Saving for a down payment on your first home in Canada can feel like a mountain to climb. But what if you already have a powerful financial tool waiting to be used? Your Registered Retirement Savings Plan (RRSP) could be the key. Thanks to the Canadian government's Home Buyers' Plan (HBP), you can borrow from your retirement savings, tax-free, to make your dream home a reality.

This guide provides clear, practical financial guidance on how to use your RRSP for a first-time home buyer down payment, with simple explanations and real-world Canadian examples.

Your RRSP: A Secret Weapon for Your Down Payment

Let's be real: coming up with a down payment is often the biggest hurdle for anyone buying a home in Canada. It’s easy to feel stuck watching property prices climb while your savings struggle to keep up. This is where your RRSP—something you've probably only thought of for retirement—can completely change the game.

The Home Buyers' Plan isn't a grant or a handout. Think of it as an interest-free loan you give yourself, straight from your own retirement funds. It’s a trustworthy way to boost your budget and get into the housing market sooner.

How Does the Home Buyers' Plan (HBP) Work?

The concept is simple but incredibly effective. The HBP lets you withdraw money from your RRSP to buy or build your first home, without getting hit by the usual withdrawal taxes. It's an actionable way to unlock a pool of money you've already worked hard to save, giving your down payment a serious boost.

The program allows a first-time home buyer to withdraw up to $35,000 tax-free. If you're buying with a partner who also qualifies, you can combine your withdrawals for a total of up to $70,000. You can get all the official details on the Government of Canada's HBP website.

The catch? You have to pay it back. But you get a generous 15-year period to do so, which keeps the yearly repayment amounts manageable for most new homeowners.

The real magic of the HBP is borrowing from yourself without an immediate tax penalty. That cash injection can be the difference-maker, helping you reach the 5%, 10%, or even the coveted 20% down payment threshold and avoid expensive mortgage loan insurance.

Manage Your Savings Smarter with NeoSpend

Juggling everything involved in buying a home is a lot—tracking RRSP contributions, saving for a down payment, and then remembering to make HBP repayments. This is where an app like NeoSpend helps you manage your money smarter.

By linking your accounts, NeoSpend gives you a clear view of your RRSP balance, making it easier to set and hit your down payment goals. Once you've used the HBP, you can even set up reminders to ensure you never miss a repayment, keeping your financial plan on track.

Do You Qualify for the Home Buyers' Plan?

Before you get lost in real estate listings, the first step is making sure you qualify for the Home Buyers' Plan (HBP). The rules, set by the Canada Revenue Agency (CRA), are specific, but you might be surprised by how flexible they can be.

The HBP is designed for first-time home buyers. But what does the CRA consider a "first-time home buyer"? Their definition is quite generous. You generally qualify if, in the four years leading up to your withdrawal, you haven't lived in a home that you or your current spouse or partner owned.

That four-year window is the key. It means that even if you owned a home years ago, you can regain your "first-time buyer" status after a few years of renting.

A Real-Life Canadian Example of the Rule

Let’s look at a common Canadian scenario. Picture Sarah and Tom, a couple looking to buy their first condo together in Calgary. Sarah has been a renter since university. Tom, however, owned a townhouse but sold it six years ago when he moved for work.

Because it’s been more than four years since Tom lived in a home he owned, the CRA considers him a first-time home buyer again. Sarah, having never owned, also qualifies. This is great news for them. They can each withdraw up to $35,000 from their separate RRSPs, giving them a potential $70,000 boost for their down payment.

Your HBP Eligibility Checklist

Getting the "first-time buyer" part right is the biggest hurdle, but there are a few other boxes you need to tick. Here’s a quick checklist of actionable insights:

- You must be a resident of Canada when you withdraw the funds and until you officially own the home.

- You need a written agreement to buy or build a home (i.e., a signed purchase agreement).

- You must intend to live in this home as your primary residence within a year of buying or building it. The HBP can't be used for an investment property.

A common misconception is that if one partner has owned a home recently, the other is automatically disqualified. That’s not true. As long as you personally meet the four-year rule, you can use your own RRSP for the HBP, even if your partner can't.

The Critical 90-Day RRSP Contribution Rule

This is a big one. Any money you want to use for the HBP must have been in your RRSP account for at least 90 days.

Why the waiting period? It's the CRA's way of preventing people from getting a quick tax break. You can't deposit money into an RRSP, claim the tax deduction, and then immediately pull it out tax-free for a down payment. The funds need to be considered genuine retirement savings first.

For example, if you deposit $10,000 into your RRSP on March 15th, you can't use that specific amount for an HBP withdrawal until at least June 13th. Any money that was already in there for over 90 days is fine to use. This makes planning ahead crucial. A tool like NeoSpend can be a lifesaver, helping you easily track when you made each deposit so you know exactly how much is eligible for the HBP.

How to Withdraw Funds from Your RRSP for a Home

So you've confirmed you're eligible for the Home Buyers' Plan. Now for the exciting part: moving that money from your RRSP into your down payment fund.

This step is straightforward, but you must follow the rules precisely to keep the withdrawal tax-free. Getting this right is key to avoiding a surprise tax bill. The entire process hinges on one specific form from the Canada Revenue Agency (CRA).

The Key Form: T1036

To make an HBP withdrawal, you need to fill out Form T1036, Home Buyers' Plan (HBP) Request to Withdraw Funds from an RRSP. You'll need a separate form for every withdrawal you make. You can easily find on the Government of Canada's website.

Most of the form is basic personal information and the amount you wish to withdraw. The crucial part is ensuring every detail is accurate, as your RRSP provider uses this form to release the funds without withholding tax. A common mistake is submitting the form too late. Give your financial institution plenty of time to process it—don't wait until the week before your closing date.

How Long Does the Withdrawal Process Take?

Once you’ve submitted your T1036 form, how long until you see the cash? The timeline can vary, but a realistic window is about 5 to 10 business days. To be safe, start the withdrawal process at least two or three weeks before you need the funds. This provides a cushion for any delays and ensures the money is in your chequing account when your lawyer calls for it.

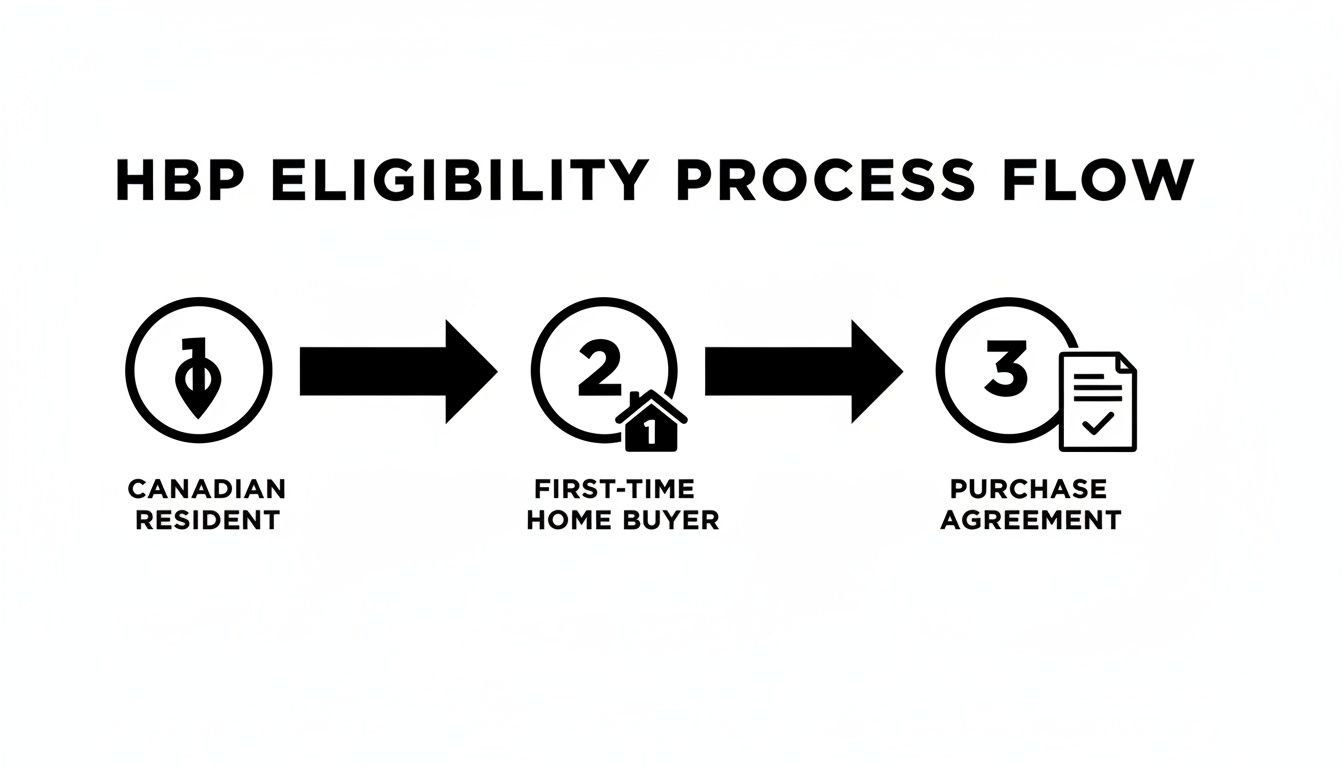

Before you even think about withdrawing, this chart makes the core eligibility checks crystal clear.

This visual breaks down the main checkpoints—being a resident, a first-timer, and having a signed purchase agreement—that you have to clear to use your RRSP for a first time home buyer purchase.

Let's Revisit That 90-Day Rule with an Example

We've mentioned it before, but this rule is so important it's worth a practical Canadian example. Any money you plan to withdraw for the HBP must have been in your RRSP account for at least 90 days.

Let's look at Maria, who is buying her first condo in Toronto. She has had $20,000 in her RRSP for several years. To boost her down payment, she deposits another $5,000 on April 1st. Her closing date is June 15th.

- The initial $20,000 is eligible. It’s been in the account for much longer than 90 days.

- The extra $5,000 she just deposited is not. By June 15th, it will only have been in the account for about 75 days, falling short of the 90-day rule.

If Maria tried to withdraw that recent $5,000, it would be treated as a regular, taxable RRSP withdrawal. This means it would be added to her income for the year, and she'd owe tax on it—exactly what the HBP helps you avoid.

The 90-day rule is not a suggestion. Plan your contributions well before you start house hunting. The smartest move is to have your funds settled long before you begin making offers.

What Happens if You Withdraw More Than the Limit?

Currently, the HBP allows you to withdraw up to $35,000 per person. Withdrawing more than that limit has immediate tax consequences.

Any amount you withdraw above $35,000 is not part of the HBP. Your financial institution must report it to the CRA as regular taxable income. For example, if you withdraw $40,000, that extra $5,000 gets added to your income for the year, and you'll pay tax on it at your marginal rate.

This is where being organized pays off. Using a tool like NeoSpend gives you a clear view of your total RRSP balance and exactly how much is eligible for the HBP. By tracking your contributions and their deposit dates, you can confidently withdraw the maximum allowed amount without accidentally triggering a surprise tax bill.

Your Guide to HBP Repayments

Borrowing from your RRSP to buy your first home is a huge win, but that’s only half the story. The other half is the long-term plan of repaying that money to yourself. This requires discipline, but thankfully, the rules are more straightforward than they sound.

Think of the Home Buyers' Plan (HBP) as an interest-free loan you've given yourself. The Canada Revenue Agency (CRA) provides a generous 15-year window to repay the entire amount. This timeline is designed to keep your annual payments from feeling like a burden, especially while you're juggling a new mortgage.

A common question is, "When do I start paying it back?" The good news is, the clock doesn't start ticking immediately. Your repayment period officially begins in the second year after the year you withdrew the money. So, if you withdraw funds in 2024, your first payment isn’t due until the 2026 tax year.

How to Calculate Your Minimum Annual Payment

Figuring out your yearly repayment is simple. The CRA takes the total amount you withdrew and divides it by 15. This gives you the minimum amount you need to contribute back each year.

Let’s use a typical Canadian scenario. Say you withdrew $30,000 from your RRSP for your down payment.

- Total HBP Withdrawal: $30,000

- Repayment Period: 15 years

- Calculation: $30,000 ÷ 15 years = $2,000 per year

This means you need to contribute at least $2,000 back into your RRSP each year and designate it as an HBP repayment. Of course, you can always pay back more than the minimum to get ahead of schedule.

Here’s a sample repayment schedule to illustrate.

Example HBP Repayment Schedule ($30,000 Withdrawal)

| Repayment Year | Minimum Annual Repayment | Remaining HBP Balance |

|---|---|---|

| 1 | $2,000 | $28,000 |

| 2 | $2,000 | $26,000 |

| 3 | $2,000 | $24,000 |

| 4 | $2,000 | $22,000 |

| 5 | $2,000 | $20,000 |

| 6 | $2,000 | $18,000 |

| 7 | $2,000 | $16,000 |

| 8 | $2,000 | $14,000 |

| 9 | $2,000 | $12,000 |

| 10 | $2,000 | $10,000 |

| 11 | $2,000 | $8,000 |

| 12 | $2,000 | $6,000 |

| 13 | $2,000 | $4,000 |

| 14 | $2,000 | $2,000 |

| 15 | $2,000 | $0 |

As you can see, consistent, manageable payments get the job done without putting a major strain on your budget.

How to Make and Designate Your Repayments

Making a repayment involves two key steps. First, contribute to your RRSP as you normally would. Second, and most importantly, you must tell the CRA that this contribution is for your HBP.

You'll do this when you file your annual tax return using Schedule 7, RRSP, PRPP and SPP Contributions and Transfers, and HBP and LLP Activities. On this form, you'll enter how much of your total RRSP contribution you want to count as your HBP repayment.

Key takeaway: You do not get a tax deduction for the money designated as an HBP repayment. You already received the tax break when you first contributed that money to your RRSP. This is just you putting it back.

What Happens if You Miss a Payment?

Life happens. If you can't make the full minimum repayment, the CRA doesn't charge penalties or interest. Instead, the amount you missed is added directly to your taxable income for that year.

Let’s say your minimum payment was $2,000, but you only repaid $500. The remaining $1,500 shortfall gets added to your income on your tax return. You'll then pay tax on that $1,500 at your marginal tax rate, losing the tax-deferred benefit on that portion of your savings.

Staying organized is key to avoiding a surprise tax bill. This is where NeoSpend helps you manage money smarter. You can set savings goals for your HBP repayment and create reminders so you never forget to designate it on your tax return.

HBP vs. Other Canadian Home Buyer Programs

The Home Buyers’ Plan (HBP) is a fantastic tool, but it’s no longer the only option. For years, using an RRSP for a first time home buyer was the main strategy, but Canada's financial landscape has evolved.

Now, aspiring homeowners have other powerful programs, especially the Tax-Free First Home Savings Account (FHSA) and the flexible Tax-Free Savings Account (TFSA). Understanding the unique benefits of each will help you map out the smartest route to your down payment.

The Game Changer: The First Home Savings Account (FHSA)

Launched in 2023, the FHSA is what many Canadians were waiting for. It combines the best features of an RRSP and a TFSA into one account designed specifically for buying your first home.

Here's why the FHSA is so powerful:

- Tax-Deductible Contributions: Like an RRSP, every dollar you contribute is tax-deductible.

- Tax-Free Growth: Your investments grow inside the account completely sheltered from tax.

- Tax-Free Withdrawals: This is the best part. When you buy a home, you withdraw everything—your contributions and the growth—without paying any tax.

This triple benefit makes the FHSA a standout choice. You get a tax break on the way in and on the way out, and unlike the HBP, there's nothing to repay. Once the funds are used for your home, the transaction is complete.

The Flexible Option: The Tax-Free Savings Account (TFSA)

While the TFSA wasn't created specifically for home buying, its flexibility makes it a strong contender for saving a down payment. Any money you contribute grows tax-free, and you can withdraw it at any time, for any reason, with no tax penalties.

The main trade-off is that TFSA contributions are not tax-deductible. You don't get the immediate tax refund that an RRSP or FHSA provides. However, its simplicity and the fact that you regain your contribution room the following year make it an invaluable savings tool.

HBP vs. FHSA vs. TFSA: A Head-to-Head Comparison

Let's break down how these three options stack up to help you create your personal game plan.

HBP vs FHSA vs TFSA: A Comparison for Canadian Home Buyers

| Feature | RRSP Home Buyers' Plan (HBP) | First Home Savings Account (FHSA) | Tax-Free Savings Account (TFSA) |

|---|---|---|---|

| Primary Use | Tax-deferred loan from RRSP for a home | Dedicated savings for a first home | General-purpose tax-free savings |

| Contribution | Tax-deductible | Tax-deductible | Not tax-deductible |

| Withdrawal | Tax-free, up to $35,000 | Tax-free for a qualifying home | Tax-free for any reason |

| Repayment | Mandatory over 15 years | No repayment required | No repayment required |

| Contribution Limit | Based on your personal RRSP room | $8,000 annually, $40,000 lifetime | Annual limit set by the government |

This table clarifies why the FHSA is gaining popularity. A 2025 BMO survey found that 56% of potential first‑time buyers now plan to use an FHSA for their down payment. You can read more about these home buyer trends to see how the market is evolving.

The Smartest Strategy? Don't Choose—Combine!

You don't have to pick just one. For many aspiring homeowners, the best approach is to combine these programs. You can max out your FHSA first, tap into the HBP for an extra boost, and use your TFSA for closing costs or moving expenses.

Imagine you need a $90,000 down payment. You could build $40,000 in your FHSA, withdraw $35,000 from your RRSP using the HBP, and pull the final $15,000 from your TFSA. This strategy lets you leverage the best features of each account. Juggling these accounts is where an app like NeoSpend becomes invaluable, giving you a clear dashboard of your progress across all your savings to help you reach your goal faster.

Answering Your Top HBP Questions

The Home Buyers' Plan can feel tricky, and it's natural to have questions when dealing with your life savings. Here are clear, trustworthy answers to some of the most common questions from first-time buyers across Canada.

Can I use the HBP if my partner already owns a home?

Yes, you can. HBP eligibility is determined on an individual basis. As long as you qualify as a first-time home buyer (meaning you haven't lived in a home owned by you or your current partner in the last four years), you are eligible. Your partner’s homeownership status doesn't prevent you from withdrawing up to $35,000 from your own RRSP.

What if my home purchase falls through?

If you've already withdrawn your HBP funds and the deal collapses, don't panic. You can cancel your HBP participation by repaying the full amount you withdrew back into your RRSP. The deadline is December 31st of the year after you made the withdrawal, giving you time to sort things out.

Can I use the HBP to buy a home for a relative?

Yes, but only in specific situations. The plan allows you to buy or build a home for a related person with a disability. The home must be more accessible or better suited for their needs. In this case, you (the person withdrawing from the RRSP) do not have to be a first-time home buyer yourself.

Is the HBP still a good idea with the FHSA available?

This is a key question. The First Home Savings Account (FHSA) is a powerful tool because contributions are tax-deductible and withdrawals for a home are tax-free, with no repayment required. It's a huge hit—by November 2024, nearly 1 million Canadians had opened an FHSA, with 57.2% of 2023 contributors aged 25-34. You can see the full stats on the FHSA's impressive first year on Canada.ca.

The best strategy isn't choosing the HBP or the FHSA—it's using them together. Max out your FHSA first (it’s a no-brainer). Then, if you still need more for your down payment, tap into the HBP.

Can I pay back my HBP faster than 15 years?

Absolutely. The 15-year repayment window is a maximum, not a requirement. You are always free to pay back more than the annual minimum. Any extra payments reduce your outstanding balance and help you rebuild your retirement savings faster.

A Takeaway for Your Home Buying Journey

Using your RRSP through the Home Buyers' Plan is a trusted and powerful strategy for Canadian first-time home buyers. While the new FHSA offers incredible benefits, the HBP remains a valuable tool, especially when combined with other savings accounts. The key is to understand the rules, plan your contributions ahead of time, and stay organized with your repayments.

With a smart strategy, you can turn your dream of homeownership into a reality. Juggling a mortgage, RRSP contributions, and HBP repayments is easier with the right tool. With NeoSpend, you get a single, clear view of your finances. Track your RRSP contributions, schedule HBP repayments, and get reminders so you never miss a deadline. Ready to manage your money smarter? Try NeoSpend today.