If you’re just starting out, the idea of building a credit rating in Canada can feel a bit abstract. But at its core, it’s really about one thing: showing lenders you can be trusted to handle borrowed money.

The best ways to do this are surprisingly simple. Make your payments on time, every single time. Keep your credit card balances from creeping up. And slowly, over time, build a track record with a few different kinds of credit. That's it. Nailing these fundamentals consistently is what separates a great score from an average one.

Your Game Plan for a Strong Canadian Credit Score

Think of your credit rating as your financial reputation, boiled down to a three-digit number. Lenders across Canada use this score to quickly gauge how risky it would be to lend you money. It has a huge say in whether you get approved for a mortgage for a condo in Toronto or a car loan for a drive through the Rockies, and it directly impacts the interest rates you’ll be offered.

A higher score tells lenders you’re a safe bet, which can save you a ton of money in the long run.

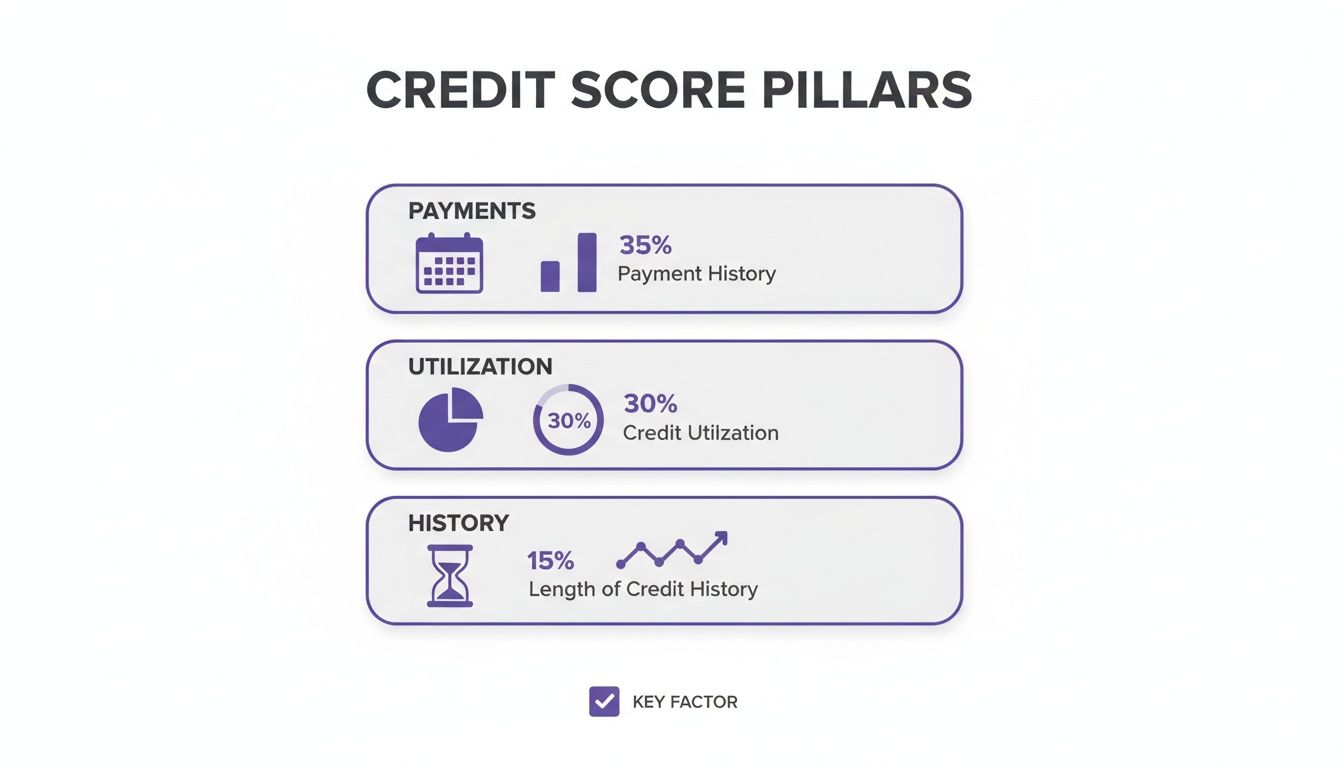

In Canada, two major credit bureaus—TransUnion and Equifax—are the keepers of this information. They gather data on your financial activities to calculate your score, which usually falls somewhere between 300 and 900. The infographic below breaks down the key ingredients that go into that final number.

As you can see, your payment history and how much credit you're using carry the most weight. If you’re looking for the biggest bang for your buck, focus your energy there first.

Why Your Credit Rating Matters for Everyday Canadian Life

Having a good credit rating isn't just about getting a 'yes' on loan applications. It’s about unlocking better financial opportunities and keeping more of your own money. A solid score can lead to lower interest rates, cheaper insurance premiums, and even help you skip the security deposit on a new phone plan or apartment rental.

The numbers don't lie. A recent Borrowell report about Canadian credit ratings and their impact showed that people with scores above 760 saved up to 1.5% on their mortgage rates compared to those with scores under 600. On a $400,000 mortgage over 25 years, that’s a difference of thousands—even tens of thousands—of dollars.

The 5 Pillars of Your Canadian Credit Score

So, what exactly are the credit bureaus looking at? While their formulas are a closely guarded secret, the five main components that make up your score are no mystery. This table breaks down the five critical factors that shape your credit score in Canada. Understanding how each one works is the first step toward taking control.

| Factor | Approximate Weight | How to Improve It |

|---|---|---|

| Payment History | 35% | Pay every single bill on time. Even one late payment can have a significant impact, so set up automatic payments or reminders. |

| Credit Utilization | 30% | Keep your balance below 30% of your available credit limit. For a card with a $1,000 limit, that means keeping your balance under $300. |

| Length of Credit History | 15% | Keep your oldest credit accounts open and in good standing, even if you don't use them often. A longer history shows stability. |

| Credit Mix | 10% | Show you can handle different types of credit, like a credit card (revolving) and a car loan or student loan (instalment). |

| New Credit | 10% | Avoid applying for too much credit in a short period. Each application creates a "hard inquiry," which can temporarily lower your score. |

Getting these five elements right is the foundation of a healthy financial future. It’s not about being perfect, but about being consistent.

Building a credit rating is a marathon, not a sprint. Small, consistent actions like setting up automatic payments and monitoring your spending add up to create a powerful financial reputation over time.

This is where having the right tools can make all the difference. An app like NeoSpend helps you manage your money smarter by bringing all your accounts into one place. It tracks your bills, sends you payment reminders, and gives you a clear picture of where your money is going, helping you stay on top of those crucial due dates.

Mastering the Core Habits of Credit Building in Canada

If you want to build a strong credit rating, it helps to start thinking like a lender. What do they really care about? It boils down to two simple things: do you pay back what you borrow, and do you do it on time?

Mastering these two core habits—timely payments and smart credit utilization—is the single most effective way to build a solid financial reputation here in Canada.

These aren't just minor suggestions; they are the absolute foundation of your credit score. Your payment history makes up a massive 35% of your score, making it the biggest piece of the puzzle. Right behind it is your credit utilization—how much of your available credit you’re using—at another 30%. That's right. Together, these two factors account for nearly two-thirds of what lenders see when they pull your file.

The Power of Consistent, On-Time Payments

Every single on-time payment you make is like a vote of confidence in your favour. On the flip side, even one payment that’s 30 days late can torpedo your score and haunt your credit report for years. Life gets hectic, and simply trying to remember every due date is a recipe for disaster. The easiest fix? Automate everything you can. Set up pre-authorized debits for fixed bills like your mobile phone, internet, and any loans. This way, your most important payments are always handled without you even thinking about it.

For bills with changing balances, like credit cards, automation is still your secret weapon.

- Set up automatic minimum payments. Think of this as your safety net. It guarantees you'll never get hit with a "late" mark, protecting your payment history from an accidental slip-up.

- Create calendar reminders. A few days before your due date, set a reminder to pop into your banking app and pay off the full balance, or at least as much as you can.

- Use a budgeting app. Tools like NeoSpend pull all your due dates into one clean dashboard. Getting a single, organized notification for all upcoming bills makes staying on top of things so much easier.

Putting these simple systems in place removes the risk of human error and helps you build a perfect payment history.

Understanding the 30 Percent Rule for Credit Utilization

The second pillar of a great credit score is your credit utilization ratio. It’s just a fancy term for the percentage of your available credit that you’re using at any given time. When lenders see that you're using a huge chunk of your available credit, it makes them nervous. It can look like you're stretched too thin.

A good rule of thumb is to keep your total credit utilization below 30% of your available limit. But the real pros—people with the highest credit scores in Canada—often keep theirs below 10%.

Let’s walk through a common Canadian scenario. Say you get a new credit card with a $1,000 limit. You use it for your monthly expenses—groceries, gas, a few subscriptions—and your balance hits $800. You're a responsible person, so you pay the full $800 balance before the due date. No problem, right?

Not so fast. Here’s the catch: your credit card company usually reports your balance to the credit bureaus before your payment is due. So, they report that you have an $800 balance on a $1,000 limit. That’s an 80% utilization rate! Even though you paid it off in full, that sky-high ratio gets recorded and can drag your score down.

Smart Strategies to Manage Your Utilization

To sidestep this common trap and get your credit-building on the fast track, you have to be strategic about when you pay. The whole game is to make sure the credit bureaus see a low balance.

Here’s how you can do it:

- Make Mid-Month Payments: Don't wait for your statement to arrive. Log in and make a payment halfway through the month. This simple move can slash your balance right before the reporting date, dramatically lowering your reported utilization.

- Request a Credit Limit Increase: After about six months of responsible card use, give your provider a call and ask for a higher limit. As long as your spending habits don't change, a higher limit instantly lowers your utilization ratio. For example, a $300 balance on a $1,000 limit is 30% utilization. But on a $2,000 limit, that same balance is only 15%.

- Track Your Spending in Real-Time: This is where a smart tool is a game-changer. The NeoSpend app can link to your accounts to show your real-time credit card balance. You can even set up alerts to ping you when your balance gets close to that 30% threshold, giving you a nudge to make a payment and keep your utilization score-friendly.

By combining dead-simple payment automation with savvy utilization management, you take direct control over the two most powerful factors in your credit rating. These aren't complicated financial schemes; they are simple, repeatable habits that lay the groundwork for long-term financial health.

Your First Steps to Building a Credit History in Canada

Trying to build a credit rating from scratch can feel like a classic Canadian catch-22. You need credit to get a score, but you need a score to get approved for credit. It's a frustrating loop, but the good news is there are a few well-worn, low-risk paths to get your financial story started.

This is where we move from theory into action. The point isn’t to go into debt; it’s to create a track record of responsible borrowing. Using the right tools, you can establish a positive payment history that credit bureaus like TransUnion and Equifax will recognize.

Start with a Secured Credit Card

For most Canadians starting from zero, a secured credit card is probably the single best tool for the job. These cards are designed specifically for people building or rebuilding their credit. How does it work? Unlike a standard credit card, a secured card requires you to put down a cash deposit. This deposit usually sets your credit limit. So, if you deposit $500, your credit limit becomes $500. This makes it incredibly low-risk for the bank because your own money secures what you can borrow. You'll find these offered by most major Canadian banks.

To make it work for you, follow this simple plan:

- Make small, routine purchases. Think of something you already pay for, like a Netflix subscription or your weekly gas fill-up.

- Pay the entire balance off every single month. This part is critical. The goal is a perfect payment history, not carrying debt and paying interest.

- Keep your balance low. Even with a small limit, aim to use less than 30% of it. On that $500 limit, that means keeping your balance under $150 when the statement comes out.

Stick with this for six to twelve months, and you can often "graduate" to a regular, unsecured credit card and get your deposit back.

Become an Authorized User

Another common strategy is becoming an authorized user on a trusted family member's credit card. If you have a parent or partner with a long, healthy credit history, they can add you to their account. You get a card in your name, and their good habits—like on-time payments and a long account history—can start appearing on your credit report. This can be a huge head start. But there's a serious catch.

Important Takeaway: If the main cardholder ever misses a payment or lets their balance get too high, that negative mark will land on your credit report, too. It could do some serious damage, so make sure you partner with someone you completely trust.

This approach really only works when there's open communication and a clear understanding about spending between you and the primary cardholder.

Use Your Existing Bills to Your Advantage

You don't necessarily need a credit card to get on the board. Some bills you're already paying can help you establish a credit file, as long as the company reports your payments to the bureaus. In Canada, the most common example is your mobile phone plan. When you sign up for a contract with a provider like Bell, Rogers, or Telus, make sure the account is in your name. These companies often report your monthly payment history.

A consistent record of paying your phone bill on time creates what’s called a "tradeline" on your credit report—an excellent first building block. This can also apply to some utility providers, so it never hurts to ask if your hydro or internet company reports to the credit bureaus.

No matter which path you take, consistency is key. Using a tool like NeoSpend can help you manage your money smarter right from the beginning. By tracking due dates and monitoring your spending, you can make sure every single payment is on time, turning everyday bills into powerful tools for building the credit you need for your future.

Thinking Beyond the Basics: Building a Strong, Diverse Credit Profile

Okay, so you’ve got the fundamentals down. You're paying your bills on time and keeping your credit card balances low. That's a huge win, and it forms the bedrock of a good credit score. But to get into that excellent credit territory, you need to show lenders you can handle more.

It’s about demonstrating financial maturity. Think of it from their perspective: someone who reliably pays off a single credit card is great. But someone who has successfully managed different kinds of debt—say, a credit card and a small car loan—is an even more proven, lower-risk borrower.

Why a Healthy Credit Mix Matters

The mix of credit products you use, known as your credit mix, makes up about 10% of your credit score. That might not seem like a lot compared to payment history, but it’s often the secret ingredient that pushes a good score into the great range. Lenders like to see that you can manage two main types of credit:

- Revolving Credit: This is your flexible credit, like credit cards and lines of credit. You borrow, pay it back, and can borrow again up to your limit.

- Instalment Credit: These are loans with a finish line. Think car loans, student loans, or a mortgage, where you make fixed payments over a set period until it's paid off.

Handling both shows you’re a versatile and reliable borrower. A recent Financial Consumer Agency of Canada (FCAC) survey even found that 68% of young professionals saw their scores jump by 40+ points after adding a small instalment loan to their profile. For more financial context, you can dig into the DBRS Morningstar report on the Canadian government's rating for more financial insights.

A Note for Freelancers and Gig Workers

For the growing number of self-employed Canadians, proving financial stability is a whole different ball game. When your income fluctuates month to month, convincing a lender you're a safe bet requires a more strategic approach. They're looking for consistency, and that can be tricky to demonstrate. This is where getting organized becomes your superpower. You need to consolidate all your income and expenses to paint a clear, compelling picture.

For gig workers, a clear financial dashboard isn't just a nice-to-have; it's a critical tool for proving your creditworthiness. When you can show lenders a complete, organized view of your cash flow, you overcome the biggest hurdle of variable income.

An app like NeoSpend can be a total game-changer here. It helps you manage your money smarter by linking your bank accounts and cards, automatically sorting your various income streams into one unified report. This gives you a clear way to demonstrate consistent cash flow over time, making you a much stronger applicant.

Playing It Smart with Credit Inquiries

As you build out your credit profile, you’re going to apply for new products. Every time you do, the lender pulls your file, resulting in a hard inquiry on your report. This can cause a small, temporary dip in your score.

One or two inquiries a year is no big deal. But a flurry of applications in a short time frame is a major red flag for lenders. This behaviour, sometimes called "credit seeking," can make it look like you're in financial trouble. To avoid this, be strategic.

Here’s how to manage it:

- Give it some space. As a rule of thumb, try to wait at least six months between applying for new credit cards or other revolving products.

- Shop for loans the right way. When you're rate-shopping for a big loan like a mortgage or car loan, the scoring models cut you some slack. Multiple inquiries for the same type of loan within a short window (usually 14-45 days) are typically bundled together and treated as a single event.

- Apply because you need it, not because of a deal. Don’t get tempted to open a new store card just to save 10% on a sweater unless it fits into your broader financial plan. Building your credit mix should be a thoughtful process, not a series of impulse decisions.

By carefully adding a mix of credit and managing new applications with a clear strategy, you’re building a resilient profile that shows lenders you’re firmly in control of your financial future.

How to Protect Your Credit Score from Common Mistakes

You’ve worked hard to build a great credit score. It’s a huge financial win, but the job isn't done just because you've hit a high number. Now comes the equally important part: protecting it. A single missed payment or an error you didn’t catch can undo months of progress.

The best defence is a good offence. By keeping a close eye on your credit reports and being smart about your financial data, you can spot trouble before it spirals and protect the solid credit rating you’ve built.

Get into the Habit of Reviewing Your Credit Reports

Think of your credit report as your financial report card. Here in Canada, you have the right to get a free copy from both TransUnion and Equifax at least once a year. This isn’t just something you should do—it’s an essential part of your financial maintenance routine.

When you pull your report, you’re on the lookout for two things: accuracy and anything that looks fishy. Go through it line by line. Make sure every account listed is actually yours and that the payment history is correct. It’s not unheard of for a simple clerical error, like a payment being marked late when it was on time, to drag down your score unfairly.

You also need to watch for signs of identity theft, like:

- Credit inquiries you don’t recognize: This could mean someone has tried opening an account in your name.

- Accounts you never opened: This is a massive red flag.

- Incorrect personal info: Double-check that your name, address, and SIN are all correct.

If you find anything wrong, contact the credit bureau right away to get the dispute process started. The sooner you catch these things, the better.

Watch Out for Subscription Creep

It’s ridiculously easy to sign up for monthly subscriptions these days—a streaming service here, a fitness app there. But this convenience comes with a hidden risk called “subscription creep.” A forgotten free trial that quietly rolls over into a paid plan can easily lead to a missed payment, especially if it’s tied to an old credit card you don't use much.

This isn’t a small problem. For Canadian families trying to stick to a budget, forgotten subscriptions are a surprisingly common source of stress and can ding a credit report. In fact, research shows that top credit-scorers are incredibly disciplined; 76% of them have zero delinquencies on their reports, a huge difference from the average person. You can learn more about how creditworthiness is viewed globally by checking out this Wikipedia article on credit ratings.

Your financial data is one of your most valuable assets. Protecting it with strong security practices is non-negotiable for maintaining long-term credit health and peace of mind.

This is where a tool like NeoSpend can be a lifesaver. The app’s bill and subscription tracker automatically finds all your recurring payments and sends you a heads-up before they’re due. It helps you find those subscriptions you forgot about, avoid late fees, and make sure every payment goes out on time.

Make Your Digital Security a Priority

Protecting your credit score also means protecting your personal information from getting into the wrong hands. Having strong digital security habits is no longer just a nice-to-have.

Start with the basics. Use strong, unique passwords for all your financial accounts. And please, enable two-factor authentication (2FA) everywhere you can. It adds a crucial layer of security that makes it much tougher for fraudsters to get into your accounts, even if they somehow get your password.

When you choose a financial app, security should be at the top of your list. NeoSpend is built with bank-level security, including 256-bit encryption, to keep your sensitive data locked down. For privacy-conscious Canadians, it’s also good to know that NeoSpend has a strict policy of never selling or sharing user data, fully aligning with modern privacy laws like PIPEDA. Taking these simple steps helps build a digital fortress around your finances, safeguarding the credit score you’ve worked so hard for.

Common Questions About Building Credit in Canada

Even with a solid game plan, you probably still have a few questions rolling around in your head. The path to a great credit score can feel a bit confusing, but trust me, you're not alone in wondering about this stuff.

Let's clear up some of the most common questions we hear from Canadians who are just getting started.

How Long Does It Take to Build a Good Credit Rating from Scratch?

Building credit is a marathon, not a sprint. Patience is key. While you can often see some positive movement on your credit report within six months of responsible borrowing, building a truly strong score takes a bit longer. Lenders are looking for a consistent, reliable track record.

Most experts would say it takes around two to three years of steady, on-time payments and smart credit management to build what’s considered a "good" credit rating in Canada—that's typically a score of 660 or higher. The main thing is consistency. Even one secured credit card used responsibly is a powerful place to start.

Can I Build Credit Without a Credit Card?

You can, but it’s definitely the scenic route. Some utility providers and most major cell phone companies, like Bell and Rogers, will report your payment history to the credit bureaus. This means just paying your phone bill on time every month can create a positive entry on your credit file.

Another option is a "credit-builder loan" offered by some financial institutions. These are small loans where your payments get reported, but you don't actually get the cash until the loan is fully paid off. It's a way to prove you can handle payments.

While these methods work, the most direct and effective way for most Canadians to build a robust credit history is by responsibly using a credit card—even a secured one with a small limit.

Does Checking My Own Credit Score Lower It?

This is a classic credit myth, and the answer is a hard no.

When you check your own score or pull your own report, it’s called a “soft inquiry.” Soft inquiries are reviews that don't impact your score at all. In fact, checking your credit regularly is one of the smartest financial habits you can build. It helps you catch errors, spot fraud, and see your progress firsthand.

The inquiries that can temporarily ding your score are “hard inquiries.” These happen when a lender pulls your report because you've applied for a new loan or credit card.

Even then, the impact is usually small and fades over time. The main takeaway? Checking your own score is not only safe but something I highly recommend. Staying informed is the first step to staying in control.

Key Takeaway: Building a great credit rating in Canada boils down to consistent, simple habits: pay all your bills on time, keep your credit card balances low, and slowly build a mix of credit products. Mastering these fundamentals is the surest path to financial health. Ready to manage your money smarter? Discover how NeoSpend can simplify your finances and help you build credit with confidence. Explore more at https://neospend.com.