Ever wonder how long it’ll take for your savings to actually grow? The Rule of 72 is a brilliant mental shortcut that gives you a surprisingly good estimate, fast. It’s a simple way to figure out how many years you’ll need for an investment to double in value based on its annual interest rate. The best part? All you do is divide 72 by the rate of return.

Your Quick Guide to the Rule of 72

In the world of personal finance, the Rule of 72 is one of the most practical tricks you can learn. It demystifies the power of compound interest without forcing you to pull out a complicated calculator. For any Canadian trying to map out their financial future, this back-of-the-napkin formula is a total game-changer, turning abstract goals into a concrete timeline.

Whether you're saving for a down payment in your Tax-Free Savings Account (TFSA) or trying to picture how your Registered Retirement Savings Plan (RRSP) might look in 20 years, the rule provides instant clarity. It’s the perfect tool for making quick comparisons between different investment options on the fly.

How the Rule of 72 Works

The formula is so simple you’ll have it memorized in seconds. All you need is one number: the annual rate of return you expect to earn.

Years to Double = 72 / Annual Interest Rate

Let's say you have an investment that's earning an average of 6% per year. Just do the math: 72 ÷ 6 = 12. That's it. It’ll take about 12 years for your money to double. This one simple calculation helps you visualize your financial journey and start making smarter choices.

This infographic breaks down how different rates of return can drastically speed up your money's growth, comparing some common investment vehicles you'll find in Canada.

As you can see, even a small bump in your annual return can shave years off the time it takes to double your investment.

Applying the Rule to Your Finances in Canada

Getting a handle on this concept is your first step toward taking real control of your financial goals. You can use this rule for almost any scenario where your money is growing over time.

Setting Savings Goals: Figure out how long it might take to double the money in your TFSA or hit another key savings target.

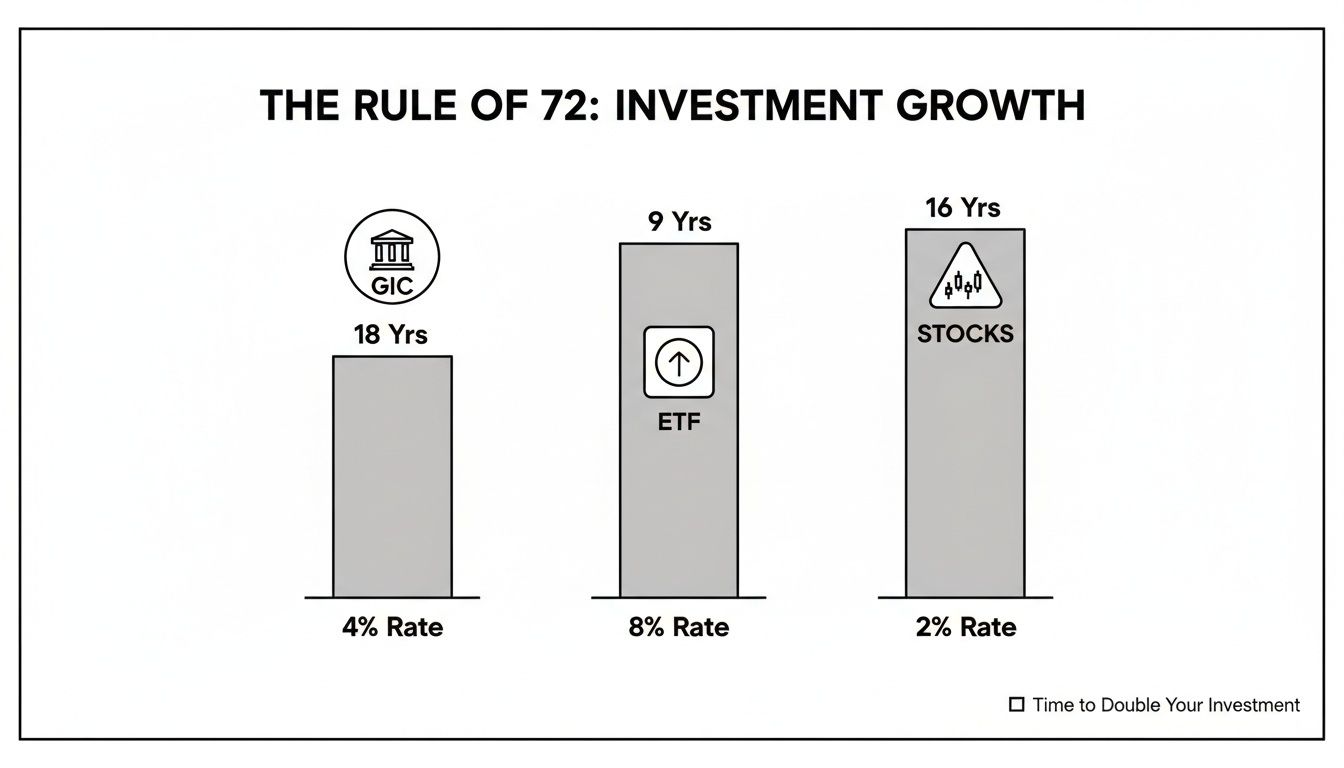

Evaluating Investments: Quickly size up the difference between a GIC offering 4% versus a balanced ETF portfolio that’s aiming for 8%.

Planning for Retirement: Get a rough idea of how your RRSP contributions today could multiply by the time you're ready to retire.

Once you internalize this simple rule, you’ll find yourself making more informed decisions that line up with your long-term plans. From there, smart tools like NeoSpend help you keep an eye on your progress. It automatically tracks your finances so you always know exactly where you stand. Combining quick estimates from the Rule of 72 with detailed tracking is a powerful way to build wealth more effectively.

The Power of Compounding Explained

Ever wonder how some people’s investments seem to explode over time while others just... don't? The not-so-secret ingredient is compound interest. And the Rule of 72 is your shortcut to understanding its incredible power.

Think of it like rolling a snowball down a snowy hill in Banff. At first, it's small. But with every rotation, it picks up more snow, getting bigger and faster as it goes. That’s exactly how compounding works with your money.

Your investment earns interest. Simple enough. But then, the next year, you earn interest on your original money plus all the interest you’ve already piled up. This is where the magic happens—your earnings start generating their own earnings, creating a growth cycle that can seriously build wealth.

Breaking Down the Magic of Compounding

Let’s keep it simple. With simple interest, if you invest $1,000 at a 5% return, you make a flat $50 every single year. After two years, you’ve got your initial $1,000 plus $100. It's predictable, but it’s slow.

Compound interest, on the other hand, builds on itself. That first year, you still make $50. But in the second year, you earn 5% on the new total of $1,050, which comes out to $52.50. It might not sound like a huge difference, but fast-forward a few decades, and this accelerating growth can lead to a massively different outcome.

This is exactly why the Rule of 72 is so brilliant. It cuts through the complex math to give you a clear picture of how compounding works for you.

Years to Double = 72 / Interest Rate

This handy formula tells you, in seconds, how long it’ll take for compounding to double your money. It makes an abstract financial concept feel real and tangible.

Why Does the Number 72 Work So Well?

You might be asking, "Why 72? Why not 70 or 75?" The number 72 is just a fantastic shortcut. While the exact math involves more complicated logarithmic formulas (the true number is closer to 69.3), 72 is a clear winner for one simple reason: it's incredibly easy to divide.

Think about it—72 is divisible by tons of common interest rates like 2, 3, 4, 6, 8, 9, and 12. This makes quick mental math a breeze for any Canadian trying to get their finances sorted.

Let's look at some real-world examples:

At 4% interest (like a GIC): 72 / 4 = 18 years to double your money.

At 8% interest (a balanced ETF portfolio): 72 / 8 = just 9 years to double.

At 12% interest (a growth-focused fund): 72 / 12 = a speedy 6 years to double.

This simple division shows you just how much your rate of return matters. A higher rate doesn't just earn you more money—it doubles your investment dramatically faster.

Grasping this core idea empowers you to make smarter financial moves. It highlights why starting early is such a game-changer and how small bumps in your returns can create huge wealth over your lifetime. To make this even easier, you can link your accounts to an app like NeoSpend, which puts all your financial performance data in one place. Seeing your real-time returns helps you apply the Rule of 72 to your own situation, turning theory into a powerful, actionable strategy.

Putting the Rule of 72 to Work in Canada

Knowing the theory is one thing, but seeing the Rule of 72 in action with real Canadian dollars is where it really clicks. This simple trick can take your financial planning from fuzzy guesswork to a clear, actionable strategy. It’s all about visualizing your goals and understanding how different choices can speed up—or slow down—your journey.

Let's ditch the abstract numbers and apply the rule to situations Canadians face every day, from saving for a first home in Halifax to building a retirement nest egg in Victoria.

Real-World Canadian Investment Scenarios

Imagine you’ve just put $10,000 into your Tax-Free Savings Account (TFSA). The goal? Turn it into $20,000. So, how long will it take? The Rule of 72 gives you a surprisingly sharp estimate based on where you put that money.

Let’s look at two common paths a Canadian investor might take:

Scenario 1: The Cautious Saver: You park your $10,000 in a Guaranteed Investment Certificate (GIC) earning a fixed 4% return each year.

The Math: 72 ÷ 4 = 18 years

The Result: Your money will take about 18 years to double to $20,000. It's a safe and steady route.

Scenario 2: The Balanced Investor: You invest the $10,000 in a balanced Exchange-Traded Fund (ETF) portfolio that has historically averaged an 8% annual return.

The Math: 72 ÷ 8 = 9 years

The Result: In this case, your investment doubles in just 9 years—literally half the time it would take with the GIC.

This simple comparison gets to the heart of investing. Taking on a bit more calculated risk can seriously accelerate how quickly you build wealth, helping you hit your financial milestones that much sooner.

Key Takeaway: The Rule of 72 isn't just math; it’s a powerful decision-making tool. It lays bare the trade-off between risk and time, helping you pick investments that actually fit your personal timeline.

The Rule of 72 is like a secret weapon for seeing the magic of compound interest. Think about the S&P/TSX Composite Index, which many Canadians invest in through their TFSAs or RRSPs. If it averages a return of around 9%, the Rule of 72 shows it would take roughly 8 years for an investment to double at that rate (72 ÷ 9 = 8).

So, if you had started with $10,000 in a TSX index fund, you could have expected it to hit $20,000 in about 8 years and then $40,000 after 16 years, assuming those returns held steady.

Using the Rule of 72 for Goal Setting

The Rule of 72 isn't just for looking forward; you can also flip the formula around to figure out the return you need to hit a specific goal. This makes it an amazing tool for setting realistic financial targets.

Let’s say a young professional in Toronto wants to double their $50,000 RRSP contribution in the next decade to get their retirement savings on track.

Goal: Double $50,000 in 10 years.

Flipped Formula: Required Rate = 72 / Years to Double

Calculation: 72 ÷ 10 years = 7.2%

To hit that target, they need to find investments capable of delivering an average annual return of at least 7.2%. This simple calculation gives them a clear benchmark to use when looking at different mutual funds, ETFs, or stocks for their RRSP.

It works for other goals, too. A family in Calgary saving for a down payment can use the same logic. If they have $40,000 today and need $80,000 in six years, they’ll quickly see they need a 12% return (72 ÷ 6 = 12). That might be the wake-up call that a standard savings account won't cut it, pushing them to explore higher-growth investment strategies.

Track Your Progress with Smart Tools

Setting these goals is the first step. But tracking your progress is what keeps you on the path to actually achieving them. This is where modern financial tools can make all the difference.

Once you’ve used the Rule of 72 to sketch out your financial roadmap, an app like NeoSpend automates the tracking for you. By linking your accounts, you get a clean, all-in-one view of how your portfolio is actually performing. You can see your real rate of return and compare it directly to the target rate you calculated.

This connection between a quick estimate and real-time data empowers you to make smarter moves. If your returns are lagging, maybe it’s time to rebalance your portfolio. If you're ahead of schedule, you can celebrate a milestone or maybe even set a more ambitious goal. NeoSpend helps close the loop, turning a simple rule of thumb into a dynamic, personalized financial plan.

The Hidden Dangers of Debt and Inflation

The Rule of 72 is fantastic for watching your investments grow, but it has a dark side. It's just as good at showing how quickly things can go wrong when compounding works against you. Think high-interest debt and the silent creep of inflation.

Knowing this isn't just about getting rich; it's about protecting what you have. When you apply the Rule of 72 to debt, you get a chilling look at how a small balance can explode into a real financial headache. It’s a bright red warning sign for anyone juggling credit card debt or expensive loans in Canada.

How Compounding Works Against You With Debt

High-interest debt is basically an investment in reverse. Instead of your money making more money for you, the lender’s money is making more money off you—and fast. Every single day you carry that balance, the interest piles on, growing the total you owe.

Let's look at a classic Canadian scenario: a store credit card with a punishing 20% Annual Percentage Rate (APR). Run that through the Rule of 72 and the result is pretty shocking:

72 ÷ 20% APR = 3.6 years

That’s right. An unpaid balance on that card could double in under four years. That $2,500 you spent on new furniture? It can easily become a $5,000 problem, trapping you in a cycle of minimum payments that barely make a dent in the original amount.

The math reveals just how terrifyingly fast high-interest debt can grow. It's not uncommon for some Canadian credit cards to have an average 24% APR. Plug that in: 72 ÷ 24 = 3 years. That $5,000 vacation you put on a credit card could balloon to $10,000 in just 36 months if you're not paying it down aggressively.

Now, compare that to a typical high-interest savings account. A modest 2% rate means your emergency fund will take 36 years to double (72 ÷ 2 = 36). It's a stark contrast that shows just how powerful these rates can be, for good or for bad. You can find more insights on how interest rates impact your finances over at PocketGuard.com.

How the Rule of 72 Impacts Your Money

This simple calculation reveals two very different financial stories: one of growth and one of erosion. Here's a quick comparison of how the Rule of 72 plays out with your investments versus your debts.

| Scenario | Annual Rate (%) | Effect on Your Money | Time to Double or Halve |

|---|---|---|---|

| Investing in an RRSP | 8% | Your investment doubles in value | 9 years |

| Holding Cash | 3% (Inflation) | Your money's buying power is cut in half | 24 years |

| Credit Card Debt | 22% | The amount you owe doubles | 3.3 years |

| Personal Loan | 11% | The amount you owe doubles | 6.5 years |

As you can see, compounding is a powerful force. When it’s on your side, it builds wealth steadily. When it’s working against you through high-interest debt, it can sink your finances just as quickly.

The Silent Thief: Inflation

Inflation is the other major threat to your money. It's the slow, steady rise in the cost of everything, which means the cash you have today will buy less tomorrow. The money you've tucked away in a low-interest savings account might feel safe, but inflation is quietly chipping away at its value every single day.

The Rule of 72 does a great job of showing just how serious this is. If Canada’s long-term inflation rate hovers around 3%, we can figure out how long it takes for your money’s value to get cut in half:

Calculation: 72 ÷ 3 (inflation rate) = 24 years

The Impact: In 24 years, every $100 you have saved today will only have the purchasing power of $50.

This really hammers home a critical financial truth: just saving isn't enough. To actually build wealth and secure your future, your money has to grow faster than inflation. If your investments are earning 4% while inflation is at 3%, your real rate of return is only 1%.

Using This Knowledge for Financial Defence

Once you understand the dark side of compounding, you can start making smarter moves with your money. It’s a shift in mindset from just saving to actively defending your financial future.

Actionable Steps You Can Take:

Prioritize High-Interest Debt: Use the Rule of 72 to see which debts are doing the most damage. A 22% credit card balance is doubling twice as fast as an 11% personal loan. That tells you exactly which one to attack first.

Invest to Beat Inflation: Your goal should always be to earn a return that’s comfortably higher than the rate of inflation. This is why investing in things like ETFs and stocks is so important for long-term goals like retirement.

Track Your Financial Health: You can't fix what you can't see. NeoSpend brings all your accounts into one place, making it easy to spot high-interest balances that need your attention. When you can see the whole picture, you can create a real plan to crush debt and get your money working for you again.

When to Be Cautious with This Rule

The Rule of 72 is an amazing mental shortcut, but it’s crucial to remember what it is—an estimate, not a crystal ball. Think of it like a roadmap for a cross-country drive. It gives you a fantastic sense of the journey, but it won't predict every traffic jam or construction detour along the way.

Its real magic is in quick, back-of-the-napkin math. For serious financial planning, though, you need to know its limits and the real-world curveballs it doesn’t see coming.

The Rule of 72 Is Not Always Precise

The formula is most accurate for interest rates in the sweet spot between 6% and 10%. Venture outside that range, and the estimates can start to drift. At super low or sky-high rates, the math gets a bit fuzzy for exact predictions, though it still gives you a decent ballpark figure.

For instance, at a 2% return, the rule says it’ll take 36 years to double your money. The real number is closer to 35 years. At a blistering 20% return, the rule suggests 3.6 years, while the actual answer is nearer to 3.8 years. The difference isn't huge, but it shows this is a rule of thumb, not an unbreakable law of finance.

What the Rule of 72 Overlooks in Canada

A few real-world factors can throw a wrench in your investment returns, and the basic Rule of 72 formula doesn't see them coming. Ignoring these can paint an overly rosy picture of your financial growth.

Here’s what the rule leaves out:

Taxes on Gains: The rule calculates growth on your pre-tax return. Here in Canada, investments in a non-registered account are hit with capital gains tax, which shaves off your actual profit and slows down your doubling time. This is exactly why registered accounts like the TFSA (where growth is tax-free) and RRSP (where growth is tax-deferred) are so powerful.

Investment Fees (MERs): Most Canadian mutual funds and ETFs have a Management Expense Ratio (MER). This annual fee is skimmed directly off your investment returns. A 2% MER on a fund earning 8% means your actual return is only 6%. Using 8% in your calculation would be misleading; you need to use 6% to get a realistic timeline.

Market Volatility: The Rule of 72 assumes a smooth, steady rate of return year after year. Let’s be real—the stock market is anything but smooth. Returns jump around, with some fantastic years and some downright painful ones. You should always use an average expected return for your calculation, and be ready for a much bumpier ride.

For a truer estimate, always use your net return—the number you get after subtracting fees and taxes from your gross investment return. This gives the Rule of 72 much more practical power.

More Precise Alternatives to the Rule of 72

When financial pros need pinpoint accuracy, they aren’t using the Rule of 72. They break out more complex logarithmic formulas. But if you just want a slightly sharper mental shortcut, there are a couple of other "rules" that work better in certain situations.

One popular alternative is the Rule of 69.3. This is the most mathematically pure number for calculating doubling time with continuously compounded interest. It's not as snappy for quick mental math, but it's technically more precise.

Using the Rule of 72 is perfect for quick financial check-ins and comparing investment options on the fly. But when it's time for serious planning, you need tools that account for all the variables. Apps like NeoSpend can help by tracking your actual returns after fees, giving you a clear picture of how your money is truly performing. This closes the gap between a quick estimate and your real-world financial reality.

Your Takeaway: Put Your Money to Work

The Rule of 72 is more than a neat math trick—it's a powerful tool for any Canadian looking to build wealth. By quickly estimating how long it takes for your money to double, you can set clear goals, compare investment options, and understand the true cost of debt. It simplifies the power of compound interest, turning a complex topic into an actionable insight.

The real magic happens when you apply this rule to your own finances. Use it to map out your journey to saving for a down payment in your TFSA or building a solid RRSP for retirement. By pairing this quick mental shortcut with a smart tool like NeoSpend to track your actual progress, you move from guesswork to a confident financial strategy.

Ready to see how fast your money can grow? Explore how NeoSpend can help you manage your money smarter and reach your goals sooner.

Questions People Ask About the Rule of 72

Okay, so we’ve broken down the what and the how. But you might still be wondering about a few things when it comes to using the Rule of 72 in the real world. That’s perfectly normal.

Let's tackle some of the most common questions we hear from Canadians trying to get a better handle on their money.

How Accurate Is the Rule of 72, Really?

It's an incredibly solid estimate, especially for interest rates between 6% and 10%—a range that covers many typical investment scenarios. The whole point isn’t to be perfectly precise; it’s designed for quick, "back-of-the-napkin" math.

Think of it this way: it’s more than good enough for setting financial goals or comparing different investment options on the fly, without needing a spreadsheet. It’s all about getting a quick gut check, not pinpoint mathematical accuracy.

Can I Use This Rule for My Stock Portfolio?

You absolutely can, but with a key consideration. The Rule of 72 works best with a fixed, predictable interest rate. As anyone with money in the Canadian stock market knows, returns are anything but fixed.

So, how do you make it work? You use your portfolio's estimated average annual return over a long period. It’s a handy way to get a rough projection of potential growth in your RRSP or TFSA, but always remember that actual returns will swing up and down from year to year. Market volatility is part of the game.

Does the Rule of 72 Account for Taxes and Fees?

Nope, and this is a big one for Canadians. The basic formula works with your gross rate of return—that’s the number you see before anyone takes a cut.

To get a truly realistic timeline, you need to use your net return. That’s the rate you’re left with after you subtract investment fees (like MERs on your mutual funds) and any taxes you’ll owe on the growth, which is a major factor for investments outside of registered accounts.

This is exactly why understanding the power of a TFSA is so important—all that growth is completely tax-free. Using only pre-tax return numbers will give you a timeline that’s too optimistic. Factoring in all the costs gives you a much clearer, and more achievable, financial picture.

Ready to move from ballpark estimates to your actual numbers? NeoSpend Inc. helps you see your true net returns by bringing all your Canadian investment and savings accounts into one simple dashboard. Track your progress, manage your goals, and make smarter decisions with your money.