Deciding between an RRSP vs. TFSA comes down to one simple question: when do you want to pay your taxes? The right answer depends on your income today and your goals for tomorrow.

A Tax-Free Savings Account (TFSA) is built for tax-free withdrawals, making it incredibly flexible and a fantastic choice for anyone saving for short-term goals or who is currently in a lower income bracket. On the other hand, a Registered Retirement Savings Plan (RRSP) gives you an immediate tax deduction when you contribute, which is a huge advantage for high-income earners looking to lower their current tax bill.

A Head-to-Head Comparison of RRSP and TFSA

Choosing between an RRSP and a TFSA is a classic Canadian financial dilemma. They are both powerful tools for growing your money, but they are designed for different purposes and offer very different tax advantages. Understanding how each one works is the first step toward building a savings plan that truly fits your life.

If you look at the numbers, you'll see a clear trend. In 2023, of the 11.3 million Canadians who put money into either account, the TFSA was the more popular pick. This tells us that many Canadians value the freedom of tax-free withdrawals over the immediate gratification of an RRSP tax deduction.

What’s really interesting is that about 2.5 million people contributed to both. This is a huge clue that the best strategy isn't always an either/or choice—it's often about using them together to maximize your savings. You can discover more insights into Canadian saving habits from Statistics Canada.

To make the decision a little easier, let's put them side-by-side.

RRSP vs TFSA At a Glance

Here’s a quick rundown of the main differences to help you see which account might be a better fit for your situation.

| Feature | RRSP (Registered Retirement Savings Plan) | TFSA (Tax-Free Savings Account) |

|---|---|---|

| Tax Treatment | Contributions are tax-deductible, lowering your current taxable income. | Contributions are made with after-tax money and are not deductible. |

| Growth & Withdrawals | Your investments grow tax-deferred. You pay tax when you withdraw the money. | Your investments grow completely tax-free. |

| Withdrawal Rules | Withdrawals are taxed as income. | Withdrawals are always tax-free. |

| Contribution Room | Based on 18% of your previous year's earned income, up to a set annual maximum. | A fixed annual limit for everyone, plus any unused room from previous years. |

| Impact of Withdrawals | Contribution room is lost forever once you take money out. | Withdrawn amounts are added back to your contribution room the following year. |

| Who It's Best For | Higher-income earners who want to reduce their tax bill now. | Anyone, but especially lower-to-middle income earners or those saving for short-term goals. |

As you can see, they’re designed for fundamentally different financial goals.

The Core Strategic Difference

Here’s the simplest way to think about it: an RRSP is about postponing your taxes, while a TFSA is about eliminating taxes on your investment gains altogether.

The choice really hinges on a simple prediction: will you be in a higher or lower tax bracket when you retire?

The fundamental question to ask is: "Will my tax rate be higher or lower in retirement?" If you expect it to be lower, the RRSP's tax deduction today is valuable. If you expect it to be the same or higher, the TFSA’s tax-free withdrawals are likely more powerful.

But remember, it's not a competition. The smartest financial plans often use both accounts in tandem. For instance, a classic strategy is to contribute to your RRSP to get a tax refund, then invest that entire refund into your TFSA.

This is where smart money management comes in. With NeoSpend, you can easily see your entire financial picture, helping you track contribution limits for both accounts and manage your money smarter.

So, How Do These Accounts Actually Work?

When you line up an RRSP and a TFSA, the core difference boils down to a simple question: Do you want a tax break now, or a tax break later? How you answer that is the first step to deciding which account is right for you. They might seem similar on the surface, but the way they handle taxes creates two very different paths for your money.

The RRSP is all about tax-deferred growth. Think of it as hitting the snooze button on your tax bill. Every dollar you contribute is deducted from your taxable income for the year, which usually means getting a nice refund come tax time.

This upfront perk is a huge draw, especially when you're in your peak earning years and your tax rate is at its highest. Your investments then grow inside the account, sheltered from annual taxes. But remember, "deferred" just means "later"—you'll eventually pay tax on the money when you pull it out in retirement, where it's treated just like regular income.

A Look at RRSP Tax Deferral in Action

Let's look at a practical example. Priya is a graphic designer in Ontario making $85,000 a year. She contributes $10,000 to her RRSP.

- Instantly, her taxable income for the year drops to $75,000.

- This moves her into a lower marginal tax bracket, and she gets an immediate tax refund of around $3,000.

That's real money back in her pocket today. The catch? When Priya retires and starts taking money out of her RRSP, every withdrawal is added to her income for that year and taxed accordingly.

The TFSA, on the other hand, runs on the magic of tax-free growth. It's the opposite of the RRSP. You contribute with money you've already paid taxes on (your after-tax dollars), so there’s no immediate tax deduction to claim.

The real payoff comes later. Once your money is in the account, every penny it earns from interest, dividends, or capital gains is completely and permanently tax-free. When you decide to take it out—whether that's tomorrow or in 30 years—it's all yours, no strings attached and no tax bill waiting for you.

One of the biggest mistakes people make is treating the TFSA like a simple savings account. It’s actually a powerful investment account where you can hold stocks, bonds, and ETFs, letting your money compound entirely shielded from the taxman.

Seeing TFSA Tax-Free Growth at Work

Now consider Ben, a junior developer in Calgary earning $60,000. He takes $6,000 of his after-tax pay, puts it in his TFSA, and invests in an ETF.

- Over five years, his investment grows to $9,000.

- He decides to pull out the whole amount to help with a down payment on a condo.

Both his original $6,000 contribution and the $3,000 he earned in growth come out completely tax-free. Just as important, that withdrawal doesn't count as income, so it won’t affect his eligibility for government benefits like the Canada Child Benefit or Old Age Security—a critical difference from the RRSP.

Getting this fundamental distinction is the first step to building a smarter financial plan. With NeoSpend, you can manage your money smarter by seeing your full financial picture in one place. It helps clarify how much after-tax cash you have for a TFSA or how an RRSP contribution might affect your yearly budget, putting you in a better position to decide.

A Detailed Comparison of Key Account Features

Beyond the tax headlines, the real difference between an RRSP and a TFSA is in the details. The mechanics—how you contribute, how you withdraw, and how each account interacts with government benefits—will truly shape your financial future. Nailing these distinctions is how you move from just saving money to building a smart, effective financial strategy.

Contribution Rules Unpacked

The way you add money to these accounts is completely different. An RRSP is designed to reward you during your peak earning years, while the TFSA offers a level playing field for every Canadian.

Your RRSP contribution room is personal. It’s calculated as 18% of your previous year's earned income, capped at an annual maximum set by the government ($31,560 for 2024). This is great for a freelancer who has a massive year; they can shelter a larger chunk of that income from taxes.

The TFSA contribution limit, on the other hand, is a simple, fixed amount for every eligible Canadian. For 2024, it's $7,000. It doesn't matter if you're a student or a CEO; the limit is the same, and any room you don't use just rolls over and accumulates year after year.

You can see how this democratic approach has changed how we save. Back in 2009, RRSPs were king, grabbing 49.2% of registered contributions while TFSAs took in just 28.2%. Fast forward to 2020, and the tables have turned: TFSAs now dominate with 51.8% of contributions. If you want to dig into the data, you can learn more about how Canadians' savings habits have evolved.

Withdrawal Rules and Room Regeneration

This is perhaps the most significant difference, and it's where the TFSA’s incredible flexibility shines. Pulling money from an RRSP is a permanent, taxable event. Taking it from a TFSA is like giving yourself a tax-free, temporary loan.

When you withdraw from your RRSP, two things happen right away:

- You get taxed: The money you take out is added to your taxable income for the year. Your bank will withhold some of that for taxes before you even see it.

- The room is gone forever: You can never put that money back. The contribution space you used is lost for good.

A TFSA withdrawal is the complete opposite. It's 100% tax-free. Even better, the full amount you took out gets added back to your contribution room on January 1st of the next year.

The TFSA's "room regeneration" feature is its superpower. It means you can tap into your savings for a down payment or an emergency, knowing that you can replenish that space later. This makes it a fantastic hybrid account for both short-term goals and long-term wealth.

Impact on Government Benefits

This is a crucial detail that too many people overlook, especially when planning for retirement. RRSP withdrawals can actually reduce the government benefits you receive, while TFSA withdrawals are invisible.

Because RRSP withdrawals count as taxable income, they drive up your net income on paper. This can trigger a "clawback" of benefits like Old Age Security (OAS) and the Guaranteed Income Supplement (GIS). For a retiree counting on every dollar, that’s a painful financial surprise.

TFSA withdrawals, however, don't count as income at all. You could pull out $100,000 from your TFSA, and it wouldn’t impact your eligibility for OAS, GIS, or even the Canada Child Benefit one bit. This makes the TFSA an incredibly powerful tool for creating tax-free income in retirement without messing up your other support systems.

Juggling these features can feel complex. This is where an app like NeoSpend helps you manage money smarter. NeoSpend's dashboard can show you both your RRSP and TFSA limits in one clean view, so you can plan your contributions and avoid that nasty 1% per month penalty for over-contributing. By seeing the whole picture, you can make confident decisions about where every dollar should go.

Real-World Scenarios: When to Choose an RRSP or a TFSA

Theory is great, but let's get practical. Deciding between an RRSP and a TFSA isn’t just about the numbers; it’s about picking the right tool for your specific life stage and goals. The best choice often becomes clear when you see how these accounts work for everyday Canadians.

The Young Professional Starting Their Career

If you're a recent grad or just getting started in your career, your income is likely the lowest it will ever be. This is prime time for the TFSA. Since you’re in a low tax bracket, the immediate tax break from an RRSP contribution just isn't that powerful yet.

Instead, putting after-tax money into a TFSA lets you build savings that grow completely tax-free. This approach saves your valuable RRSP contribution room for your peak earning years, when that tax deduction will provide a much bigger benefit.

Example Scenario: Meet Chloe, a 25-year-old marketing coordinator in Toronto earning $55,000 a year. She's managed to save $6,000.

- If she chooses a TFSA: She contributes that $6,000 of after-tax money. If it grows to $10,000 in 10 years, she can withdraw the entire amount for a down payment, completely tax-free.

- If she chooses an RRSP: She contributes $6,000 and gets a tax refund of around $1,500. However, she’s used up RRSP room that would be far more valuable later on when she’s earning $100,000 and in a much higher tax bracket.

For Chloe, the TFSA is the clear winner for its flexibility and long-term tax efficiency.

The High-Income Earner at Their Peak

Now, let's fast-forward to someone in their 40s or 50s, right at the top of their career. For high-income earners, the RRSP's immediate tax deduction is its superpower. Every dollar contributed directly reduces their taxable income, often leading to a significant tax refund.

This is the classic RRSP play: lower your tax bill during your highest-earning years, then withdraw the money in retirement when your income—and your tax rate—is presumably lower.

A key thing to remember is your expected retirement income. If your tax rate stays the same or goes up in retirement, the RRSP’s edge starts to fade. A CIBC analysis actually shows that for many people, TFSA outcomes can be just as good or even better. You can learn more about how TFSAs can outperform RRSPs in retirement.

The Freelancer with Fluctuating Income

Freelancers and gig workers understand income volatility. One year can be a blockbuster, and the next can be a grind. This is where the TFSA's incredible flexibility becomes an absolute lifesaver.

Because you can withdraw from a TFSA tax-free and get that contribution room back the next year, it’s a perfect safety net. A freelancer can pull money out during a slow month without any tax consequences or permanently losing that savings space. Try that with an RRSP, and you’ll get taxed on the withdrawal and that contribution room is gone for good.

Example Scenario: David is a freelance web developer with a variable income. Last year, he earned $120,000. This year, a big project fell through, and he's projecting $50,000.

- He can take $15,000 from his TFSA to cover his bills without owing a dime in tax.

- Come January 1st, that $15,000 of contribution room is added back, ready for him to refill once business picks up again.

The Family Saving for a Down Payment

For families saving for their first home, the RRSP vs. TFSA debate gets really interesting, as both accounts offer a strong case.

The TFSA is the simple, clean option. You save after-tax dollars, the money grows tax-free, and you can pull out the full amount for your down payment—no strings attached.

The RRSP has a special feature: the Home Buyers' Plan (HBP). It lets each partner withdraw up to $60,000 from their RRSP tax-free to buy a first home. The only catch is you have to repay this "loan" to your RRSP over 15 years. The huge advantage here is that your initial contributions gave you a tax refund, which can supercharge your down payment fund.

Choosing between them often boils down to personal discipline. Whichever route you take, an app like NeoSpend can help. Its goal-tracking features let you set up a dedicated "Down Payment" fund, watch your progress, and see exactly how close you are to making homeownership a reality.

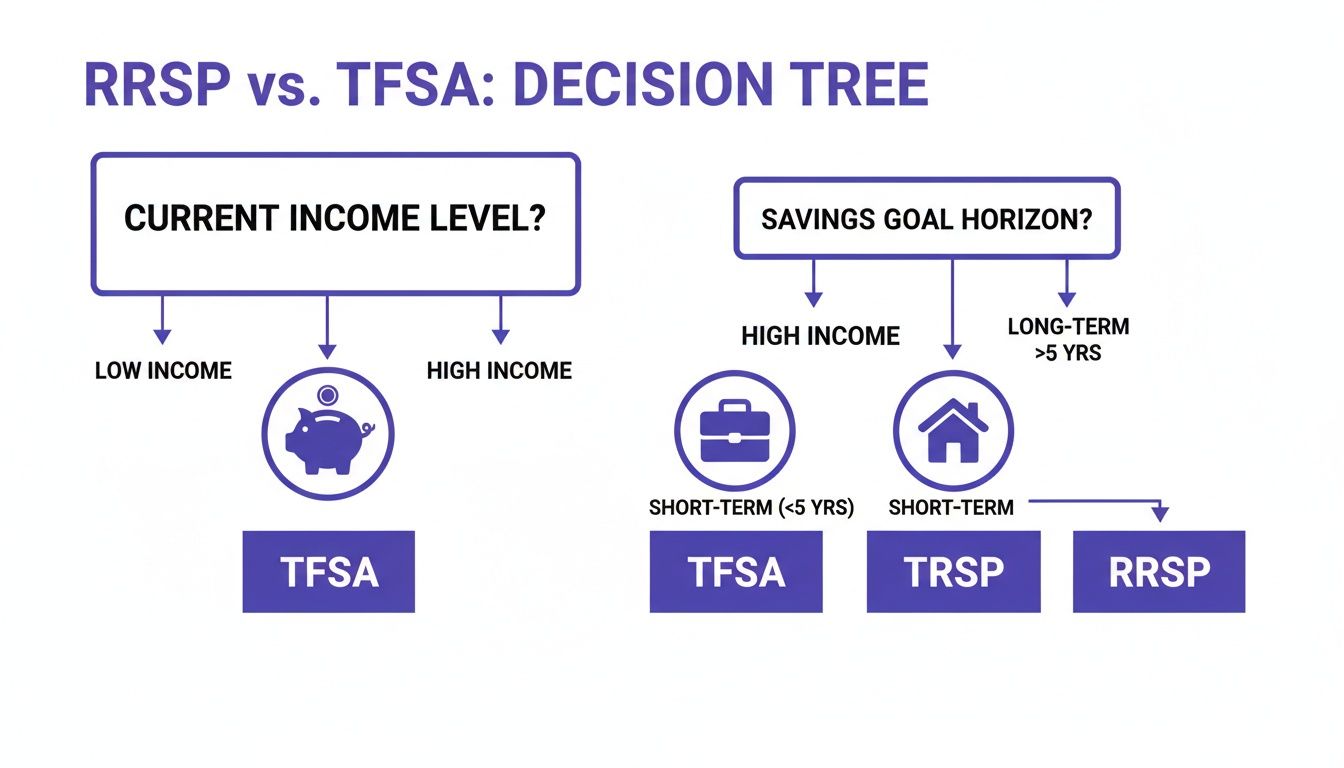

Your Decision-Making Cheat Sheet

Okay, we've covered the details, scenarios, and tax implications. It’s a lot to take in. To simplify things, let's cut through the noise with a straightforward decision guide.

Finding Your Path

The whole point is to answer a couple of key questions: What's your income today? And what are you saving for?

Your answers will guide you. For example, if you're saving for a down payment you'll need in three years, your strategy will be totally different from someone in their peak earning years saving for retirement two decades from now. Getting clear on your goals is half the battle.

This decision tree maps out the three most common routes for Canadians.

As you can see, your current income and how soon you need the money are the two biggest factors. If you're a high-income earner, that RRSP tax deduction is incredibly powerful. But if you’re just starting your career or have a shorter-term goal in mind, the TFSA’s tax-free withdrawals and flexibility are tough to beat.

This flowchart isn't a substitute for a full financial plan with an advisor. But it's an excellent starting point to feel confident about your next step and to grasp why one account might be a better fit for you than the other.

Ultimately, this visual reinforces the main takeaway: there’s no single "best" account. It all comes down to your personal situation.

This is where having a crystal-clear picture of your finances is non-negotiable. Using a tool like NeoSpend gives you the hard numbers you need to make informed decisions. When you can see exactly where your money is going and how much you have left to save, you can choose with real confidence.

How to Maximize Both Accounts With Smart Tracking

Picking the right account is a great first step, but the real magic happens when you use both accounts together to hit your financial goals faster. Smart management isn't just about putting money in—it's about automating, strategizing, and knowing where every dollar is going.

![]()

One of the most effective strategies is to put your contributions on autopilot. Set up regular, pre-authorized payments to both your RRSP and TFSA. This builds a solid savings habit. Even small, consistent deposits can grow into a huge nest egg thanks to the power of compounding.

Here’s another pro tip: take your RRSP tax refund and contribute it directly to your TFSA. This creates a powerful savings loop where your tax-deferred money generates a refund that then fuels your tax-free growth.

The Critical Role of Smart Tracking

You can't manage what you don't measure. Juggling RRSP and TFSA contribution limits is tricky, especially since they change every year. It's an easy place for people to make mistakes, which is why smart tracking is essential.

Knowing your exact contribution room is a must. If you go over the limit in either account, you’ll get hit with a penalty tax of 1% per month from the Canada Revenue Agency (CRA) on the excess amount. A simple oversight can quickly become a costly headache.

A unified tracking system turns your big financial plans into small, daily actions. When you see your progress in real-time, staying motivated and making smarter money moves becomes second nature.

How NeoSpend Simplifies Everything

This is exactly what NeoSpend was built for. The app lets you link all your investment accounts—RRSP, TFSA, and more—into one clean dashboard. Forget logging into multiple banking apps; you get a complete picture of your financial life in one spot.

NeoSpend helps you manage your money smarter with proactive insights into your contribution room and alerts to help you avoid over-contribution penalties. It makes it easy to visualize your progress toward your goals, turning abstract numbers into real results.

RRSP vs. TFSA: Your Questions Answered

When you're trying to figure out the best place to grow your money, a few common questions always pop up. Let's clear up some of the most frequent RRSP vs. TFSA queries.

Can I Have Both an RRSP and a TFSA?

Absolutely. Not only can you have both, but for most Canadians, it’s the smartest way to build wealth. You’re free to contribute to both an RRSP and a TFSA in the same year, provided you haven’t maxed out your contribution room for either.

A popular strategy is to contribute to your RRSP to get the immediate tax deduction. When your tax refund arrives, transfer the entire amount directly into your TFSA. This creates a powerful savings loop, using tax-deferred funds to fuel tax-free growth.

What Happens If I Over-Contribute?

This is one area where you need to be careful. The Canada Revenue Agency (CRA) imposes a penalty tax of 1% per month on any amount over your contribution limit. That applies to both RRSP and TFSA accounts, and those penalties can add up quickly.

Keeping a close eye on your contribution limits is essential. This is where an app like NeoSpend can be a lifesaver, helping you manage your money smarter by giving you a clear, consolidated view of your contribution room.

Which Account Is Better If My Retirement Income Will Be Higher?

It’s not the most common scenario, but if you genuinely expect to be in a higher tax bracket in retirement than you are today, the TFSA is almost always the better choice. It’s all about when you pay the tax.

With an RRSP, you get a tax deduction now (at your current, lower rate) but pay taxes on withdrawals later (at your future, higher rate). With a TFSA, you contribute after-tax money, but every single dollar you take out in retirement is completely tax-free.

The core principle is simple: pay tax when your rate is lowest. If that’s now, a TFSA wins. If it will be in retirement, the RRSP has the advantage.

Do I Lose My RRSP Contribution Room If I Withdraw Money?

Yes, and this is a massive difference between the two accounts. When you take money out of an RRSP (unless it’s for the Home Buyers' Plan), that contribution room is gone forever. Plus, the amount you withdraw gets added to your taxable income for the year.

The TFSA is the complete opposite. Any amount you withdraw is added back to your contribution room on January 1st of the following year. This makes the TFSA incredibly flexible for a down payment, a major purchase, or an emergency fund, because you can "borrow" from yourself without permanently losing that valuable savings space.

Your Takeaway: Choosing between an RRSP and a TFSA depends entirely on your current income and future goals. A TFSA offers flexibility and tax-free withdrawals, perfect for short-term goals and lower-income earners. An RRSP provides an immediate tax break, ideal for high-income earners planning for retirement. For many, the best strategy is using both.

Ready to take control of your financial future? With NeoSpend, you can see your entire RRSP and TFSA picture in one place, track your goals, and make smarter decisions with confidence. Stop guessing and start knowing. Discover how NeoSpend simplifies your finances today.