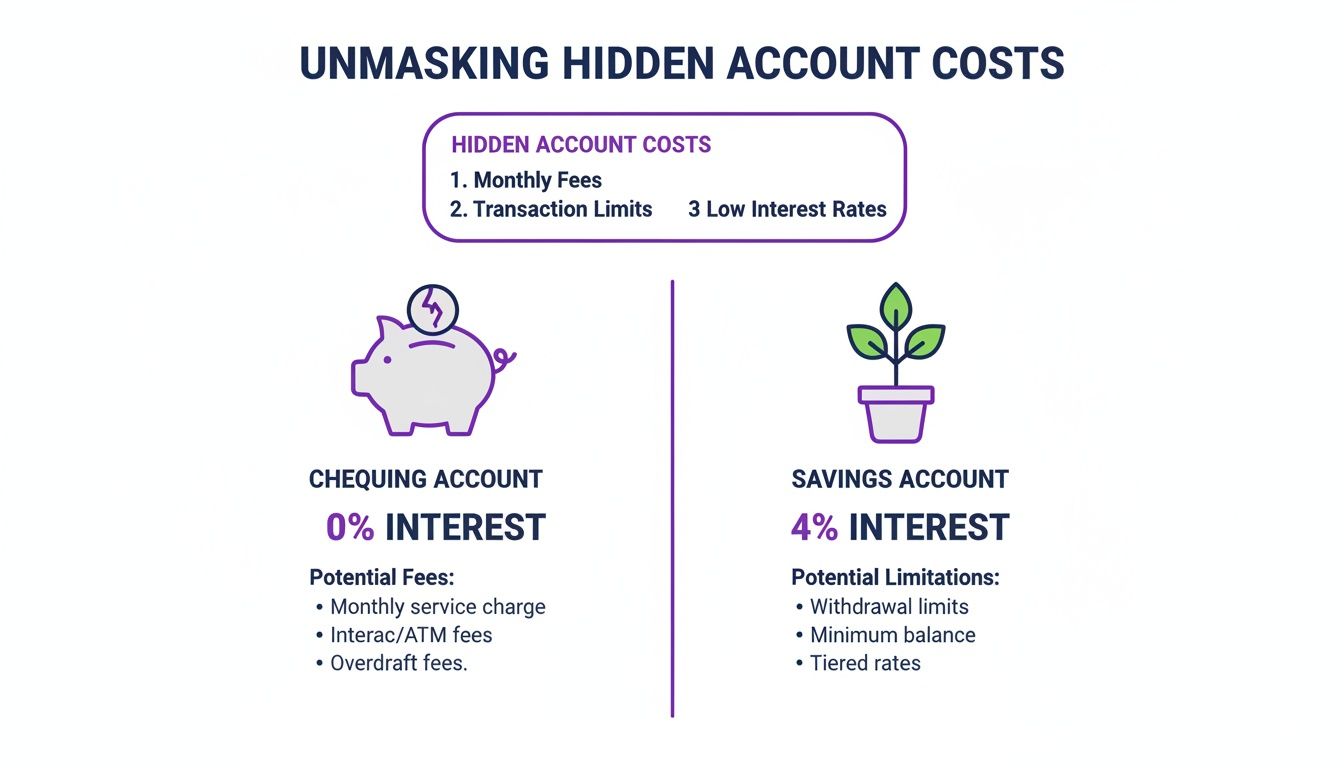

The Hidden Costs of Choosing the Wrong Account

Picking the wrong bank account is like trying to fill a bucket with a hole in it. You keep pouring your money in, but it’s slowly leaking out without you noticing. The biggest leak? Keeping too much cash in a chequing account.

These accounts are workhorses for day-to-day spending, but most of them pay you 0% interest. That means your money isn't working for you; it's just sitting there, losing its buying power to inflation every single day.

Let's use a real-world Canadian example. Imagine you've saved $10,000 for a down payment on a new car and it's just sitting in your chequing account. If that account earns nothing, five years from now, you'll still have exactly $10,000. The problem is, that $10,000 won't buy you as much car as it does today, thanks to Canada's rising cost of living.

The Opportunity Cost of Zero Interest

Now, what if you had moved that same $10,000 into a high-interest savings account (HISA) earning a modest 3% per year? After five years, the magic of compounding would turn your balance into roughly $11,592.

That’s nearly $1,600 you could have earned, just by putting your savings in the right place. That's the definition of opportunity cost—the gain you give up when you choose one option over another.

And this isn't a small problem. A recent J.D. Power study found that while people are happier with mid-size banks for their daily transactions, a ton of Canadians still stash their savings in low-yield accounts at the big banks. It’s a habit that costs you, especially when that extra interest could have been used to pay down debt or boost your savings. You can learn more about these banking trends and what they mean for your money.

Death by a Thousand Fees

It's not just about the interest you're missing out on. Chequing accounts can also nickel-and-dime you to death with fees. Sure, some premium accounts might waive them if you keep a hefty balance, but many standard accounts come with a lineup of charges that add up fast.

Here are the usual suspects to watch for in Canada:

- Monthly Maintenance Fees: Just for having the account, you could be paying anywhere from $4 to $30 a month.

- Transaction Limits: Go over your monthly limit for debit purchases or withdrawals, and you’ll get hit with per-item fees.

- e-Transfer Fees: Some are free, but many accounts start charging after a certain number of transfers, often about $1.50 a pop.

- Overdraft Fees: Accidentally spend more than you have? That mistake could cost you a $50 fee, plus interest on the overdrawn amount.

These little charges might not seem like a big deal on their own, but they create a slow, steady drain on your balance. The best way to fight back is to get proactive. Using an app like NeoSpend to keep an eye on your balances and track fees can turn your banking from a chore into a powerful tool for building wealth.

A Detailed Breakdown of Account Features

To really get the difference between a savings and a chequing account, we have to look past the simple "spending vs. saving" label. The true story is in the details—the interest rates, the fees, and how easily you can get to your cash. Each feature is a trade-off between everyday convenience and your long-term ability to build wealth.

Let’s break these features down with some real-world Canadian examples to see how they actually play out in your financial life.

Interest Rates: The Engine of Growth

A chequing account is built for one thing: frequent transactions. It was never designed to grow your money. In fact, most chequing accounts in Canada offer a grand total of 0% interest. Any money just sitting there is actively losing its buying power to inflation. It's a slow leak you might not even notice.

On the flip side, a savings account is specifically designed to put your money to work. High-interest savings accounts (HISAs) are especially great for this. Imagine a family in Halifax saving $5,000 for a trip to Disney World. A HISA earning 3-4% annually could add over $150 to their fund in a single year from compounding growth, all without them having to lift a finger.

The bottom line is simple: keeping large sums of cash in a chequing account comes with an invisible cost. You’re not just missing out on potential earnings; you're letting inflation quietly eat away at your savings.

This infographic paints a pretty clear picture of the growth potential between the two.

You can see how a chequing account can feel like a leaky bucket for your wealth, while a savings account helps it grow steadily over time.

To give you a clearer side-by-side view, let's put these core features into a table. This helps break down exactly what you're getting—and what you're giving up—with each account type.

Detailed Feature Comparison: Chequing vs. Savings

| Feature Analyzed | Chequing Account (For Spending) | Savings Account (For Growing) | Key Takeaway for Canadians |

|---|---|---|---|

| Interest Rate | Typically 0%. Your money is sitting idle, not earning anything. | Can be 3-5% or higher with a good HISA. Actively grows your money. | Parking large sums in a chequing account means you're losing money to inflation. |

| Transaction Access | High. Unlimited debit, e-Transfers, and ATM withdrawals are common. | Low. Often limited to 1-2 free withdrawals per month. | Chequing is built for daily use; savings is built to discourage frequent access. |

| Monthly Fees | Common. Often $4-$30 unless you maintain a minimum balance. | Rare. Most high-interest savings accounts have no monthly fees. | You're paying for convenience with a chequing account. Savings accounts are typically free. |

| Primary Purpose | Day-to-day cash flow management: paying bills, buying groceries, receiving pay. | Earmarked savings: emergency funds, vacation goals, down payments. | Use the right tool for the right job to avoid unnecessary fees and lost growth. |

This table isn't just about features; it's about strategy. The goal is to use each account for its intended purpose to maximize your financial health—get the convenience you need without sacrificing the growth you want.

Accessibility and Transaction Limits: The Convenience Factor

Chequing accounts are all about easy access. They come loaded with debit cards, chequebooks, and often unlimited e-Transfers, making them the perfect hub for your daily life. A freelance graphic designer in Vancouver, for example, absolutely needs those unlimited e-Transfers to get paid by clients and pay contractors without running into annoying and costly limits. That immediate, unrestricted access is key to managing her business cash flow.

Savings accounts, on the other hand, deliberately put up some roadblocks. Banks do this to encourage you to leave your money alone so it can actually grow. You might get one or two free withdrawals a month, but after that, you could be looking at fees of $5 or more for every transaction. This friction is a feature, not a bug—it makes you think twice before dipping into your savings for non-emergencies.

This is where a tool like NeoSpend can help you find that perfect balance. By seeing all your accounts in one dashboard, you can easily keep just enough cash in your chequing for the month's expenses while making sure every other dollar is parked in a HISA, earning interest and pushing you toward your goals. That unified view from NeoSpend helps you manage money smarter by stopping you from accidentally leaving too much idle cash in a zero-interest account.

Making It Work: Real-Life Canadian Scenarios

Knowing the difference between a chequing and a savings account is great, but the real magic happens when you use them to organize your financial life. There’s no single “right” way to set up your accounts; it all comes down to your income, your goals, and your lifestyle.

Let’s look at how a few different Canadians might set up their finances.

The Student in Montreal

Meet Sophie. She's a university student in Montreal, working part-time at a café to cover her tuition, rent in the Plateau, and her STM pass. Her income is modest, so every dollar has a job.

- Her Chequing Account: This is her mission control. Her paycheque lands here, and it’s what she uses for everything—from textbooks and groceries to grabbing a late-night poutine with friends. She uses a no-fee student account with unlimited e-Transfers so she can easily pay her roommate her share of the rent.

- Her Savings Account: Sophie opened a high-interest savings account (HISA) with one goal: a semester abroad. She set up an automatic transfer of $50 for every payday. It’s consistent, and the high interest gives her a small boost. By keeping this money separate, she's not tempted to dip into her travel fund for everyday spending.

The Family in Calgary

Now let's head west to Calgary and meet the Chens. They're juggling a mortgage, two kids, and car payments, which means their financial life has a few more moving parts. They need a system to manage daily expenses while saving for big-picture goals.

Here’s their setup:

- Joint Chequing Account: This is the household’s nerve centre. Both their salaries get deposited here, and all recurring bills are paid from this account—the mortgage, utilities, car insurance, and groceries.

- Emergency Fund HISA: In a separate HISA, they’ve stashed six months of living expenses. This money is off-limits. It's their safety net for when life happens, like the furnace inevitably dying during a Calgary cold snap.

- Goal-Specific Savings Accounts: The Chens also have a couple of other savings accounts. One is for their annual family trip, and the other is for topping up their kids' RESPs. By creating these "buckets," they can clearly see their progress toward each goal.

This multi-account strategy gives the Chens total clarity. They know precisely what’s for bills and what’s for the future, which makes budgeting feel less like a chore and more like a plan.

The Gig Worker in Vancouver

Finally, there’s Liam, a freelance web developer in Vancouver. His income fluctuates—some months are great, others are quiet. A rigid budget doesn't work for him, so his biggest challenge is managing inconsistent cash flow while saving for taxes and his own goals.

Liam's strategy is all about creating structure:

- A Business Chequing Account: Every client payment lands here first. He uses this account strictly for business costs, like software subscriptions and co-working space fees.

- A Personal Chequing Account: Liam pays himself a steady "salary" every two weeks, transferring a set amount from his business account to his personal one. This creates the predictability he needs for his personal life.

- A "Tax" Savings Account: This is non-negotiable. The moment a client payment comes in, he skims 30% off the top and moves it into a dedicated HISA for his income tax and GST/HST. Come tax season, there are no nasty surprises.

For all these different scenarios, an app like NeoSpend can be a game-changer. It pulls all your different accounts into one dashboard, so you can see the whole picture at a glance. It makes it easy to track those automated transfers and make sure every single dollar is working for you, whether it’s for today’s coffee or tomorrow’s dreams.

How to Structure Your Accounts for Financial Success

Knowing the difference between a savings and a chequing account is one thing, but making them work together is where you can really build wealth. A smart account structure isn't just about storing your money; it’s about creating an automated system that actively helps you reach your goals.

The core idea is to treat your savings like your most important bill. This is the classic "pay yourself first" method, and it’s the single most effective way to guarantee you’re putting money toward your goals every month.

Instead of just saving whatever is left over after all your spending (which is often nothing), you flip the script. The moment your paycheque lands in your chequing account, an automatic transfer should move a set amount straight into your savings. This simple automation takes willpower completely out of the equation.

The Power of Financial Bucketing

Once your savings are on autopilot, the next step is to give every dollar a specific job. We call this financial bucketing, and it’s as simple as setting up different savings accounts for different goals. This strategy brings incredible clarity and motivation, and it stops you from accidentally raiding your house down payment fund for a weekend trip.

Here’s a simple but incredibly effective setup for most Canadians:

- One Primary Chequing Account: This is your financial command centre. All income flows in, and all daily bills and expenses flow out. Keep just enough in here to cover monthly costs, plus a small buffer.

- One Emergency Fund HISA: This is your top-priority savings bucket. Set up automatic transfers until you have 3-6 months of essential living expenses saved. This account is only for true emergencies—like a sudden job loss or a burst pipe, not a sale on a new TV.

- Multiple Goal-Specific Savings Accounts: This is where it gets fun. Create separate high-interest savings accounts for your other big goals, like a new car, a European vacation, or a wedding. Give them specific names like "Hawaii Fund" or "New Car 2026." It makes the goals feel real and keeps you motivated.

This approach is more important than ever. While Canadians have traditionally been good savers, recent trends show household savings rates are dipping. Way too many people leave extra cash sitting in their chequing accounts earning 0%, missing out on the compounding power of a savings account. You can dive deeper into how Canadian savings habits are changing and what it means for your financial strategy.

Your Financial Control Centre

Structuring your accounts this way creates a goal-achieving machine. But juggling multiple accounts can feel like a headache. That’s where a tool like NeoSpend can step in and act as your financial control centre.

NeoSpend gives you a single, unified view of all your accounts—chequing, savings, and investments—in one clean dashboard. Its AI-powered engine analyzes your cash flow, spots idle cash sitting in your low-interest chequing account, and suggests optimal transfers to your different savings buckets. NeoSpend helps you be proactive, making sure every dollar you have is working as hard as it can for you.

Your Top Questions About Savings and Chequing Accounts

Even after you understand the basics of chequing vs. savings, practical questions always come up. Getting these details right is what separates a messy financial life from a smooth, confidence-boosting one.

Let's clear up some of the most common questions Canadians have.

How many bank accounts should I have?

There's no single right answer, but for most people, the sweet spot is at least three accounts. This creates a simple, powerful system for managing your money.

- One Chequing Account: This is your command centre for day-to-day cash flow. All income lands here, and all daily bills and debit purchases flow out.

- One Emergency Fund Savings Account: This is non-negotiable. It’s your financial safety net, holding three to six months of essential living expenses for true, unexpected emergencies only.

- One Goal-Specific Savings Account: Saving for a down payment, a trip to Europe, or a new car? Give that goal its own dedicated account. Watching the balance grow is incredibly motivating and keeps you from accidentally spending your savings.

This three-part structure creates a clear boundary between money for spending, money for emergencies, and money for your future.

What is a high-interest savings account?

A high-interest savings account (HISA) is essentially a savings account that works much harder for you. While a regular savings account at one of the big banks might offer a tiny sliver of interest (if you’re lucky), a HISA is designed to actually help your money grow with a competitive interest rate.

We’re talking about interest rates that are often 3% to 5% or even higher, which is a world away from the near-zero rates you’ll find elsewhere.

Think of it this way: a standard savings account is like a safe—it just holds your money. A HISA is more like fertile soil—it holds your money and helps it grow. If you're serious about reaching your savings goals faster, a HISA isn't just nice to have; it's essential.

The real difference isn't just about safety; it's about momentum. A HISA accelerates your progress toward your financial goals without adding the risk of investing.

Apps like NeoSpend can be a huge help here. They can track down the best HISA rates for you, making sure your cash is always parked in the most profitable spot.

Can I pay bills from a savings account?

You can, but you absolutely shouldn't. Savings accounts are built for saving, not spending. To discourage you from dipping into them too often, banks usually limit the number of free transactions you can make each month—often just one or two.

If you go over that limit, you'll get hit with fees, sometimes around $5 for every extra transaction. Those fees will quickly erase any interest you’ve earned.

Here’s the simple, fee-free way to do it:

- Set up all your bill payments to come directly from your chequing account. It’s built for this kind of activity.

- If you need to tap into your savings to cover a bill, transfer the exact amount you need over to your chequing account first.

- Pay the bill from your chequing account as you normally would.

This simple two-step process keeps your accounts clean, helps you avoid fees, and reinforces the discipline of separating your spending money from your savings.

Is an emergency fund a savings account?

Yes, your emergency fund should absolutely be kept in a savings account—specifically a high-interest one. What makes it an "emergency fund" is its purpose, not the account type itself.

While your other savings accounts might be for exciting, planned goals like a vacation or a new car, your emergency fund is a critical pot of money set aside for the truly unexpected: a sudden job loss, a major car repair, or a surprise medical bill.

This isn't just semantics; it's a crucial mindset shift. Your emergency fund is a firewall between you and financial disaster. It needs to be liquid (easy to access), which is why a HISA is the perfect place for it. You get a solid interest rate, but the money is there the second you need it without any penalties.

The Takeaway: Using chequing and savings accounts for their intended purposes is the foundation of smart money management. Keep your daily spending money in a chequing account and let the rest of your cash grow in high-interest savings accounts dedicated to specific goals. This simple strategy protects your savings, helps you avoid fees, and accelerates your journey to financial success.

Ready to see everything in one place and make every dollar work harder? Take control of your finances today with NeoSpend. Explore how our AI-powered insights can help you optimize your savings and chequing accounts for success. Learn more at NeoSpend.