Learning how to save money in Canada isn’t about luck; it’s about having a clear plan. A good plan involves setting specific goals, building smart habits, and using the right tools to automate your progress. This is how saving money becomes a natural part of your financial life instead of a monthly chore.

Building Your Financial Foundation in Canada

Let's be real: with the cost of living on the rise, saving money in Canada can feel like a huge challenge. But it's not impossible. This guide is designed to provide you with a straightforward, practical plan to get your finances on track and build a secure future.

Saving money is more than just putting cash aside; it’s about creating a foundation for your dreams. Whether you're saving for a down payment on a condo in Calgary, building a healthy emergency fund for peace of mind, or planning for retirement, the principles are the same.

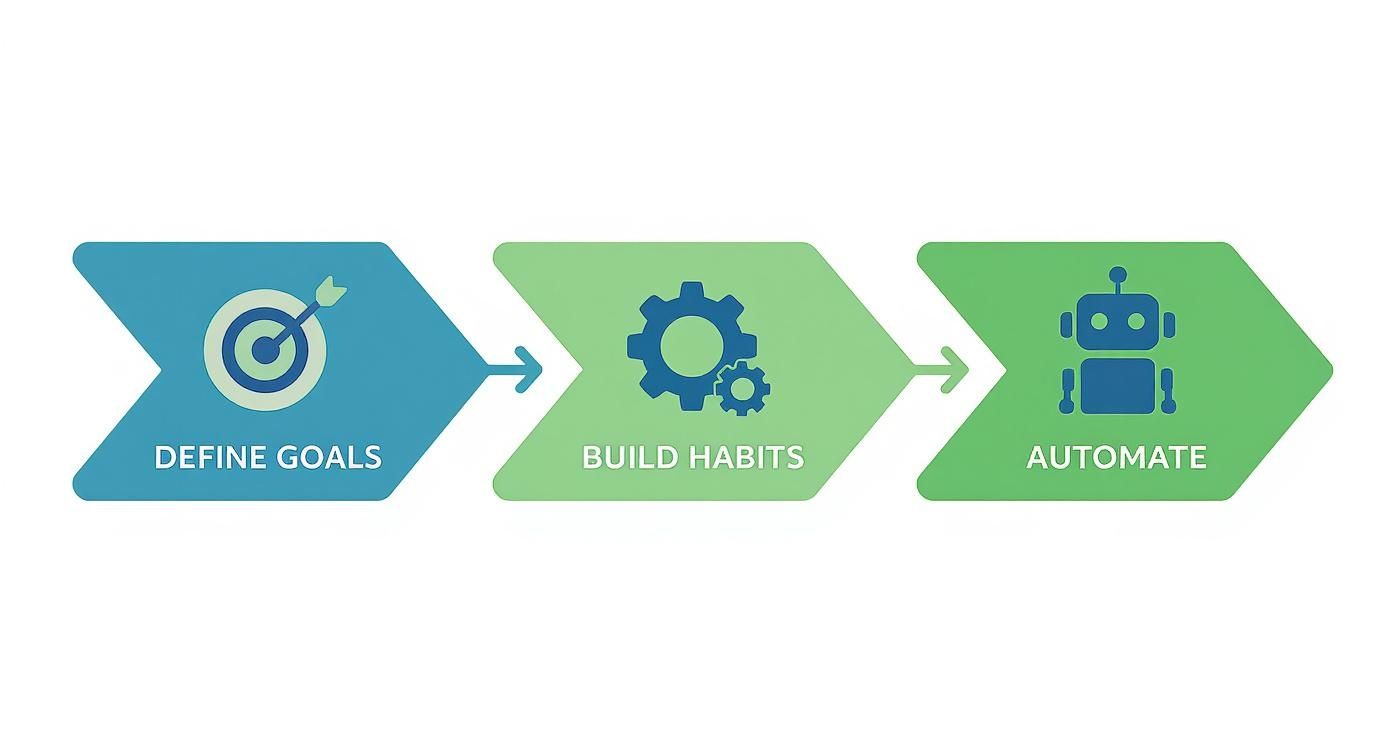

The process is simpler than you might think and boils down to three key steps. This visual breaks down exactly what it takes to build a strong financial base.

As you can see, success starts with knowing what you’re working toward (defining goals), turning those intentions into consistent actions (building habits), and then making it all effortless (automating).

Defining Your Savings Goals

Before you can save effectively, you need to know why you're saving. A vague goal like "save more money" is easy to ignore when you're tempted by a spontaneous purchase. To stay motivated, you need specific, personal goals.

So, what does financial well-being look for you? It could be:

A rock-solid emergency fund that covers three to six months of living expenses, so you're prepared for unexpected events.

Saving up for a down payment on a home, whether that's in Vancouver or Halifax.

Planning for a comfortable retirement so you can enjoy your later years without financial stress.

Finally getting ahead and paying off high-interest debt, like a credit card balance or student loan.

When you have a clear target, your motivation soars. It changes your mindset from "I can't spend" to "I'm investing in my future." You're not just cutting back; you're building something important.

Canadian saving habits can shift dramatically based on economic conditions. For instance, while the household saving rate in Canada has traditionally been around 7.5%, it soared to 26.5% in mid-2020 as spending options were limited. Since then, the rate has settled back down to around 5-6%, which highlights the need for an intentional saving strategy. You can explore more in this economic data report.

Small Habits Create Big Momentum

Forget trying to overhaul your entire financial life overnight. The most effective approach is to build small, consistent habits that add up over time. It’s like training for a marathon—you start with a short jog, not the full 42 kilometres.

True financial progress isn't about one massive leap. It's about hundreds of small, smart decisions made consistently over time. The key is to start, no matter how small.

Here are a few simple habits to get you started:

Do a weekly money check-in: Set aside 15 minutes every Sunday to review your bank and credit card transactions. See where your money went without judgment—the goal is awareness.

Set aside a small, fixed amount: Start with something that feels easy, like $25 per paycheque. You can always increase it later as you build confidence.

Use the 24-hour rule: For any non-essential purchase over a certain amount (say, $50), wait 24 hours before buying. You’ll be surprised how often the impulse fades.

These actions might seem minor, but they’re how you build the financial discipline needed for long-term success. To help you get going, here’s a simple action plan for your first month.

Your First 30 Days Savings Action Plan

| Week | Focus Area | Actionable Step | Potential Savings |

|---|---|---|---|

| Week 1 | Track Spending | Use an app or notebook to track every dollar you spend for seven days to see where your money truly goes. | Awareness (Priceless) |

| Week 2 | Cut One Thing | Identify one recurring expense to cut (e.g., a daily latte, a streaming service you don't use) and cancel it. | $20 - $100/month |

| Week 3 | Automate a Small Amount | Set up an automatic transfer of $25 from your chequing to your savings account the day after payday. | $50/month (if paid bi-weekly) |

| Week 4 | Meal Plan | Plan your meals for the week, create a grocery list, and stick to it. Avoid eating out for five days. | $50 - $150/week |

Following these simple steps can help you build the foundational habits for real financial change. After 30 days, you'll not only have saved money but also gained valuable insights into your spending patterns.

Track Your Financial Progress with NeoSpend

Let’s be honest: most budgets fail. They often feel restrictive and complicated, causing us to give up after just a few weeks. The secret to a successful budget isn't about restriction; it's about clarity. It's about creating a plan that fits your real life, not an idealized version of it.

Track your financial progress with NeoSpend, a crucial aspect of adhering to a savings plan is consistent tracking, which can alleviate the burden of relying solely on willpower. Neospend is crafted to assist you in monitoring your finances affectively. While it doesn't automate savings, it enables you to track your financial progress, giving you a clear view of how close you are to reaching your goals. With NeoSpend, you can effortlessly keep an eye on your savings, avoiding the need for spreadsheets. This approach supports a "pay yourself first" mindset, encouraging smart money management and helping you stay on track towards building wealth.

Create a Budget That Actually Works for You

Let’s be honest: most budgets fail. They often feel restrictive and complicated, causing us to give up after just a few weeks. The secret to a successful budget isn't about restriction; it's about clarity. It's about creating a plan that fits your real life, not an idealized version of it.

So, let's build one that sticks. We'll start by figuring out exactly what’s coming in and where it’s all going—from your daily Tim Hortons run to your monthly phone bill. Understanding these patterns is the first step toward taking control of your money.

Uncover Your True Spending Habits

Before you can direct your money where to go, you need to understand where it has been going. This isn’t about judging yourself for that late-night Uber Eats order; it’s simply about gathering data.

For one month, track every single dollar. It may sound like a chore, but it's one of the most eye-opening financial exercises you can do. Use a notebook, a spreadsheet, or an app to log everything you spend.

The goal is to see where your cash disappears. You’ll likely be surprised at how small, frequent purchases add up. A few dollars on coffee here and a forgotten streaming subscription there can quickly become a significant portion of your monthly income.

The 50/30/20 Rule: A Canadian Starting Point

A great framework to start with is the 50/30/20 rule. It’s simple and provides clear guidelines without overwhelming you with too many categories. Here’s how it works with your after-tax income:

Here’s the breakdown:

50% for Needs: This covers your essential expenses, such as mortgage or rent, groceries from Sobeys, utilities, car payments, and minimum debt payments.

30% for Wants: This is for everything that makes life enjoyable, like dining out, concert tickets, travel, your Spotify subscription, and hobbies.

20% for Savings & Debt Repayment: This portion is for building your future. It includes contributions to your emergency fund, TFSA, RRSP, and any extra payments to get out of debt faster.

The 50/30/20 rule is a guide, not a strict law. If you’re living in Toronto or Vancouver, your housing costs might take up more than 50% of your income. That's okay. You'll just need to adjust the other categories. The goal is to be intentional with your money, whatever the percentages are.

Your Secret Weapon: Automated Tracking with NeoSpend

Manually tracking every purchase can get tedious. This is where technology can be your best friend in your quest to save money in Canada. An app like NeoSpend automates this entire process for you.

By securely connecting your bank accounts and credit cards, NeoSpend does the heavy lifting, automatically categorizing your transactions. It can show you that you spent $120 on groceries last week or that your subscriptions totalled $45 last month. This provides a real-time, accurate picture of your finances without spreadsheets. The app’s spending insights highlight trends you might have missed, making it easy to spot where you can cut back and make smarter choices.

It's also important to recognize that saving ability varies across Canada. During the pandemic, the national household saving rate hit a record 26.5%, but this figure masks significant disparities. Higher-income households saw their savings grow, while many lower-income families struggled to cover essentials, as shown in these Canadian saving rate disparities on Statista. This is a powerful reminder of why a personalized budget that reflects your situation is so critical.

Build Your Budget and Put It to the Test

Now it’s time to put it all together. With your tracked spending data, you can draft your first budget.

Know Your After-Tax Income: Determine the actual dollar amount you have to work with each month.

Sort Your Spending: Go through your tracked expenses and label each one as a "Need," "Want," or "Saving."

Check Against the 50/30/20 Guideline: How do your numbers compare? Are you spending 70% on needs and only managing to save 5%? This is just data, not a judgment.

Look for Leaks: If your ratios are off, find areas to adjust. The "Wants" category is often the easiest place to start. Can you reduce restaurant meals or cancel a streaming service you rarely use?

Remember, your budget is a living document. Review it monthly to see how you did. Life changes, and your budget should be flexible enough to adapt. The goal is progress, not perfection.

Find Big Savings on Your Biggest Expenses

Once your budget is in place, it's time to find significant savings. While clipping coupons is helpful, the biggest wins come from tackling the "big three" expenses for most Canadians: housing, transportation, and food.

Making even small cuts in these areas can free up hundreds of dollars each month. This isn’t about sacrificing your quality of life; it’s about spending more strategically where it counts the most. Let’s explore some practical ways to do that.

Slash Your Grocery Bill Without Sacrificing Quality

Food costs have become a major source of stress for many Canadians. The good news is that with a bit of planning, you can significantly reduce your grocery bill. The most effective strategies happen before you even enter the store.

A great place to start is with flyer apps and price matching. Apps like Flipp are a game-changer, allowing you to browse weekly flyers from Loblaws, No Frills, and Food Basics in one place. If you see chicken on sale at one store, most competitors will match the price if you show them the ad.

Other simple yet powerful tactics include:

Shop with a list. Period. Impulse buys are a budget killer. A clear plan keeps you focused and helps you avoid tempting end-of-aisle displays.

Never shop hungry. When you're hungry, everything looks delicious, which often leads to a cart full of unnecessary items and a much higher bill.

Embrace store brands. For staples like flour, sugar, and canned goods, store brands like President's Choice or No Name are often just as good as brand-name versions but at a lower cost.

Rethink Your Transportation Costs

For many Canadians, a car is essential. However, it's also a major expense. When you add up car payments, insurance, gas, and maintenance, the total can be staggering. It’s worth taking a close look at where you can cut costs.

If you live in a city like Toronto or Montreal with a good public transit system, try leaving the car at home more often. A monthly transit pass is almost always cheaper than the daily costs of driving and parking.

The real cost of owning a car goes way beyond the monthly payment. Once you factor in insurance, gas prices that swing wildly, seasonal tire changes, and those pop-up repair bills, the annual expense can be staggering. Tracking every one of these costs in an app like NeoSpend can be a real eye-opener, showing you exactly how much you're spending and helping you decide if downsizing, carpooling, or taking the bus more often makes better financial sense.

Even if you need your car daily, you can still save. Use an app like GasBuddy to find the cheapest fuel nearby, and keep your tires properly inflated to improve mileage. It also pays to shop around for car insurance annually—rates can vary significantly between providers for the same coverage.

Find Savings in Your Housing Expenses

Housing is likely your single largest monthly expense, but that doesn't mean it’s completely fixed. Whether you rent or own, there are opportunities to save.

If you're a renter, don't be afraid to negotiate your lease renewal, especially if you've been a reliable tenant. Research what comparable units in your neighbourhood are renting for to strengthen your position.

For homeowners, refinancing your mortgage when interest rates are low can significantly reduce your monthly payments. It’s also a good idea to conduct an annual review of your utility bills. Small changes can lead to big savings over time:

Adjust your thermostat. Turning it down a few degrees in the winter and up in the summer can make a noticeable difference in your heating and cooling costs.

Unplug your electronics. Many devices draw "phantom power" even when turned off. Using power bars that you can switch off makes it easy to cut this waste.

Hunt down drafts. A little weather-stripping around leaky windows and doors can make your home more comfortable and lower your heating bill.

By focusing on these three major spending categories, you can unlock significant savings and accelerate your progress toward your financial goals.

Make Your Banking Work for You, Not Against You

Think of your bank account as a tool. It should help you build wealth, not slowly drain your money through hidden fees. Many Canadians don't realize how much they lose to monthly account fees, e-transfer charges, and out-of-network ATM withdrawals—often adding up to hundreds of dollars a year.

It's time to stop paying to access your own money.

Making your bank work for you begins with an honest look at what you’re paying for. Is there a monthly "maintenance" fee on your statement? Do you get charged for sending a friend money for lunch? These small costs are pure profit for the bank and a direct hit to your savings. Fortunately, modern banking options can help you plug these leaks for good.

Embrace No-Fee Chequing and High-Interest Savings

The rise of online-only banks in Canada has been a game-changer. Without the overhead of physical branches, these digital banks pass the savings on to you. This means no monthly account fees, unlimited free e-transfers, and often no minimum balance requirements.

At the same time, your savings should be earning you money. A High-Interest Savings Account (HISA) is essential. While traditional banks might offer a mere 0.01%, many online banks offer significantly higher rates. This is how you make your money work harder for you, even while you sleep.

Spotting and Eliminating Sneaky Bank Fees

Hidden bank fees are everywhere. The Big Five banks are convenient, but they often come with a complex menu of fees. A quick "financial health check" of your accounts can be very revealing.

Review your last few bank statements and look for these common culprits:

Monthly Maintenance Fees: Often $4 to $30 per month just for having an account.

Transaction Limits: Charges for exceeding a certain number of debits per month.

E-transfer Fees: Some accounts still charge $1.50 per transfer.

Non-Sufficient Funds (NSF) Fees: A harsh penalty, often $45 or more, if a payment bounces.

ATM Withdrawal Fees: Using an ATM outside your bank's network can cost $3 to $5 each time.

Think of your bank account like any other subscription. If you're paying a monthly fee but not getting real value, it's time to cancel. That money belongs in your savings, not helping the bank's bottom line.

A quick comparison shows how much you could save by switching to a fee-free model.

Typical Bank Fees vs Fee-Free Alternatives

| Fee Type | Typical Cost at Major Banks | Cost with No-Fee Alternatives | Annual Savings Potential |

|---|---|---|---|

| Monthly Chequing Fee | $4 - $30/month | $0 | $48 - $360 |

| E-transfer Fee | $1.50 per transfer | $0 (Unlimited) | $18+ (per dozen) |

| ATM Withdrawal Fee | $3 - $5 per withdrawal | $0 (within network) | $36+ (per dozen) |

| Exceeding Transactions | $1.25+ per transaction | No limit | Varies |

Even just eliminating the monthly chequing fee can put hundreds of dollars back in your pocket annually. The benefits of going fee-free are impossible to ignore.

Get a Clear View with NeoSpend

Combing through bank statements is tedious. This is where a platform like NeoSpend can be a huge help. By securely linking your chequing, savings, and credit accounts, you get a single, unified view of your entire financial life.

NeoSpend's smart categorization automatically flags recurring bank fees, so they can no longer hide. You can see at a glance what you're paying each month and pinpoint which accounts are costing you money. This clarity empowers you to take action—whether that means switching to a no-fee plan at your current bank or moving your money to a digital bank that better serves your needs.

Turn Your Savings Into Long-Term Wealth

Getting a handle on your savings is a huge accomplishment, but it's just the beginning. The real magic happens when you make that money work for you. Letting your cash sit in a regular savings account means it's slowly losing purchasing power to inflation.

This is where you shift from simply saving to building wealth. In Canada, we have incredible tools to help you do just that. It's more straightforward than you might think. We're not here to give stock tips, but to explain the accounts that can supercharge your growth. Understanding how they work is the first step to harnessing the power of compound growth—where your money starts earning its own money.

Understanding Your Key Options: TFSA vs. RRSP

When Canadians talk about investing, two acronyms dominate the conversation: the TFSA (Tax-Free Savings Account) and the RRSP (Registered Retirement Savings Plan). Both are designed to help your investments grow faster by sheltering them from taxes, but they work in different ways and are suited for different goals.

Think of them as different tools for different jobs.

| Feature | Tax-Free Savings Account (TFSA) | Registered Retirement Savings Plan (RRSP) |

|---|---|---|

| Main Tax Benefit | Contributions aren't tax-deductible, but all growth and withdrawals are 100% tax-free. | Contributions are tax-deductible, lowering your taxable income today. Withdrawals are taxed as income in retirement. |

| Best For | Flexible goals like a down payment, a new car, or a vacation. It's also a great tool for lower-income earners. | Long-term retirement savings. It's especially powerful for those in their peak earning years who want a significant tax refund now. |

| Withdrawals | You can pull money out anytime, tax-free. You also regain the contribution room the following year. | Withdrawals are taxed, and you permanently lose the contribution room (with a few exceptions for home buying and education). |

Understanding these differences is key to choosing the right strategy for your life.

Which Account Is Right for Your Goals?

Let's use a couple of everyday Canadian scenarios to make this clear.

Meet Maya, a 28-year-old graphic designer in Halifax saving for a down payment on her first condo. For her, the TFSA is a clear winner. She can contribute her after-tax money, watch it grow completely tax-free, and when she’s ready to buy, withdraw every penny without paying taxes on the gains. The flexibility is perfect for her medium-term goal.

Now, consider David, a 45-year-old engineer in Calgary in his highest-earning years. His focus is on reducing his current tax bill and building a nest egg for retirement. The RRSP is his powerhouse. Every dollar he contributes reduces his taxable income, potentially leading to a large tax refund. That money then grows tax-deferred until he retires, when he will likely be in a lower tax bracket.

Your financial goals and current income are the biggest clues for deciding between a TFSA and an RRSP. But remember, it's rarely an "either/or" situation. Most savvy Canadians use both to create a well-rounded financial plan.

This kind of long-term thinking is a core part of our financial culture. Canada's gross savings rate has consistently hovered around 25% of GDP for decades, showing a strong commitment to putting money away for the future. You can explore the data in this report on Canada's saving rates, which highlights how our collective savings strengthen the economy.

Common Questions About Saving Money in Canada

Navigating your finances can bring up a lot of questions. Whether you're just starting or looking to optimize your savings plan, getting clear answers is the first step toward feeling in control. Let's tackle some of the most common questions from Canadians trying to build their wealth.

How Much Money Should I Actually Be Saving Each Month?

This is a personal question, and the answer is different for everyone. A common guideline is the 50/30/20 rule, which suggests aiming to put 20% of your take-home pay toward savings and extra debt payments. For example, if you bring home $3,000 a month, your target would be $600.

However, if you live in a high-cost-of-living city or are paying off significant debt, hitting 20% right away might feel out of reach. The most important thing is to just start. Pick a number that feels manageable, even if it's only $50 a month. Building the habit is more important than the initial amount.

Is It Better to Pay Off Debt or Save Money?

This is a classic financial dilemma, and the best answer usually depends on interest rates.

High-Interest Debt: If you have credit card debt at 19.99% or higher, make paying it off your top priority. No investment can reliably guarantee a 19.99% return, so every dollar you put toward that debt is a guaranteed win.

Low-Interest Debt: For loans with lower interest rates (e.g., a student loan or car loan under 6%), you have more flexibility. You could make the minimum payments while also contributing to a high-interest savings account or your TFSA, where your money could potentially earn more than the debt is costing you.

A helpful tip is to build a small emergency fund first—even just $1,000—before aggressively tackling debt. This cushion can prevent you from using a credit card for unexpected expenses.

What Is the Fastest Way to Build an Emergency Fund?

Starting an emergency fund from scratch can feel daunting, but a focused approach can help you build it quickly. The goal is to save three to six months of essential living expenses.

Think of your emergency fund as financial insurance, not an investment. It’s the cash that keeps a flat tire or a leaky roof from completely derailing your long-term goals.

Here’s how to accelerate the process:

Automate It: Set up an automatic transfer to a separate high-interest savings account for the day after you get paid. This "pay yourself first" strategy ensures the money is saved before you can spend it.

Capture Windfalls: Any extra cash you receive—a tax refund, a work bonus, a birthday gift—should go straight into this fund.

Add a Side Hustle: Even a few hours a week of side work can make a big difference. Driving for a ride-share service or doing freelance work can add a few hundred dollars to your fund each month.

How Can I Save Money With an Irregular Income?

For freelancers or gig workers, traditional savings advice doesn't always apply. The key is to create your own "paycheque" system to smooth out income fluctuations.

Each time you get paid, immediately divide the money into different accounts. A common approach is:

50% for business expenses and, crucially, to set aside for taxes.

30% into your personal chequing account. This is your "salary."

20% straight to savings (emergency fund, TFSA, RRSP, etc.).

This system creates predictability from an unpredictable income, ensuring you're consistently saving. Tools like NeoSpend can be especially helpful here, as they can identify patterns in your income and suggest realistic savings targets based on your actual earnings, removing the guesswork from financial planning.

The takeaway is clear: saving money in Canada is achievable with the right strategy and tools. By setting clear goals, building small habits, and automating your finances, you can take control of your money and build a secure future.

Ready to make saving effortless? NeoSpend provides the tools you need to see your full financial picture, track spending automatically, and hit your goals faster. Discover how NeoSpend can work for you.

Article created using Outrank