Figuring out where to park your retirement savings can feel like a huge decision. Should you focus on your company's pension plan or your own RRSP? The truth is, it's not always an either/or situation. For most Canadians, the real win comes from understanding how both of these powerful tools work together to build a secure future.

At its core, the difference is pretty straightforward. A pension plan is an employer-sponsored program built to give you a steady income stream when you retire. On the other hand, an RRSP (Registered Retirement Savings Plan) is a personal savings account that you control. Let’s break down what that means for you.

Understanding Your Core Retirement Tools

When you’re laying the groundwork for your future, pensions and RRSPs are the heavy hitters. Think of a workplace pension—officially a Registered Pension Plan (RPP)—as the more hands-off, structured route. Your employer sets it up, contributes to it (often matching what you put in), and handles all the investment management. It's designed to be a set-it-and-forget-it system that grows automatically.

An RRSP puts you firmly in the driver's seat. You decide how much to contribute (up to your annual limit), pick your own investments, and have far more say over how and when you access your money. It’s the DIY approach to retirement savings.

The Two Flavours of Canadian Pension Plans

It's super important to know that "pension" isn't a one-size-fits-all term. In Canada, they typically come in two main varieties, and the difference is massive for your financial future.

- Defined Benefit (DB) Pensions: These are the classic pensions you hear about. They promise a specific, predictable monthly payout for life once you retire. The amount is locked in by a formula, usually based on your salary and how many years you worked there. With a DB plan, your employer takes on all the investment risk. For example, a teacher in Ontario might have a DB plan that guarantees them a reliable income for life.

- Defined Contribution (DC) Pensions: With a DC plan, both you and your employer contribute a set amount into an investment account in your name. Your final retirement income depends entirely on how those investments perform over time. The investment risk here is all on you. A marketing manager at a tech startup, for instance, might have a DC plan where their retirement income depends on market growth.

This distinction is a big deal when comparing a pension plan vs. an RRSP, because a DC pension acts a lot more like a group RRSP than a traditional DB plan.

Helpful Takeaway: The key difference comes down to control versus predictability. Pensions offer an automated, often predictable path managed for you, while RRSPs give you total freedom and personal control over your money.

To get a clearer picture, let's start with a high-level look at the main differences. This quick comparison will set the stage for a deeper dive into what it all means for your wallet.

Quick Look: Pension Plan vs RRSP at a Glance

| Attribute | Employer Pension Plan (RPP) | Registered Retirement Savings Plan (RRSP) |

|---|---|---|

| Who Contributes? | You and your employer, almost always. | Mostly you, though a spouse can contribute to a spousal RRSP. |

| Who Manages Investments? | A professional plan administrator hired by your employer. | You or an advisor you choose. |

| How You Get Paid | Usually as a predictable monthly income for life (an annuity). | You withdraw funds as you need them (after converting to a RRIF). |

| Primary Benefit | Automated savings, employer matching, and professional management. | Complete flexibility and personal control over your money. |

With this foundation in place, we can dig into the specifics of how these plans impact your taxes, investments, and long-term financial security in Canada.

How Contribution Limits and Tax Breaks Work for Canadians

When you’re weighing a pension plan against an RRSP, the biggest differences pop up in how much you can contribute and how you get a break on your taxes. The rules can feel a bit tangled at first, but getting a handle on them is the key to maximizing your retirement savings and keeping your tax bill in check.

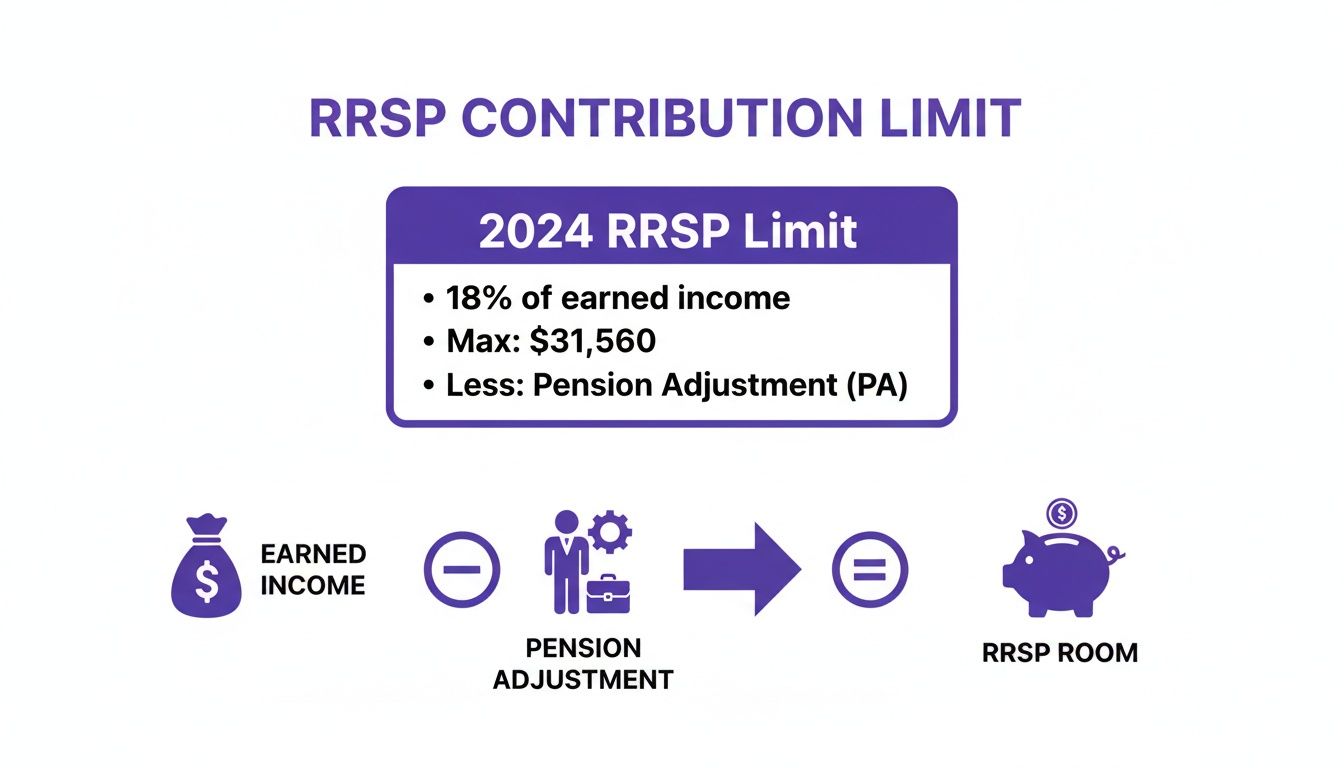

The Canada Revenue Agency (CRA) has firm rules about how much you can stash away in these tax-sheltered accounts. For your RRSP, it seems simple on the surface: you can put in 18% of your earned income from last year, up to a set maximum. But this is exactly where your pension and RRSP start to interact.

How a Pension Plan Impacts Your RRSP Contribution Room

If you're part of a workplace pension plan, your RRSP contribution room shrinks. It’s designed this way to keep the tax system fair since contributions to both plans get you a tax deduction. Your employer calculates the value of the pension benefit you earned over the year and reports it to the CRA.

This value is called a Pension Adjustment (PA). You’ll find your PA amount in Box 52 of your T4 slip. The CRA then automatically subtracts this from what you could have otherwise contributed to your RRSP for the next year.

Canadian Example: Let's say Maria, a nurse in Calgary, earned $70,000 last year. Her RRSP room would typically be 18% of that, or $12,600. But, she's also in her hospital's Defined Contribution pension plan. Her employer reported a Pension Adjustment (PA) of $7,000 on her T4.

To get her new RRSP limit, we just do the math: $12,600 (18% of income) - $7,000 (PA) = $5,600. So, Maria can only contribute a maximum of $5,600 to her personal RRSP this year.

This whole process is in place to prevent "double-dipping" on tax-deferred growth. The PA makes sure that the total amount you can save for retirement with a tax advantage is fair, whether you have a pension, an RRSP, or both.

Diving into the Contribution Structures

The structural differences between a company pension (an RPP) and a personal RRSP really show up in the annual limits set by the CRA. For RRSPs, the dollar limit is 18% of your previous year’s earned income (up to a cap), minus any Pension Adjustment. In contrast, the limits for defined contribution (DC) pension plans are often higher, while a defined benefit (DB) pension is based on your years of service. These pension limits are designed to help replace your salary in a more predictable way, whereas RRSPs are completely voluntary and funded by you alone. You can find a full breakdown of the current annual limits on these financial planning figures.

The Tax Deduction Process: How You Get Your Money Back

How you actually get your tax break is another major difference. With a pension, it’s all automatic. With an RRSP, you have to take action.

Pension Plan Tax Deductions

- Automatic and Instant: Your contributions come right off your paycheque before taxes are calculated. That means you get your tax relief on every single payday, lowering the tax withheld and leaving more money in your pocket throughout the year.

RRSP Tax Deductions

- Claimed Once a Year: You contribute to your RRSP with your after-tax pay. To get the tax benefit, you have to claim your total contributions when you file your annual income tax return. This usually results in a tax refund for the taxes you overpaid.

This really boils down to cash flow. A pension gives you a steady, immediate tax reduction, while an RRSP typically gives you a lump-sum refund once a year. Getting a clear view of your money helps you plan better. With a tool like NeoSpend, you can see your paycheque deductions and track your RRSP savings all in one spot, making it easier to manage your money smarter.

A Detailed Feature-by-Feature Comparison: Pension Plan vs RRSP

To really settle the pension plan vs. RRSP debate for your situation, we have to go beyond the basics and see how they actually work in the real world. Let’s put the key features head-to-head to see how they stack up on growth, control, and flexibility. This deeper dive will help you figure out which one clicks with your own financial style.

Employer Matching: The Closest Thing to Free Money

One of the biggest wins for a workplace pension is the employer match. This is where your company chips in, often matching your contributions up to a certain percentage of your salary. It's a huge boost to your savings. An RRSP is a personal account, so it doesn't come with a built-in matching feature. While some employers offer a Group RRSP with a match, that’s a company perk, not a standard feature of RRSPs themselves.

Actionable Insight: If your employer offers a pension match, contributing enough to get the full amount is almost always your smartest first move. Not doing so is like turning down a guaranteed return on your investment—and who would do that?

Investment Control: Who’s in the Driver’s Seat?

This is where the two retirement paths really fork. With a workplace pension—whether it’s a DB or DC plan—you have little to no say in the day-to-day investment picks. A professional plan administrator handles the whole portfolio for you. An RRSP, on the other hand, puts you firmly in control. You can choose everything from low-risk GICs and bonds to individual stocks, ETFs, and mutual funds. This hands-on approach is perfect if you want to build a portfolio that’s a perfect match for your own risk tolerance.

Remember, that Pension Adjustment (PA) is the key here. It’s the mechanism that keeps things fair by reducing your RRSP room to account for the retirement benefits you’re already building up at work.

Portability: What Happens When You Change Jobs?

In today's job market, people change roles more frequently. How your retirement savings move with you is a massive factor in the pension vs. RRSP showdown. RRSPs are champions of portability. Since the account is all yours and not tied to an employer, you can move it between financial institutions whenever you want, as long as it's a direct transfer without tax implications.

Pension plans are a different story. When you leave a job, your vested funds (meaning they’re officially yours after a certain period, usually two years) are also “locked-in.” This means you have to transfer the pension’s value into a special kind of account called a Locked-In Retirement Account (LIRA) or a similar locked-in RRSP.

Withdrawal Rules: Getting Your Hands on Your Money Before Retirement

Your ability to dip into your funds before you retire is another major point of difference. With an RRSP, you can pull money out anytime, for any reason. The catch? Whatever you withdraw gets added to your taxable income for that year, and you lose that contribution room forever. It can be a pricey way to handle an emergency, but the option is there. Pension funds, especially once they're in a LIRA, are built for one thing: retirement income. The rules are strict, and early withdrawals are basically off-limits except in very specific cases of financial hardship, which vary by province.

Creditor Protection: Keeping Your Nest Egg Safe

This is an often-overlooked but critical difference: how well are these accounts shielded if you run into serious financial trouble? Under Canadian bankruptcy laws, RRSPs are generally protected from creditors, with the exception of contributions made in the 12 months right before filing for bankruptcy. This helps keep your long-term savings safe. Workplace pension plans (RPPs) and LIRAs offer even stronger protection. They’re almost always fully shielded from creditors, no matter when the contributions were made. This makes them one of the most secure assets you can possibly own.

In-Depth Comparison: Pension Plans and RRSPs

This table breaks down the nitty-gritty details, helping you see at a glance how each account stacks up across the features that matter most to Canadians.

| Feature | Employer Pension Plan (RPP) | Registered Retirement Savings Plan (RRSP) |

|---|---|---|

| Employer Contributions | Common feature (employer matching is a key benefit). | Not a standard feature, though some Group RRSPs offer it. |

| Investment Control | Professionally managed; you have little to no control. | Full control over investment choices (stocks, bonds, ETFs, etc.). |

| Contribution Limits | Set by the plan, affects your RRSP room via Pension Adjustment (PA). | 18% of previous year's earned income, up to a max ($31,560 in 2024). |

| Portability | Less portable; funds are "locked-in" and transfer to a LIRA when you leave a job. | Highly portable; can be transferred between institutions at any time. |

| Early Withdrawals | Highly restricted; only for specific financial hardship cases. | Flexible; can withdraw anytime, but it's taxable and you lose the room. |

| Creditor Protection | Very strong; generally fully protected from creditors. | Good protection; shielded from creditors except for contributions made in the last 12 months. |

By really getting a handle on these details, you can build a retirement strategy that truly works for you. Using a tool like NeoSpend can help you see the whole picture, letting you track both your pension and your personal RRSP in one place. It makes managing your total retirement picture that much easier.

Your Retirement Strategy at Every Stage of Life

Your financial journey isn't a straight line, so your retirement plan shouldn't be either. The right answer to the "pension vs. RRSP" question changes a lot from your first real job to your last few years in the workforce. Let's break down how to approach things based on where you are right now in Canada.

The Young Professional Just Starting Out (20s)

Scenario: You're 26, you’ve just landed a great job in Toronto, and it comes with a DC pension plan. Your company will match every dollar you put in, up to 5% of your salary.

At this point, your game plan is simple. Your absolute number one goal is to contribute enough to get that full employer match. It’s a guaranteed return on your money that you literally can't get anywhere else. Even after that, your Pension Adjustment (PA) will likely leave you with some RRSP contribution room. If you have cash to spare after securing the match, opening a personal RRSP is a brilliant move.

The Freelancer or Gig Worker (30s)

Scenario: A 35-year-old freelance graphic designer in Vancouver has no company pension. For them, the RRSP isn't just a good idea—it's the core of their retirement strategy. This is all about discipline.

- Make it automatic: Set up monthly transfers to your RRSP.

- Go big in good years: When you land a massive project, funnel as much as you can into your RRSP to get a bigger tax deduction.

- Be strategic with deductions: In a leaner year, you can contribute but hold off on claiming the deduction until a future year when your income—and tax rate—is higher.

Mid-Career and Juggling Priorities (40s)

Scenario: A 45-year-old couple in Montreal is balancing a mortgage, RESPs for their kids, and their own retirement. One partner has a rock-solid DB pension from a government job, while the other has a Group RRSP at a tech company.

Their first priority is for the partner with the Group RRSP to max out their employer match. After that, they need to weigh the guaranteed return of paying down their mortgage faster against the potential growth in an RRSP. If their mortgage rate is low, the long-term upside of investing in an RRSP might win out. This is where NeoSpend can be a huge help, giving them a clear view of their cash flow to direct toward their goals.

Nearing Retirement and Shifting Focus (50s-60s)

Scenario: A 60-year-old in Halifax plans to retire in five years. They have a healthy DC pension and a sizable RRSP. The goal is no longer about aggressive growth; it’s about protecting what they've built and turning it into a reliable income stream.

The main priority now is to de-risk their portfolio, usually by shifting RRSP investments away from volatile stocks and into more conservative holdings like bonds and GICs. It's also time to map out a withdrawal strategy, coordinating their pension, RRIF (what an RRSP becomes), CPP, and OAS to create a predictable income that keeps them in the lowest possible tax bracket.

What Happens to Your Pension and RRSPs Down the Road?

Thinking about retirement savings isn't just about the here and now. The choices you make today will echo for decades, shaping not just your golden years but also what you leave behind for your family. Let's dig into the long-term game: how do these accounts stack up when it comes to taxes, government benefits, and your estate?

The OAS Clawback: A Canadian Reality Check

Here’s something many Canadians don’t think about until it’s too late: your retirement income can actually reduce your government benefits. Both pension payments and withdrawals from a Registered Retirement Income Fund (RRIF)—what your RRSP eventually turns into—count as taxable income.

This is a big deal because of the OAS recovery tax, better known as the "OAS clawback." If your retirement income crosses a certain threshold (which the government sets each year), you have to start paying back some of your Old Age Security pension. For many retirees, their pension or RRIF is exactly what pushes them over that limit.

For instance, say the income threshold is $86,912. If your combined income from a pension, RRIF, and other sources hits $96,912, you'll owe the government 15% of that $10,000 difference. Suddenly, your benefits aren't worth as much as you thought.

This is where RRSPs (and RRIFs) show a key advantage. You can control how much you withdraw each year, giving you the flexibility to stay under the clawback threshold. A pension, on the other hand, is a fixed monthly payment you can't adjust.

Passing It On: Beneficiary and Estate Rules in Canada

What happens to your hard-earned money when you're gone? This is another area where pensions and RRSPs are worlds apart, with major tax consequences for your estate.

With an RRSP, you can name a beneficiary.

- The Spousal Rollover: Name your spouse or common-law partner, and the entire value of your RRSP can be transferred to their RRSP or RRIF, completely tax-free.

- Anyone Else: If you name your kids or your estate, the full value of the RRSP is considered income on your final tax return, which can trigger a massive tax hit.

Pension plans play by a different set of rules, dictated by the plan itself and provincial law.

- Defined Benefit (DB) Pensions: These usually come with survivor benefits. Your surviving spouse will continue to receive a portion of your pension—often 50% to 60%—for the rest of their life.

- Defined Contribution (DC) Pensions: The total value is typically passed on to your spouse, who can roll it into their own locked-in account, much like an RRSP rollover.

Access to these plans isn't equal across Canada. Data shows that families in the highest income brackets are far more likely to have a workplace pension, which is a big reason why RRSPs have become the go-to retirement tool for so many Canadians. You can get a closer look at this trend in this deep dive into Canada's retirement income system.

No matter your mix of accounts, keeping track of everything is essential. With NeoSpend, you can see your RRSPs right alongside your other finances, giving you and your family a clear, complete picture of your estate.

Unify Your Retirement View with NeoSpend

Trying to decide between a pension plan and an RRSP can feel like you're being pulled in two different directions. But you don't have to choose one over the other. The real secret is making them work together. Think of them as two key players on the same team—your retirement team.

So, how do you pull it all together? Here’s a quick, actionable checklist to help you figure out where to put your money first.

Your Pension and RRSP Decision Checklist

Get Your Full Employer Match: If your workplace offers a pension or Group RRSP with matching, this is your absolute first move. Always contribute enough to get the full match. It's basically free money.

Check Your Remaining RRSP Room: Once you’ve secured the match, grab your latest Notice of Assessment from the CRA. Your Pension Adjustment (PA) reduces your total RRSP contribution limit, but there’s a good chance you still have plenty of room to work with.

Line It Up with Your Financial Goals: Are you saving for your first home? An RRSP is a clear winner here, thanks to the Home Buyers' Plan (HBP). Same goes for education with the Lifelong Learning Plan (LLP).

Know Your Investment Style: If you’d rather set it and forget it, the professionally managed nature of a pension plan is perfect. But if you want to be in the driver’s seat, a personal RRSP gives you that control.

See Your Entire Financial Picture in One Place

Juggling a pension, an RRSP, a TFSA, and all your other accounts can feel like trying to piece together a puzzle. That’s where a tool like NeoSpend comes in. It brings your entire financial world into one simple, clear dashboard. You can link your RRSP and other investment accounts to get a complete picture of your retirement savings, letting you see exactly where you stand at a glance.

It’s a known fact that many Canadians, despite seeing RRSPs as a cornerstone of their retirement, don't actually max out their contributions. NeoSpend’s budgeting features help you spot where your money is going each month, so you can find extra cash to direct toward your RRSP and close that savings gap. You can learn more about these trends and how to get ahead with smarter contributions here.

Helpful Takeaway: Genuine financial control comes from seeing the big picture. When you can view all your retirement accounts and your daily spending in one place, you can make smarter decisions, find more money to save, and actually watch your progress toward your goals. Explore how NeoSpend can put you in charge of your financial future.

Your Top Questions, Answered

When you're trying to figure out the best way to save for retirement, a few common questions always seem to pop up. Let's tackle some of the big ones Canadians often ask about pensions and RRSPs.

Can I Have a Pension and an RRSP at the Same Time?

Yes, you absolutely can, and for most Canadians with a pension, it's a smart move. Having a workplace pension reduces your personal RRSP contribution room—you'll see this calculated as a Pension Adjustment (PA) on your T4 slip—but it almost never wipes it out completely. Topping up that remaining RRSP room is a fantastic strategy to accelerate your retirement savings.

What Happens to My Pension if I Switch Jobs?

When you leave a job, you can't just take your vested pension funds as cash. They're "locked-in" to protect your retirement savings. You usually have a few choices:

- Move it to a LIRA: The most common path is transferring the funds into a Locked-In Retirement Account (LIRA). It's basically an RRSP, but with stricter withdrawal rules.

- Transfer to your new pension: If your new employer offers a similar pension plan, you might be able to roll your old one directly into it.

- Small balance payout: In some specific cases, if the pension amount is very small, you may have the option to unlock it and transfer it to your regular RRSP or take it as a taxable cash payout.

The Big Debate: Pay Down the Mortgage or Contribute to an RRSP?

This is a classic Canadian financial crossroads. There’s no single right answer because it’s deeply personal. Paying down your mortgage gives you a guaranteed, risk-free return equal to your mortgage interest rate. Contributing to an RRSP offers the potential for higher returns from market growth, plus an immediate tax deduction. If you’re sitting on a high-interest mortgage or are risk-averse, attacking the mortgage is a great bet. But if your mortgage rate is low and you’re in a higher tax bracket, the RRSP's combined power of tax savings and potential growth is tough to beat.

Ready to see how all these pieces fit together in your own financial life? NeoSpend gives you a single view of your RRSP, spending, and savings so you can find extra money to put toward your goals. Take control by visiting https://neospend.com to see how it works.