If you want to improve your credit score in Canada, it really boils down to two things: paying every bill on time and keeping your credit card balances low. Seriously, that’s it. These two habits carry the most weight and show lenders you can be trusted with their money. Get these right, and you’re already on your way to unlocking better financial opportunities.

Getting to Know Your Canadian Credit Score

Before you can start improving your score, you have to know what you’re working with. Think of your credit score as your financial report card, boiled down to a simple three-digit number. In Canada, that number usually falls somewhere between 300 and 900.

Lenders use this score as a quick snapshot of how risky it would be to lend you money. A high score tells them you’re a safe bet, which often leads to better interest rates on big-ticket items like mortgages and car loans. A lower score? That can make it tougher to get approved at all, or you might get stuck with sky-high interest rates.

The Two Major Players in Canadian Credit

Here in Canada, there are two main credit bureaus calling the shots: Equifax and TransUnion. They’re the ones collecting all the financial data from lenders to create your credit reports and scores.

While their scoring models can differ slightly, they’re both looking at the same fundamental information. It’s always a good idea to check your reports with both bureaus since you never know which one a potential lender will pull from.

Your score isn't set in stone—it's always changing based on your financial moves. The great news is this puts the power directly in your hands. Consistent, smart habits will absolutely move the needle in the right direction.

What Actually Makes Up Your Credit Score

Your score is a mix of five key ingredients, each with a different level of importance. Understanding what they are is the first step to figuring out how to make real improvements.

Let's break down the factors that influence your credit score and what they mean for you as a borrower in Canada.

What Makes Up Your Credit Score in Canada

| Factor | Importance (Approx. %) | What It Means for You |

|---|---|---|

| Payment History | 35% | This is the big one. It's a record of whether you've paid your bills on time. A single late payment can hurt your score. |

| Credit Utilization | 30% | This is the percentage of your available credit you're using. Lenders get nervous if you're maxing out your cards. |

| Length of Credit History | 15% | A longer, well-managed credit history is a positive sign. It shows you have experience handling credit responsibly. |

| Credit Mix | 10% | Lenders like to see that you can manage different types of credit, like a credit card (revolving) and a car loan (instalment). |

| New Credit Inquiries | 10% | When you apply for new credit, it creates a "hard inquiry." Too many in a short time can suggest you're in financial trouble. |

Seeing all these pieces together shows that a healthy score is about more than just one action—it's the sum of your financial habits.

Your credit score is more than just a number—it’s a reflection of your financial habits. Building a strong score is a marathon, not a sprint, and it starts with understanding exactly where you stand today.

Trying to keep track of all these moving parts can feel overwhelming, especially if you have multiple accounts. This is where a tool like NeoSpend helps people manage money smarter. It pulls all your financial accounts—chequing, credit cards, loans—into a single, easy-to-read dashboard. You get a real-time view of your spending, balances, and due dates, which makes managing the very factors that build your score so much easier.

Did you know that paying your bills on time is the single most powerful way to boost your credit score in Canada? According to FICO, payment history accounts for a whopping 35% of your FICO Score. With recent data showing that nearly 1.4 million Canadians missed a credit payment in a single quarter, it’s clear how easy it is to slip up. These missed payments can hang around and damage your score for up to six years.

On the flip side, consistent on-time payments can turn things around. The average Canadian FICO Score was 760 in 2024, but with credit card balances on the rise, staying on top of payments is more critical than ever. You can explore more data on Canadian credit trends to see just how much this matters for your financial health.

Master Your Payment History for a Healthier Score

If there's one golden rule in the world of credit, it's this: your payment history is king. It's not just a small piece of the pie; it makes up a whopping 35% of your credit score. For lenders across Canada, this is the number one thing they look at to gauge how reliable you are. A clean record of on-time payments tells them you're a safe bet.

Just one slip-up—one late payment—can knock your score down, and that blemish can stick around on your Canadian credit report for as long as six years. The good news? This is the one area where you have complete control. It all boils down to making late payments a non-issue.

Automate Your Fixed Expenses

Let’s be honest, life gets busy. The easiest way to guard against a simple mistake is to set up automatic payments for your fixed bills. This is a game-changer for any expense that stays the same month after month.

Think about these predictable costs in your budget:

Car insurance premiums: This is usually a set amount, making it a perfect candidate for autopay.

Monthly phone bill: Most Canadian carriers make it easy to set up pre-authorized payments right from your bank account.

Internet and streaming services: Set it and forget it. You get uninterrupted service and another on-time payment on your record.

Instalment loan payments: Got a car loan or a personal loan? The payment is always the same, so automate it.

Taking these off your mental to-do list eliminates the chance of human error. No more "oops, I forgot" moments that could sabotage your score.

Taming Your Variable Bills

Okay, so what about the bills that are all over the place? I'm talking about your hydro bill or credit card statements that change every month. Automating the full balance might not be smart if you don't know the exact amount, but you can still build a system to stay on top of them.

Imagine you're a freelancer in Vancouver juggling client invoices, a fluctuating income, and a stack of personal bills. It's incredibly easy for a due date to get lost in the shuffle.

A strong credit score is built on consistency. The goal isn't just to avoid late payments, but to create a system that makes on-time payments the default, not the exception.

This is where a solid financial tool can be your best friend. Instead of bouncing between different banking apps and websites, a tool like NeoSpend brings all your bills and due dates into one clean dashboard. It sends you smart alerts before a payment is due, acting like a personal financial assistant. You get a heads-up, giving you plenty of time to review the bill and pay it manually—all without the risk of an automated payment overdrawing your account.

What to Do If You Miss a Payment

It happens to the best of us. If you realize you’ve missed a payment, don’t panic. The key is to act fast and be strategic to minimize the damage.

Here’s your action plan:

Pay Immediately: The second you notice it, go pay at least the minimum amount due. The faster you act, the better.

Contact Your Creditor: Pick up the phone and call them. If you’ve got a good track record of paying on time, they might be willing to waive the late fee as a courtesy. It never hurts to ask.

Ask About Reporting: While you have them on the line, politely ask if they can hold off on reporting the late payment to the credit bureaus (Equifax and TransUnion). Most lenders don't report a delinquency until it's 30 days past due. If you're only a few days late, you have a very good chance of keeping it off your report entirely.

A little bit of proactive communication goes a long way. Lenders would much rather work with a customer who owns up to a mistake than one who disappears. Explaining what happened and showing you're on top of it can make all the difference.

Tackle Your Credit Utilization for a Quick Boost

Once you’ve got your payment history sorted, the next big lever you can pull for a surprisingly fast credit score bump is your credit utilization ratio. It sounds technical, but it’s just the percentage of your available credit that you’re currently using. This little number is a huge deal, making up about 30% of your score.

Canadian lenders watch this metric like a hawk. Let’s say you have a credit card with a $10,000 limit and you’ve got a balance of $8,000 sitting on it. That’s a utilization of 80%. To a lender, that’s a red flag. It can look like you’re overextended and relying too much on credit to get by.

The golden rule? Try to keep your overall credit utilization below 30%. Staying under this threshold signals that you’re managing your finances responsibly and aren't about to max out your cards. Honestly, the lower you can get it, the better.

How Should You Tackle Your Balances?

Getting your balances down is priority one, but where do you even start? There are a couple of popular strategies that can give you a clear game plan. Let's walk through them with a realistic Canadian scenario.

Picture a recent grad living in Toronto, juggling a few different debts:

A major bank credit card: $2,500 balance at 19.99% interest.

A retail store card: $500 balance at a painful 29.99% interest.

A provincial student loan: $15,000 balance at 6.5% interest.

The Debt Avalanche Method

This approach is all about math. You focus on demolishing the debt with the highest interest rate first, no matter how big or small the balance is. In our example, you'd throw every spare dollar at that $500 store card because of its brutal 29.99% rate, while just making minimum payments on everything else. Once it's gone, the 19.99% bank card is next. This method saves you the most money in interest over the long haul.

The Debt Snowball Method

The snowball method is more about psychology. Here, you attack the smallest debt first to score a quick, motivating win. You’d still go after the $500 store card first, but because it’s the smallest balance, not because of the interest. Wiping that first debt off your list feels amazing and builds the momentum you need to keep going.

There’s no right or wrong answer here. The avalanche is the most efficient on paper, but the snowball's power to keep you motivated can't be underestimated.

What About Credit Limit Increases?

This might sound a little backward, but sometimes asking for a higher credit limit can actually help your utilization ratio. If that $10,000 limit gets bumped up to $15,000, your $8,000 balance instantly drops your utilization from a scary 80% to a much more respectable 53%.

But—and this is a big but—this strategy only works if you have the discipline not to use the extra credit. The entire point is to lower the ratio, not to dig a deeper hole. Also, be aware that asking for an increase can trigger a hard inquiry on your report, which might temporarily ding your score by a few points.

The fastest path to a better credit score often runs through your credit card balances. Lowering your utilization shows lenders you’re in control of your finances, not the other way around.

Trying to keep track of utilization across a few different cards can get messy. This is where an app like NeoSpend helps people manage money smarter. It links up with your Canadian bank and credit card accounts to give you a single, clear dashboard of all your balances and limits. You can see your utilization on each card at a glance, making it easy to decide which balance to pay down first for the biggest impact on your score. Seeing that progress in one place is a great way to stay motivated and make smarter moves for your financial health.

Build a Diverse and Long-Standing Credit History

When we talk about credit scores, everyone knows that paying bills on time and keeping balances low are the big ones. But there are two other pieces of the puzzle that often get overlooked: the age of your credit accounts and the variety of credit you're managing.

Together, these factors make up about 25% of your credit score. A long, stable, and diverse credit history tells lenders you have experience and can handle different kinds of financial responsibility. Think of it as a financial resume—one that shows years of consistent borrowing is way more impressive than a short or one-dimensional record. Lenders in Canada want to see that you're a reliable partner for the long haul.

Why You Should Keep Old Accounts Open

It’s so tempting. You finally pay off that old credit card you got back in university, and your first instinct is to close it and declutter your wallet. While it feels like a good spring cleaning move, closing that account could actually ding your score.

Here's why: when you close an old account, you erase its entire history. This shortens the average age of all your accounts, which can make you look like a less experienced borrower in the eyes of a lender.

Let’s look at a real-world example.

Picture a young family in Calgary, Liam and Chloe, who are saving up for their first house. Their credit profile includes a ten-year-old student loan, a three-year-old car loan, and two credit cards. One card is from their university days, and the other is a newer travel rewards card.

They've just paid off the old university card and are thinking about closing it. But keeping it open, even if they just use it for a tiny recurring bill like their streaming service, helps them in two huge ways:

It preserves that long history, which props up the average age of their credit.

It keeps that card's credit limit as part of their total available credit, which helps keep their overall utilization ratio nice and low.

Lenders see a long credit history as a sign of stability. Resisting the urge to close your oldest accounts is one of the easiest ways to protect your score as you build your financial future.

The Power of a Healthy Credit Mix

Lenders don't just want to see a long history; they also want to see that you can successfully juggle different types of credit. A healthy credit mix shows you're financially versatile. There are two main categories of credit that Canadian lenders are looking at.

Types of Credit:

Revolving Credit: This is your credit cards and lines of credit. You can borrow, repay, and borrow again up to a certain limit.

Instalment Loans: These are loans with fixed payments over a set time—think mortgages, car loans, or personal loans.

Having a combination of these, like a credit card and a car loan, shows you can handle both revolving debt and fixed-payment obligations. But hold on—this doesn't mean you should run out and get a loan just to beef up your mix. The best way to do this is to let it happen naturally as your life and financial needs change.

If you're just starting out, like a student or a newcomer to Canada, opening your very first credit account is a massive step. A secured credit card is often the perfect entry point. You provide a security deposit (which usually becomes your credit limit), making it a low-risk way for you to build a positive payment history from scratch. Once you've proven you're reliable, you can graduate to an unsecured card and add other credit types when it makes sense for you.

Keeping track of these long-term strategies means you need a bird's-eye view of your whole financial picture. This is where a tool like NeoSpend really comes in handy. By linking all your accounts, you can see the age of each one and monitor your credit mix all in one spot. It helps you make smarter decisions—like keeping that old account active—so you can build a strong, diverse credit profile that opens doors to your biggest goals.

Find and Fix Errors on Your Credit Report

Think of your credit report as the detailed story behind your score. The problem? Sometimes, that story gets the facts wrong. A study from the Public Interest Advocacy Centre (PIAC) found that errors on Canadian credit reports are alarmingly common.

We're not talking about small typos. These can be big, score-damaging mistakes, like a payment you made on time being marked as late, or even an account that isn't yours showing up.

Becoming your own financial detective and fixing these errors is one of the most powerful moves you can make to boost your credit score. It’s like proofreading your financial life story. When your report is clean and accurate, lenders see the real you—not a version messed up by a clerical error.

How to Get Your Free Canadian Credit Reports

In Canada, you have the right to get a free copy of your credit report from both of the major credit bureaus, Equifax and TransUnion, at least once a year. You can do it online, by mail, or over the phone.

It's a smart idea to get both. Why? Because some lenders only report to one bureau, which means an error could be lurking on one report but not the other.

Once you have the reports in hand, it's time to put on your detective hat. Go through them line by line, paying extra close attention to a few key areas:

Personal Info: Is your name, address, and SIN all correct? Simple mistakes here can cause big headaches.

Account History: Do you recognize every account listed? Double-check for any late payments you know for a fact you paid on time.

Credit Inquiries: Make sure every "hard inquiry" was actually from a time you applied for a loan or credit card.

The Process for Disputing Errors

Spotted something that looks off? Don't panic. There's a clear process to get it fixed. Both Equifax and TransUnion have official dispute resolution forms right on their websites. This is your starting point.

To make your case airtight, you need to back it up with evidence. Gather any documents you have that prove your claim, like:

Bank statements showing a payment cleared on time.

A letter from a creditor confirming an account is paid in full.

A police report if an account was opened fraudulently.

When you fill out the dispute form, be direct and clear. Instead of just saying, "This is wrong," be specific. For example: "The account from XYZ Telecom (Account #12345) is incorrectly showing a late payment for May 2024. I've attached my bank statement showing the payment was made on May 15th."

An error on your credit report isn't just a number—it's a roadblock to your financial goals. Actively monitoring and correcting your report is a powerful act of financial self-defence.

After you submit the dispute, the credit bureau is legally required to investigate. They'll typically contact the creditor who reported the information. This can take up to 30 days, so you’ll need a bit of patience. If they confirm the error, they'll correct your report and mail you an updated copy.

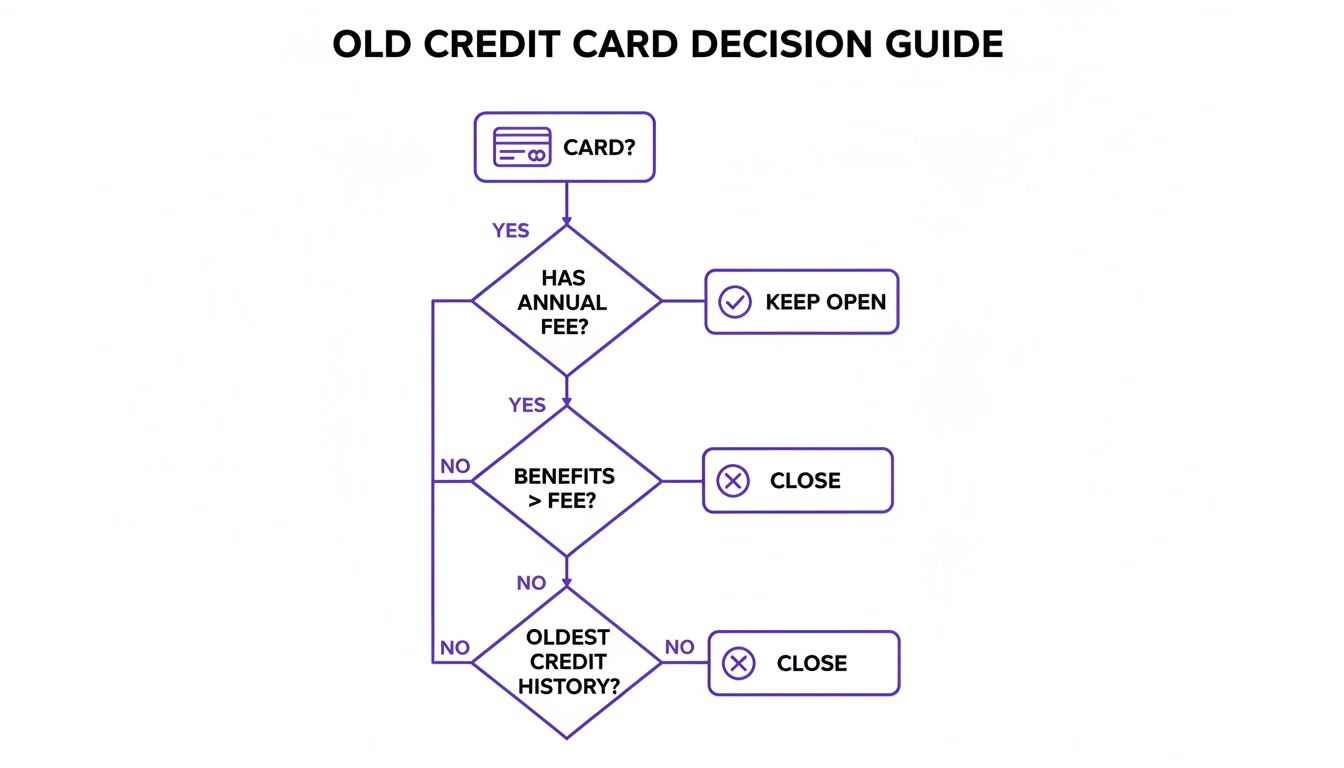

Now, deciding what to do with your older, accurate accounts can be a bit tricky. This flowchart breaks down the thought process for whether you should keep or close an old credit card.

The biggest takeaway here is that keeping old, no-fee cards open is usually your best bet. It lengthens your credit history, which is a major plus for your score. Juggling all this—manually checking reports and making smart account decisions—can feel overwhelming. An app like NeoSpend can be a huge help by putting a consolidated view of all your accounts in one place, making it way easier to spot issues and stay on top of your credit health.

Credit Strategies for Different Life Stages

Your financial life changes, and so should your credit strategy. What works when you're a student at McGill is going to look a lot different from what you need when you're buying a house in Calgary. The secret to a great credit score isn't just about following rules; it's about adapting your game plan as you hit new milestones.

Everyone's journey is a bit different, but let's break down some smart moves for common situations Canadians find themselves in.

For Students Building Credit from Scratch

Getting your first credit product can feel like a classic catch-22: you need a credit history to get credit. The trick is to start small and be disciplined. Your main goal is simply to show lenders you can be trusted, even before you have a long track record.

A student credit card or a secured credit card is your best bet here. They’re designed for people with thin or non-existent credit files. A secured card is especially low-risk for banks because you put down a small security deposit, which usually becomes your credit limit.

Use it for a small, predictable expense—like your monthly streaming subscription or a bus pass—and then pay the entire balance off every single month. Seriously. That one habit is the bedrock of a healthy credit score.

For Young Professionals and Gig Workers

Jumping into your career or the world of freelancing brings a whole new level of financial complexity. If you're a freelance graphic designer in Montreal, you know that some months are amazing while others are... not. That income rollercoaster makes a solid budget and on-time payments non-negotiable.

Your mission is to prove you're reliable, even when your paycheques aren't.

Keep your credit card balances low. It's tempting to lean on credit during slower months, but that's a dangerous trap. Try to build a buffer during the good times so you aren't forced to carry a balance.

Never, ever miss a payment. With income coming in at odd times, it’s easy to let a due date slip by. Set up calendar alerts, automatic payments—whatever it takes.

Build that emergency fund. Having three to six months of living expenses tucked away is a game-changer. It means a client paying late is an annoyance, not a financial crisis that sends you into debt.

This is where a tool like NeoSpend can make a real difference. It lets you see all your freelance income and expenses in one spot, giving you a clear picture of your cash flow so you can plan ahead and never get caught off guard.

Your life stage dictates your financial focus. Whether you're building your first credit account or managing a complex family budget, the principles of on-time payments and low utilization remain the same—only the application changes.

For Growing Families and Homebuyers

Once you start adding a mortgage, a car loan, and maybe even a joint account with your partner into the mix, your financial world gets a lot bigger. At this stage, your focus shifts from building credit to protecting the great score you have so you can lock in the best interest rates for life's biggest purchases.

If you have joint accounts, communication is everything. Both of your credit habits are tied to that account, so you have to be on the same page about spending and bill payments.

When you’re gearing up to buy a home, lenders will put your credit report under a microscope. That means you’ll want to pay down existing balances to lower your debt-to-income ratio. It’s also smart to put a freeze on any new credit applications for several months before you apply for a mortgage.

Managing a busy household budget is tough, but an app like NeoSpend can help you track shared expenses and make sure nothing slips through the cracks as you work toward those big family goals.

Here's a quick summary of how your credit priorities might change as you move through life.

Credit-Building Focus by Life Stage

The primary goals and challenges you'll face with your credit shift over time. For a student, the biggest hurdle is just getting started. For a family, it's about juggling multiple large debts responsibly.

| Life Stage | Primary Goal | Key Challenge | Recommended Action |

|---|---|---|---|

| Student | Establish a positive history | Limited or no credit history | Get a secured or student credit card and pay it off in full monthly. |

| Young Professional | Manage fluctuating income | Irregular cash flow and new expenses | Build an emergency fund and use budgeting tools to automate payments. |

| Growing Family | Qualify for major loans | Juggling multiple debts and joint accounts | Maintain low credit utilization and coordinate with your partner on finances. |

No matter where you are, the core principles—paying on time and keeping balances low—always apply. You just have to adjust your strategy to fit your life.

Your Top Credit Questions, Answered

Let's be honest, the world of credit scores can feel a bit mysterious. When you're trying to build a better score, a lot of questions pop up. I get it. Here are some straightforward answers to the things Canadians ask most often.

How Long Does It Really Take to Improve a Credit Score?

This is the big one, and the answer is: it depends on what you’re fixing.

If you’ve got a maxed-out credit card and you pay down a huge chunk of it, you could see a jump in your score in as little as 30 to 60 days. The same goes for getting an error removed from your report. Those are quick wins.

But the real heavyweight champion of your credit score is your payment history. Lenders want to see that you’re reliable over the long haul. Building that kind of trust takes time. For significant, lasting improvement, you’re usually looking at a timeline of 6 to 12 months of consistent, on-time payments.

Will Checking My Own Credit Score Hurt It?

Nope, not at all. Think of it like looking in the mirror—it doesn't change what you see.

When you check your own score or pull your report from Equifax or TransUnion, it's called a "soft inquiry." It's for your information only and has zero impact on your score.

A "hard inquiry" is different. That happens when a lender pulls your file because you've applied for something new, like a mortgage or a credit card. These can cause a small, temporary dip in your score, but we’re usually only talking a few points.

What's a Good Credit Score to Aim for in Canada?

In Canada, scores run from 300 to 900. Anything over 660 is generally considered "good," and you'll likely get approved for most standard credit products. But good shouldn't be your final destination.

The real sweet spot is 760 or higher. Hitting that "excellent" range is where the magic happens. You unlock the best interest rates, get better terms, and have more negotiating power. We’re talking about saving thousands of dollars on a mortgage or car loan.

Getting your score into that top tier tells lenders you're a safe bet, and they'll compete for your business.

Keeping track of all the moving parts—balances, payments, and progress—is what makes the difference. Using an app like NeoSpend can help you see everything in one place, making it easier to make the smart, consistent choices that build an excellent credit score.

Key Takeaway: Improving your credit score in Canada is a marathon, not a sprint, but focusing on two key habits—always paying bills on time and keeping your credit card balances below 30% of your limit—will deliver the biggest results. Regularly checking your credit reports for errors is another powerful step you can take today.

Ready to see your whole financial picture in one place? NeoSpend gives you AI-powered insights and bill tracking to help you manage your money smarter. Explore how it works at https://neospend.com.