Getting a handle on your debt starts with one simple, powerful move: knowing exactly what you owe. It’s the essential first step before you can even think about a payoff plan. You need to pull together all your debt info, get it organized, and create a clear snapshot of your financial reality. Only then can you start building a real strategy to get out of the red.

Your Starting Point: Understanding Your Debt

Before you can build any momentum on your journey to becoming debt-free, you need a map. That map is a clear, detailed list of every single dollar you owe.

It’s easy to feel crushed by a vague sense of "being in debt," but turning that anxiety into a concrete list is the most empowering thing you can do right now. This isn't about judging yourself; it's about taking back control. The goal is to swap that feeling of ambiguity for cold, hard clarity. You need to know the specific details for each loan or credit account, not just the grand total. This information will drive every decision you make from here on out.

Gather Every Piece of Your Debt Puzzle

Start by grabbing the most recent statements for all your debts. Don't leave anything out, no matter how small it feels. For most Canadians, this list will look something like this:

- Credit Cards: Every single one. That includes your main card from a bank like RBC or TD, but also that store card from The Bay you forgot about.

- Lines of Credit: Any personal or home equity lines of credit (HELOCs) you have open.

- Student Loans: Dig up the details for both government loans, like the Ontario Student Assistance Program (OSAP) or Canada Student Loans, and any private ones.

- Car Loans: Find the paperwork for your vehicle financing.

- Personal Loans: Add any installment loans from banks, credit unions, or other lenders.

- Mortgages: Even though it’s often considered "good debt," your mortgage is a huge piece of your financial picture. Include it.

Let's be real, juggling all these different accounts is a pain. This is where a tool like NeoSpend can be a lifesaver. Instead of logging into five different websites, you can link all your accounts in one spot. The app gives you a single, secure dashboard showing all your balances, which makes this whole process way simpler.

Organize Your Debts for Maximum Clarity

Once you have your statements, it’s time to create a master list. A simple spreadsheet works great, but even a notebook will do the trick. For each debt, you need to jot down four key things: the creditor, the total balance, the interest rate (APR), and the minimum monthly payment.

Seeing all these numbers lined up is often a huge wake-up-call. You might realize that a small store credit card has a jaw-dropping 29.99% interest rate, making it a top priority even if the balance isn't that high. This detailed view turns your debt from one big scary monster into a series of smaller, more manageable targets.

To help you get started, here's a table to organize your own debt snapshot.

Your Personal Debt Snapshot Example

Organize your debts to see the full picture at a glance. This example shows how to list each debt with its critical details, preparing you to choose a payoff strategy.

| Debt Name (Creditor) | Total Balance | Interest Rate (APR) | Minimum Payment |

|---|---|---|---|

| OSAP Loan | $18,000 | 6.5% | $210 |

| CIBC Visa Card | $4,500 | 19.99% | $90 |

| Honda Car Loan | $12,000 | 4.9% | $350 |

| The Bay Credit Card | $850 | 29.99% | $25 |

Laying it all out like this gives you a strategic blueprint. While debt levels vary from person to person, the need for this kind of clarity is universal. For instance, household debt in California is shockingly high, with the average household owing an estimated $259,000, mostly from mortgages in a tough housing market. It just goes to show how critical solid financial management is, no matter where you live. You can find more details about these household debt trends to see the bigger picture.

The most critical step in any debt-free journey is the first one: facing the numbers. By creating a comprehensive list of what you owe, you replace fear and uncertainty with a clear, actionable plan.

Choosing Your Debt Repayment Strategy

Alright, you’ve done the hard work of getting a clear, organized list of everything you owe. Now comes the fun part: deciding how you’re going to attack it. This isn't just about randomly throwing extra cash at your balances; it's about creating a focused battle plan. For most Canadians, it comes down to two powerhouse strategies: the Debt Avalanche and the Debt Snowball.

Each one works a little differently, tapping into different motivations. The right one for you really depends on your personality and what’s going to keep you in the fight for the long haul. Let’s dig into how they both work so you can figure out which path will get you to debt freedom the fastest.

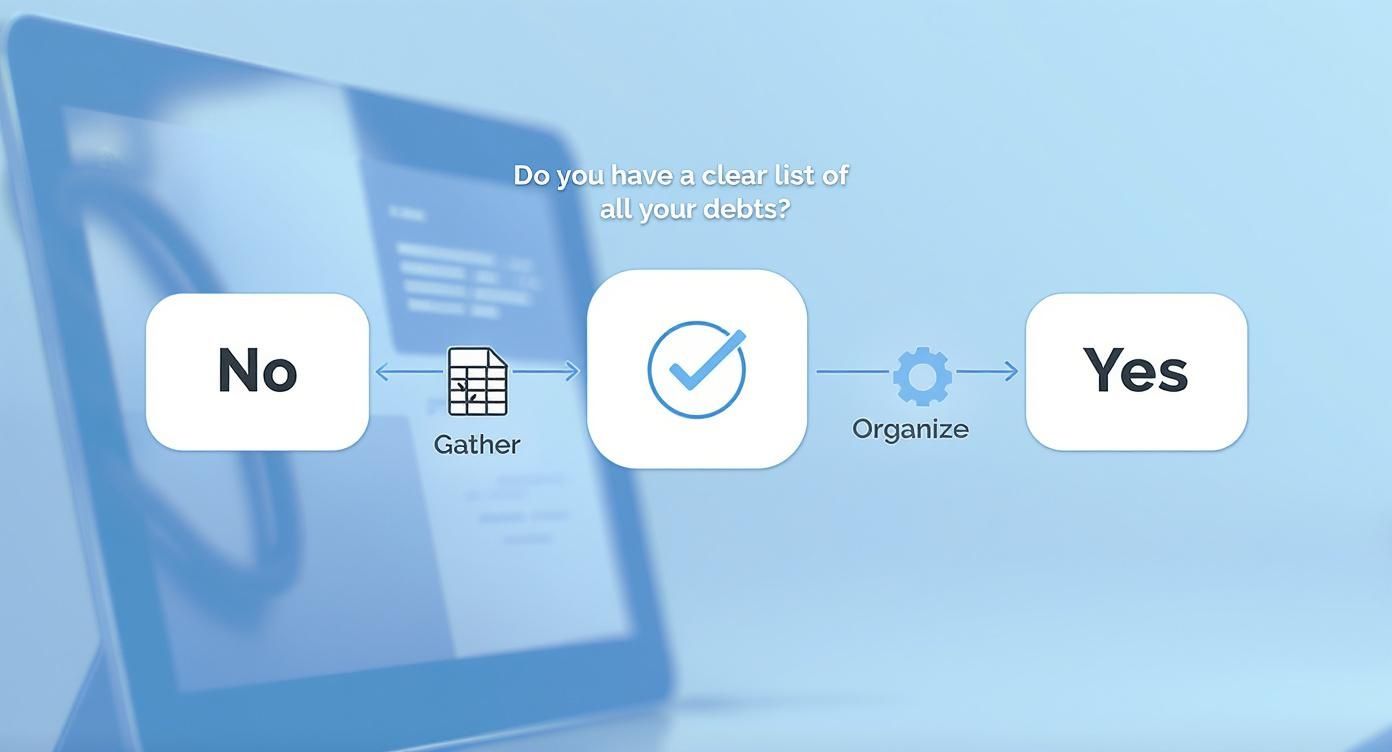

To get a sense of where you are in the journey, this little flowchart is pretty handy. It all starts with getting organized before you can pick your weapon of choice.

As you can see, once your debt info is all sorted, the next move is picking a strategy—which is exactly where we are right now.

The Debt Avalanche Method: Save the Most Money

If you’re a numbers person, the Debt Avalanche is your best friend. From a purely mathematical standpoint, it’s the most efficient way to pay off debt. The whole idea is to focus on the debt with the highest interest rate (APR) first, no matter how big or small the balance is.

Here’s the game plan:

- Keep making the minimum payments on all your debts. Don't miss any.

- Throw every extra dollar you can find towards the debt with the highest APR.

- Once that beast is slain, you "avalanche" all the money you were paying on it (the minimum payment plus all that extra cash) onto the debt with the next-highest interest rate.

- You just keep repeating this process until everything is gone.

This approach saves you the most money in interest over time because you're wiping out your most expensive debts first. The only catch? If your highest-interest debt is also a massive one, it might take a while to feel like you're making progress, which can be a bit of a grind. This method is perfect if you're motivated by the long-term financial win.

The Debt Snowball Method: Build Momentum Fast

The Debt Snowball is all about psychology and quick wins. Instead of getting hung up on interest rates, you tackle your debts from the smallest balance to the largest, ignoring the APR.

The steps feel pretty similar, but the focus is different:

- Again, keep up with all your minimum payments.

- Channel all your extra money toward the debt with the tiniest balance.

- Once that little debt is gone—bam!—you get a quick, powerful win. It feels amazing.

- You then roll everything you were paying on it into the next-smallest debt. Your "snowball" of payments gets bigger and bigger as you knock out each debt, creating momentum that keeps you fired up.

Sure, you might pay a little more in interest compared to the avalanche method, but the psychological boost from clearing debts off your list is incredibly powerful. For a lot of people, those early victories are exactly what they need to see the whole plan through to the end. This is the strategy for you if seeing fast progress is what keeps you in the game.

Debt Avalanche vs. Debt Snowball: Which Is Right for You?

So, which team are you on? Both methods work, but they appeal to different mindsets. This table breaks down the core differences to help you decide.

| Feature | Debt Avalanche | Debt Snowball |

|---|---|---|

| Primary Focus | Highest interest rate (APR) | Smallest balance |

| Best For | People motivated by math and saving the most money in the long run. | People who need quick wins and visible progress to stay motivated. |

| Main Advantage | Saves the most money on interest over the life of your loans. | Provides powerful psychological boosts by clearing debts quickly. |

| Potential Downside | Can feel slow if your highest-interest debt has a large balance. | You'll likely pay more in total interest compared to the avalanche method. |

| The Vibe | The logical, financially optimal path. | The momentum-building, emotionally rewarding path. |

Ultimately, choosing a repayment strategy is less about which one is technically "better" and more about which one you’ll actually stick with. Consistency is everything.

It also helps to see how your personal plan fits into the bigger picture. For instance, recent reports show the average Canadian's non-mortgage debt is climbing, heavily influenced by rising interest rates. When the Bank of Canada makes changes, it directly impacts how much your debt costs you, which just highlights why having a solid repayment plan is so crucial. You can read more about these consumer debt trends from Experian to understand how these economic shifts play out.

Whether you go with the math-driven avalanche or the motivation-focused snowball, the most important step is to commit. In the next section, we’ll dive into how to build a budget that frees up the extra cash you need to make either of these strategies a reality.

Building a Budget to Free Up Cash

A debt repayment plan is a great start, but it needs fuel to really get going. To make a serious dent in what you owe, you have to find extra money to throw at it. This is where a budget becomes your secret weapon.

Forget the idea that budgeting is about restriction—it's about taking back control. It gives you a crystal-clear picture of where your money is actually going, so you can point it toward what really matters: getting out of debt for good.

First things first, you need to track your spending. For one full month, log every single transaction. I'm talking about everything, from your morning Tim Hortons coffee to your monthly hydro bill. This is often a massive eye-opener and can expose spending habits you didn’t even realize you had.

Understanding Your Canadian Spending Habits

A generic budget template you find online just won't cut it. To get a realistic view of your finances, you need to think like a Canadian and account for our unique expenses.

When you start categorizing, make sure your budget includes things like:

- Housing: Your mortgage or rent, plus property taxes and tenant/home insurance.

- Utilities: Get specific here. Think hydro, natural gas (which can skyrocket in the winter), water, and internet.

- Transportation: Car payments, insurance, gas, maintenance, and maybe a Presto or Compass card.

- Groceries: Are you a Loblaws regular, a No Frills fan, or do you hit up the local farmers' market? It all adds up differently.

- Financial Goals: Don't forget your RRSP or TFSA contributions. These are non-negotiable.

- Subscriptions & Memberships: All those streaming services, gym memberships, and other little recurring charges.

This is where a tool like NeoSpend can be a game-changer. Instead of digging through endless bank statements, the app automatically pulls in and categorizes every transaction from your linked Canadian accounts. Its AI can even sniff out those sneaky subscriptions you forgot you were paying for, giving you an instant list of potential savings.

Finding Extra Cash Without Major Sacrifices

Once you see the full picture, you can start making strategic cuts. This isn't about living on instant noodles. It’s about trimming the fat and putting that money to work on your debt. You'd be surprised how much small, painless changes can add up.

Don't underestimate the power of small, consistent changes. Finding an extra $100-200 a month to put toward your debt can shave years off your repayment timeline and save you thousands in interest.

Look for the easy wins. Could you switch to a more affordable grocery store for some items? Or maybe get serious about meal planning to cut down on food waste and pricey takeout? Sometimes it’s as simple as calling your cell phone provider to see if you can get a better deal on your data plan.

Taking Action to Lower Your Monthly Bills

Cutting back isn't your only move. You can also play offence by negotiating a better deal on the bills you’re already paying. A lot of Canadians just accept the price they're given, but many of your biggest monthly expenses are more flexible than you think.

Here are a few things you can do right now:

- Negotiate Your Bills: Pick up the phone and call your internet, mobile, and cable providers (like Bell, Rogers, or Telus). Tell them you’re re-evaluating your budget and exploring other options. You’d be amazed how often a "loyalty discount" or a cheaper plan suddenly becomes available.

- Shop Around for Insurance: Never, ever automatically renew your car or home insurance. Get fresh quotes every single year. Rates change constantly, and a few quick phone calls could easily save you hundreds.

- Review Your Subscriptions: Use NeoSpend to see a clean list of every recurring payment. Get ruthless. Are you really using all of them? Cancelling just two services you don't use could free up $30-$50 per month.

By building a real-world budget and hunting down savings, you're not just cutting back—you're generating new cash flow to destroy your debt. This turns your budget from a boring tracking sheet into a powerful engine driving you toward financial freedom.

Accelerating Your Progress with Smart Moves

Just making minimum payments is a slow-motion trap. It’s a guaranteed way to stay in debt for years, sometimes even decades, while interest charges eat away at your progress. If you want to get out of debt fast, you have to go on the offensive.

This means finding ways to throw more money at your balances each month. You can attack this from two angles: bringing more money in or cutting down your interest costs. Both are powerful on their own, but when you combine them, you can seriously supercharge your journey out of debt.

Let's dig into some of the most effective strategies for Canadians to get ahead.

Boost Your Income with a Canadian Side Hustle

Squeezing more out of your existing budget is a solid first step, but sometimes the fastest way forward is simply to earn more. A side hustle gives you a dedicated stream of cash that you can aim directly at your highest-priority debt, letting you make a real dent without having to sacrifice your day-to-day spending money.

The good news is that the Canadian gig economy is full of flexible options that can fit around a 9-to-5. You don’t have to build a whole second career—you just need to find something that works for you.

Here are a few ideas to get the wheels turning:

- Go Freelance: Got skills in writing, graphic design, social media, or web development? Platforms like Upwork and Fiverr can link you up with clients from all over the world.

- Join the Gig Economy: Services like SkipTheDishes, Uber Eats, and Instacart let you earn on your own time delivering food or groceries. Total flexibility.

- Share Your Knowledge: Are you a math whiz or fluent in French? Online tutoring is a fantastic way to help students while building your debt-crushing fund.

- Sell Your Stuff: We all have things lying around we don't use anymore. Tossing them up on Kijiji or Facebook Marketplace can turn that clutter into cash surprisingly fast.

The key is to dedicate 100% of that side hustle income directly to your debt. This isn't "fun money"—it's a targeted tool to fast-track your journey to financial freedom.

Lower Your Interest Costs with Strategic Moves

Earning more is great, but cutting down the interest you’re paying can be just as game-changing. High interest rates are the real enemy here, since they ensure a huge chunk of your payment goes straight to the lender instead of chipping away at your actual balance.

One of the simplest and most overlooked moves is to just ask for a better rate. A lot of Canadians think their credit card interest rate is non-negotiable, but that’s not always true—especially if you have a good history of paying on time.

A quick phone call could save you a ton. Here’s a simple script you can use:

- You: "Hi, my name is [Your Name] and I've been a loyal customer for [Number] years. I'm focused on paying down my balance faster and was hoping you could help me with a lower interest rate on my account."

- Be Ready for a Follow-Up: If they ask why, you can say, "I've received some more competitive offers, but I’d really prefer to stay with you if we can find a rate that works better for me."

Even a small drop from 19.99% to 16.99% can save you hundreds, if not thousands, over the life of the debt. The worst they can do is say no, so it’s always worth a shot.

Consider Debt Consolidation or a Balance Transfer

If you're juggling multiple high-interest debts, like a few different credit cards, rolling them all into a single, lower-interest loan can make your life a whole lot easier and save you a bundle. The two most common options in Canada are debt consolidation loans and balance transfer credit cards.

A debt consolidation loan is a personal loan you take out to pay off all your other debts at once. You’re left with just one predictable monthly payment, usually at a much friendlier interest rate than your credit cards. It’s a great option if you can qualify for a good rate and want a clear finish line.

A balance transfer credit card lets you move your expensive balances onto a new card with a promotional 0% or low-interest rate for a set period, like 6 to 12 months. This is an amazing strategy if you’re confident you can crush the balance before that intro period ends. Just be careful—if you don't, the rate can shoot right back up.

Making this call requires having a crystal-clear picture of your finances. This is where a tool like NeoSpend really helps, by pulling all your debt information into one place. Its dashboard gives you a bird's-eye view of all your balances and interest rates, giving you the hard data you need to decide if consolidation is the right move for you.

Tracking Progress and Staying Motivated

Getting started on a debt repayment plan is a big deal, but let’s be real—the real challenge is sticking with it. The road to becoming debt-free is a marathon, not a sprint. Keeping that momentum going, especially when life throws you a curveball or the progress feels painstakingly slow, is what will get you across the finish line.

This is exactly where tracking your progress becomes your secret weapon. It turns all your hard work from abstract numbers on a screen into concrete proof that what you're doing is actually working. Watching those balances get smaller is the dose of positive reinforcement you need to keep pushing forward.

![]()

Visualizing Your Wins

You need a simple, consistent way to see your progress. The method itself doesn't have to be fancy; it just has to be something you'll actually use. The whole point is to create a visual reminder of how far you’ve come.

Here are a few classic methods lots of Canadians swear by:

- A Simple Spreadsheet: Fire up Excel or Google Sheets. Make a basic chart with each debt, its starting balance, and its current balance. Update it every month after you make your payments and get that satisfaction of seeing the numbers drop.

- Debt Thermometers: This one’s a classic for a reason. Draw a big thermometer for each debt (or just one for your grand total) and colour it in as you chip away at the balance. It’s surprisingly fun and a great visual way to celebrate every dollar you pay off.

- A Whiteboard: Stick a whiteboard somewhere you can’t miss it, like in your kitchen or home office. List your debts and update the numbers monthly. It keeps your goal right in front of you, every single day.

These manual methods are great, but they do require a bit of discipline. If you want something more hands-off, a financial app can do the heavy lifting. This is where a tool like NeoSpend can make a huge difference. You link up your Canadian bank accounts, credit cards, and loans, and the app gives you a live dashboard of your finances. You can see all your debt balances updating in real time, with motivating charts that show your progress without you having to enter a single thing.

Celebrate Your Small Victories

To stay in this for the long haul, you absolutely have to celebrate your milestones. Paying off debt is just a series of small wins that eventually add up to a life-changing accomplishment. Taking a moment to recognize those wins is how you avoid burnout.

Set small, reachable goals and give yourself a little reward when you hit them. The trick is to pick rewards that won't blow your budget or, worse, add more debt.

For instance, you could plan a small celebration for:

- Paying off your very first (or smallest) debt.

- Hitting a certain milestone, like paying off 10% or 25% of your total debt.

- Making six extra payments in a row without missing a beat.

Your rewards don't need to be expensive. Think about cooking a nice dinner at home, taking a day trip to a nearby park, or just giving yourself an evening to binge-watch a show without feeling guilty. The idea is to acknowledge your hard work and recharge your batteries.

Staying Focused When You Feel Like Quitting

Look, there will be months where an unexpected bill pops up or you feel like you’re barely making a dent. It happens to everyone. The important thing is not to let one tough month derail your entire plan.

In those moments, go back to your "why." Remind yourself why you even started this journey. Was it to finally get rid of that financial stress? Save for a down payment? Achieve the freedom to travel? Reconnecting with that original motivation is often the push you need to keep going.

Managing personal debt is a universal struggle. Even governments grapple with paying down what they owe. Take California, for example—it holds the largest state government debt in the United States, a mind-boggling $497 billion. This shows the kind of discipline it takes at every level to get finances under control. You can even explore more details about this government financial data to see how these principles apply on a massive scale.

Whether you're tackling a credit card balance or a budget the size of a country's, the rules of the game are the same: track your progress, celebrate the wins, and never lose sight of the end goal.

Got Questions About Paying Off Debt? We’ve Got Answers.

Jumping into a debt repayment plan is a huge move, and it’s completely normal to have questions pop up along the way. Getting solid answers you can trust is key to staying motivated and on track.

Let’s tackle some of the most common questions we hear from Canadians who are getting serious about ditching their debt for good.

How Will Paying Off Debt Affect My Credit Score?

This is a big one, and the answer isn't always what people expect. As you start knocking down your balances, you’ll see a positive change in your credit score over time. Why? A huge piece of your score is your credit utilization ratio—that’s just the amount of credit you're using versus how much you have available. Lower balances mean a lower ratio, and lenders absolutely love to see that.

But, you might see a temporary dip. For example, if you pay off a credit card you’ve had for ages and immediately close the account, it can shorten the length of your credit history. The best move is often to keep old, no-fee accounts open, even with a zero balance. It helps preserve that long, positive history you’ve built.

Should I Throw My Tax Refund at My Debt?

When that tax refund from the CRA lands in your bank account, it can feel like you've won the lottery. It's so tempting to splurge, but using it to make a big payment on your highest-interest debt is one of the smartest things you can do for your financial future.

Just think about it: dropping $1,500 on a credit card with a 19.99% interest rate could save you hundreds in future interest charges and cut months off your repayment plan. It's a massive shortcut on your path to becoming debt-free.

Pro Tip: Always target high-interest debt when you get a lump sum of cash. It’s your chance to make a real dent in the principal and stop interest from piling up.

When Is It Time to Call in a Professional?

If you're feeling totally underwater—maybe you're missing payments or getting calls from collection agencies—it might be time to get some professional guidance. In Canada, a non-profit credit counselling agency is a fantastic place to start.

These organizations aren't here to judge. They're here to help you:

- Roll all your payments into one manageable monthly plan.

- Talk to your creditors about lowering your interest rates.

- Give you the tools and education you need to manage your budget.

There's no shame in asking for help. A credit counsellor can map out a clear path forward when you feel stuck, giving you a sustainable plan to pay off your debt for good.

The journey to paying off debt quickly is all about clarity, commitment, and consistency. Start by understanding exactly what you owe, choose a repayment strategy that fits your personality, and build a budget that frees up cash to accelerate your progress. Remember, every extra payment brings you one step closer to financial freedom.

Ready to see your entire financial picture in one place? NeoSpend gives you the tools to track your progress, spot savings, and finally crush your debt. See how our AI-powered insights can help you build a smarter budget and hit your goals faster. Discover NeoSpend today.

Article created using Outrank