Think of a personal financial plan as your financial roadmap—a clear, living guide that helps you use your money to build the life you actually want. It takes all the scattered pieces of your financial world and organizes them into a single, straightforward strategy for everything from covering monthly bills to saving for a down payment or investing for retirement.

Why Every Canadian Needs a Personal Financial Plan

Let's be honest: managing money in Canada can be stressful. The cost of living is rising, retirement feels like a mountain to climb, and debt can feel overwhelming. It’s enough to make anyone feel stuck and unsure of where to even start.

A personal financial plan is the antidote to that chaos. It's not some rigid, joy-sucking rulebook. It's a flexible game plan that puts you back in the driver's seat. This guide is built to do just that—turn confusing numbers into a clear, actionable picture of your financial life, with practical steps designed for the unique challenges we face as Canadians.

The Reality of Financial Stress in Canada

If money feels like a constant weight on your shoulders, you’re not alone. Recent research from the FP Canada Financial Stress Index revealed that money is the #1 source of stress for Canadians, beating out every other cause by more than double.

Canadians are juggling a lot of worries all at once. The top concerns are:

- Paying monthly bills (37%)

- Saving enough for retirement (34%)

- Saving for a major purchase (31%)

- Paying down debt (30%)

This anxiety hits those under 55 the hardest, and here’s the kicker: people without a financial plan feel that stress nearly twice as intensely. It’s a clear sign that having a plan isn't just a "nice-to-have"—it's a critical tool for your well-being.

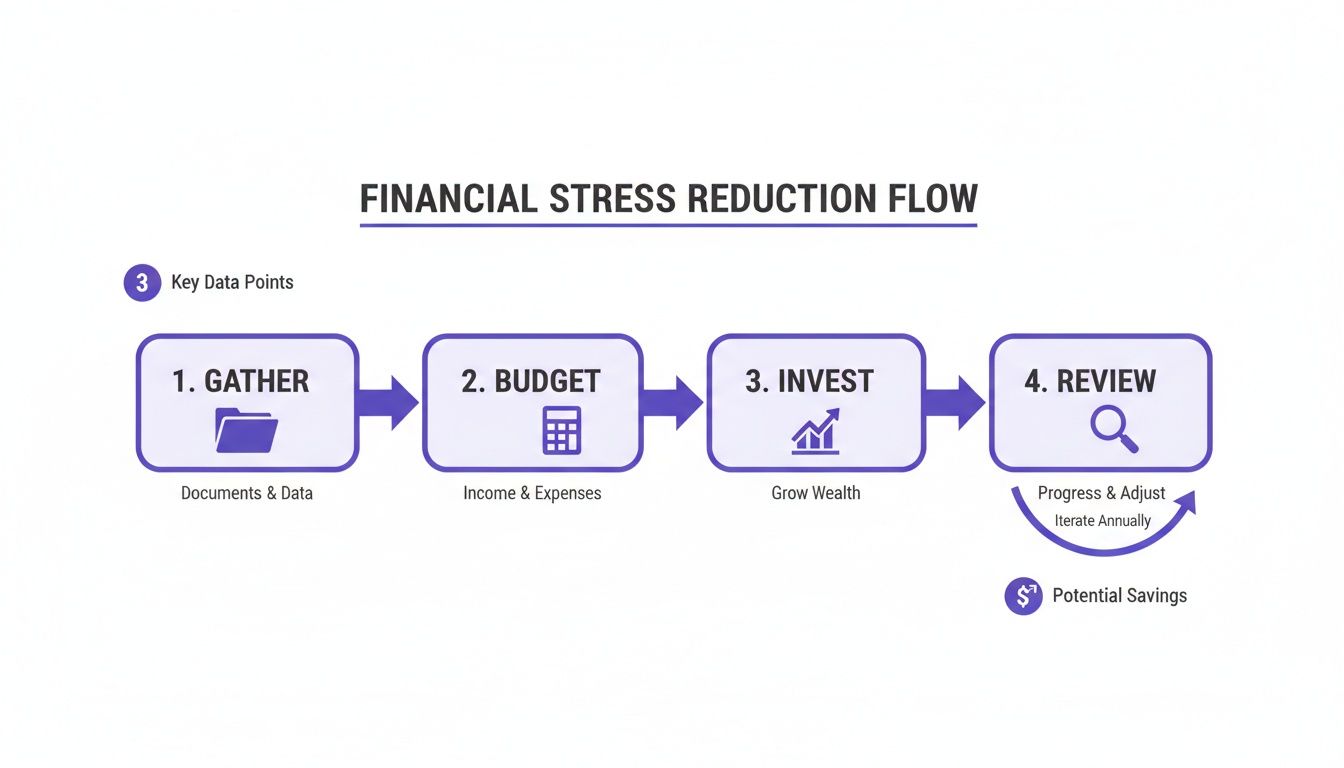

This simple flow chart breaks down how to turn that financial stress into a structured plan of action.

The key takeaway is that a methodical approach—gathering your info, building a budget, investing with a purpose, and checking in on your progress—is the most direct way to counter the chaos that fuels financial anxiety.

How a Financial Plan Brings You Clarity

A personal financial plan is like a GPS for your money. It shows you exactly where you are, helps you lock in your destination, and then gives you the turn-by-turn directions to get there.

The benefits kick in almost immediately.

- You regain control. Finally, you'll know exactly where your money is going every month.

- Your anxiety goes down. A clear plan eliminates the uncertainty that breeds stress.

- You hit your goals faster. You can be intentional with your money, pointing it directly at what matters most to you, whether that's a down payment on a home or a trip to see the Northern Lights.

A great financial plan isn’t about being perfect; it’s about making progress. Just getting a clear view of your finances is the single most powerful step you can take toward a more secure future.

This is where a tool like NeoSpend comes in. It’s built to make this whole process simpler. By linking all of your accounts in one place, NeoSpend automatically organizes your spending and gives you that unified picture you need to start planning. Instead of drowning in spreadsheets and bank statements, you get one clean dashboard that makes managing your money feel totally doable.

Step 1: Get the Full Picture of Your Finances

Before you can map out where you're going, you need to know exactly where you are right now. The first step in building a solid personal financial plan is to pull every piece of your financial life into one spot. It’s all about getting that 360-degree view of your money so you can make smart, informed decisions.

Think of it like planning a road trip across Canada. You wouldn’t just hop in the car and start driving from Halifax without knowing how much gas you have or even what your destination is. Your finances are no different. You need to see everything at once: your chequing and savings accounts, what you owe on your credit cards, any personal loans, and how your investments like your TFSA and RRSP are doing.

Why Seeing It All in One Place is a Game Changer

Let’s be real—hopping between different banking apps and investment logins is a pain. It's almost impossible to get a true sense of your net worth or cash flow when you're manually plugging numbers into a spreadsheet. This is exactly where most financial plans fall flat before they even get off the ground.

When you bring everything together on a single dashboard, you take the guesswork out of the equation. You can see your cash on hand, how much you owe, and how your investments are performing in a single glance. This complete picture is the foundation for any good financial strategy.

Your net worth—what you own minus what you owe—is your financial starting line. Getting a precise, real-time number is the most empowering first step you can take in creating a personal financial plan.

A Real-World Canadian Example

Meet Sarah, a professional living in Vancouver. Like a lot of Canadians, her finances are spread out.

- Her day-to-day chequing account and a credit card are with CIBC.

- She’s got her TFSA and other investments going through Wealthsimple.

- Her condo mortgage is with BMO.

To get a handle on things, Sarah used to have to log into three separate websites and punch numbers into a spreadsheet. It was a chore, and the information was usually outdated by the time she was done.

This is where a tool like NeoSpend completely changes the game. By securely syncing her accounts from CIBC, Wealthsimple, and BMO, Sarah gets a live, all-in-one dashboard. Now, her chequing balance, credit card debt, TFSA growth, and mortgage principal are all right there, updating automatically. That clarity gives her the solid ground she needs to build the rest of her personal financial plan with confidence.

Taking Stock of Your Debts

Knowing what you have is only half the battle; you also need a crystal-clear picture of what you owe. For most Canadians, debt is a major part of their financial reality. While our net wealth as a nation has been on the rise, so has our debt. In fact, recent economic studies show that total credit market debt has climbed to a staggering $3.0 trillion, which really drives home how important it is to track it carefully. You can read more about the Canadian household balance sheet from Desjardins' economic studies.

It's crucial to list out every single debt you're carrying, big and small.

- Mortgage Loans: For most homeowners, this is the big one.

- Car Loans: A major monthly expense for many.

- Student Loans: A long-term reality for countless graduates.

- Credit Card Balances: This high-interest debt can snowball fast if not managed.

- Lines of Credit: Don't forget about secured and unsecured lines of credit.

Seeing all these numbers together helps you figure out which debts to attack first and build a real repayment strategy into your personal financial plan. Once you have the complete picture, you're not just guessing anymore—you're ready to make strategic moves.

Step 2: Create a Budget That Actually Works for You

Let's be honest, the word "budget" can feel restrictive. It brings up images of spreadsheets and cutting out everything you enjoy. But a modern budget isn’t about saying "no" to everything. It's about getting a clear picture of where your money is going so you can start telling it where you want it to go.

It’s a tool for awareness, not restriction. And thankfully, we can ditch the manual receipt-tracking. Today’s tools can turn this tedious chore into an insightful and automated process.

Let Your Past Spending Guide Your Future Plan

Here’s a secret: most budgets fail because they’re built on wishful thinking. We tell ourselves we’ll only spend $400 on groceries, but a quick look at our bank statements shows we’ve been spending closer to $700 for months. That kind of budget is set up to fail.

Instead of guessing, what if your real spending habits built the budget for you?

This is exactly where a tool like NeoSpend comes in. Once you connect your accounts, it digs into your transaction history and automatically starts sorting everything. It knows the difference between your Tim Hortons run, your weekly Loblaws haul, and your PRESTO card top-up. You get an instant, honest look at your spending habits, no manual entry required.

This data-first approach is the bedrock of a budget you can actually stick to—because it’s based on your real life, not a fantasy one.

Find Hidden Spending and Score Easy Wins

When you see all your spending laid out and categorized, patterns you never noticed before start to emerge. It’s often the small, "harmless" purchases that quietly add up to a major expense.

Think about a family in Halifax wondering where their paycheque goes each month. By linking their accounts to NeoSpend, they instantly see a breakdown of their monthly subscriptions:

- $18.99 for the family streaming bundle

- $12.99 for a music subscription

- $24.99 for a fitness app they haven't used in months

- $45.00 on various gaming and cloud storage services

Suddenly, they can see they're spending nearly $300 a month on subscriptions spread across different cards. That single insight is huge. They can now consolidate, cancel what they don’t need, and put that cash directly into their TFSA. NeoSpend even lets you tag specific expenses with goals like "#FamilyVacation" or "#HomeReno" to see exactly how your spending is tracking.

A great budget doesn’t just show you where your money went; it empowers you to tell your money where to go next. It transforms your personal financial plan from a static document into an active tool for building wealth.

With the cost of living on everyone’s mind, this level of clarity is critical. A recent Finder survey found that 43% of Canadians are worried about affording basic necessities. The biggest pressure points? Groceries (51%) and rent (27%). Having a solid budget isn't a luxury anymore; it's essential. You can see how Canadians are managing their money in the full report.

A clear budget gives you back a sense of control when prices feel out of control. To give you a starting point, here is a sample budget for a typical Canadian household.

Sample Monthly Budget for a Canadian Household

This table provides a sample budget breakdown for a household with a net monthly income of $6,000, illustrating common expense categories and target percentages.

| Expense Category | Example Cost | Percentage of Income |

|---|---|---|

| Housing (Rent/Mortgage) | $2,100 | 35% |

| Transportation | $600 | 10% |

| Groceries | $720 | 12% |

| Utilities & Bills | $360 | 6% |

| Debt Repayment | $300 | 5% |

| Savings & Investments | $900 | 15% |

| Personal & Discretionary | $600 | 10% |

| Subscriptions & Insurance | $420 | 7% |

Of course, your numbers will look different, but this gives you a framework to compare against your own spending patterns.

Build Your Budget in Minutes, Not Hours

Once you have an accurate picture of your past spending, setting up your new budget is ridiculously easy. NeoSpend uses your history to suggest realistic starting points for each category.

If it sees you’ve spent an average of $650 on groceries for the past three months, it will suggest that as your starting budget. If your goal is to trim that back, you can adjust it to $600 and then watch your progress in real-time. This immediate feedback loop makes managing your money feel less like a chore and more like a winnable game. It ensures your financial plan is built on a solid, accurate foundation from day one.

Step 3: Set and Automate Your Canadian Savings Goals

Okay, you've dialled in your budget. Now for the fun part. This is where you shift from just managing your spending to actively building wealth—the most exciting part of any personal financial plan.

This is the moment your "someday" dreams start turning into "soon" realities. It’s about being intentional with your money and, most importantly, paying your future self first. In Canada, our two most powerful tools for this are the Tax-Free Savings Account (TFSA) and the Registered Retirement Savings Plan (RRSP).

Choosing the Right Savings Account for Your Goals

Understanding the difference between a TFSA and an RRSP is a game-changer for any Canadian. They're both fantastic, but they serve different purposes. Making the right choice can save you thousands in taxes down the road.

Here's the simplest way to think about it: RRSPs give you a tax break now, while TFSAs give you a tax break later.

RRSP (Registered Retirement Savings Plan): When you put money into an RRSP, you can deduct that amount from your income at tax time. This means you pay less tax today. The catch? When you pull the money out in retirement, it's considered income, and you'll pay tax on it then.

TFSA (Tax-Free Savings Account): You contribute to a TFSA with money you've already paid tax on (after-tax dollars), so there’s no immediate deduction. But the real magic is that every dollar of growth and every withdrawal is 100% tax-free. Forever.

So, which one should you use? It depends on your income, what you're saving for, and when you think you'll need the cash.

Choosing between a TFSA and an RRSP often comes down to your current versus your expected future income. If you expect to be in a higher tax bracket now than in retirement, the RRSP is often a great choice. If you're in a lower tax bracket now or need flexibility, the TFSA is incredibly powerful.

TFSA vs. RRSP: Which Is Right for You?

Deciding where to put your savings can feel a bit overwhelming. This quick breakdown should help you figure out which account aligns best with your income, career stage, and what you’re trying to achieve.

| Feature | Tax-Free Savings Account (TFSA) | Registered Retirement Savings Plan (RRSP) |

|---|---|---|

| Contribution | Made with after-tax money; no immediate tax deduction. | Made with pre-tax money; contributions are tax-deductible. |

| Withdrawal | Withdrawals are 100% tax-free at any time. | Withdrawals are taxed as income at your marginal rate. |

| Best For | Flexible goals like a down payment, car, or emergency fund. Ideal for lower-income earners. | Long-term retirement savings. Ideal for higher-income earners. |

| Contribution Room | You get it back the following year after a withdrawal. | Once you withdraw, that contribution room is lost forever. |

For many Canadians, the answer isn't "one or the other" but "both." You might funnel money into a TFSA for shorter-term goals and use your RRSP strictly for the long haul of retirement.

The Unbeatable Power of Automation

The single most effective strategy for hitting your savings goals is automation. "Set it and forget it." When you take willpower out of the picture, your savings just happen.

This is where your financial plan gets its superpowers. You’re not just hoping to have money left over; you're building a system that saves for you.

Here's how to put it into action:

- Get Specific: Don’t just save "for a car." Aim for something real, like, "Save $15,000 for a new car in 3 years."

- Do the Math: A $15,000 goal over 36 months breaks down to $417 per month. Easy.

- Automate the Transfer: Now, go into your banking app and schedule a recurring transfer for $417 from your chequing to your TFSA. The trick is to set it for the day after your paycheque lands.

This simple act builds a powerful habit without you having to think about it.

With an app like NeoSpend, you can elevate this whole process. You can create a specific goal right in the app, link it to one of your savings accounts, and watch your progress unfold automatically. Seeing that bar creep closer to your target is an amazing motivator and makes your whole financial plan feel tangible and real.

Step 4: Master Your Bills and Plan for Emergencies

Having a solid budget and clear savings goals is the engine of your personal financial plan. But it only takes one missed bill or a sudden emergency to throw the whole thing off course.

Even the most buttoned-up plan is vulnerable if you don’t have a system for your day-to-day payments and a safety net for when life happens. These aren’t just minor details—they’re the defensive plays that protect all your hard work. A single late payment can mean penalty fees and a ding to your credit score, while a surprise car repair can force you to dip into your long-term savings.

The Hidden Costs of Unmanaged Bills

It’s surprisingly easy to underestimate the damage disorganized bills can do. It usually starts small, like a $15 late fee on your hydro bill. But the real trouble comes from "phantom subscriptions."

We've all been there. You sign up for a free trial for a streaming service you forgot to cancel, or an annual software renewal automatically hits your account. These little charges fly under the radar, but they can easily bleed hundreds of dollars from your budget every year. For a young professional in Toronto, that’s the difference between maxing out their TFSA contribution and falling short.

This is exactly where a smart tracker like NeoSpend becomes a game-changer. It pulls all your recurring payments into one clean list. It scans your connected accounts to find your bills and subscriptions, then sends you reminders before they’re due. It can even flag things like duplicate charges so you can cut the fat and redirect that cash toward your goals.

Mastering your monthly cash flow isn't just about budgeting for big expenses. It's about building a reliable system that prevents small leaks from sinking your financial ship. This is a foundational piece of a resilient personal financial plan.

By getting a real handle on these details, you make sure the money you’ve carefully budgeted actually goes where you want it to.

Building Your Financial Safety Net: The Emergency Fund

Once your bills are sorted, the next move is to prepare for the unexpected. Life is unpredictable. Your car’s transmission could give out on the Don Valley Parkway, or you could face a temporary job loss. Without a financial buffer, these moments can quickly spiral into a full-blown crisis.

That buffer is your emergency fund: a stash of cash set aside only for these situations. Its job is to cover essential expenses so you don’t have to rack up debt or sell your investments at the wrong time.

So, how much do you need? For most Canadians, a good rule of thumb is to have three to six months' worth of essential living expenses saved up.

Here’s a quick way to figure out your number:

- List Your Must-Haves: Add up your core monthly costs. We're talking rent or mortgage, utilities, groceries, transportation, and minimum debt payments. Leave out the extras for now.

- Do the Math: Let's say your essential monthly expenses add up to $3,500. A three-month emergency fund would be $10,500, while a six-month fund would be $21,000.

- Choose Your Target: If you’re in a stable job with multiple income streams, three months might feel right. If you're a freelancer or work in a more volatile industry, aiming for six months provides a much stronger safety net.

The key is turning that intimidating number into an achievable goal. Inside the NeoSpend app, you can create a specific goal called "Emergency Fund" and link it to a high-interest savings account. From there, set up a small, automated weekly or bi-weekly transfer. Watching that goal grow transforms the idea from something stressful into an empowering milestone.

Step 5: Keep Your Financial Plan Aligned with Your Life

A great personal financial plan isn't something you create once and then file away. It's not a static document etched in stone. Think of it more like a living guide that needs to evolve right along with you.

Life happens. Your priorities shift, your income changes, and your goals get bigger. The most successful financial journeys are marked by regular check-ins, ensuring your money is working for the person you are today—not the person you were last year.

When to Review and Update Your Plan

Getting into the habit of an annual review is a fantastic start. But some moments in life are a clear signal that it's time to take a closer look right away. These are the times that can fundamentally change your income, expenses, or long-term dreams.

You'll definitely want to revisit your plan after:

- A big change in your income. This could be a promotion, a new job, or a side hustle taking off.

- Hitting a major life milestone. Getting married, having a baby, or buying your first home in a place like Calgary will completely reshape your financial world.

- An unexpected windfall or inheritance. This is a massive opportunity to supercharge your goals, but it needs a thoughtful strategy.

- Your long-term goals change. Maybe you've decided to retire five years earlier, or you're now prioritizing travel over everything else.

Your financial plan should empower you, not box you in. Regular reviews turn it from a rigid set of rules into a responsive tool that actually serves your evolving life.

Using Real-Time Insights to Stay on Course

This is where having all your financial info in one place really pays off. Instead of waiting for a huge life event to force a review, you can make small, smart adjustments as you go. With a tool like NeoSpend, you don't have to guess if you're on track—the data is right there.

For instance, you might glance at your spending trends and notice that your grocery bill has slowly crept up. That’s your cue to tweak the budget. Or maybe you see that your investments have done better than expected, and you can confidently bump up your automated contributions to your RRSP.

These insights from NeoSpend turn your review process from an annual chore into a simple, ongoing conversation with your money. This constant feedback loop is what keeps your personal financial plan relevant and perfectly aligned with the life you want to live.

Your Top Personal Financial Plan Questions, Answered

As you start piecing together your financial plan, it’s natural for questions to pop up. Let's tackle some of the big ones we hear all the time from Canadians just getting started.

How Often Should I Check In on My Plan?

Think of your financial plan like a living document. A deep dive once a year is a solid baseline. But any major life event—a new job, getting married, buying a home, or growing your family—is a signal to sit down and see what needs adjusting.

Of course, you don't have to wait for a big milestone. Using an app like NeoSpend gives you a real-time pulse on your money. This makes it easy to do quick monthly check-ins to make sure your budget and savings are still on track with where you are right now.

What's the Biggest Mistake People Make?

Hands down, it's creating a budget that’s way too strict. A personal financial plan with zero wiggle room for a spontaneous dinner out or a weekend trip is doomed from the start. It just isn't sustainable for most people.

The plans that actually work are built around your real life, not an idealized version of it. That’s where linking your actual accounts with a tool like NeoSpend becomes a game-changer. It helps you set realistic goals you can actually hit because they're based on your true spending habits.

The point of a financial plan isn’t to be perfect; it's to make progress. Ditch the idea of a flawless-but-impossible budget and focus on building a plan that works for your life.

Should I Tackle Debt or Start Saving First?

This really comes down to one thing: the interest rate on your debt.

If you're carrying high-interest debt like credit card balances—often with rates of 19.99% or more—that should be your number one priority. Paying that off gives you a guaranteed "return" that's almost impossible to beat by investing.

For lower-interest debt, like a mortgage or student loan, you can take a more balanced approach. It often makes sense to keep up with your regular payments while also putting money into your TFSA or RRSP. This way, you're managing your debt and building your long-term wealth at the same time.

Your Takeaway

Creating a personal financial plan is the most powerful step you can take towards reducing financial stress and achieving your goals. By getting a clear picture of your finances, building a realistic budget, and automating your savings, you put yourself firmly in control of your future.

Ready to put all this into practice? NeoSpend gives you the tools to build, track, and manage your own financial plan with confidence. See how it works and start your journey to financial clarity.