Ready to start investing in Canada? It’s far more straightforward than you might think. The process comes down to a few key steps: getting your finances in order, picking the right investment account, choosing a platform, and building a simple, low-cost portfolio. This guide will walk you through everything, step-by-step.

Why Bother Investing? It's Your Path to Financial Freedom

Let's be real—just stashing cash in a savings account isn't going to cut it anymore. With the cost of living always on the rise (thanks, inflation), your money slowly loses its buying power over time. Investing is how you get ahead of the curve. It’s the single most effective way for everyday Canadians to build real, long-term wealth.

Think of it like this: saving is like parking your money in a garage. It's safe, but it isn't going anywhere. Investing is like putting that money on an escalator. It’s about making your money work for you, so you can eventually hit your big financial goals—whether that’s buying a home, retiring without worry, or paying for your kid's education.

The Magic of Compounding

The secret sauce behind all of this? A powerful little concept called compounding.

Compounding is when the returns your investments earn start generating their own returns. It's like a snowball rolling down a hill—it starts small, but as it rolls, it picks up more snow, getting bigger and faster. Your money does the exact same thing. For example, a small, consistent investment of $100 a month can balloon into a surprisingly large amount over a few decades, all thanks to this powerful effect.

The most important thing is to just get started. Time is your best friend in the market, giving compounding all the room it needs to work its magic. Seriously, even small, regular contributions can grow into a massive nest egg down the road.

The Basic Building Blocks of Your First Portfolio

You don't need to become a stock market wizard to get started. For most Canadians, the simplest approach is the best one. You’ll really only need to know about two main types of investments:

- Stocks (or Equities): When you buy a stock, you're buying a tiny piece of a public company, like Royal Bank of Canada or Shopify. If the company does well, the value of your piece can go up.

- Exchange-Traded Funds (ETFs): These are a beginner's best friend. An ETF is basically a big basket that holds hundreds or even thousands of different stocks (and sometimes bonds). Buying a single share of an ETF instantly diversifies your money across all those companies. It's diversification on easy mode.

But before you invest a single dollar, you need to know where your money is going. A clear budget gives you control and shows you exactly how much you can comfortably invest each month. This is where a smart money management app like NeoSpend helps people manage money smarter. It lets you see all your accounts in one place to easily spot those extra dollars you can put to work.

Get Your Financial House in Order Before You Invest

It's tempting to jump right into the stock market, but hitting the ground running without a solid financial base is like building a house on a shaky foundation. Before you put a single dollar into an investment, you need to get your day-to-day money sorted. This isn’t about putting off your wealth-building goals; it’s about making sure you start from a place of strength.

Think of it as a pre-flight checklist. Ticking these boxes creates a crucial safety net. It protects you from being forced to sell your investments at the worst possible time—like during a market dip—just to cover a surprise expense.

Figure Out Where Your Money is Actually Going

First things first: you need a clear picture of your cash flow. You can't figure out how much you can afford to invest if you have no idea where your paycheque disappears every month. This is where a budget comes in, and no, it doesn’t have to be a nightmare spreadsheet.

Just try tracking your income and spending for a month. The process puts your habits in black and white, and you might be shocked by what you find. That daily Tim Hortons run or a few forgotten subscriptions can really add up.

The NeoSpend app automates this whole process. Link your Canadian bank accounts and credit cards, and it crunches the numbers for you, automatically sorting your spending. You get an instant, clear view of your financial life, making it easy to spot where you can trim the fat and free up cash for investing.

Crush Your High-Interest Debt

Not all debt is created equal. A mortgage with a low interest rate is one thing; credit card debt at 19.99% is a completely different beast. High-interest debt is a five-alarm fire for your finances because the interest charges will almost certainly grow faster than your investments.

Think about it: if you have a $5,000 credit card balance at 20% interest, your investments would need to return 20% every single year just for you to break even. Paying off that credit card, on the other hand, is a guaranteed 20% return on your money. You can't beat that, and it's completely risk-free.

Pro Tip: Make it your absolute priority to pay off any debt with an interest rate above 7-8%. We’re talking credit cards, payday loans, and sometimes even personal lines of credit. Get them gone before you start investing seriously.

Build Your Emergency Fund

Life happens. The car breaks down, the dishwasher floods the kitchen, or a job loss comes out of nowhere. An emergency fund is your financial shield—a pool of cash set aside for exactly these kinds of unwelcome surprises.

The goal is to have 3 to 6 months' worth of essential living expenses tucked away. To get your number, just add up your non-negotiable monthly bills:

- Rent or mortgage

- Utilities (hydro, internet, etc.)

- Groceries and gas

- Insurance premiums

- Minimum debt payments

So, if your essential monthly costs are around $3,000, a healthy emergency fund would be between $9,000 and $18,000. Park this money in a high-interest savings account (HISA). It needs to be safe and easy to access, but keep it separate from your daily chequing account so you're not tempted to dip into it.

Know Your "Why": Define Your Goals

Finally, ask yourself the most important question: what am I actually investing for? Your answer is the blueprint for your entire investment strategy. Every financial goal has a timeline, and that timeline dictates how much risk you can comfortably take on.

- Short-Term Goals (1-3 years): This could be a down payment for a car or a big trip to Banff. Any money you need this soon should be kept far away from the stock market in something super safe.

- Medium-Term Goals (4-9 years): Maybe you're saving for a house down payment or a wedding. Here, you could consider a more balanced portfolio with a mix of stocks and bonds.

- Long-Term Goals (10+ years): This is the classic stuff—retirement or saving for your kids' education (RESP). With a long runway, you can generally take on more risk for a shot at higher returns.

Knowing your "why" is what will keep you going. It helps you stay motivated and, more importantly, stay the course when the market gets a little turbulent.

Choosing the Right Canadian Investment Accounts

Once you’ve built a solid financial foundation, the next move is picking the right accounts. In Canada, where you invest is just as important as what you invest in. Think of investment accounts as special containers for your stocks and ETFs. Some of these containers come with incredible tax benefits designed by the government to encourage us to save. Using them smartly can save you thousands in taxes over your lifetime.

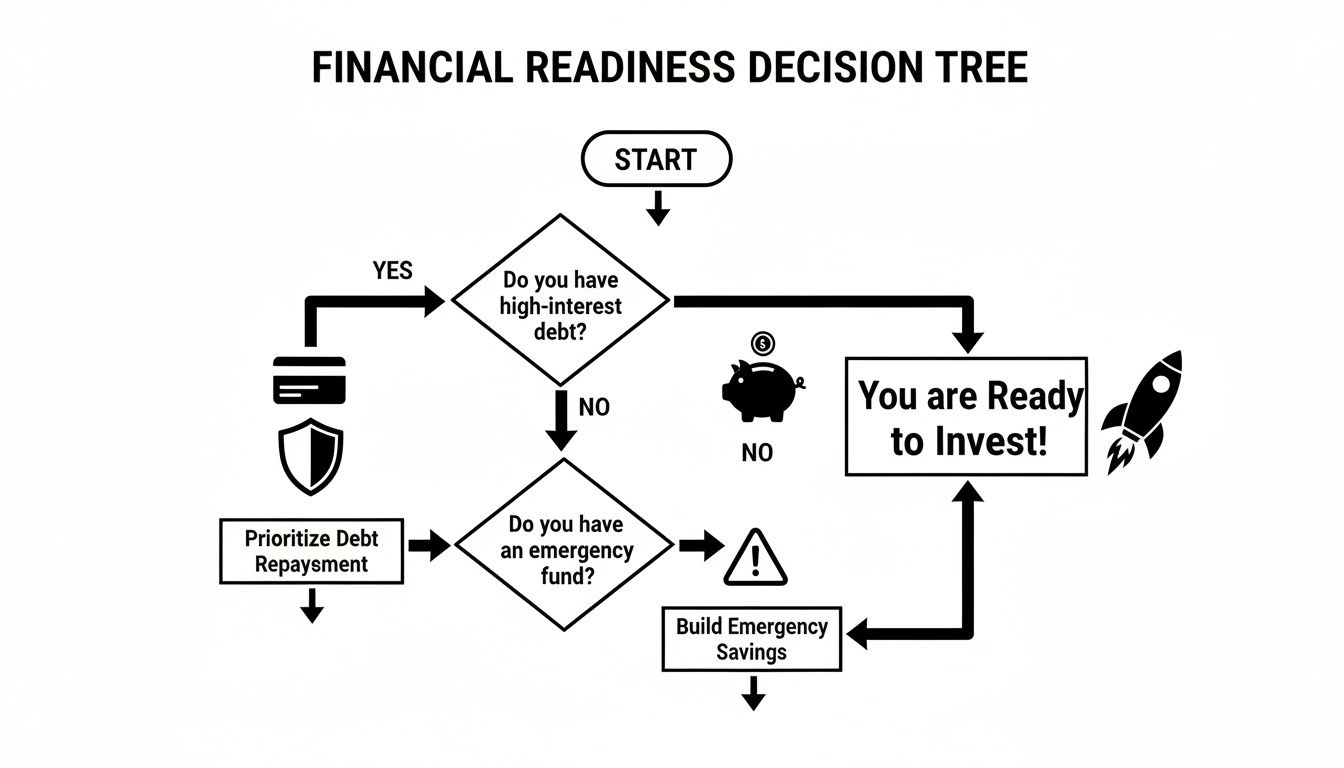

Before you jump in, it's worth taking a quick self-assessment to see if you're truly ready. This decision tree is a great visual guide.

The takeaway is clear: tackle high-interest debt and build that emergency fund before you start investing.

The TFSA: Your Flexible Friend

The Tax-Free Savings Account (TFSA) is, hands down, the most powerful investment tool for most Canadians. Don't let the name fool you. It's not just for "savings"—it's a full-blown investment account where your growth and withdrawals are 100% tax-free.

Every year, the government gives you a certain amount of contribution room. For 2024, that amount is $7,000. If you've been 18 or older since 2009 and never put a dime in, your total room could be as high as $95,000.

Here's a real-world Canadian example:

Take Sarah, a graphic designer in Toronto making $60,000 a year. She's saving for a condo down payment and wants flexibility. The TFSA is perfect. Her money can grow, and when she's ready to buy, she can withdraw it all tax-free. Plus, she gets that contribution room back the next year. It’s a win-win for short and long-term goals.

The RRSP: Your Retirement Powerhouse

The Registered Retirement Savings Plan (RRSP) is the original workhorse for retirement savings in Canada. Its main superpower is the immediate tax deduction. Every dollar you contribute to your RRSP can be deducted from your taxable income, which often leads to a nice tax refund come April.

Your money grows tax-deferred inside the account. You only pay tax when you withdraw it, which is typically in retirement when you're likely in a lower tax bracket.

Your contribution limit is 18% of your previous year's earned income, up to a maximum ($31,560 for the 2024 tax year), plus any unused room you've accumulated.

Who is the RRSP perfect for?

Let's look at David, an engineer in Calgary earning $120,000. He's in a high tax bracket and wants to lower his tax bill now. By contributing $20,000 to his RRSP, he drops his taxable income to $100,000. This will likely trigger a big tax refund, which he can then turn around and reinvest. Smart.

TFSA vs. RRSP: Which Account Is Right for You?

| Feature | Tax-Free Savings Account (TFSA) | Registered Retirement Savings Plan (RRSP) |

|---|---|---|

| Primary Benefit | Tax-free growth and tax-free withdrawals. | Tax-deductible contributions and tax-deferred growth. |

| Contribution Limit (2024) | $7,000 per year, plus unused room from previous years. | 18% of prior year's earned income, up to $31,560. |

| Withdrawal Rules | Withdraw anytime, tax-free. Contribution room is restored the next calendar year. | Withdrawals are taxed as income. Contribution room is lost permanently. |

| Best For... | Lower-to-middle income earners, saving for short-term goals (down payment, car), or anyone who values flexibility. | High-income earners looking to reduce their current tax bill and save for long-term retirement goals. |

| Impact on Gov't Benefits | Withdrawals do not count as income, so they don't affect benefits like GIS or OAS. | Withdrawals count as income and can reduce eligibility for income-tested government benefits in retirement. |

For many people, the best strategy involves using both accounts. But if you're just starting, the TFSA often offers more flexibility and is easier to understand.

Other Important Accounts to Know

- Registered Education Savings Plan (RESP): If you have kids, this is a no-brainer. You save for their post-secondary education, and the government chips in with the Canadian Education Savings Grant (CESG), matching 20% of your contribution up to $500 per year. It's free money for your child's future.

- Non-Registered Accounts: Once you've maxed out your TFSA and RRSP, you can use a non-registered (or taxable) account. There are no contribution limits, but you'll have to pay capital gains tax on your investment profits.

Juggling these accounts can get messy. This is where an app like NeoSpend really shines. It helps you get a single, clear view of your entire investment picture, making it simpler to track your progress and see if you're making the most of each account's tax advantages.

Finding the Right Canadian Investment Platform For You

Okay, you’ve figured out which account to open (hello, TFSA!). Now for the fun part: deciding where to actually open it. The platform you pick is your command centre for buying, selling, and watching your money grow. In Canada, you’ve basically got three main paths, each built for a different kind of investor.

Robo-Advisors: The Set-It-and-Forget-It Approach

New to investing and feeling overwhelmed? A robo-advisor might be your new best friend. These are digital platforms that use smart algorithms to build and manage a diversified portfolio for you. You just answer a few questions about your goals and risk tolerance, and the technology takes it from there. Platforms like Wealthsimple have made this approach super accessible for Canadians.

- Who it’s for: Beginners who want a simple, automated, and low-cost way to invest without making day-to-day decisions.

- The upside: Super easy to get started, low fees (usually around 0.5%), and they handle all the rebalancing for you.

- The downside: You don't get to pick individual stocks or ETFs, and human advice is limited.

This is perfect for someone like Maria, a busy nurse in Halifax who wants her money to work for her but has zero interest in researching stocks. She just wants to set up automatic deposits and know her money is in good hands.

Discount Brokerages: The Do-It-Yourself Route

If you like to be in the driver's seat, a discount brokerage (or online brokerage) is your lane. This is the DIY option where you get direct access to buy and sell individual stocks, ETFs, and more. All the big Canadian banks have one (like RBC Direct Investing), and there are great independent players like Questrade too. This path takes more effort but gives you total flexibility and the lowest ongoing costs.

Choosing a discount brokerage means you're taking on the responsibility of building and maintaining your own portfolio. It offers the ultimate control but requires a willingness to learn the basics.

This is the right fit for someone like Liam, a tech enthusiast in Waterloo who enjoys digging into company research. He wants to build his own portfolio of specific tech ETFs, and a discount brokerage gives him the low-cost freedom to do just that.

Traditional Financial Advisors: The Full-Service Guidance Model

For those who want a real person to guide them through their entire financial life—not just investing—a traditional financial advisor is the classic choice. You'll work one-on-one with a professional who can help with retirement planning, taxes, and your estate. This high-touch service naturally comes with higher fees, often 1% to 2% (or more) of your assets each year.

See the Big Picture with NeoSpend

No matter which path you take, it’s easy to end up with accounts all over the place. NeoSpend is a game-changer here. You can securely link all your different accounts—yep, including your new investment accounts—to get a single, real-time dashboard of your entire financial world. Instead of juggling multiple logins, you can see your net worth in one place, which helps you stay motivated and make smarter decisions.

How to Build Your First Low-Cost Portfolio

Alright, this is where the rubber meets the road—picking your actual investments. The best approach for most beginners is shockingly simple. You don't need to be a stock-picking wizard. Instead, the modern, smarter way is to build a powerful, cheap portfolio with just one or two investments. The goal isn't to find the next Amazon; it's to own a tiny piece of the entire global economy.

The Magic of All-in-One ETFs

The single biggest game-changer for new investors in Canada has been the arrival of all-in-one Exchange-Traded Funds (ETFs). Think of them as a complete, globally diversified portfolio crammed into one single ticker. When you buy a single share of an all-in-one ETF, you are instantly buying thousands of stocks and bonds from companies all over the world. It’s the ultimate "set it and forget it" solution because the fund manager handles all the diversification and rebalancing for you. You buy one thing, and that's it. You're done.

This strategy lets you capture the growth of the entire market. For example, historically, the Canadian stock market has delivered positive long-term returns despite short-term fluctuations. By owning a piece of everything through an ETF, you tap into that long-term potential. You can see more details on the performance of the Canadian stock market here.

Matching Your Portfolio to Your Risk Tolerance

The only choice you need to make is picking the all-in-one ETF that matches your personal risk tolerance—a fancy way of saying how comfortable you are with your account balance bouncing around. It depends on your age, when you need the money, and your personality.

Your portfolio will generally be a mix of two things:

- Stocks (Equities): The growth engine. They have higher potential returns but come with more bumps along the road.

- Bonds (Fixed Income): The shock absorbers. They're more stable and provide a cushion when the stock market gets rocky.

An all-in-one ETF just pre-packages this mix for you. If you're young and investing for retirement decades away, you'd probably lean towards an ETF with more stocks. If you're saving for a down payment in five years, you'd want the stability of more bonds.

The Big Idea: You aren't trying to beat the market; you're trying to be the market. A low-cost, diversified ETF portfolio ensures you capture the returns of global economic growth over the long term, which is the most reliable way to build wealth.

Sample Beginner ETF Portfolios for Canadians

To make this feel more real, let's look at a few popular all-in-one ETFs from providers like Vanguard and iShares. Think of these as examples to show you how it works—always do your own digging to find the perfect fit. The table below breaks down a few options by risk profile. Each ticker symbol represents a different mix of stocks and bonds.

| Risk Profile | Example All-in-One ETF (Ticker) | Stock/Bond Allocation | Ideal For |

|---|---|---|---|

| Conservative | Vanguard Conservative ETF Portfolio (VCNS) | 40% Stocks / 60% Bonds | Investors with a short time horizon or very low risk tolerance who prioritize capital preservation. |

| Balanced | Vanguard Balanced ETF Portfolio (VBAL) or iShares Core Balanced ETF Portfolio (XBAL) | 60% Stocks / 40% Bonds | A great middle-of-the-road option for those with medium-term goals or a moderate comfort level with risk. |

| Growth | Vanguard Growth ETF Portfolio (VGRO) or iShares Core Growth ETF Portfolio (XGRO) | 80% Stocks / 20% Bonds | Long-term investors (10+ years) who are comfortable with more volatility for a chance at higher returns. |

| All-Equity | Vanguard All-Equity ETF Portfolio (VEQT) or iShares Core Equity ETF Portfolio (XEQT) | 100% Stocks / 0% Bonds | Investors with a very long time horizon and a high risk tolerance who want to maximize their growth potential. |

Picking one of these ETFs through your discount brokerage is one of the simplest and most effective ways to start building real wealth in Canada.

Bringing It All Together with NeoSpend

Building your portfolio is a massive win, but seeing how your investments fit into your overall financial picture is key to staying motivated. This is where a tool like NeoSpend becomes your secret weapon. You can link all your accounts—including your shiny new investment portfolio—into a single, clean dashboard. You get a real-time snapshot of your net worth, letting you see exactly how your contributions are making a difference.

Your Top Investing Questions Answered

Dipping your toes into the investing world for the first time? It's totally normal to have questions. Let's tackle some of the most common ones from new Canadian investors so you can move forward with clarity.

How Much Money Do I Really Need to Start?

This is probably the biggest myth holding people back: the idea that you need a huge lump sum. Honestly, that couldn't be further from the truth. You can get started with as little as $1.

No, that’s not a typo. Thanks to Canadian robo-advisors and commission-free trading platforms, the old barriers are gone. What matters most isn't the amount you start with, but the simple act of starting and staying consistent. An automatic transfer of $25 a week is infinitely more powerful over the long haul than waiting five years to save up thousands to invest all at once.

Are My Investments Actually Safe in Canada?

Yes, Canada has a solid safety net in place that gives investors peace of mind. The vast majority of investment firms are members of the Canadian Investor Protection Fund (CIPF). The CIPF protects the money in your accounts for up to $1 million per account type (so, $1M for your RRSP, another $1M for your TFSA, etc.). This covers you in the highly unlikely scenario that your investment firm goes out of business.

It’s important to know what the CIPF doesn't cover. It protects you from your brokerage failing, but it does not protect you from the normal ups and downs of the market. Investing always carries risk, and your portfolio's value will fluctuate.

What Fees Should I Be Watching Out For?

Fees are the silent killer of your investment returns. Keeping your costs low is one of the most effective things you can do. Here are the big ones to watch:

- Management Expense Ratio (MER): The yearly fee that ETF and mutual fund companies charge for managing the fund. It’s shown as a percentage and taken right out of your investment automatically. Stick to funds with low MERs—anything under 0.25% is fantastic.

- Trading Commissions: If you're using a discount brokerage, you might get charged a fee every time you buy or sell. The good news is that many Canadian platforms now offer commission-free buying for ETFs.

- Management Fees: Robo-advisors charge their own fee on top of the MERs, usually between 0.25% and 0.50%. This pays for the service of building and managing your portfolio so you don't have to.

How Often Should I Be Checking My Portfolio?

For a long-term, hands-off investor, the answer is way less than you think: almost never. It's tempting to log in and check your balance every day, but that habit often causes more harm than good. Daily market swings are just noise and can lead to emotional decisions, like panic selling when things dip. A healthier approach is to schedule a check-in just once or twice a year to ensure your strategy still aligns with your goals. For your day-to-day focus, use a tool like NeoSpend to keep tabs on your budget and saving rate—the numbers you can actually control.

Key Takeaway

Starting to invest in Canada is more accessible than ever. The key is to build a solid financial foundation first: create a budget, crush high-interest debt, and build an emergency fund. Then, choose the right tax-advantaged account (like a TFSA), pick a low-cost platform, and build a simple portfolio with an all-in-one ETF. Stay consistent, and let time do the heavy lifting.

Ready to get a crystal-clear view of your entire financial life? With NeoSpend, you can connect all your bank and investment accounts in one place, track your progress automatically, and find more money to put toward your goals. Take control of your finances and start your journey with NeoSpend today.