Ever glanced at your credit card statement and seen a negative balance? It can be a bit confusing, but all it means is you’ve overpaid your credit card. In simple terms, you sent your card issuer more money than you actually owed.

Think of it like loading up a gift card at Tim Hortons and accidentally adding an extra $20. That extra money doesn't disappear—it's still yours to spend on your next double-double.

What It Means to Overpay a Credit Card

Overpaying your credit card happens more often than you’d think, and it’s a pretty common scenario for many Canadians. The good news is, it’s not a financial disaster. It just means that for a little while, your credit card company owes you money.

This credit shows up on your statement as a negative balance, usually with a minus sign right in front of the number, like -$50.00.

Most of the time, this happens because of simple timing issues or a slip of the finger when making a payment. Let's say you pay off your entire balance, and then a few days later, a refund for that jacket you returned from The Bay finally hits your account. That refund has nowhere else to go, so it creates a credit.

Why Do Credit Card Overpayments Happen?

Getting to the bottom of why you have a negative balance is usually pretty simple. Nine times out of ten, it’s completely accidental.

Here’s a quick look at the most common reasons why you might end up with extra money on your card.

Common Overpayment Scenarios in Canada

This table breaks down the typical situations that lead to an overpayment. It’s a handy way to quickly figure out what might have happened with your account.

| Scenario | Common Canadian Cause | Typical Outcome |

|---|---|---|

| The Double-Up | You forgot you had an automatic payment scheduled with your bank and paid the bill manually too. | A credit equal to your last bill payment sits on your account. |

| The Refund Twist | You returned an item and the refund was processed after you'd already paid your bill. | The refund amount creates a negative balance. |

| The Typo | You accidentally added an extra zero or mixed up the numbers when paying online (e.g., $500 instead of $50). | A significant credit appears on your account, waiting to be used or refunded. |

| The Rewards Payout | You cashed in your reward points for a statement credit when your balance was already low or zero. | The rewards create a credit balance that can cover future spending. |

With Canadians managing over 101 million credit cards and nearly half carrying an average monthly balance of $4,499, it's easy to see how payments can get tangled. You can dig into more of these trends in these insights on Canadian credit card statistics.

While some people even overpay on purpose to free up their credit line, most of us just want a clear view of our finances without any surprises.

No matter how it happens, the result is always the same: a credit balance on your account. You can either leave it there to cover your next few purchases or ask for the money back. This is where a tool like NeoSpend helps people manage money smarter. It pulls all your account balances into one clear dashboard, so you can easily spot things like an overpayment before you even start scratching your head.

How Canadian Banks Handle Overpayments

So, you've overpaid your credit card bill and a negative balance is staring back at you from your account summary. Don't sweat it—this happens all the time, and Canadian banks have a standard, no-fuss process for this exact situation. Whether you're with RBC, TD, Scotiabank, or any other institution, the playbook is pretty much the same.

That extra money doesn’t just disappear. It sits on your account as a credit balance. Think of it like pre-loading a gift card for yourself; the money is there, ready for your next shopping trip. This credit automatically gets applied to any new purchases you make, chipping away at your future statement balance without you having to lift a finger.

Let's say you accidentally paid an extra $100, leaving you with a -$100.00 balance. If you then go spend $70 on groceries at Loblaws, that charge simply eats into your credit. Your new balance won't be a $70 debt; it'll still be a -$30.00 credit. It's that simple.

What Are Your Options When You Overpay?

When you’ve got a negative balance, you’re in the driver’s seat. You basically have two choices, and your decision just comes down to whether you need the cash back in your chequing account or if you're cool with letting it cover upcoming spending.

- Leave the Credit Balance: This is the easiest option. Just keep using your card like you normally would. That negative balance will automatically pay for your new charges until it's all used up. It’s a completely passive way to sort out the overpayment with zero effort.

- Request a Refund: If you’d rather have the money back in your bank account, you're entitled to a full refund of the overpaid amount. All it takes is a quick call to your credit card issuer to get the ball rolling.

Key Takeaway: A credit balance is your money, plain and simple. Canadian banks will either let you spend it down or give it back to you when you ask. You're always in control.

Getting Your Money Back: A Step-by-Step Guide

Decided you want the cash? The process is straightforward, but it does require you to take action. First, double-check the exact overpayment amount on your online banking portal or your latest statement. Then, flip over your credit card, find the customer service number, and give them a ring.

When you get an agent on the line, just explain that you have a credit balance and would like it refunded. They’ll run through some security questions to confirm it’s you, then ask how you want to receive the funds. Most banks can do a direct deposit right into your chequing account, though some might still mail you a physical cheque.

As for timing, it can vary. You can generally expect the money to land in your account within 7 to 14 business days.

Throughout all this, an app like NeoSpend can be a real lifesaver. Its dashboard pulls all your accounts into one place, making it dead simple to spot a negative balance the second it happens. You can also easily track when your refund has been processed, keeping your finances clear, organized, and under control.

What an Overpayment Does to Your Credit Score

Let's get straight to it. Many Canadians wonder what happens when you overpay your credit card. The two big questions are always: "How does it affect my credit score?" and "Do I earn interest?" The answers are probably not what you expect, and they unlock a surprisingly powerful way to look at your debt.

The biggest, most immediate effect is on your credit utilization ratio—that's just a term for the percentage of your available credit you're actually using. If you overpay and end up with a negative balance, your utilization on that card drops to 0%. This can give your credit score a little nudge in the right direction, since credit bureaus see low utilization as a sign you're managing your finances well.

Can Overpaying Actually Help Your Credit Score?

While that negative balance might bump your score up a few points, it’s not a magic trick for long-term credit health. Some people use this as a short-term strategy right before they apply for a big loan, like a mortgage. The idea is to overpay a credit card just before the statement date, making sure a zero balance gets reported to the credit bureaus.

However, it's not a silver bullet. For a genuinely healthy credit score that lenders trust, nothing beats consistently paying your balance in full every month. That kind of reliability speaks volumes more than a one-time overpayment ever could.

The real power move isn’t about creating a negative balance. It’s about "overpaying" in the sense of paying way more than your minimum payment. This is the real game-changer for getting out of debt.

Overpaying vs. Making Minimum Payments

When it comes to interest, the answer is simple: you won't earn any on that extra cash sitting on your credit card account. It just waits there for your next purchase.

The much more impactful way to "overpay" is to throw more than the minimum payment at your balance each month. This isn't just a good idea; it's a critical strategy for getting ahead financially.

With the average non-mortgage debt for Canadians creeping up to $22,147, just paying the minimum is like trying to bail out a leaky canoe with a teaspoon. High interest rates mean those tiny payments barely make a dent in what you actually owe. By making a conscious choice to overpay, you start attacking the principal balance head-on. This saves you a ton of money on interest and drastically shortens your timeline to being debt-free. You can dig into the numbers in this Equifax Canada consumer trends report.

This is where smart tools come in handy. For instance, NeoSpend helps people manage money smarter by analyzing your spending to find those little pockets of cash you could be putting toward your debt. It helps you see where you can make extra payments, so you can break free from that high-interest cycle faster.

What to Do After an Accidental Overpayment

Sent a bit too much cash to your credit card company? First off, don't panic. It might feel a little strange seeing your credit card owe you money, but it's a super common scenario in Canada and an easy fix. Your money isn't lost.

The first thing to do is just confirm it. Hop into your online banking or mobile app and pull up your credit card statement. You're looking for a negative balance. It’ll show up with a minus sign right in front, something like -$50.00. That's your confirmation that the bank owes you.

Your Next Steps: Leave It or Get It Back?

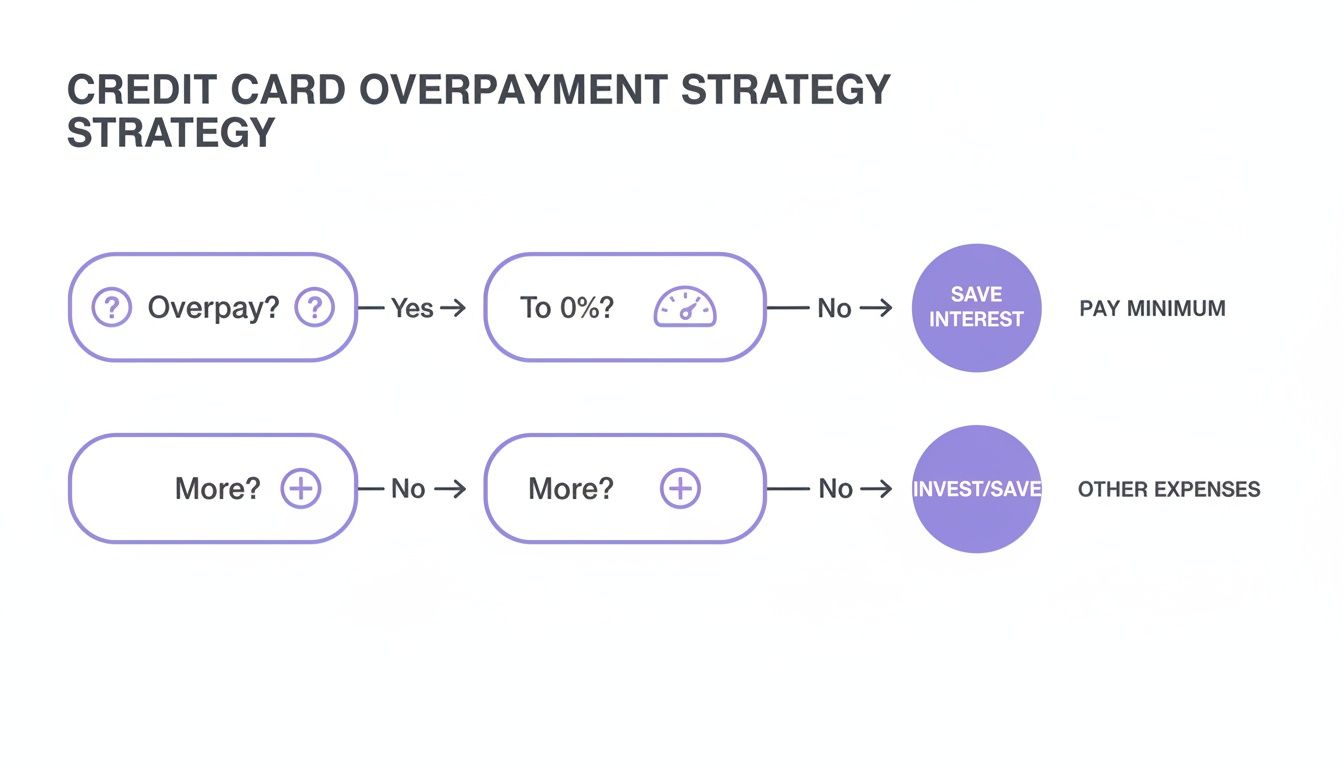

Once you've spotted that negative balance, you basically have two choices. The right one for you really just boils down to whether you need that cash back in your chequing account or not.

- Option 1: Leave It Be: Honestly, the easiest route is to just do nothing. That credit will just sit on your account, waiting to pay for your next purchases. If you have a -$50.00 balance and grab a $30 lunch, your new balance will simply be -$20.00. The problem sorts itself out.

- Option 2: Request a Refund: If you'd rather have the money back in your bank account, you're absolutely entitled to ask for it. This takes a tiny bit of effort on your part, but it's a straightforward process.

This decision tree gives you a quick visual of how to think about it.

As the chart shows, you can let the overpayment credit your future spending or work to get your balance down to zero.

How to Get Your Money Back

If you decide you want that cash back, just find the customer service number on the back of your credit card and give them a call. Make sure you have your account details ready.

Simply explain that you have a credit balance and would like a refund. The agent will walk you through a few identity verification steps and then get the request processed. They'll give you a timeline, but it usually takes about 7-14 business days for the money to show up. It's a good idea to set a calendar reminder to check on it if you haven't seen it by then.

This is where a tool like NeoSpend can really come in handy. Instead of having to dig through different statements, its single dashboard shows all your account balances in one place. An oddity like an overpayment stands out immediately, so you’re never caught by surprise and always feel in control of your money.

Using Overpayments to Your Financial Advantage

Most people overpay their credit card by accident, but what if you did it on purpose? It might sound strange, but a strategic overpayment can actually be a clever tool in your financial kit.

Instead of being a mistake you need to fix, an intentional overpayment can help you hit specific goals, like giving your credit score a little lift or getting a handle on your debt. It’s all about knowing how the system works and making it work for you, especially when you’re gearing up for a big purchase.

Can You Overpay a Credit Card to Boost Your Credit Score Temporarily?

One of the sneakiest—and smartest—ways to use an overpayment is to give your credit score a temporary bump. This is a great little trick for Canadians getting ready to apply for a mortgage, a car loan, or any other major line of credit where every point counts.

Here’s the game plan: pay off your entire balance, then overpay your credit card by a small amount just before your statement closing date. This forces a $0 balance to be reported to the credit bureaus. That means your credit utilization on that card drops to zero, which can nudge your score up just when you need it most.

The Best "Overpayment" Strategy for Crushing Debt

While a negative balance has its uses, the most powerful way to “overpay” is much simpler: just pay more than the minimum payment every single month. This is, hands down, the best way to aggressively tackle high-interest credit card debt and save a ton of money in the long run.

With 54% of Canadians carrying a credit card balance from month to month, this strategy is more important than ever. Many people think it’ll take them more than six months to clear their debt, but you can slash that timeline by making strategic extra payments. You can get more details on these trends in NerdWallet’s Canadian credit card report.

Expert Insight: Just paying the minimum on a high-interest card is a recipe for staying in debt for years. When you consistently pay more, you’re hitting the principal balance directly. That means you pay less interest over time and get to debt-free much faster.

This is where NeoSpend makes a real difference. It helps people manage money smarter by getting to know your spending habits and pointing out where you can afford to chip in a little extra on your payments. With those personalized insights, NeoSpend helps you build the best payment plan to wipe out your debt faster and keep more of your money, bringing your financial goals that much closer.

How NeoSpend Helps You Manage Payments Wisely

Trying to keep track of multiple credit cards, payment due dates, and refunds can sometimes feel like you're juggling too many things at once. A simple slip-up, like an auto-payment going through right after you’ve already paid, or a refund hitting your account unexpectedly, can lead to an accidental overpayment.

While it’s not the end of the world, it does mean your cash is tied up with the credit card company. This is exactly why having a single, clear view of your money is so important.

NeoSpend is built to cut through that financial fog. Instead of hopping between different banking apps to check balances, our dashboard pulls everything into one secure spot. You get a real-time look at all your credit cards at once, making it dead simple to spot a negative balance the second it shows up.

Get Smart Alerts and Stay Ahead of Overpayments

Picture this: you're a young professional in Toronto with a couple of credit cards from different banks. You pay off one card in full, but then a big refund for a cancelled flight finally comes through. It’s easy for that extra credit to get lost in the shuffle.

NeoSpend’s smart alerts are like having a financial watchdog in your corner. Our AI can detect unusual activity—like a sudden negative balance—and will ping you with a notification. This heads-up means that overpaid cash doesn't just sit in your account unnoticed, so you always know exactly where your money is.

A consolidated view of your finances is the first step toward preventing common mistakes. When you can see everything in one place, you’re less likely to overpay a credit card or miss an important due date.

Track Bills and Subscriptions with Ease

Another common reason for overpaying? Good old-fashioned human error. Maybe you did some quick mental math on your balance that was slightly off, or you completely forgot a pending refund was on its way when you made a payment.

The bill and subscription tracking feature in NeoSpend takes all that guesswork out of the picture. It keeps a running tab of what you owe and when it's due, so you're always working with an accurate snapshot of your expenses. This helps eliminate those manual calculation mistakes and lets you manage your cash flow more effectively.

By giving you a complete, up-to-the-minute overview of your financial world, NeoSpend helps you sidestep those common payment pitfalls and handle your money with confidence.

Your Top Questions About Overpaying a Credit Card, Answered

Let's clear up some of the common questions Canadians have when they find a negative balance on their credit card statement. Here are some quick, straightforward answers to help you feel more confident about managing your money.

Can I Overpay My Credit Card to Increase My Spending Limit?

This is a common myth, but the short answer is no. Your credit limit is a set amount your bank trusts you with based on your financial picture. While overpaying does give you a temporary credit balance you can spend down, it doesn't actually raise your official credit limit.

For example: if your limit is $5,000 and you overpay by $200, you technically have $5,200 you can use. But on paper, your credit report will still show that $5,000 limit.

How Long Does It Take to Get a Refund in Canada?

So you've called your bank to get that negative balance refunded. How long will it take? It depends on the bank, but you can typically expect to see the money back in your chequing account or get a cheque in the mail within 7 to 14 business days.

It's always a good idea to just ask your credit card issuer for their specific timeline when you make the request.

Will I Earn Interest if I Overpay My Credit Card?

Unfortunately not. A credit balance on your card won't earn you a single cent of interest. Unlike a high-interest savings account where your money grows, an overpayment just sits there as a credit waiting to be used. It has no positive impact on interest and definitely won't make you any money.

Is It a Good Idea to Overpay My Credit Card Every Month?

It's a fantastic habit to pay your balance off in full every month, but there's no real advantage to consistently overpaying to maintain a negative balance. In fact, if you do it too often, some card issuers might flag it as unusual activity on your account.

The best strategy is simple: just pay what you owe. You'll avoid interest charges and keep your account in good standing.

Key Takeaway: Accidentally overpaying your credit card isn't a problem—it’s an easy fix. The most powerful way to "overpay" is by intentionally paying more than your minimum to crush debt faster. Keeping your payments straight is the key to financial peace of mind.

NeoSpend gives you a single, clear view of all your balances, so you can track your payments with total accuracy and catch any overpayments right away. Feel like you're in control of your finances by trying NeoSpend today.