Before you start looking for ways to avoid capital gains tax, it's crucial to understand the basics. So, what is a capital gain? It’s simply the profit you make when you sell (or “dispose of”) an asset—like stocks, mutual funds, or a rental property—for more than you originally paid for it.

The most important thing to remember is that you’re not taxed on the whole profit. In Canada, only 50% of your capital gain gets added to your income and taxed at your personal rate. This key detail is a game-changer, and it’s where smart, practical planning can seriously lower your tax bill.

How Capital Gains Tax Actually Works in Canada

Let's clear the air. Many Canadians hear "capital gains tax" and picture a complex, unavoidable penalty on their investment growth. The good news is, it's not that scary, and the system has built-in rules you can use to your advantage.

To really get it, you just need to understand three key concepts:

- Adjusted Cost Base (ACB): This is your all-in cost for an asset. Think of it as the purchase price plus any expenses you paid to get it, like trading commissions or legal fees.

- Proceeds of Disposition: This is what you got for the asset when you sold it, after subtracting any costs associated with the sale (like another commission fee).

- The 50% Inclusion Rate: This is the magic number. The Canada Revenue Agency (CRA) only considers half of your capital gain to be taxable income.

The government doesn't tax your entire profit, just half of it. That’s a huge distinction that opens the door to strategic tax planning.

Let's Walk Through a Real-World Example

Imagine you bought 100 shares of a popular Canadian tech company a few years back in your non-registered account.

Here’s what your initial investment looked like:

- Purchase Price: 100 shares @ $50/share = $5,000

- Trading Commission: $10

- Your Adjusted Cost Base (ACB): $5,000 + $10 = $5,010

Fast forward a few years, the stock has performed well, and you decide it’s time to sell. You offload all 100 shares at $150 each.

- Sale Proceeds: 100 shares x $150 = $15,000

- Selling Commission: another $10

- Your Net Proceeds: $15,000 - $10 = $14,990

So, what's your capital gain?

Capital Gain = Net Proceeds - Adjusted Cost Base

$14,990 - $5,010 = $9,980

Your total profit is $9,980. But the CRA only cares about half of that. We just apply the 50% inclusion rate.

- Taxable Capital Gain: $9,980 x 50% = $4,990

This $4,990 is the amount that gets added to your income for the year. If you're in a 30% tax bracket, the tax hit on this tidy profit would be about $1,497 ($4,990 x 30%). That’s a practical and manageable amount.

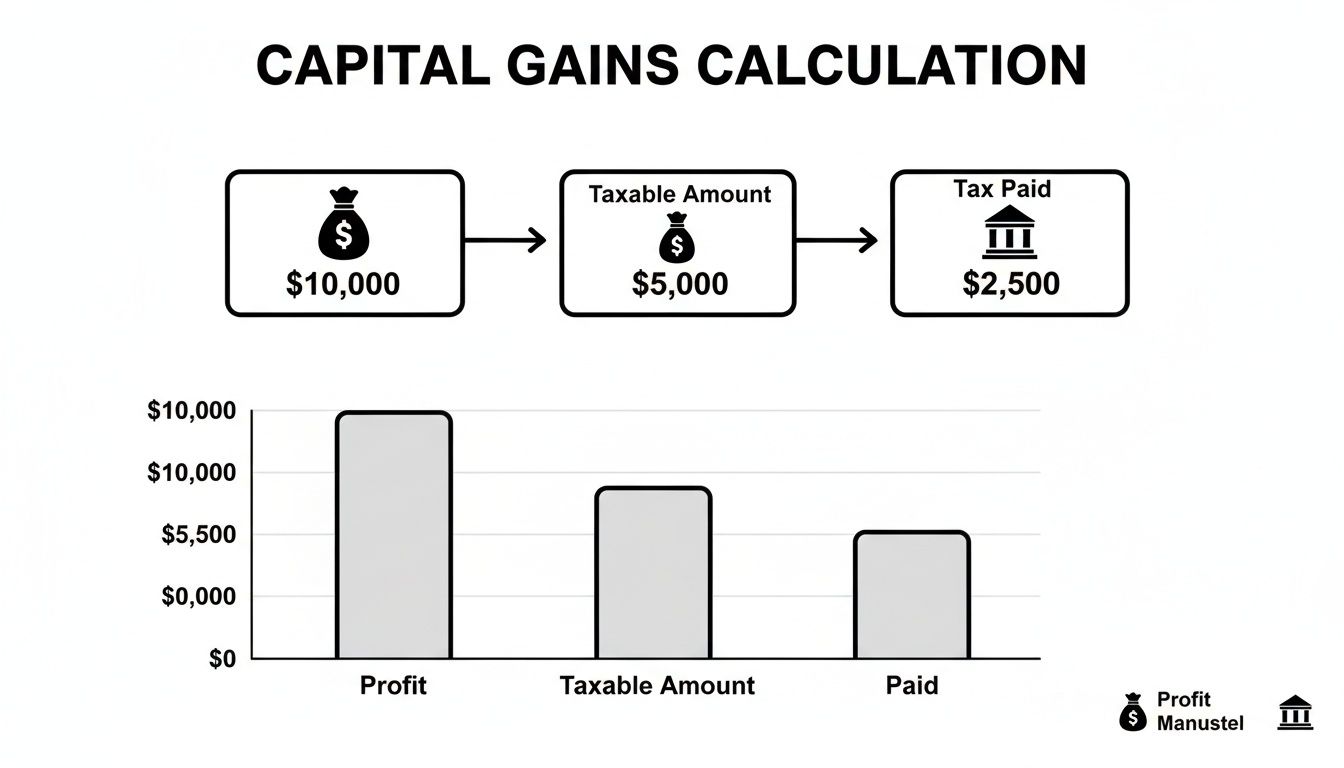

To make this even clearer, here’s a simplified breakdown assuming a clean $10,000 profit.

Quick Look at a Capital Gains Tax Calculation

| Metric | Amount | Description |

|---|---|---|

| Total Capital Gain | $10,000 | The total profit you made from selling your asset. |

| Inclusion Rate | 50% | The percentage of the gain that is subject to tax in Canada. |

| Taxable Capital Gain | $5,000 | The amount that will be added to your annual income. |

As you can see, the inclusion rate cuts your taxable amount in half right off the bat, significantly reducing the final tax you'll owe.

Smart Planning Starts with Smart Tracking

This example makes one thing crystal clear: keeping good records isn't just for accountants. If you forgot to factor in those commission fees, your ACB would be lower, and you'd end up paying more tax than you need to. For anyone making multiple trades, tracking the ACB for every single stock or ETF can turn into a real headache.

This is where having the right tools helps you manage your money smarter. An app like NeoSpend helps you pull all your financial data into one place, making it much easier to track investment-related expenses as they happen. Staying organized is the foundation of good tax planning and ensures you’re not leaving money on the table for the CRA.

Shield Your Investments Inside Registered Accounts

One of the most effective ways to avoid capital gains tax in Canada has nothing to do with complicated loopholes. It’s simply about where you choose to hold your investments. Think of registered accounts like the Tax-Free Savings Account (TFSA) and the Registered Retirement Savings Plan (RRSP) as special shelters designed by the government to protect your money from the taxman.

These accounts aren’t investments themselves. They’re more like containers that shield whatever you put inside—stocks, ETFs, mutual funds—from taxation. Any capital gains, dividends, or interest your investments generate within these accounts grow tax-free or tax-deferred. This allows your money to compound much more powerfully than it ever could in a regular, taxable account. This is the starting point for anyone serious about building wealth in Canada.

The TFSA: Your Ticket to Tax-Free Growth

The TFSA is, without a doubt, the most powerful tool for eliminating capital gains tax for the average Canadian investor. The name says it all. Any growth you achieve inside a TFSA is 100% tax-free, and when you decide to take the money out, those withdrawals are tax-free too.

Let’s use a simple Canadian scenario: you buy into a Canadian tech ETF inside your TFSA, and over the next decade, it does incredibly well. When you sell those shares to fund a down payment or take a dream vacation, every penny of that profit is yours. The Canada Revenue Agency (CRA) doesn’t touch it.

This diagram shows you what happens to a capital gain in a normal, non-registered account.

If you held that same investment in a TFSA, the last two steps—"Taxable Amount" and "Tax Paid"—would simply vanish. Gone.

The RRSP: Deferring Taxes for a Bigger Payoff Later

Your RRSP works a little differently, but it's just as crucial. The big win here is that contributions are tax-deductible, which means they reduce your taxable income right now, often leading to a nice tax refund in the spring.

Once inside the RRSP, your investments grow tax-deferred. You don’t pay a cent of tax on the capital gains from year to year. The tax bill only comes due when you start withdrawing the money, which for most people is in retirement when their income—and tax bracket—is much lower. The RRSP is all about kicking the tax can down the road, letting your investments grow at full speed for decades.

Just remember the key distinction: TFSA withdrawals are always tax-free. RRSP withdrawals, however, are counted as taxable income in the year you take them out.

A Tale of Two Accounts: A Practical Comparison

Let's see how this plays out with real numbers. Imagine you invest $20,000 in stocks. Ten years later, your investment has blossomed into $50,000, leaving you with a $30,000 capital gain.

- In a Non-Registered Account: Half of that gain ($15,000) gets added to your income for the year. Assuming a 35% marginal tax rate, you're on the hook for a $5,250 tax bill.

- In a TFSA: You sell the stocks and pull out the entire $50,000. You owe $0 in tax. That $30,000 profit is all yours.

The difference is massive. It’s why maxing out your registered accounts should be a top priority every single year. For instance, if you manage to grow $100,000 in a TFSA to $300,000, that entire $200,000 gain is tax-free. In a non-registered account, that same gain could easily trigger a tax bill north of $50,000. You can find more great examples of tax-sheltering strategies over at Wealthsimple.

Getting into the rhythm of contributing consistently is key. Setting up automatic transfers with a money management app like NeoSpend makes it feel effortless. By seeing your whole financial picture in one place, you can more easily manage your money smarter, find the cash to contribute, and hit your TFSA and RRSP goals—the true foundation of a solid tax-reduction plan.

Your Home Is Your Biggest Tax Shelter: Claiming the Principal Residence Exemption

For most Canadians, their biggest asset isn't a stock portfolio—it’s the roof over their head. This makes the Principal Residence Exemption (PRE) one of the most powerful and widely used tools for wiping out capital gains tax in this country.

Simply put, when you sell the home you’ve designated as your primary residence, this exemption can erase the entire capital gain. We're talking about a potentially massive tax saving.

Let's put that in perspective. Say you bought a home in Toronto for $400,000 and sold it a decade later for $1.1 million. That’s a $700,000 gain that could be completely tax-free thanks to the PRE. No other investment gets this kind of preferential treatment.

But, as with anything tax-related, the Canada Revenue Agency (CRA) has rules. Getting them right is critical to avoid a nasty, unexpected tax bill.

What Actually Qualifies as a Principal Residence?

To be eligible, a property has to meet a few basic conditions. You must own it (alone or with someone else), and you, your spouse (current or former), or one of your kids must have lived in it for at least part of the year.

The definition of "property" is quite flexible. It can be:

- A house, apartment, or condo

- A cottage or cabin

- A mobile home

- Even the unit you live in within a duplex

This flexibility means you could designate your cottage as your principal residence. But—and this is a big but—there's a major catch.

The “One Property Per Year” Rule

This is where the real strategy comes in. For any given year, your family unit (that’s you, your spouse, and any kids under 18) can only designate one property as your principal residence.

You can't have your cake and eat it too. You can’t claim the exemption on both your city house and your cottage for the same years of ownership.

Imagine a common Canadian scenario: you own a house in Calgary and a cabin in Canmore. When you sell the cabin, you’re forced to make a choice for every single year you owned both properties. If you use the PRE to shelter the gain on the cabin, you give up the right to claim it on your Calgary home for those same years. That could come back to bite you with a huge tax bill when you eventually sell the house.

Key Takeaway: You have to pick which property gets the tax-free shield for each overlapping year you own them. The smart move is to calculate which property has the bigger average gain per year and save the exemption for that one.

Partial Exemptions and Reporting—Don’t Skip This

What if a property wasn’t your main home for every single year you owned it? The CRA has a formula to figure out how much of the gain is tax-exempt.

The formula looks like this: (Number of years designated + 1) / (Total years owned) x Total Gain.

That little "+1" is a bonus. It’s designed to cover you in years when you move, letting both your old and new homes qualify as your principal residence in the same year. It's a small but helpful detail.

For instance, you owned a condo for 10 years but only designated it as your principal residence for 6 of them. The tax-free portion of your profit would be (6 + 1) / 10 = 70%. The other 30% of the gain is a taxable capital gain.

Here's something you can't ignore: even if your entire gain is exempt, you must report the sale. Since 2016, the CRA requires you to report the sale of your principal residence on Schedule 3 of your tax return. If you don't, you could face penalties, and they could even deny your claim altogether. Keeping track of sale documents and dates is essential—a tool like NeoSpend is a lifesaver for keeping all those financial records organized and accessible.

Using Tax-Loss Harvesting to Offset Gains

Beyond parking your money in registered accounts and using exemptions, one of the most powerful tools in your tax-minimizing toolkit is timing. Selling assets in a year when your income is lower—maybe you're on parental leave, switching careers, or newly retired—means any capital gains you trigger will be taxed at a much friendlier marginal rate.

But the real pro move here is tax-loss harvesting. It’s a simple, yet brilliant, strategy. You sell an investment that’s in the red to intentionally create a "capital loss." That loss can then be used to cancel out a capital gain from one of your winning investments. Think of it as using one portfolio loss to wipe out the tax bill on a big win.

This isn't just a frantic, year-end activity. It’s a smart, actionable insight you can use anytime. The whole point is to turn those "paper" losses into a tangible, tax-saving reality.

A Quick Look at How It Works

Let's say you have two different stocks in your non-registered portfolio this year.

- Your Winner: You sold some bank shares and locked in a sweet $10,000 capital gain.

- Your Loser: You’re also holding shares in a renewable energy company that have dropped in value, and you’re currently sitting on a $7,000 unrealized loss.

If you do nothing, you’re looking at a $5,000 taxable capital gain ($10,000 x 50%) tacked onto your income.

But if you get strategic, you can sell the energy stock and "realize" that $7,000 loss. Now, you can use that loss to directly offset your gain.

Your net capital gain is suddenly just $3,000 ($10,000 gain - $7,000 loss). The taxable portion of that is only $1,500 ($3,000 x 50%). You just saved yourself the tax on $3,500 of income.

This strategy is a perfectly legal and effective way to manage your tax liability. As the Government of Canada outlines, realized losses can be carried back three years or forward indefinitely, making them a flexible tool for long-term tax planning. Learn more about the capital gains inclusion rate on canada.ca.

Watch Out for the Superficial Loss Rule

Of course, the Canada Revenue Agency (CRA) is one step ahead of anyone trying to game the system. You can’t just sell a stock to claim a loss and then immediately buy it back the next day. That’s a big no-no, thanks to the superficial loss rule.

This rule says your capital loss will be denied if you, or someone affiliated with you (like your spouse), buys the exact same property within a 61-day window—that’s 30 days before the sale and 30 days after.

So, what if you still believe in that company long-term? You have a couple of solid options that keep you in the market without breaking the rules:

- Just wait: The simplest route is to wait 31 days before you repurchase the same stock or ETF.

- Buy something similar: Instead of buying back the exact same energy stock, you could immediately reinvest the cash into a different renewable energy company or a broad clean energy ETF. This way, you stay exposed to the sector’s potential upside while your loss claim remains valid.

This approach definitely requires you to keep a close eye on your portfolio to spot these opportunities when they pop up.

Stay on Top of It With the Right Tools

Tax-loss harvesting isn’t just a mad dash in December. Market volatility can create the best opportunities in March, August, or any other time of year. If you wait until the last minute, you might miss the most opportune moment to offset your gains.

This is where having all your financial information in one place is a game-changer. Using a tool like NeoSpend gives you a single dashboard for all your investment accounts. It helps you manage money smarter by making it so much easier to track performance across the board and spot those harvesting opportunities in real-time. Instead of sifting through a half-dozen different brokerage statements, you get a clear, consolidated view that helps you make tax-smart moves and keep more of your money working for you.

For Business Owners and Families: Next-Level Strategies

While registered accounts and tax-loss harvesting are the bread-and-butter for every investor, some of the most powerful tax-saving tools are unlocked in specific situations. For entrepreneurs, farmers, and anyone thinking about their family's financial legacy, Canada’s tax code has some incredibly generous provisions.

These strategies are definitely more complex and almost always require a chat with a tax professional. But understanding them is the first step. Let's dig into how you can protect your most valuable assets for the long haul.

The Game-Changer: The Lifetime Capital Gains Exemption

Easily one of the most significant tax breaks in Canada is the Lifetime Capital Gains Exemption (LCGE). It's the government's way of rewarding the risk-takers who build Canadian businesses from the ground up. The LCGE lets owners of qualified small businesses, farms, or fishing properties shelter a massive chunk of their capital gains when they sell.

As of June 25, 2024, that exemption limit was boosted to $1.25 million. Think about that. If you sell your qualifying small business corporation (QSBC) shares for a $1.5 million profit, you could exempt the entire gain up to the $1.25 million limit. Depending on your marginal tax rate, that could save you hundreds of thousands of dollars. You can find more detailed analysis on Canada's capital gains tax competitiveness from the Fraser Institute.

Picture this: you started a tech company in your garage years ago and poured your life into it. Now, you’re ready to sell your shares for a $1.2 million profit. Without the LCGE, you’d be looking at a taxable gain of $600,000. With it? You could potentially wipe that entire tax bill off the map, keeping over $300,000 in your pocket.

Smart Family Planning: The Spousal Rollover

For couples, one of the most common and effective ways to defer capital gains is the spousal rollover. This rule lets you transfer capital property—like stocks, mutual funds, or even a rental property—to your spouse or common-law partner without having to pay any immediate tax.

Instead of the CRA treating it as a sale, the asset "rolls over" to your spouse at its original cost base (ACB). The tax bill is effectively kicked down the road until your spouse eventually sells the asset.

This is a go-to strategy for a few key reasons:

- Income Splitting: If your spouse is in a much lower tax bracket, transferring an income-producing asset can shift the future tax burden on gains to them.

- Estate Planning: It’s a cornerstone of estate planning. It allows assets to pass seamlessly to a surviving spouse without an immediate tax hit, providing critical financial stability during a tough time.

Just be aware of the attribution rules—any income (like dividends) generated by the asset might still be taxed in your hands. But for capital gains, the deferral is the real prize.

The Power of Giving Back (Strategically)

Being charitable can also bring some serious tax perks, especially when you donate appreciated assets. One of the most tax-smart ways to give is by donating publicly traded securities (stocks, mutual funds, etc.) directly to a registered charity.

Here’s the magic: when you donate these securities in-kind—meaning you transfer the actual shares, not cash—the capital gains inclusion rate on that donation drops to zero.

This creates a powerful double tax benefit: You get a donation tax credit for the full market value of the securities, and you completely eliminate the capital gains tax you would have paid if you'd sold them first.

Let’s say you want to donate $20,000. You could sell stocks that have a $10,000 capital gain to get the cash, but you'd owe tax on a $5,000 taxable gain. By donating the stocks directly, that tax bill vanishes. You still get the full $20,000 donation receipt to use on your tax return.

Whether you're exploring the LCGE, a spousal rollover, or strategic donations, careful planning and meticulous record-keeping are non-negotiable. This is where tools like NeoSpend can be a huge help, consolidating your financial data so you and your tax pro have a clear picture to work from when executing these advanced strategies.

Common Questions on Canadian Capital Gains Tax

When it comes to capital gains, a few questions pop up constantly. Getting clear, practical answers is the first step to making smart financial moves and legally minimizing your tax bill. Let's break down some of the most common questions from Canadians.

Do I Pay Capital Gains Tax on Gifted Property?

In most cases, yes—and this trips a lot of people up.

When you gift an asset like stocks or a cottage to anyone other than your spouse, the Canada Revenue Agency (CRA) considers it a deemed disposition. This is a term that means the CRA treats it as if you sold the asset at its current fair market value, even if no money changed hands.

You, the person giving the gift, are on the hook for reporting the capital gain and paying the tax.

For example, say you gift stocks worth $50,000 to your adult child. If you originally bought them for $10,000, you’ve just created a $40,000 capital gain for yourself. That means you’ll have a $20,000 taxable gain to report on your tax return.

Can I Claim a Capital Loss on My Home?

This is a firm no. Your principal residence is what the CRA calls personal-use property.

The Principal Residence Exemption is a huge perk, allowing you to sell your home tax-free. But the rule doesn't work in reverse. If you sell your home for less than what you paid, the CRA sees that as a personal loss, not an investment loss. You can’t use it to offset capital gains from your other investments, like stocks or mutual funds.

How Long Must I Hold an Asset to Avoid Tax?

This is a popular myth, likely borrowed from tax rules in other countries. In Canada, there is no magic holding period that eliminates or even reduces capital gains tax. A gain is a gain whether you held the asset for 24 hours or 24 years.

The tax gets triggered when you sell for a profit, period. The real strategy isn't about how long you hold an asset, but where you hold it.

An investment held in a Tax-Free Savings Account (TFSA) for one year can generate a massive profit with $0 tax owing. On the flip side, an investment held for three decades in a regular non-registered account will still face capital gains tax when you eventually sell.

What Records Should I Keep for Tax Purposes?

Good records are your best friend at tax time. Without them, you’re just guessing, and the CRA isn’t a fan of guesswork. Being organized is the secret to proving your numbers and making sure you don't overpay.

At a minimum, you need to hang onto:

- Proof of purchase: Trade confirmations or statements showing what you paid and when.

- Proof of sale: Documents showing what you sold the asset for and the date.

- Records of any costs: Keep track of commissions, brokerage fees, or legal fees. These costs adjust your cost base and reduce your gain.

- Property improvement receipts: For real estate, every receipt for a major upgrade (a new kitchen, an addition) increases your cost base and shrinks your future tax bill.

This is where a good financial tool is a game-changer. Instead of drowning in a shoebox full of crumpled receipts, an app like NeoSpend can help you track and categorize everything digitally. Having a clean, organized record of your financial life makes tax time way less stressful and ensures your calculations are spot on.

Understanding how to avoid capital gains tax is all about using the right strategies—from maximizing your TFSA and RRSP to timing your sales. The key takeaway is that with smart planning, you have significant control over your tax bill.

Ready to get a clearer picture of your finances and make tax season a breeze? NeoSpend brings all your accounts into one place, helping you track expenses and manage your money with confidence. Find out more at neospend.com and explore how smart tracking leads to smarter tax planning.