So, how much can you really put in your TFSA? The answer isn't a single number—it’s a personal limit that grows with you, year after year.

For 2024, the annual contribution limit is $7,000. But that’s just this year's piece of the puzzle. The real power of the TFSA is that any unused contribution room from previous years carries forward indefinitely, meaning your total available space is probably a lot higher.

Understanding the Annual TFSA Contribution Limits

Think of your TFSA contribution room like a bucket you can fill up over time. Every year you’re eligible, the government adds a little more space to it. Your personal limit is the total of all those annual additions, minus whatever you've already put in.

This system is designed to be flexible. Life happens, and you might not have extra cash to contribute every single year. The good news? You don't lose that space. It just rolls over, waiting for you whenever you’re ready to catch up. This cumulative feature is what makes the TFSA such a powerhouse for building wealth at any age.

The Official Annual Limits Since 2009

To figure out your total lifetime contribution room, you need to know the annual limit for every year since you turned 18 and had a valid Social Insurance Number (SIN). These limits have changed over the years, adjusted for things like inflation or government policy.

For example, while the TFSA limit for 2024 is $7,000, back when the program first launched in 2009, it was just $5,000. You can find more details on the TFSA limit history to see how it's evolved.

To get a clear picture, here’s a quick breakdown of the official limits since day one.

Annual TFSA Contribution Limits By Year

This table breaks down the annual TFSA dollar limit set by the Canadian government since 2009. You can use it to calculate your total accumulated contribution room.

| Year | Annual TFSA Limit |

|---|---|

| 2009–2012 | $5,000 |

| 2013–2014 | $5,500 |

| 2015 | $10,000 |

| 2016–2018 | $5,500 |

| 2019–2022 | $6,000 |

| 2023 | $6,500 |

| 2024 | $7,000 |

By adding up the limits for each year you were eligible, you can get a solid estimate of your total room.

Key Takeaway: If you were 18 or older in 2009 and have never contributed a single dollar to a TFSA, your total contribution room as of 2024 would be a whopping $95,000.

Knowing these annual figures is the first step, but trying to track contributions across different accounts can be a pain. A smart money management tool like NeoSpend can help. By seeing all your finances in one place, you get the clarity you need to make smarter decisions about how much to contribute and when, helping you stay on track with your goals.

How Your Personal TFSA Contribution Room Works

Think of your TFSA contribution room less like a static piggy bank and more like an accordion—it expands every year. The total amount you can put into a TFSA is unique to you, and it’s based on more than just this year's limit. It’s a cumulative total that grows right along with you.

Understanding how this works is the secret to maximizing your tax-free growth potential. It all boils down to three key parts.

The Three Pillars of Your Contribution Room

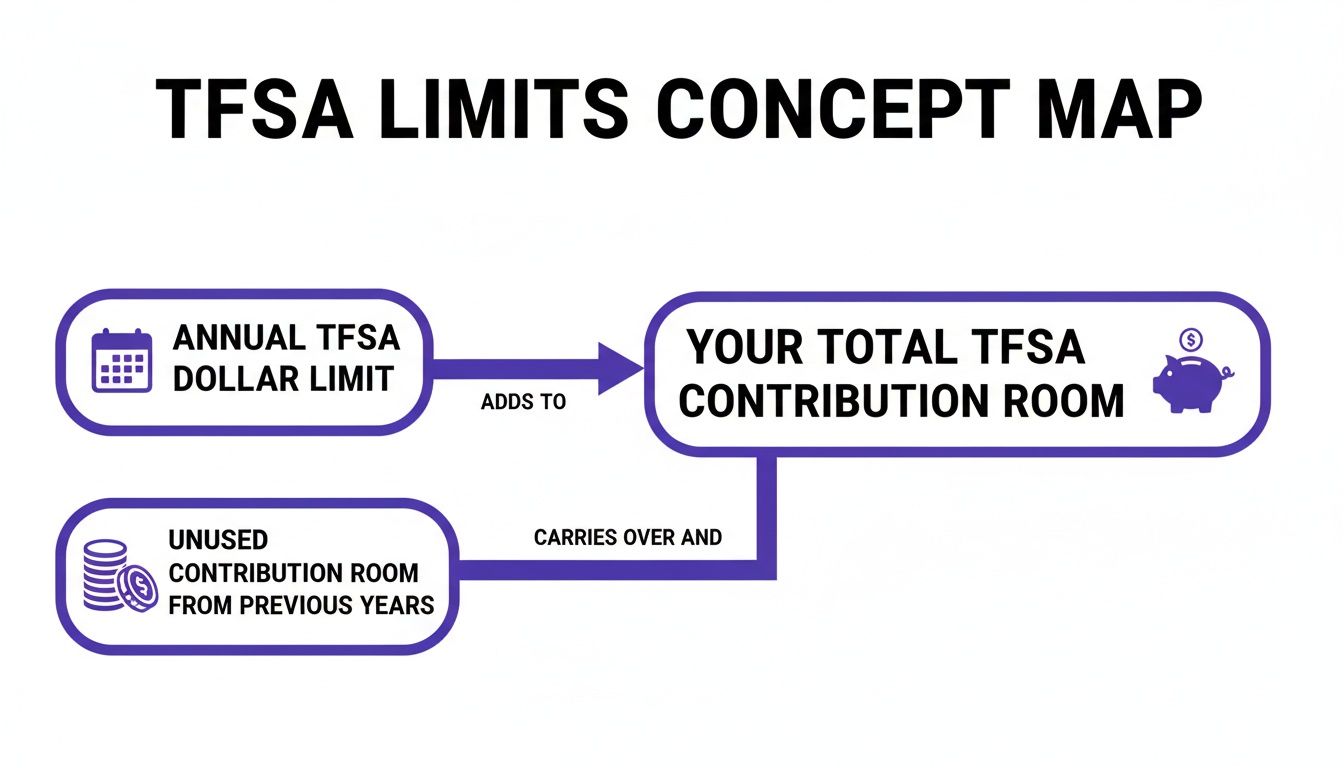

Your personal limit is calculated by adding three things together. This system ensures you never lose out on contribution space, even if you have a year where you can't save much.

Here's the simple formula:

- The annual TFSA limit for the current year. For 2024, that’s $7,000.

- All your unused contribution room from previous years. Any space you didn't use in the past carries forward indefinitely. No "use it or lose it" here.

- The total amount of any withdrawals you made last year. This is a powerful feature. When you take money out, that exact amount gets added back to your contribution room the following January.

This concept map breaks down how the annual limit and your unused room combine to create your total contribution space.

As you can see, your total available room is much more than a single year's limit; it's a lifetime accumulation of every dollar you've been eligible to contribute since you turned 18.

An Analogy to Make It Simple

Let’s try a different way to think about it. Imagine your TFSA room is a water bottle.

Every year, the government makes your bottle a little bigger (the annual limit). If you only fill it halfway one year, that empty space doesn’t just vanish—it’s still there, waiting for you.

Now, if you decide to drink some of the water (make a withdrawal), that space opens up again. The catch? You have to wait until the start of the next year to refill that specific part. It’s a dynamic system that adapts to your savings habits and life events.

Your Personal TFSA Limit = (This Year's Limit) + (All Past Unused Room) + (Last Year's Withdrawals)

Manually keeping tabs on contributions and withdrawals, especially if you have TFSAs at different banks, can get messy. This is where a tool like NeoSpend becomes a financial lifesaver. It pulls all your accounts into one dashboard, giving you a clear, real-time view of your transactions. This helps you track what you’ve put in without the tedious guesswork, so you can avoid accidentally going over your limit.

Calculating Your TFSA Room with Real-Life Examples

Knowing the rules for your TFSA contribution room is one thing, but seeing how they play out in everyday Canadian scenarios is where it all clicks. Let’s walk through three common examples to see how the math works in real life.

Example 1: The First-Time Contributor

Meet Maya, a 22-year-old recent grad from Calgary. She turned 18 in 2020 but hasn't opened a TFSA yet. To figure out her total contribution room for 2024, we just add up the annual limits for every year since she’s been eligible.

It’s a simple tally:

- 2020: $6,000

- 2021: $6,000

- 2022: $6,000

- 2023: $6,500

- 2024: $7,000

Maya’s total accumulated contribution room in 2024 is $31,500. She can put that entire amount into a new TFSA anytime without worrying about penalties.

Example 2: The On-and-Off Saver

Now, let's look at David, a 40-year-old from Toronto who opened his TFSA in 2018. Heading into 2024, his total lifetime contribution room was $46,500. He’s contributed a total of $25,000 over the years and has never taken any money out.

His calculation is straightforward:

- Lifetime Room (start of 2024): $46,500

- Total Contributions Made: -$25,000

- Unused Room from Past Years: $21,500

- 2024 Annual Limit: +$7,000

David’s total available contribution room for 2024 is $28,500. That’s how much more he can add to his TFSA this year.

Remember, every Canadian's TFSA limit is unique. It’s crucial to track your personal contributions and withdrawals to know your exact room and avoid penalties. This is where the NeoSpend dashboard comes in handy, letting you see all your account activity in one place.

Example 3: The Home Buyer Who Made a Withdrawal

Finally, meet Chloe from Vancouver. She’s been a diligent saver. At the start of 2023, she had maxed out her $88,000 of available TFSA room. But in June 2023, she withdrew $50,000 for a down payment on a condo.

Here’s how we figure out her 2024 room:

- Unused Room from Previous Years: $0 (since she was maxed out)

- Withdrawal Amount from 2023: +$50,000 (this full amount is added back on Jan 1, 2024)

- 2024 Annual Limit: +$7,000

Chloe’s new TFSA contribution room for 2024 is $57,000. She now has the space to start rebuilding her savings by re-contributing the money she took out, plus this year's new limit.

The One TFSA Mistake You Can't Afford to Make

The TFSA is wonderfully flexible, but there’s one rule you don’t want to break: the contribution limit. Going over that limit is a surprisingly common mistake, and it can get expensive, fast. The Canada Revenue Agency (CRA) watches this closely, and the penalty can eat into your savings before you even realize it.

The consequences are serious. If you over-contribute, you’ll get hit with a penalty tax of 1% per month on the highest excess amount during that month. This isn't a one-time fee; the tax keeps getting applied every single month until you fix the problem.

How Quickly Over-Contribution Penalties Add Up

Let's break it down. Say you miscalculate and put $5,000 too much into your TFSA in February. That’s a penalty of $50 for the month (1% of $5,000).

If you don’t catch it, the meter keeps running. You’ll be dinged another $50 for March, $50 for April, and so on. Left unchecked for a full year, that simple mistake could cost you $600 in penalties—money that could have been growing, tax-free.

Heads Up: The 1% penalty is calculated on the highest excess amount in your TFSA during the month. Even if you pull the money out mid-month, you’re still taxed for that entire month based on how much you were over at the peak.

How to Fix an Over-Contribution

Realizing you've put in too much is stressful, but don't worry—there's a straightforward fix. If you act quickly, you can minimize the damage.

Here’s exactly what to do:

- Withdraw the Excess Amount Immediately. The moment you spot the error, take out the exact over-contributed amount. This stops the penalty clock for all future months.

- Contact the CRA. The CRA will likely send you a proposed TFSA return flagging the over-contribution and the penalty you owe. You'll have to file a Form RC243, Tax-Free Savings Account (TFSA) Return, to report the situation and calculate the tax.

- Pay the Penalty. Settle the amount you owe as soon as you can to avoid any extra interest charges.

Proactive management can save you this headache. This is where an app like NeoSpend can be a game-changer. It helps you see all your financial transactions in one place, making it simple to track your TFSA deposits in real-time. It’s like having a financial co-pilot, helping you steer clear of these costly mistakes altogether.

How to Find Your Official TFSA Contribution Room

While tracking your contributions yourself is the best way to know your limit in real-time, the Canada Revenue Agency (CRA) is the official source of truth. Checking your number with the CRA is a smart way to double-check your own math and ensure you're on the right track.

Checking Your Limit Through CRA My Account

The easiest way to get the official number is through the CRA’s online portal, My Account for Individuals.

It's pretty straightforward:

- Log in to your CRA My Account.

- Navigate to the “RRSP and Savings Plans” section.

- Click on “Tax-Free Savings Account (TFSA)”.

- You’ll see your “TFSA contribution room as of January 1” for the current year.

This figure includes the new annual limit, any room you didn’t use in previous years, and any withdrawals you made last year.

One big catch: The number on the CRA website isn't live. Financial institutions only report TFSA transactions once a year, so there’s a major delay. Any money you’ve put in or taken out this year won’t be reflected in that number.

Using the MyCRA Mobile App

If you’re on the go, the MyCRA mobile app offers a quick snapshot. Once you log in, you can find your TFSA contribution room just as easily. It shows the exact same figure as the desktop site, making it perfect for a quick check-in.

Because of the reporting lag, treat the CRA’s number as a trusted baseline, not your current balance. This is where a personal finance tool like NeoSpend truly shines. By linking your accounts, NeoSpend gives you an up-to-the-minute view of your transactions. You can see every TFSA deposit the moment it happens, closing the information gap left by the official reporting delays. That way, you always know exactly how much room you have left.

Why the TFSA Is a Canadian Savings Superstar

The Tax-Free Savings Account has become more than just another place to stash cash—it has fundamentally changed how Canadians approach building wealth. Its combination of flexibility and tax-free growth has made it the MVP for smart savers across the country.

Unlike a regular savings account where you pay tax on interest, or an RRSP where you're taxed on withdrawals, the TFSA lets your investments grow completely tax-free. That means every dollar of growth—from interest, dividends, or capital gains—is all yours. This is a massive advantage that helps your money compound much faster.

A Modern Tool for Every Financial Goal

The TFSA’s real magic lies in its versatility. You can use it for almost any financial goal without facing penalties.

- Emergency Fund: Keep your rainy-day fund accessible while it grows tax-free.

- Major Purchases: Saving for a car, a down payment on a home, or that dream trip? A TFSA can help you get there faster.

- Retirement Savings: It’s an incredible partner to your RRSP. You can pull money out in retirement without it affecting your government benefits or paying a cent of tax.

This flexibility is why it's become so popular. By 2020, Canadians were putting more money into TFSAs than anywhere else, making up 54.8% of all contributions to registered savings plans, as noted in a study on household financial assets. This shift shows that Canadians are embracing the TFSA's power.

The TFSA isn’t just an account; it’s a modern financial strategy. It’s designed to let you save for short-term needs and invest for long-term growth, all under one tax-free roof.

Managing this superstar account deserves a modern approach. Using a tool like NeoSpend lets you see all your accounts in one dashboard, making it simple to track your contributions and watch your savings grow. It gives you the clarity you need to make the smartest moves with your money.

Your Top TFSA Questions, Answered

We’ve covered the details, but a few questions always come up when Canadians talk about TFSAs. Let's tackle them head-on.

What Happens if I Don’t Contribute in a Given Year?

Absolutely nothing bad happens. If you skip a contribution for a year (or several), you don't lose that room. It simply rolls over and gets added to the next year's limit, accumulating indefinitely. This is one of the TFSA's best features—you can always catch up later.

Can I Re-Contribute Money I Withdrew?

Yes, you can. Any money you take out of your TFSA gets added back to your contribution room. But timing is everything. That room only becomes available again at the start of the next calendar year. So, if you pull out $5,000 this year, you must wait until January 1st of next year to put it back in (unless you already have other unused contribution room available). Re-contributing in the same year is a common way people accidentally over-contribute.

Does Investment Growth Affect My Contribution Room?

Nope! This is where the TFSA really shines. Any growth your money makes inside the account—from stocks, interest, or other investments—is completely tax-free and has zero impact on your contribution limit. The government only tracks what you put in, not what it grows into. This lets your money compound without being eroded by taxes, helping you build wealth faster.

The Takeaway: Your TFSA contribution room is a personal, cumulative limit that grows every year. The key to maximizing its benefits is to track your contributions and withdrawals carefully to avoid penalties.

Ready to manage your money smarter? See everything NeoSpend has to offer and take control of your financial future today.