Wondering how much of your paycheque you should actually be saving? It’s a common question for many Canadians. A great rule of thumb to start with is the 50/30/20 rule. It’s a simple but powerful guideline that suggests putting 20% of your after-tax income toward your savings goals.

Think of it as a solid foundation for building a financially secure future, without the headache of tracking every single penny.

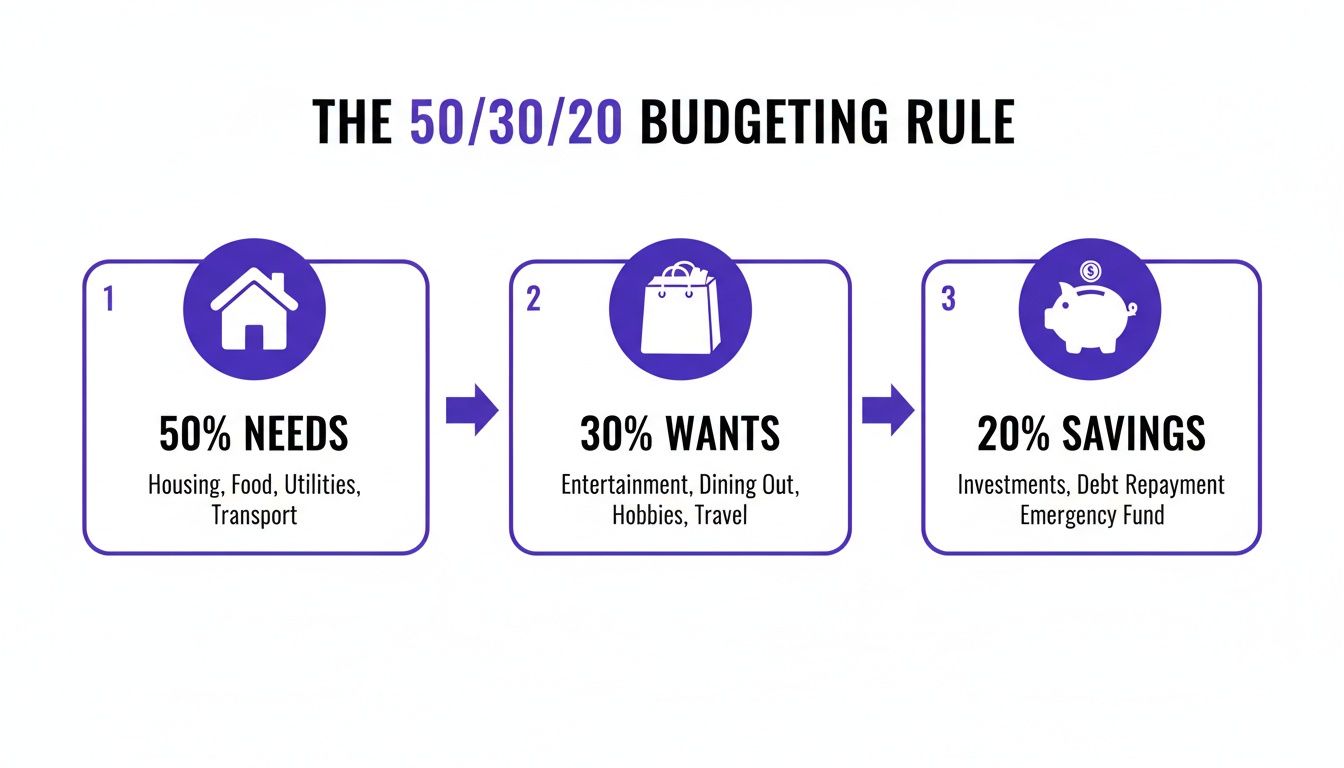

Breaking Down the 50/30/20 Savings Rule

The 50/30/20 rule is so popular because it’s incredibly straightforward. Instead of getting bogged down in dozens of tiny expense categories, you just split your money into three main buckets. Every dollar has a job to do the moment it lands in your account.

It’s less about strict, restrictive budgeting and more about creating a balanced, intentional plan for your money. You get to cover your essentials, enjoy your life now, and still build wealth for the future. For a lot of Canadians, this simple framework takes the guesswork and stress out of personal finance.

Understanding Each Category

Let's get practical. Here’s how your take-home pay gets divided:

- 50% for Needs: This is the biggest chunk, and it’s for all the absolute essentials. We’re talking rent or mortgage, groceries, utilities, your transit pass to get to work, and the minimum payments on any debts. These are the non-negotiables that keep your life running smoothly.

- 30% for Wants: This is the fun stuff! It covers all your lifestyle choices and discretionary spending. Think dining out with friends in Toronto, your Netflix and Crave subscriptions, a weekend getaway to Canmore, or that new jacket you’ve been eyeing. This is the money that adds joy and personality to your life.

- 20% for Savings: This is where the magic happens. This slice of your paycheque is dedicated to your financial goals. That means building up your emergency fund, making extra payments on high-interest debt (like credit cards), and investing in your TFSA or RRSP. This 20% is your investment in your future self.

To give you a clearer picture, here’s a quick summary of how it all works.

A Quick Look at the 50/30/20 Savings Rule

The 50/30/20 rule is a popular starting point for allocating your after-tax income. It provides a simple structure to balance your current expenses with future goals.

| Spending Category | Percent of Paycheck | What It Typically Covers |

|---|---|---|

| Needs | 50% | Rent/mortgage, groceries, utilities, transportation, minimum debt payments. |

| Wants | 30% | Dining out, entertainment, hobbies, shopping, travel. |

| Savings | 20% | Emergency fund, debt repayment (above minimums), investments (TFSA, RRSP). |

This framework isn’t about perfection; it’s about providing a clear, balanced path for your money each month.

By dedicating a specific percentage to savings right off the bat, you're "paying yourself first." This simple shift in mindset makes saving a non-negotiable priority—just like paying rent—instead of an afterthought.

This approach gives you a quick diagnostic of your financial health. If your "Needs" are eating up 70% of your income, that’s a clear signal to look for ways to cut back on fixed costs. Or, if your "Wants" are creeping up, you know exactly where you can dial things back.

Making this whole process even easier is where a little tech comes in handy. An app like NeoSpend can automatically categorize your spending for you, showing you a real-time breakdown of your 50/30/20 split. It gets rid of the need for manual spreadsheets and gives you a clean, visual report card on your habits, making it a breeze to stay on track.

Calculating a Savings Rate That Actually Works for You

Those popular rules of thumb, like the 50/30/20 method, are a fantastic place to start. But let's be honest—they're not a one-size-fits-all solution for life here in Canada. Your perfect savings rate is deeply personal. It's a number that needs to reflect your unique income, your debts, and what you’re actually trying to build for your future.

Figuring this out isn't about getting tangled up in complicated spreadsheets. It’s about taking back control. When you find your personal savings rate, you get a clear, honest snapshot of your financial health. That's what lets you make smart decisions that line up with the life you want to live.

How to Find Your Personal Savings Rate

Calculating your savings rate is refreshingly simple. It’s just a straightforward formula that shows you exactly what percentage of your income you’re tucking away.

Your Savings Rate = (Total Amount Saved / Total Take-Home Pay) x 100

Let’s quickly break that down. Your "total amount saved" is any money you’re actively putting aside—think contributions to your TFSA or RRSP, cash for your emergency fund, or even extra payments you’re making on debts (anything above the minimum). Your "total take-home pay" is just the net amount that lands in your bank account after all the taxes and deductions are gone.

So, if your monthly take-home pay is $4,000 and you sock away $600, your savings rate is a solid 15%. Knowing this number is the critical first step toward setting goals that you can actually hit.

Savings Rates in Real Canadian Scenarios

Your ideal savings rate is going to shift depending on where you are in life and, frankly, where you live. The financial reality for a software developer in pricey Vancouver is worlds away from a teacher building a life in more affordable Halifax.

Let's look at a couple of real-world examples:

- Priya, a Vancouver Software Developer: Priya brings home $6,000 a month. With Vancouver's sky-high rent and living costs, her "Needs" eat up a huge chunk of her budget. She's aiming to save $1,200 a month, which puts her at a 20% savings rate. It’s a tight balance, but it lets her max out her TFSA while still having enough left to enjoy the city.

- Marc, a Halifax Teacher: Marc’s take-home pay is $4,200 a month. The lower cost of living gives him a lot more breathing room. After covering the mortgage and family expenses, he saves $840 a month. That’s also a 20% savings rate, which he funnels into his RRSP and his kids’ RESP.

See? The percentage might be the same, but how they get there looks completely different. What really matters is building a plan that fits your life without making you feel squeezed. It’s all about striking that sustainable balance between living well today and setting yourself up for tomorrow.

Ditch the Manual Math with Automation

Look, nobody loves manually tracking every single dollar just to figure out their savings rate. It's tedious, and it's easy to fall behind. This is where modern tools can seriously simplify your financial life.

Instead of fighting with a spreadsheet, an app like NeoSpend can do all the heavy lifting for you. You just securely connect your bank accounts, and it automatically crunches the numbers by analyzing your income and expenses.

This gives you an up-to-the-minute calculation of your personal savings rate right on your dashboard—no manual entry required. It’s a game-changer for effortlessly tracking your progress and staying on top of your goals.

Smart Savings Strategies for Different Canadian Lifestyles

The 50/30/20 rule is a fantastic starting point, but let's be real—your financial life doesn't fit neatly into a template. The real answer to "how much of my paycheque should I save?" shifts and evolves as you do.

A savings plan that works for a young professional grinding it out in downtown Toronto is going to look completely different from one for a growing family in Calgary or a freelancer hustling in Montreal. Your strategy needs to be flexible, adapting to your unique circumstances and goals. By looking at a few real-life Canadian scenarios, we can build a savings habit that feels less like a strict rule and more like a custom-fit plan.

To put this into perspective, let's break down how savings goals and rates can change depending on where you are in life.

Savings Goals and Rates for Different Life Stages

| Your Life Stage | Suggested Savings Rate | Top Financial Priorities |

|---|---|---|

| Young Professional (20s-Early 30s) | 15-20% | Building an emergency fund, aggressively paying down high-interest debt (like student loans), and starting to invest in a TFSA. |

| Growing Family (30s-40s) | 10-15% | Maximizing RRSP contributions (especially with employer matching), funding RESPs for children's education, and saving for larger family goals like a home upgrade or vacations. |

| Freelancer / Self-Employed (Any Age) | 25-30% | Creating a robust emergency fund (6+ months), setting aside funds for taxes (income tax, HST/GST), and consistently funding personal retirement accounts (RRSP/TFSA). |

These aren't rigid rules, but they give you a solid idea of how priorities shift. Now, let's see what this looks like in action.

For the Young Professional Building a Career

Meet Maya, a 28-year-old graphic designer living in a major Canadian city. After taxes, she brings home about $4,500 a month. Her biggest hurdles? Sky-high rent, a stubborn student loan, and all the temptations that come with city living.

Maya’s main goal is to carve out some financial independence. She's focused on crushing her student debt while also getting a head start on long-term investing.

- Savings Rate: Maya targets 15-20% of her pay, which works out to about $675 to $900 each month.

- Top Priorities: She splits her savings between a three-month emergency fund, making extra payments on her student loans to save on interest, and consistently feeding her TFSA.

- How NeoSpend Helps: Maya uses NeoSpend to create specific goals like "Emergency Stash" and "Student Loan Freedom." The app automatically tracks her progress, showing her exactly where her money is going, which is a huge motivator.

For the Growing Family Balancing It All

Now picture Liam and Chloe, a couple in their late 30s with two young kids. Their combined take-home pay is $8,000 a month. Their financial life is a constant juggling act between daily costs like daycare and groceries, and looking ahead to retirement and their kids' education.

Their focus has shifted to long-term security. They need every dollar to work as hard as possible for their family's future.

Key Insight: For families, the game changes from aggressive individual saving to strategic, multi-goal planning. It’s all about balancing today's needs with long-term security for everyone under one roof.

- Savings Rate: They aim to save 10-15% of their income, landing between $800 and $1,200 monthly. It’s a smaller percentage than Maya's, but on a larger household income, it's a significant amount.

- Top Priorities: Their savings are automatically funnelled into three main buckets: their RRSPs (taking full advantage of employer matching), a Registered Education Savings Plan (RESP) for the kids, and a "Family Fun" fund for vacations.

- How NeoSpend Helps: Liam and Chloe use NeoSpend’s dashboard for a bird's-eye view of their household cash flow. They’ve set up bill reminders for the mortgage and daycare, and the app’s insights help them spot places to trim spending—like on groceries or subscriptions—to free up more cash for their RESP.

For the Freelancer Navigating Fluctuating Income

Finally, let’s look at David, a 40-year-old freelance writer. His income is a rollercoaster—one month he might clear $7,000, the next it could be $3,500. His biggest challenge is creating stability without a predictable paycheque.

For freelancers like David, the secret is to save a much higher percentage during the good months to ride out the lean ones. This approach smooths out the financial ups and downs that are part of the gig economy. In the current economic climate, this kind of discipline is more crucial than ever. For a freelancer earning $80K a year after expenses, saving 25% means putting aside $20,000 annually, giving their RRSP and TFSA a powerful boost. More insights on building financial security can be found in the current economy on calbudgetcenter.org.

- Savings Rate: David shoots for an ambitious 25-30% of every single invoice. This aggressive rate ensures he has enough to cover his taxes, business expenses, and personal savings without breaking a sweat.

- Top Priorities: His number one goal is a rock-solid six-month emergency fund. He also meticulously sets aside money for income tax and HST/GST payments in separate accounts and makes regular contributions to his personal RRSP.

- How NeoSpend Helps: David leans on NeoSpend to wrangle his variable cash flow. By linking his business and personal accounts, he gets one unified view of his entire financial world. He uses the app’s flexible goal-setting feature to adjust his savings based on what he earns each month, and its smart nudges help him spot non-essential expenses to cut during slower periods.

Balancing Savings with Debt and Major Financial Goals

Figuring out how much to save gets a whole lot trickier when you're also staring down a mountain of debt or dreaming about big life goals. It’s that classic Canadian money puzzle: do you throw every spare dollar at your student loan, or do you start building a down payment for a house?

The good news? You don’t actually have to choose one over the other.

With a solid strategy, you can make real progress on all fronts. It’s all about figuring out where your money makes the biggest impact and creating a plan that moves you forward without making you want to tear your hair out. You can absolutely save for your future while tackling the debt you have today.

Tackling Debt The Smart Way

Let's be clear: not all debt is created equal. The real key is to prioritize high-interest debt—the kind that grows like a weed and costs you a fortune over time. Think of it like a leaky bucket; you have to patch the biggest, gushiest holes first to stop losing money.

- High-Interest Debt (The Priority): This is your credit card debt, often with interest rates that shoot past 20%. This stuff can snowball out of control fast, so making more than the minimum payment is non-negotiable.

- Moderate-Interest Debt (The Manager): This bucket usually holds things like car loans or personal lines of credit. They’re important to manage, but they don’t grow with the same terrifying speed as a credit card balance.

- Low-Interest Debt (The Slow Burn): Government student loans and your mortgage typically fall in here. They have lower interest rates and long repayment schedules, making them much more manageable to carry while you work on other goals.

The most powerful approach is to always make the minimum payments on all your debts, but then funnel every extra cent you have toward the one with the highest interest rate. This strategy saves you the most money in the long run, period.

Popular Debt Repayment Strategies

Once you’ve got your debt priorities straight, you need a game plan. Two of the most popular methods out there are the debt avalanche and the debt snowball. They both work wonders; the "best" one is just the one that keeps you fired up and in the game.

- The Debt Avalanche: This is the purely logical approach. You list your debts from the highest interest rate to the lowest. Then, you hammer away at the highest-rate debt with all your extra cash while making minimum payments on everything else. Mathematically, this saves you the most money on interest.

- The Debt Snowball: This one is all about psychology and momentum. You list your debts from the smallest balance to the largest and attack the smallest one first. Getting that first quick win gives you a huge motivational boost to keep rolling and tackle the next one.

Juggling Multiple Financial Goals

Trying to save for a down payment, a wedding, and retirement all at once can feel completely overwhelming. But here’s the secret: it’s not about doing everything perfectly. It’s about making steady, intentional progress on the things that actually matter to you.

This is where visualizing your goals becomes a game-changer. By creating separate "buckets" or funds for each objective, you’re giving every single dollar a specific job. You can physically see how close you are to that "Dream Trip to Italy" or your "New Car Fund," which makes saving feel way more real and exciting.

For example, you could decide to split your 20% savings rate up: maybe 10% goes straight to your RRSP, 5% gets tucked away for your down payment, and the last 5% is for that European vacation you’ve been dreaming of. The exact split is completely up to you and what you value most.

This is exactly what the goal-tracking feature in an app like NeoSpend is built for, letting you see all your different savings goals in one simple dashboard.

Those visual progress bars give you instant clarity. You can see at a glance which goals are on track and which might need a little extra love. By managing everything in one place, you can confidently decide exactly where every dollar from your paycheck should go.

Putting Your Savings on Autopilot for Guaranteed Success

Let’s be honest: the secret to consistently hitting your savings goals isn’t about having superhuman willpower. It’s about building a smart system that does the heavy lifting for you. The single most effective strategy is a simple one: “paying yourself first,” and the best way to pull it off is with automation.

This whole approach flips the usual way of saving on its head. Instead of trying to save whatever’s left at the end of the month, you treat your savings like any other non-negotiable bill. By setting up automatic transfers from your chequing account to your savings—whether it’s a TFSA or a high-yield savings account—the moment your paycheque lands, you remove the temptation to spend that money.

It’s a small tweak that turns saving into an effortless habit rather than a daily struggle. Your financial future gets funded before you even have a chance to think about it.

Why Automation Is Your Best Friend

Relying on memory and discipline alone to save money is a recipe for falling short. Life gets busy, unexpected costs pop up, and even the best intentions can go out the window. Automation acts as a powerful barrier against all of that.

When you automate your savings, you’re creating a system that works for you, not against you. That consistency is what really builds momentum and lets you take advantage of compounding over time. Saving is no longer an active chore; it's a success story quietly running in the background.

How to Set Up Your Automatic Savings System

Getting started is surprisingly simple. You can usually get it done in just a few minutes through your online banking portal.

- Choose Your Destination: Decide where your savings will go. A high-interest savings account for your emergency fund, a TFSA for tax-free growth, or an RRSP for retirement are all great options.

- Determine the Amount: Look at your personal savings rate and pick a fixed amount to transfer from each paycheque.

- Schedule the Transfer: Set up a recurring transfer for the same day you get paid. If you’re paid bi-weekly, schedule a bi-weekly transfer. It’s that easy.

Key Insight: Automating even a small amount is so much better than saving nothing at all. You can start with just $25 per paycheque and gradually bump it up as you get more comfortable with your budget. The goal is to build the habit first.

While setting a target is a great start, many people are falling behind. Canadians should be aiming to save 15-20% of their paycheque to build real financial security. On a $6,000 monthly take-home pay, saving 15% ($900) adds up to $10,800 a year. That’s a life-changing boost for your TFSA. You can learn more about the economic outlook from this Comerica report.

This is exactly where a tool like NeoSpend can make a huge difference. The app’s smart insights analyze your cash flow and spending patterns to suggest an ideal, sustainable amount to automate. It helps you find that sweet spot where you're saving consistently without feeling the pinch, making sure your automated system is set up for long-term success.

A Few Common Questions About Saving Your Paycheque

Once you’ve got the basics down, the real-life questions start to bubble up. It's one thing to hear you should save a certain amount, but it’s a whole different ball game when you're staring at a pile of debt or a budget that already feels stretched to its limit.

Let's walk through some of the most common hurdles Canadians face when they decide to get serious about saving. Think of this as your practical guide for those tricky "what if" moments.

Should I Save or Pay Off Debt First?

Ah, the classic financial tug-of-war. The best move here isn't usually all-or-nothing. It's about balance and smart prioritization.

High-interest debt—think credit card balances sitting at 19.99% or more—is a five-alarm fire. The interest you're paying is almost certainly costing you way more than you could earn from any standard savings account. That means your main focus should be on wiping it out as fast as you can.

But—and this is a big but—don't neglect your emergency fund entirely. Putting aside even $500 to $1,000 creates a crucial buffer. That little safety net is what stops a surprise car repair from sending you right back into high-interest debt, trapping you in a cycle that's incredibly frustrating to break.

The Framework: First, build a small starter emergency fund. Then, throw everything you can at high-interest debt. Once that’s gone, pivot back to building up your emergency fund to a full 3-6 months of living expenses and start ramping up your other long-term savings.

What If I Can’t Afford to Save 20 Percent Right Now?

Don't let the 20% rule scare you into doing nothing. If that number feels completely impossible right now, that's okay. The most important thing you can do is simply start.

Forget perfection. Aim for progress. Starting with just 1% or 2% of your paycheque is a huge win because you're building the habit of paying yourself first. On a $4,000 monthly take-home pay, saving 2% is $80. It might not sound like a game-changer, but that's $960 in a year you wouldn't have had otherwise.

Here’s a simple game plan to get you going:

- Start small: Pick a percentage that feels almost ridiculously easy, like 1%.

- Automate it: Set up an automatic transfer for that amount to hit your savings account every single payday.

- Level up slowly: Every time you get a raise or pay off a debt, bump your savings rate up by another 1%. You’ll barely feel the difference in your day-to-day spending, but your savings will start to grow on their own.

Where Is the Best Place to Put My Savings in Canada?

Okay, so you're saving money. Great! Now, where should it live? In Canada, you’ve got a few great options, and each one is built for a different job.

- High-Interest Savings Account (HISA): This is the perfect home for your emergency fund and any short-term goals (think saving for a vacation or a down payment on a car). Your money is safe, you can get to it easily, and it earns more interest than a standard chequing account.

- Tax-Free Savings Account (TFSA): The TFSA is a powerhouse for medium to long-term goals. Any growth your money sees inside—from interest, dividends, or investments—is completely tax-free. Seriously. This makes it amazing for goals like a house down payment or beefing up your retirement nest egg.

- Registered Retirement Savings Plan (RRSP): As the name suggests, an RRSP is mainly for retirement. The money you put in is tax-deductible, which lowers your taxable income for the year. The investments inside grow tax-deferred until you pull the money out in retirement.

How Can an App Like NeoSpend Help Me Save More?

Knowing what to do is half the battle; actually doing it is the other half. This is where a good money management app stops being a "nice-to-have" and becomes your secret weapon.

An app like NeoSpend cuts through the noise by pulling all your financial info into one simple dashboard. Instead of wondering where your money disappeared to last month, you get an automatic, categorized breakdown of your spending habits. That clarity is the first step toward finding extra cash to save.

For instance, NeoSpend helps you:

- Spot Savings Opportunities: Its smart insights comb through your spending and flag places you could cut back, like that subscription you forgot about or all those late-night food delivery orders.

- See Your Progress: When you set up goals in the app, you can actually watch yourself get closer to them. Seeing the progress bar for your "Emergency Fund" or "Dream Trip" fill up is an incredible motivator.

- Stay on Budget without the Headache: The app's automatic tracking shows you in real-time if you’re sticking to your 50/30/20 plan. It does the heavy lifting, so you always know exactly how much you have left to spend or save.

By taking the manual labour out of tracking and analyzing your money, NeoSpend gives you the power to make smarter choices without the stress.

The most important takeaway is that your ideal savings rate is personal. While 20% is a fantastic goal, starting small and being consistent is what truly builds wealth. Automating your savings, even a little, is the key to turning good intentions into real progress.

Ready to stop guessing and start taking control of your finances? Try NeoSpend to get clear insights into your spending and start building a stronger financial future today.