Whenever you search "how much for retirement Canada," you're likely to see some eye-popping headlines. Numbers like $1.7 million get thrown around a lot. It's enough to make anyone a little nervous.

But that single, intimidating number isn't the whole story. The real goal isn't to hit some magic figure—it's to build a reliable stream of income that lets you live the life you want after you stop working. This guide provides clear, practical financial guidance to help you figure out your personal number and create a plan to get there.

What's Your Canadian Retirement Number?

Let's cut through the noise. That massive number you see in the news can feel completely out of reach. But here’s the thing: your retirement number is deeply personal. It's unique to you. The key isn't to chase a generic target but to figure out what you actually need with some simple, trustworthy financial guidance.

A great place to start is with the "70% rule." It’s a simple rule of thumb that suggests you’ll need about 70% of your pre-retirement income each year to keep up your current standard of living. It’s not set in stone, but it gives you a solid ballpark number to start your planning.

So, why 70% and not 100%? The logic is pretty straightforward: many of your biggest expenses will shrink or disappear once you retire.

You stop saving for retirement: That chunk of your paycheque you were diligently putting into your RRSP or TFSA? It’s now freed up to be spent.

Your tax bill gets smaller: With a lower annual income, you'll almost certainly drop into a lower tax bracket.

Work costs vanish: Say goodbye to daily commutes, professional wardrobes, and other expenses that come with a job.

The mortgage is gone (hopefully!): Most Canadians aim to have their mortgage completely paid off by the time they clock out for the last time.

Naturally, this is just a starting point. Your personal spending habits, travel dreams, and future health needs will all play a part in shaping your final number.

How Do Canadians Feel About Their Savings?

It’s clear retirement is on everyone’s mind. A recent BMO survey found that Canadians, on average, think they need $1.7 million to retire comfortably. And with inflation and the rising cost of living, many worry they won't have enough saved.

But people are taking action. The same report noted that average annual RRSP contributions jumped significantly, a clear sign that Canadians are getting serious about closing their savings gap. You can dig into more of BMO's findings on Canadian retirement perspectives on their newsroom.

Understanding where your money is going right now is the first, most critical step in building a realistic plan. This is where a tool like NeoSpend helps people manage money smarter. By automatically tracking your income and spending, NeoSpend gives you the clarity you need to see your full financial picture and start planning for your future with real confidence.

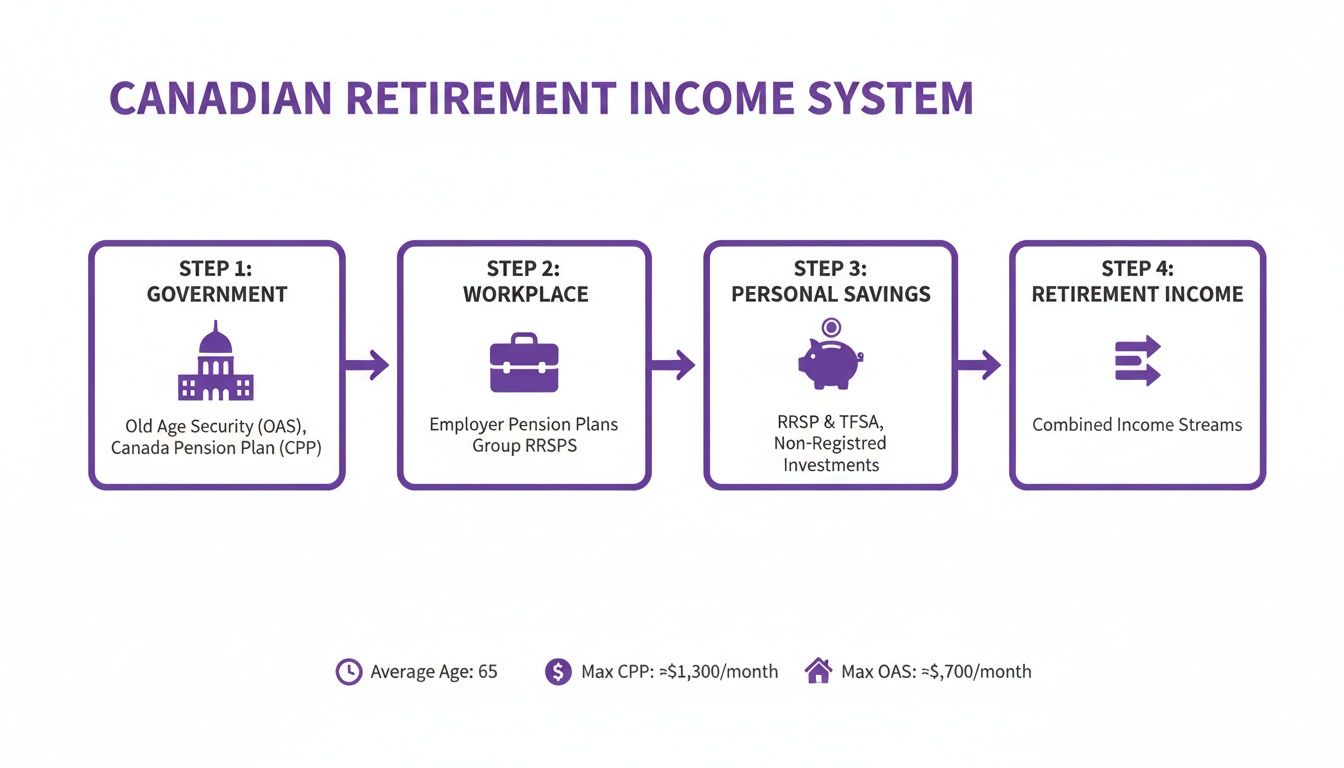

Understanding Canada's Three Pillars of Retirement

When you think about your retirement income, don't picture one giant pot of money. It’s more like a sturdy, three-legged stool. For a stable and comfortable retirement, you need all three legs working together. This clear concept is at the heart of Canadian retirement planning.

Let's break down how these three pillars team up to build your financial future.

Pillar 1: Government Benefits

The first leg of the stool is the foundation provided by the Canadian government. These programs are designed to give every eligible Canadian a baseline income once they stop working. We'll explain these simply.

There are two key programs to know:

Canada Pension Plan (CPP): Think of this as a savings plan you pay into throughout your career. You and your employer both contribute from each paycheque. The more you earn and contribute over the years, the more you get back in retirement.

Old Age Security (OAS): Unlike CPP, OAS isn't tied to your work history. It's a payment that goes out to most Canadians aged 65 and older who meet the residency requirements. It’s a foundational, reliable income stream.

Together, these government benefits create a crucial safety net, ensuring a basic level of financial support for all retirees.

Pillar 2: Workplace Pensions

The second pillar is made up of pension plans offered through your job. If you have one of these, you're in a great position—it’s a structured way to save with a direct boost from your employer.

Workplace pensions typically come in two main flavours:

Defined Benefit (DB) Plans: Your employer promises you a specific, predictable monthly payment for life, calculated from your salary and years of service. They handle the investment risk, so your payout is guaranteed.

Defined Contribution (DC) Plans: You and your employer both contribute a set amount into an investment account in your name. What you end up with depends on those contributions and how the investments perform.

A huge perk with many DC plans or Group RRSPs is the employer match. If your company offers to match your contributions, max it out. It's literally free money and one of the best ways to supercharge your savings.

Pillar 3: Your Personal Savings

The final leg of the stool is the one you build yourself: your personal savings and investments. This is how you bridge the gap between what government and workplace pensions provide and the retirement lifestyle you're actually dreaming of.

This is where accounts like Registered Retirement Savings Plans (RRSPs) and Tax-Free Savings Accounts (TFSAs) become your best friends. They offer powerful tax advantages to help your money grow faster.

Here's a practical example using current figures: The max CPP payout at age 65 will be around $1,433 a month in 2025, and the top OAS payment is $727.67. Meanwhile, the 2025 TFSA contribution room is $7,000, and the RRSP limit is $32,490 (tied to your income). OAS benefits also get "clawed back" if your net income exceeds $93,454 for 2025. You can dig into these numbers and more with the 2025 financial planning facts from The Angus Group.

Seeing how these pillars fit together is key. An app like NeoSpend makes this easier by letting you link all your different accounts into one dashboard. This gives you a bird's-eye view of your entire financial world, making it simple to track your progress toward your retirement goals.

How to Calculate Your Personal Retirement Target

Alright, rules of thumb are a decent start, but now it’s time to get personal. Let's move beyond the averages and figure out your number. This is a simple, step-by-step process to land on a retirement target that actually makes sense for you and provides an actionable insight into your financial future.

We'll walk through it together.

This chart is a great visual summary of how all the pieces of Canada’s retirement income system fit together.

As you can see, building your nest egg is a team effort. It's a mix of government programs, what you get from work, and your own hard-earned savings.

Step 1: Estimate Your Annual Retirement Expenses

First, you need a solid idea of how much you'll be spending each year in retirement. The best way to do this is to look at what you spend now and then adjust it for your future life.

Some expenses will probably vanish (mortgage, commuting), but others could increase (travel, hobbies, healthcare).

This is where an app like NeoSpend becomes a powerful tool. It automatically sorts your current spending into categories, giving you a real-world baseline. From there, you can adjust those categories to paint an accurate picture of your future needs, helping you manage money smarter.

Step 2: Subtract Your Guaranteed Income

Once you have your yearly spending number, it's time to subtract all the income you can count on from other places. This is where those first two pillars of Canadian retirement—government and workplace pensions—come into play.

Tally up the annual income you expect from:

Canada Pension Plan (CPP): Your My Service Canada Account gives you a personalized estimate.

Old Age Security (OAS): The government publishes the current maximum payment amounts, which is a good starting point.

Workplace Pensions: Your plan administrator can provide a statement showing your projected income.

The amount you're left with is what we call your annual income gap. It's the shortfall your personal savings need to cover.

Step 3: Use the Rule of 25

Okay, final step. We need to turn that yearly gap into a total savings target. A straightforward and trusted method for this is the "Rule of 25," which is built on the well-known 4% safe withdrawal rate.

Just multiply your annual income gap by 25. The number you get is a solid estimate of the total nest egg you need to have saved up by retirement day.

Annual Income Gap x 25 = Your Personal Retirement Target

The logic here is that your investments should grow enough to let you safely pull out 4% each year to live on (adjusted for inflation) without depleting your principal. It’s a powerful shortcut to get a real, tangible answer to the "how much is enough?" question.

A Calgary Family Example:

Let's see this in action. Meet the Patels, a couple in Calgary mapping out their future.

Estimate Expenses: After tracking everything, they figure they'll need $60,000 a year for a comfortable retirement.

Subtract Income: They look up their estimates and expect a combined $25,000 per year from CPP and OAS.

Find the Gap: $60,000 (Expenses) - $25,000 (Pensions) = $35,000 (Annual Gap).

Calculate the Target: $35,000 (Gap) x 25 = $875,000.

Just like that, the Patels have a clear, actionable goal. Their target retirement nest egg is $875,000. This number isn't a random figure; it's custom-built for their life and plans.

Choosing Your Savings Tools: RRSP vs. TFSA

Once you have your personal retirement number, the next big question is where to grow that money. In Canada, two accounts are the heavyweights for building wealth: the Registered Retirement Savings Plan (RRSP) and the Tax-Free Savings Account (TFSA). Understanding how they work is a huge part of figuring out how much you need for retirement in Canada.

Instead of drowning in financial jargon, it helps to think of them as two different kinds of investment gardens.

The RRSP Garden: This one gives you a tax break on the seeds (your contributions) you plant now. Everything grows sheltered from tax, but when you harvest in retirement, you’ll pay income tax on your withdrawals.

The TFSA Garden: Here, you use after-tax money to plant your seeds. The magic is that the entire harvest—every dollar of growth and every withdrawal—is yours to keep, completely tax-free, forever.

Nailing down this core difference is the key to picking the right account for you.

When an RRSP Makes the Most Sense

The RRSP is designed to help you save for the future by giving you a tax benefit today. Any money you contribute is tax-deductible, which lowers your taxable income for the year and often results in a tax refund.

This makes the RRSP a no-brainer for Canadians in their peak earning years. If you're in a higher tax bracket now than you expect to be in retirement, the RRSP is a clear winner.

For example, a marketing manager in Toronto making $95,000 a year who puts $10,000 into her RRSP knocks her taxable income down to $85,000. That simple move could save her over $3,000 on her current tax bill, which can then be reinvested.

Why the TFSA Offers Unbeatable Flexibility

The TFSA, on the other hand, is the champion of flexibility. You don’t get an upfront tax deduction, but its tax-free growth and withdrawals make it incredibly powerful.

It's perfect for lower-income earners or anyone just starting their career. If your tax rate is low, the RRSP deduction isn't worth as much. Saving in a TFSA lets your money grow completely tax-free without using up valuable RRSP room that will be more impactful when you're earning more. The TFSA is also amazing for saving for goals other than retirement, like a down payment, since you can withdraw funds tax-free anytime.

So, how do you pick? Most Canadians don't have to.

RRSP vs TFSA At a Glance

These accounts aren't mutually exclusive—in fact, they work best together. This keyword-rich table helps you understand their key differences to build a strategy that fits your life.

| Feature | RRSP (Registered Retirement Savings Plan) | TFSA (Tax-Free Savings Account) |

|---|---|---|

| Contributions | Tax-deductible | Not tax-deductible (made with after-tax money) |

| Contribution Limit | 18% of previous year's earned income, up to an annual maximum | A fixed annual limit set by the government |

| Investment Growth | Tax-deferred | Completely tax-free |

| Withdrawals | Taxed as regular income | Completely tax-free |

| Effect on Govt. Benefits | Withdrawals are considered income and can reduce benefits like OAS and GIS | Withdrawals do not count as income and have no impact on benefits |

| Withdrawal & Re-contribution | Contribution room is lost permanently after withdrawal | Withdrawn amounts are added back to your contribution room the next year |

| Best For... | Higher-income earners; long-term retirement savings | Everyone, especially lower/middle-income earners; flexible savings goals |

A common and effective strategy is to max out your TFSA first, then start filling up your RRSP—especially if your employer offers a matching program. Don't leave free money on the table!

Managing these accounts can feel complex, but this is where a tool like NeoSpend simplifies everything. It helps you manage money smarter by linking all your accounts to one dashboard. You can track contributions and monitor progress toward your retirement goals, ensuring you're making the most of these powerful savings tools.

Actionable Strategies to Boost Your Retirement Savings

Staring at your personal retirement number can feel a bit like looking at the peak of a mountain. It’s intimidating. But closing the gap between here and there is totally doable with consistent, practical steps. This isn't about financial wizardry; it’s about building simple habits that make a massive difference over time.

Here are some real-world ways to get your savings into high gear.

Make Your Savings Automatic

Of all the financial advice out there, pay yourself first is one of the most effective strategies. Don't just save what's left over at the end of the month. Instead, automate it.

Set up an automatic transfer from your chequing account to your RRSP or TFSA for the day after you get paid. This simple trick turns saving from a chore into an effortless habit. Even a small, consistent amount can balloon into a significant sum thanks to the magic of compounding.

Maximize Your Employer RRSP Match

If your employer offers an RRSP matching program, you need to grab it with both hands. This is the closest thing you’ll ever get to free money, and not taking full advantage of it is like turning down a guaranteed return on your investment.

For example, if your employer matches your contributions up to 4% of your salary and you’re only putting in 2%, you're leaving part of your paycheque on the table. Your top priority should be contributing enough to get that full match.

This is especially critical when many Canadians are starting from a tough spot. A recent 2025 Canadian Retirement Survey revealed that a staggering 36% of Canadians have less than $5,000 in savings, and 20% have no savings at all. These numbers drive home how vital every savings tool—especially an employer match—is.

Find Hidden Savings with Smart Budgeting

Your monthly budget is hiding more cash than you think. Small, unnoticed leaks can add up to a lot of money. The trick is simply getting a clear view of where every dollar is going.

A good budgeting app becomes your best friend. By linking your accounts, you get an instant look at your spending habits and can easily spot opportunities to save more.

Forgotten Subscriptions: Do you have streaming services or apps you forgot about? An app will flag those recurring charges.

Spending Creep: Are you spending way more on takeout than you realize? Seeing the actual numbers can be a powerful wake-up call.

Better Deals: Could you be paying less for your phone bill or home insurance? Identifying your biggest expenses is the first step to shopping around.

Tools like NeoSpend are built for exactly this. It automatically sorts your transactions, tracks bills, and gives you a clear dashboard of your financial life. That clarity helps you find those hidden dollars and redirect them toward your retirement goals, turning small changes into a huge boost for your savings.

Your Next Steps on the Path to Retirement

Figuring out how much you need for retirement in Canada can feel overwhelming, but it's not about nailing one massive, scary number. It’s a personal journey—one that involves getting honest about the lifestyle you want, understanding where your money will come from, and making a solid plan to close any gaps.

The goal is to trade anxiety for clarity and actionable insights.

We’ve broken down the big stuff: the 70% rule, Canada’s three retirement pillars (CPP/OAS, workplace pensions, and personal savings), and how to choose between an RRSP and a TFSA. You now have real strategies to start boosting your savings.

Helpful Takeaway

The most important thing to remember is that planning for retirement isn't a "set it and forget it" task. It's a living process. Life happens, and your plan will need to adapt. The single most powerful first step is getting a crystal-clear picture of where your money is going right now. A solid grip on your current finances is the foundation for everything else.

This is where a tool like NeoSpend can be a game-changer. It pulls all your accounts together and tracks your spending automatically, giving you a complete, real-time view of your financial life in one spot. By following the steps in this guide and using smart tools to stay on track, you’re not just chasing a random number; you’re building a realistic target and a clear roadmap to get there.

Common Questions About Retiring in Canada

Figuring out retirement brings up a lot of questions. It's totally normal. Let's walk through some of the big ones that pop up for Canadians trying to pin down their magic number.

What is a good retirement savings rate for Canadians?

You’ll often hear the 10% to 15% rule—save that much of your pre-tax income. Think of it as a solid starting block, not the finish line. If you start in your 20s, 10% might do the trick. But if you’re getting a later start or have big dreams for retirement, you’ll probably want to push that closer to 15% or even higher.

Can I actually retire on just CPP and OAS in Canada?

For almost everyone, the answer is no. Relying only on the Canada Pension Plan (CPP) and Old Age Security (OAS) won't be enough to maintain the lifestyle you're used to. These government benefits are a fantastic safety net, but they're designed to cover the basics. In 2025, the combined maximum is around $2,161 a month, or just under $26,000 a year. For most people, that’s a huge pay cut, which is why your own savings are so incredibly important.

How do I factor in inflation and market growth for my retirement plan?

Inflation is the sneaky force that makes your money worth less over time. Your savings need to outrun it. This is why simply stashing cash isn't enough; you need to invest it. The good news is that smart planning already has this covered. The 'Rule of 25', for example, is built on the idea that your investments will deliver a conservative return after inflation, allowing you to withdraw about 4% each year without running out of money.

What’s the best way for self-employed Canadians to save for retirement?

When you're self-employed, there’s no company pension or employer match, so saving is 100% on you. This makes an RRSP your best friend. Every dollar you contribute lowers your taxable income, which is a huge win. The key is to create your own "paycheque deduction" by setting up automatic, recurring transfers to your RRSP and TFSA. It mimics the discipline of a traditional workplace plan.

Getting a handle on these questions starts with knowing where your money is going today. NeoSpend pulls all your accounts into one simple view, so you can see the full picture, track your progress, and build that retirement fund with confidence.