The official TFSA contribution limit for 2024 is $7,000, but that number doesn't tell the whole story. Your personal maximum TFSA amount is likely much higher.

Why? Any contribution room you didn't use in previous years rolls over, accumulating since you turned 18. Understanding your unique, cumulative total is the key to unlocking the full power of this incredible tax-free savings account.

So, What's Your Actual TFSA Contribution Limit?

Your personal TFSA maximum isn't just the single number announced by the government each year. It's a running total—a personal savings bucket that grows every year you're eligible. This dynamic figure depends on your age, your contribution history, and any withdrawals you've made.

Knowing this number is crucial, as it tells you exactly how much you can deposit to maximize tax-free growth without facing penalties.

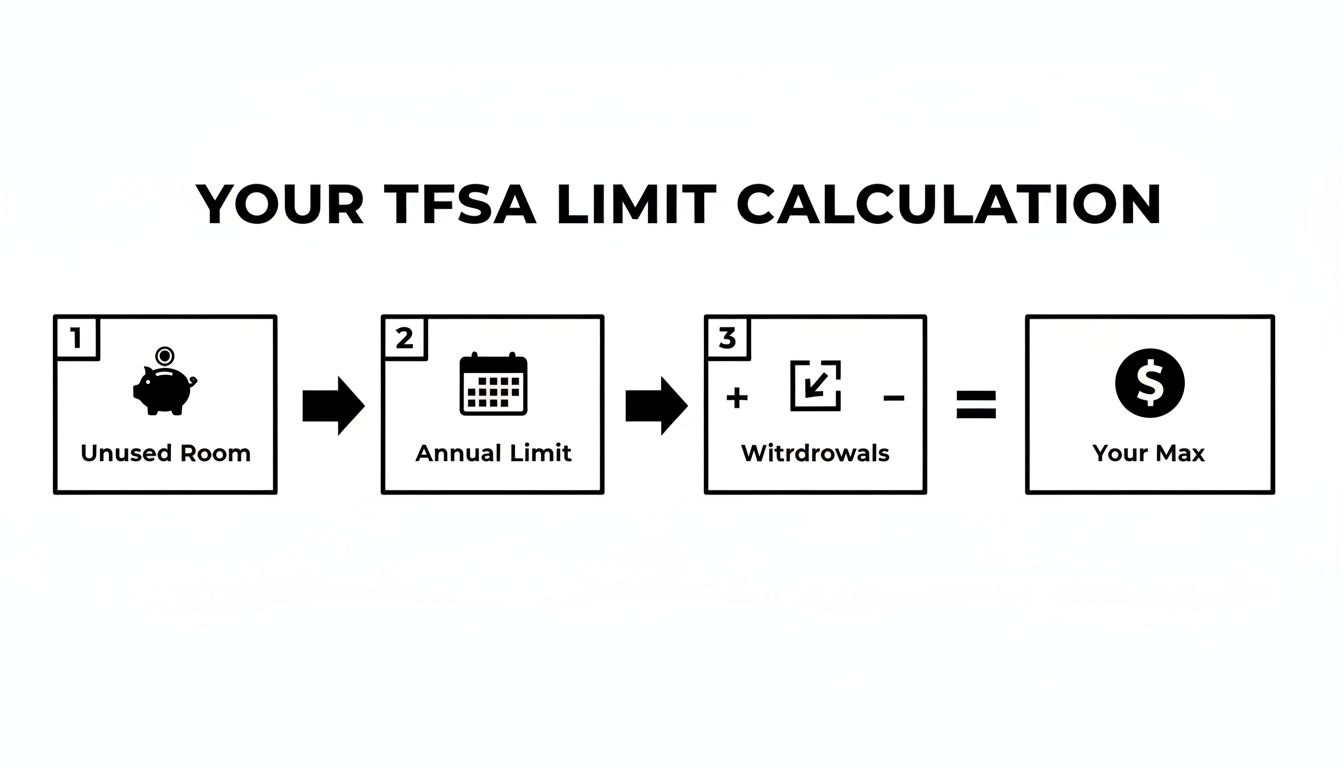

Your total available contribution room is calculated from three key components:

The Annual Limit: This is the new amount set by the government for the current year. For 2024, it's $7,000.

Carry-Forward Room: This is the TFSA's best feature. Any space you didn’t use in previous years is automatically added to this year's limit.

Withdrawals from the Previous Year: Did you take money out last year? The full amount you withdrew is added back to your contribution room on January 1st of the following year.

The Power of Cumulative Contribution Room

This carry-forward feature is incredibly powerful. Let's imagine you became eligible for a TFSA when it launched in 2009 but never contributed. Your available room has been quietly growing ever since.

As of 2024, someone who was 18 or older in 2009 and has never contributed would have a total TFSA contribution room of $95,000. This demonstrates how significantly your personal limit can grow over time. You can see a helpful breakdown of how TFSA limits have changed over the years on Wealthsimple.com.

The biggest mistake Canadians make is assuming the annual limit is all they can contribute. Your real power lies in understanding and using your accumulated room from past years.

This is where smart money management makes a difference. Using a tool like NeoSpend to track your finances gives you a clear view of your cash flow, making it easier to see how much you can comfortably set aside in your TFSA. Knowing your personal maximum is the first step to achieving tax-free growth and avoiding costly over-contribution penalties.

How Your Personal TFSA Contribution Room Works

While the annual TFSA limit gets the most attention, your personal contribution room is what truly matters. It’s not a one-size-fits-all figure; it’s a dynamic limit shaped by your financial history. Think of it less as a strict yearly allowance and more as a personalized savings bucket that expands over time.

Your total room is a combination of three key elements. Understanding how they work together is the secret to maximizing your TFSA without accidentally incurring penalties.

The Three Pillars of Your TFSA Room

Instead of focusing on a single number, think of your TFSA limit as a simple formula that adds three amounts together to determine your unique maximum for the year.

The Current Year's Limit: The fresh contribution room the government grants every eligible Canadian for the year.

Unused Carry-Forward Room: This is the TFSA's superpower. Any room you didn't use in past years rolls forward indefinitely. You never lose it.

Previous Year's Withdrawals: If you took money out of your TFSA last year, that exact amount is added back to your contribution room. Just remember, this happens on January 1st of the next calendar year.

This diagram illustrates how these three parts combine to form your total contribution room.

As you can see, it all adds up. The cumulative nature of the TFSA ensures you’re never penalized for not being able to contribute the maximum amount every single year.

A Real-World Canadian Example

Let's make this practical with an example. Meet Chloe. She turned 18 several years ago and has accumulated $20,000 in unused contribution room. In 2023, she didn't contribute anything but withdrew $5,000 for an emergency home repair.

For 2024, Chloe’s total contribution room is calculated as follows:

$20,000 (Her Unused Room) + $7,000 (2024 Annual Limit) + $5,000 (Her 2023 Withdrawal) = $32,000

Just like that, her personal limit for the year is significantly higher than the standard $7,000. This flexibility is what makes the TFSA such a powerful savings tool for Canadians.

A common mistake involves the timing of withdrawals. Remember, any amount you take out is only added back to your room on January 1st of the next year. Re-contributing that money in the same year without having enough existing room can lead to over-contribution penalties.

Juggling these numbers doesn't have to be complicated. An app like NeoSpend helps you see your savings patterns and withdrawals in one place. With a clear financial picture, you can track what you’ve put in, plan your next deposit confidently, and ensure you stay within your personal maximum TFSA amount.

Why Does the TFSA Limit Change Every Year?

If you've been following your TFSA, you've likely noticed the annual contribution limit isn't static. One year it’s $6,000, the next it’s $6,500. This isn't arbitrary; it’s part of a system designed to protect the value of your savings.

The government adjusts the TFSA limit over time by linking it to Canada's inflation rate, as measured by the Consumer Price Index (CPI), and then rounding it to the nearest $500. This helps your savings keep pace with the rising cost of living. You can see the year-by-year changes in this TFSA contribution limit overview on MoneySense.ca.

Keeping Your Savings Power Strong with Inflation Indexing

The primary reason for the changing limit is inflation. Simply put, the money you have today will buy less in the future. That’s inflation—the gradual decrease in your money's purchasing power.

To ensure your TFSA savings don’t lose value over time, the federal government indexes the limit to the Consumer Price Index (CPI). As the cost of living rises, the TFSA limit is adjusted upward to match.

The limit doesn't increase by a small, precise amount each year because the government rounds the inflation-adjusted figure to the nearest $500. This is why the limit might remain the same for a few years before jumping up—it waits for cumulative inflation to push it past the next $500 milestone.

Indexing is a crucial feature. It’s the government's commitment to ensuring the TFSA remains a powerful long-term savings tool, so its value isn't slowly eroded by rising costs.

A Quick Look at the TFSA Limit’s History

The evolution of the limit shows its stability and steady growth. It began in 2009 with a $5,000 limit. Since then, it has progressed through several key stages:

2009-2012: Remained steady at $5,000.

2013-2014: Increased to $5,500 due to inflation.

2015: Experienced a one-time jump to $10,000.

2016-2018: Reverted to $5,500 after a policy change.

2019-2022: Climbed to $6,000.

2023: Rose again to $6,500.

2024: Reached its current level of $7,000.

This progression from $5,000 to $7,000 demonstrates a long-term commitment to helping Canadians build wealth. Understanding that these changes are tied to economic factors can give you confidence in your financial planning. It is important that you manage your money and see how your contributions align with the changing limits, so you can simplify the process of maximizing your tax-free growth.

How To Calculate Your Personal Maximum TFSA Amount

Knowing the TFSA rules is one thing, but calculating your personal contribution limit is what puts you in control. While the CRA provides official figures, you don't have to wait for them to update their systems to make contributions.

The good news is you can use a simple, reliable formula to determine your exact room right now, allowing you to invest your money early in the year.

The Go-To Formula For Your TFSA Room

Calculating your personal contribution room is straightforward. You just need to add three key numbers together.

The Simple Formula: [Unused Past Room] + [Current Year’s Limit] + [Last Year’s Withdrawals] = Your Total Contribution Room

This formula works for everyone, whether you're a seasoned contributor or just getting started. Let's apply it to a few common Canadian scenarios.

Putting The Formula Into Practice With Canadian Scenarios

To make this crystal clear, let's walk through a few common situations. We'll use the 2024 annual limit of $7,000 for all examples.

Scenario 1: The New Grad

Meet David. He recently started his career and has saved up some cash but hasn't contributed much to his TFSA yet. He has $15,000 in unused room from previous years and made no withdrawals last year.

His calculation: $15,000 (Unused Room) + $7,000 (2024 Limit) + $0 (Withdrawals) = $22,000

David's total TFSA room for 2024 is $22,000.

Scenario 2: The On-and-Off Saver

Now, let’s look at Priya. She contributes to her TFSA when she can. She has $5,000 in unused room carried forward. Last year, she withdrew $10,000 for a dream vacation.

Her calculation: $5,000 (Unused Room) + $7,000 (2024 Limit) + $10,000 (2023 Withdrawal) = $22,000

Priya also has $22,000 of room for 2024. This shows how taking money out one year increases your contribution limit the next year.

Scenario 3: The Home Buyer

Finally, there's Liam. He used his TFSA to save for a down payment and had maxed it out, leaving him with $0 in unused room. Last year, he withdrew $50,000 to buy his first home.

His calculation: $0 (Unused Room) + $7,000 (2024 Limit) + $50,000 (2023 Withdrawal) = $57,000

Liam now has a massive $57,000 of room available to start rebuilding his savings for his next big financial goal.

Contribution Room Scenarios

Here’s a side-by-side comparison showing how different histories impact current contribution room.

| Scenario | Previous Contributions | Last Year's Withdrawal | Current Year Room |

|---|---|---|---|

| The New Saver | Has $15,000 of unused room. | $0 | $22,000 |

| The On-and-Off Saver | Has $5,000 of unused room. | $10,000 | $22,000 |

| The Big Spender | Fully maxed out ($0 unused). | $50,000 | $57,000 |

As you can see, past withdrawals play a huge role in determining your available room for the year ahead.

Keeping track of your own numbers is essential. Using an app like NeoSpend makes this easier by helping you monitor your savings and withdrawals in one place. When you have a clear picture of your finances, calculating your TFSA room is a simple, stress-free task that keeps you on track.

Avoiding The Costly Mistake Of Over-Contributing

Knowing your personal TFSA limit is more than just good financial practice—it’s crucial for protecting your money. The Canada Revenue Agency (CRA) takes over-contributions very seriously, and the penalty can quickly erode your hard-earned savings.

If you contribute more than your limit, you will be charged a 1% tax on the highest excess amount for every month the extra money remains in your account. This penalty continues to accumulate until you withdraw the excess funds or new contribution room opens up the following year to absorb it.

A 1% monthly tax might not sound like much, but it adds up fast. A simple miscalculation can become a significant financial drain, undermining the tax-free growth you were trying to achieve.

How Over-Contribution Penalties Add Up

Let's illustrate with a real-world example. Imagine you miscalculated your room and accidentally over-contributed by $3,000 on February 1st.

The Penalty: A 1% tax on $3,000 is $30 per month.

The Cost: If you don't notice the error until the end of the year, that's 11 months of penalties.

Total Penalty: 11 months x $30/month = $330.

In this scenario, you’ve paid $330 in taxes, completely negating the benefits of your TFSA. This is why careful tracking is so important. You can find more details about its history and how TFSA limits are set from Harvest Portfolios.

The most reliable way to avoid penalties is to know your exact limit. Your best source of information is the CRA’s "My Account" portal, which displays your official contribution room as of January 1st each year.

Your Best Defences Against Over-Contributing

Preventing this costly mistake comes down to staying organized. Here are two practical tips:

Check Your CRA My Account: Before making a large contribution, log in to your CRA My Account to see the official contribution room figure. Keep in mind it may not be updated until February or March for the current year.

Track Your Contributions: Maintain your own record of all TFSA deposits and withdrawals throughout the year.

Staying on top of your limit is much easier with the right tools. Using a budgeting app like NeoSpend lets you earmark savings specifically for your TFSA. By tracking every dollar you set aside, you create a clear, running tally of your contributions throughout the year, making sure you never accidentally step over your personal maximum. It’s a simple habit that keeps you organized, in control, and safely within your limit.

Smart Strategies To Maximize Your TFSA Growth

Understanding the rules is the first step, but building wealth with your TFSA comes down to consistent action. The most effective strategy is to automate your contributions. This shifts saving from an afterthought to a priority.

The best way to do this is to "pay yourself first." Instead of saving what's left at the end of the month, set up an automatic transfer from your chequing account to your TFSA every payday. Even a small, regular contribution adds up significantly over time, thanks to the power of compounding.

Find Your Hidden Savings

To contribute consistently, you need to know where your money is going. This is where a smart tool like NeoSpend can be a game-changer. It provides insights into your spending habits, and show you where you can earmark extra cash to direct toward your savings goals.

See where your money really goes: Automatically categorize your spending to identify areas where you can cut back.

Set clear savings goals: Create a specific TFSA goal in the app to stay motivated and track your progress.

Automate with confidence: Once you know how much you can comfortably save, set up recurring transfers in your bank to make your contributions effortless.

The key to maximizing your TFSA’s potential isn’t making one large deposit. It's building the small, consistent habit of saving that snowballs into significant, tax-free growth over time.

By making TFSA contributions a priority, you take control of your financial future. NeoSpend provides the clarity and tools to build that consistency, helping you reach your maximum TFSA amount and watch your wealth grow.

Answering Your Top TFSA Limit Questions

Let's clear up some of the most common questions Canadians have about TFSA limits. This will help you get the details right and manage your account with confidence.

What Happens If I Contribute Before The CRA Updates My Room?

This is a common timing issue. At the beginning of the year, you have new contribution room, but your CRA My Account may not reflect it yet. So, what should you do?

The safest approach is to wait until the CRA updates its records, usually by February or March. If you have diligently tracked your contributions and withdrawals, you can contribute based on your own calculations, but be 100% certain they are accurate.

A good compromise is to contribute an amount you know is safely under your limit, then add more once the CRA provides the official figure.

Does Investment Growth Affect My Contribution Room?

No, and this is one of the TFSA's greatest advantages. Your contribution room is only affected by the money you deposit and withdraw.

Any dividends, interest, or capital gains your investments earn inside your TFSA are completely tax-free. More importantly, this growth does not use up any of your contribution room, allowing your money to compound without limits.

This is a powerful feature. It means your investments can grow much faster than in a taxable account, and you never have to worry that a successful year in the market will impact your personal maximum TFSA amount.

How Is My TFSA Room Calculated If I'm A New Resident In Canada?

Welcome to Canada! For new residents, TFSA eligibility begins in the year you meet three conditions: you turn 18, you become a resident of Canada for tax purposes, and you have a valid Social Insurance Number (SIN).

You do not receive retroactive contribution room for the years you lived outside of Canada before becoming a resident. For example, if you moved to Canada in 2023 at age 30, your TFSA contribution room would start from that year. You would not get credit for the years between turning 18 and your arrival.

Key Takeaway: Your personal maximum TFSA amount is a cumulative total of the annual limits, your unused room from previous years, and any withdrawals made in the prior year. Calculating this number accurately is the key to maximizing tax-free growth and avoiding penalties.

Taking control of your finances starts with a clear view of your money. NeoSpend provides the tools to track your savings and contributions effortlessly, so you can make the most of your TFSA with confidence. Discover how NeoSpend simplifies money management.