Improving your credit score in Canada boils down to a few powerful habits. Pay your bills on time, keep your credit card balances low, and show lenders you can be trusted over the long run. Master these basics, and you’ll be on your way to better interest rates and achieving your biggest financial goals.

Why Your Credit Score Matters in Canada

Picture this: you're a young professional in Toronto, diligently saving for a down payment on a condo, only to find out a surprisingly low credit score is standing between you and a mortgage pre-approval. It’s a scenario that plays out across the country. Your credit score isn’t just a random number; it’s a snapshot of your financial reliability that lenders, landlords, and even some employers use to assess you.

In Canada, your financial activities are tracked by two major credit bureaus: Equifax and TransUnion. They collect information from your creditors (like banks and credit card companies) to create your credit report, which generates a score typically ranging from 300 to 900. The higher your score, the more trustworthy you appear to lenders.

The Real-World Impact on Your Wallet

A healthy credit score is your VIP pass to major financial milestones. It directly influences the deals you'll get on almost everything. For example, someone with a 760 score might secure a car loan at 4% interest. Meanwhile, another person with a 620 score could be offered the same loan at 11%—a difference that costs thousands of extra dollars over time.

A good score makes a real difference:

- Better Interest Rates: You'll land lower rates on mortgages, car loans, and lines of credit, which means more money stays in your pocket.

- Easier Approvals: Lenders are more willing to approve your applications for new credit cards and loans.

- Higher Credit Limits: Proving you can handle credit responsibly often leads to higher limits, which can help improve your score.

- More Rental Options: Landlords often check credit reports. A strong score can put you at the top of the list for that perfect apartment in a competitive market.

The Building Blocks of Good Credit

Improving your score isn't about complex financial wizardry; it's about mastering a few core habits. Nail these, and you're building a stronger financial foundation for your future.

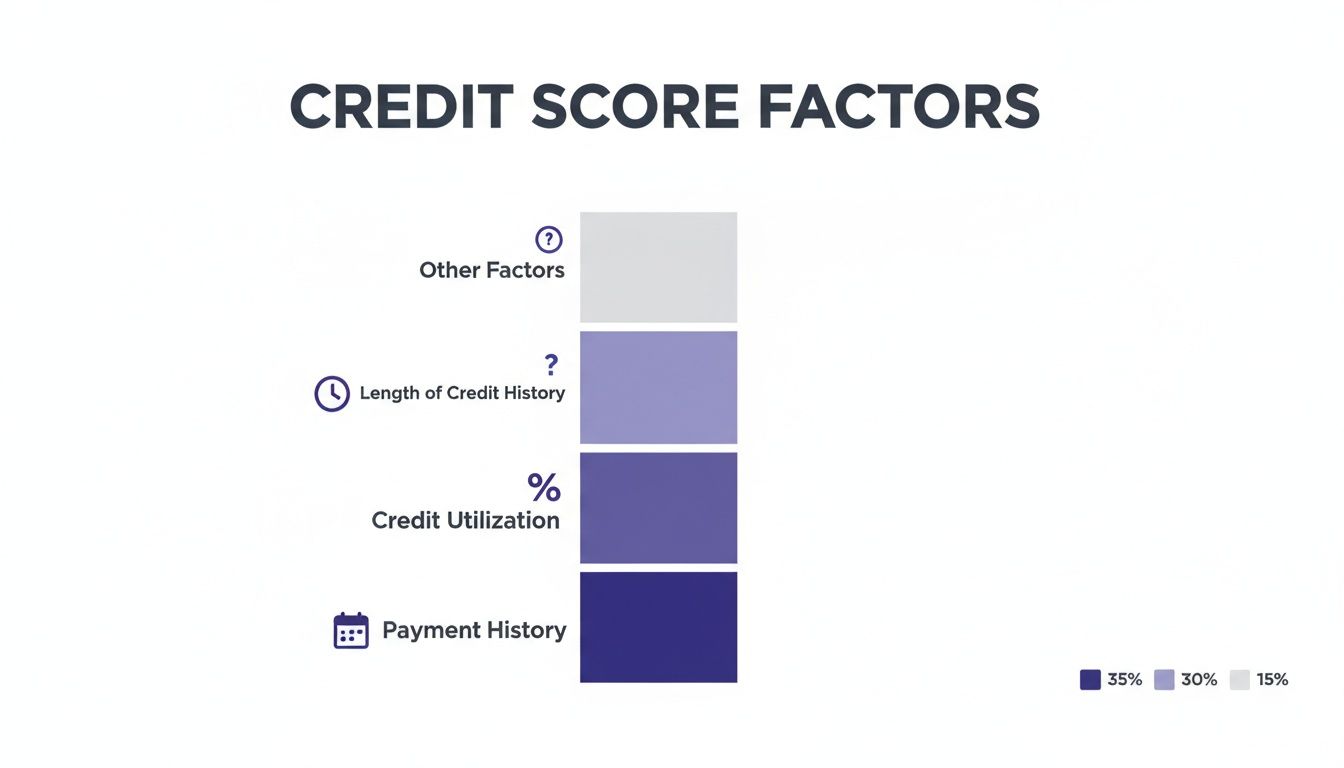

Your payment history is the most important factor—it makes up about 35% of your score. Nothing builds trust with lenders faster than a long, consistent record of paying your bills on time, every time.

Another critical piece is keeping your credit card balances low. A good rule of thumb is to use less than 30% of your available credit limit. Finally, time is your ally. A long, positive credit history demonstrates that you have experience managing credit responsibly.

This is where smart tools make all the difference. An app like NeoSpend helps you manage money smarter by putting all your accounts into one clear view. When you can see your balances, bills, and spending habits at a glance, you’re in a much better position to stay on track and make informed decisions.

Your First Step: Check Your Credit Report

Before you can start making improvements, you need to know exactly where you stand. Think of it as a financial health check-up. Your first move should be to get your credit reports from both of Canada's main credit bureaus, Equifax and TransUnion.

You're legally entitled to a free copy of your report from each bureau by mail at least once a year. Many Canadians also use free online services to monitor their credit regularly, which is a fantastic way to keep an eye on your financial health without affecting your score.

What to Look For Beyond the Score

Once you have your reports, it's time to review them carefully. Don’t just glance at the three-digit score. Comb through every detail, line by line. You’d be surprised how often errors pop up, and they can unfairly drag your score down.

Keep an eye out for these specific red flags:

- Accounts You Don't Recognize: This could be a simple mix-up, but it could also be a sign of identity fraud. If you spot a credit card or loan you never opened, you need to act immediately.

- Incorrect Personal Information: Ensure your name, address, and SIN are all listed correctly. Even a small typo can cause reporting problems.

- Late Payments That Were Actually On Time: This is a big one. A single incorrectly reported late payment can do serious damage to your score. Lenders look for consistency, and a mistake like this breaks that pattern.

- Duplicate Accounts: Sometimes a single debt gets listed twice by mistake. This can throw off your credit utilization ratio and make your overall debt look larger than it is.

Imagine a freelancer from Vancouver who pulls her report and finds a late payment from her telecom provider. She knows she paid it on time and has the bank statement to prove it. That one error could be the difference between getting approved for a new business loan or being turned away.

How to Dispute Errors and Fix Your Report

Finding an error is step one; getting it corrected is the real work. Both Equifax and TransUnion have formal dispute processes you can follow to set the record straight.

The process typically involves submitting a form that details the error and attaching any proof you have. For instance, if you're disputing a late payment claim, a bank statement showing the on-time transaction is your best evidence. This is where a tool like NeoSpend becomes incredibly useful. You can easily search your transaction history to pinpoint exact payment dates and amounts, giving you the hard proof needed to build a strong dispute case.

Correcting even a small mistake on your credit report can give your score a significant boost. It's one of the most direct ways to improve your credit score because you're removing inaccurate negative information that shouldn't be there.

Don't underestimate the power of a clean, accurate report. By making this check-up a regular habit—at least once a year—you ensure your score is a true reflection of your financial responsibility. That’s the foundation for any plan to improve your credit.

Master On-Time Payments for a Stronger Score

When it comes to your credit score, nothing is more important than your payment history. It's the first thing lenders check, and it tells them one simple thing: can they count on you to pay them back on time?

Think of it as building a reputation. Every on-time payment is a vote of confidence. A single late one is a red flag. This one habit is so critical that it makes up about 35% of your total score, carrying more weight than any other factor.

Automate Your Bills to Avoid Missed Payments

Life gets busy, and it's easy for a due date to slip by. Imagine a family in Calgary juggling a mortgage, a car payment, a few credit cards, and multiple streaming subscriptions. Forgetting just one of those bills is an honest mistake, but the ding to their credit score can be painful and last for years.

The single best strategy to avoid this is automation. Set up automatic payments for all your recurring bills—like your car loan, mortgage, or phone bill. This takes human error out of the equation.

Paying on time, every time, is the absolute foundation of a great credit score. As experts at Experian confirm, your payment history accounts for a huge 35% of your score. If you can establish 6 to 12 months of perfect on-time payments, you're showing lenders exactly what they want to see. This is especially powerful if you're recovering from past late payments.

For credit cards and other bills where the amount changes, a great safety net is to automate at least the minimum payment. That way, you’re never officially late. You can always log in before the due date and pay off the rest of the balance yourself.

Use Reminders and Smart Tools as a Backup Plan

Even with automation, it’s smart to have a backup. A simple calendar alert on your phone a few days before a bill is due can be a lifesaver. It’s a helpful nudge to ensure you have enough cash in your account to cover the payment.

This is where a tool like NeoSpend feels like your financial command centre. Instead of juggling multiple banking apps and websites, NeoSpend brings all your upcoming bills into one place.

It helps you manage money smarter by:

- Tracking all your due dates: See every bill and subscription in one clean, simple view.

- Sending helpful reminders: Get a heads-up so a payment never catches you by surprise.

- Preventing missed payments: By keeping everything front and centre, you can make sure nothing falls through the cracks.

This level of organization is invaluable for building the solid, positive payment history that lenders love to see.

The Timeline for Rebuilding Trust with Lenders

If late payments have hurt your score in the past, don't lose hope. The path to recovery is paved with consistency. Lenders care far more about your recent actions than what you did two years ago.

Once you establish a solid pattern of on-time payments for 6 to 12 months, you effectively start overwriting that old negative history. This steady, positive behaviour proves you’ve built better habits and rebuilds that crucial trust with creditors. It's not a quick fix, but it's the most powerful way to improve your credit score for the long haul.

Lower Your Credit Utilization for a Quick Boost

While your payment history is the long game in building credit, managing your credit utilization ratio (CUR) is your power play. It's one of the few factors you can change quickly, often delivering some of the fastest improvements to your credit score.

Your CUR is simply the percentage of your available credit that you’re currently using. Lenders see a high ratio as a red flag—a potential sign of financial stress. On the other hand, a low ratio tells them you’re managing your debt comfortably.

Keeping this number below 30% is the golden rule for great credit health.

Understanding the 30% Rule

So, what does this look like in a real Canadian scenario?

Imagine you have a single credit card with a $5,000 limit. To stay under the 30% threshold, you'd want to keep your balance below $1,500. If you have multiple cards, the same principle applies to your total available credit versus your total balances.

This chart breaks down the most important parts of your credit score, and you'll see credit utilization is a huge piece of the puzzle.

As you can see, the amount of credit you use is second only to your payment history, which shows just how much direct control you have over this factor.

Actionable Ways to Lower Your Ratio

Getting your CUR down is a powerful strategy. Take a student in Montreal who maxed out their credit card on textbooks and living expenses. By creating a plan to pay down that balance aggressively, they could see their score jump in just one or two billing cycles.

Here are a few practical ways to lower your utilization:

- Make multiple payments a month. Instead of one large payment on the due date, try making smaller payments throughout the month. This keeps your reported balance lower when your card issuer sends a snapshot to the credit bureaus.

- Pay before your statement date. The balance on your statement closing date is often what gets reported. Paying off a large chunk before this date can make a huge difference.

- Focus on high-balance cards first. If you have multiple cards, concentrate on paying down the one with the highest utilization ratio to make the biggest impact.

The results can be significant. Financial experts agree that lowering your credit utilization is often the fastest way to a better score. We've seen it firsthand—people who dropped their utilization from 90% down to under 30% have seen their scores increase by as much as 70 points in a single month.

A unified dashboard like NeoSpend gives you a real-time view of all your balances, making it easy to see your credit utilization across all accounts at a glance. This clarity is crucial for staying on top of your balances and making strategic payments.

The table below breaks down how lenders generally view different utilization levels. It's a good guide for understanding where you should aim to be.

Credit Utilization Ratio Impact on Your Score

| Utilization Ratio | Risk Level | Potential Impact on Score |

|---|---|---|

| 0% - 9% | Excellent | This is the ideal range, showing you use credit responsibly without relying on it. Lenders love this. |

| 10% - 29% | Good | A healthy and responsible range. You're well within the recommended limit and look like a low-risk borrower. |

| 30% - 49% | Fair | This starts to raise a few eyebrows. Lenders may see this as a sign of potential financial strain. |

| 50% - 74% | High | Considered risky. High utilization can significantly lower your score as it suggests you're overextended. |

| 75% - 100% | Very High | This is a major red flag for lenders and can severely damage your credit score. |

Aiming for that "Excellent" or "Good" category is your best bet for a healthy score.

Use Technology to Your Advantage

Knowing where you stand is half the battle. NeoSpend, for example, can analyze your spending habits to find areas where you might be able to cut back. By spotting opportunities to save, you can free up more cash to pay down debt and systematically lower your utilization ratio, month after month.

Build a Diverse and Long-Lasting Credit History

While fixing your payment habits and credit utilization can deliver quick wins, a truly solid credit score is built on a diverse and long-standing credit history. From a lender's perspective, they want to see that you can responsibly handle different kinds of debt over the long haul.

A healthy credit profile has a good mix of credit types. The two main categories are:

- Revolving Credit: This is credit you can use and repay repeatedly, like a credit card or a line of credit.

- Installment Loans: This is debt with a fixed end date where you make regular payments, like a car loan, mortgage, or personal loan.

Successfully managing both types of credit shows lenders you have the financial discipline to handle different commitments—a huge trust signal that boosts your score.

Why Credit History Length and Variety Matter

The length of your credit history makes up about 15% of your score. A longer history gives lenders more data, painting a clearer picture of your reliability.

This is why you should think twice before closing your oldest credit card, even if you don't use it. That account is the anchor of your credit age. Closing it can shorten your credit history and cause your score to dip.

If you're new to Canada or rebuilding your credit, this can feel like a catch-22: how do you build a history if no one will give you credit? A secured credit card from a Canadian bank or credit union is a fantastic first step. You provide a small security deposit, which becomes your credit limit. It's a low-risk way to prove you can handle credit and start building that positive payment history.

Get Credit for Bills You Already Pay

One of the smartest ways to build your credit file is to get recognized for payments you’re already making on time, like rent. Reporting your rent payments to the credit bureaus can be a game-changer, especially for those who are "credit invisible."

When rent payments are added to credit reports, TransUnion found in a 2021 study that people saw their scores jump by an average of 60 points. You can see for yourself the impact of rent reporting on credit scores.

By using a mix of credit, keeping old accounts open, and using smart strategies like rent reporting, you’re not just playing defence. You're actively building a strong financial reputation that will open doors for you down the road.

Ultimately, building a diverse and lasting credit history is all about telling a story of long-term reliability. It shows you’re a consistent, responsible borrower, which is exactly what lenders are looking for.

Your Top Credit Score Questions Answered

Even with a solid game plan, you might still have a few questions. Let's tackle some of the most common things Canadians ask when working to improve their credit.

How Long Does It Take to Improve My Credit Score?

Patience is key, but you won't be waiting forever. If you're focused on lowering high credit card balances, you could see a positive bump in your score in as little as 30 to 60 days after you pay them down.

For bigger fixes, like recovering from missed payments, you’ll need to demonstrate consistency. Expect to show 6 to 12 months of solid, on-time payment history before your score truly starts to reflect that positive change. Building great credit is a marathon, not a sprint.

Will Checking My Own Score Hurt It?

No, not at all. This is a common myth. Checking your own credit report or score is a "soft inquiry" and has zero impact on your score. In fact, it’s one of the best financial habits you can build.

A "hard inquiry" is what can cause a small, temporary dip. This happens when a lender pulls your report because you've applied for new credit, like a loan or credit card.

Should I Close My Old, Unused Credit Cards?

It’s tempting, but it's almost always better to keep them open. Closing an old credit card can backfire in two ways. First, you lose that card's credit limit, which can cause your overall credit utilization ratio to increase. Second, you erase a piece of your credit history, which shortens the average age of your accounts.

A better strategy is to keep old, no-fee cards open. Just use them for a small purchase every few months to ensure the issuer doesn't close the account for inactivity.

Think of your oldest credit accounts as the foundation of your financial history. A longer history shows lenders you have experience managing credit responsibly. Closing them is like knocking out a support beam—it’s not worth the risk.

Can Paying My Cell Phone Bill Help My Credit Score?

In Canada, your regular, on-time payments for utilities like your cell phone or hydro bill are not typically reported to the credit bureaus. So, unfortunately, they don't help build your score.

However, there's a catch: if you don't pay those bills and the account is sent to a collections agency, that negative mark will absolutely show up on your credit report and can cause serious damage. So, while they don't help your score, they can definitely hurt it.

Key Takeaway: Improving your credit score is an achievable goal. By consistently paying bills on time, keeping your credit card balances low, and regularly checking your credit report for errors, you can build a stronger financial future.

Ready to take control of your finances? With NeoSpend, you can see your spending, bills, and credit progress all in one place, making it easier to put these strategies into action. Get started with NeoSpend and begin making smarter money moves today.