The dividend yield formula is one of the most straightforward yet powerful tools in a Canadian investor's toolkit. At its core, it tells you how much income a company pays out in dividends each year relative to its stock price.

Think of it like the interest rate on a savings account, but for your stocks. It’s a simple percentage that cuts through the noise and shows you the income-generating potential of an investment, helping you make smarter financial decisions.

What Is Dividend Yield and Why It Matters for Canadians

Let's use a simple analogy. When you put money into a high-interest savings account, the bank pays you a set percentage every year. The dividend yield is the stock market equivalent. It’s a quick snapshot of the cash flow a company sends back to you, the shareholder, for every dollar you have invested.

This single number makes it incredibly easy for Canadian investors to compare the income potential of different stocks. For example, a stock with a 4% dividend yield is essentially paying you $4 in annual cash for every $100 you’ve put into it. This makes it a go-to metric for anyone focused on building a reliable stream of passive income.

Building Your Financial Goals

For Canadians planning for the long haul, understanding dividend yield isn't just a "nice-to-have"—it's a game-changer. It helps you strategically build your portfolio to hit your personal financial goals.

- Tax-Free Income: When you hold dividend-paying stocks inside a Tax-Free Savings Account (TFSA), all that dividend income can grow completely tax-free. This is a powerful way to generate income without giving a cut to the CRA.

- Compounding Growth: Inside a Registered Retirement Savings Plan (RRSP), those dividends can be automatically reinvested to purchase more shares, kick-starting the powerful engine of compounding growth for your retirement nest egg.

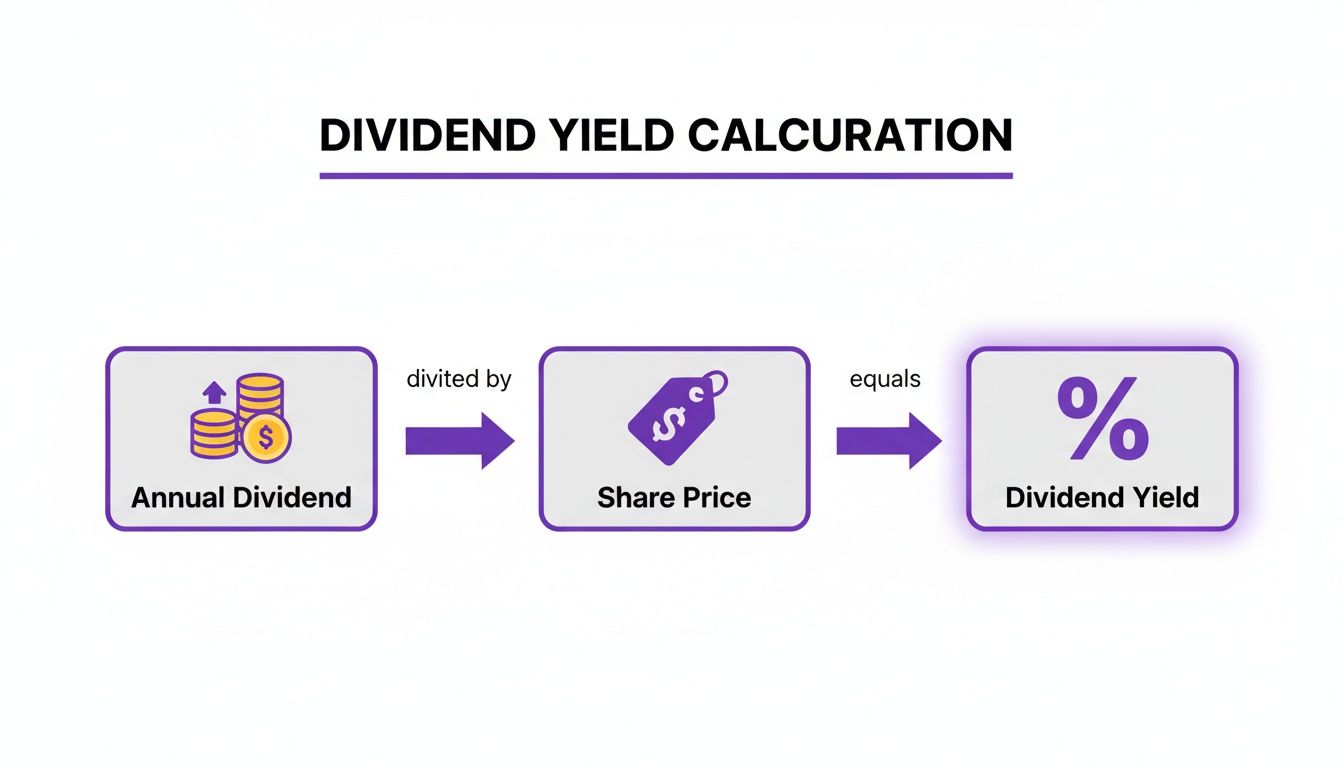

The formula is simply a company's annual dividend per share divided by its current share price. It's a quick calculation that helps Canadians see exactly how much their investments are paying them. If you want to see this in action, check out some charts on how dividend yields are tracked in Canada.

By keeping an eye on your portfolio's dividend yield, you get a real-time pulse on its income-generating power. That clarity is what empowers you to make smarter decisions and stay on track toward your financial goals.

Using a money management app like NeoSpend helps you manage money smarter by making all of this much simpler. It pulls all your investment accounts together, so you can easily see how your portfolio is performing and how much dividend income you're actually earning, all in one spot.

How to Calculate Dividend Yield Step by Step

Ready to crunch some numbers? Don't worry, the dividend yield formula isn't nearly as intimidating as it sounds. You only need two key pieces of information, and both are surprisingly easy to find.

Here's the formula in all its glory:

Dividend Yield = (Annual Dividend Per Share / Current Share Price) x 100

Multiplying by 100 just flips the decimal into a simple percentage, which makes it much easier to read and compare. Let's break down each part so you know exactly what to look for.

The Two Key Ingredients

To calculate dividend yield, you really only need two numbers. You can usually find them on any major financial news site or right inside your brokerage app.

Annual Dividend Per Share: This is the total cash a company pays out over a year for every single share you own. Since companies often pay dividends quarterly, you might need to add up the last four payments. More often, though, you'll find an "annualized" figure already calculated for you.

Current Share Price: This one's simple. It’s the live market price for one share of the stock. Because stock prices fluctuate constantly, this number is just a snapshot in time.

Once you have those two figures, it's just a quick division problem. This simple calculation gives you a powerful tool for comparing the income potential of different stocks you're considering.

A Real Canadian Example

Let's walk through it with a company every Canadian knows: Bell Canada (BCE Inc.).

First, you'd pull up its stock details on your investing platform. Let's pretend you see the following info:

- Annual Dividend Per Share: $3.99

- Current Share Price: $45.50

Now, we just plug those numbers into our formula:

Dividend Yield = ($3.99 / $45.50) x 100

Do the math, and you get 0.0877. Multiply that by 100, and you land on a dividend yield of 8.77%. In simple terms, this means for every $100 you invest in BCE at this exact price, you could expect to get about $8.77 back in dividends over the next year.

Having all your investment info in one place with an app like NeoSpend makes this so much easier. Instead of bouncing between different brokerage accounts to find share prices and dividend info, you can see your whole portfolio in one spot. This helps you quickly check the yield and track the performance of everything you own.

Trailing Yield vs. Forward Yield for Canadian Investors

When you pull up a stock's dividend yield, you might not realize you're looking at one of two very different numbers: the trailing yield or the forward yield. Knowing which is which is absolutely critical if you want to make smart, forward-looking decisions for your Canadian portfolio.

Think of it like driving a car. The trailing yield is your rearview mirror—it tells you exactly where you've been. The forward yield is what you see through the windshield—it’s your best guess about the road ahead. Both views are essential, but they tell you completely different things about your journey.

This simple visual breaks down the calculation that drives both yield types.

As you can see, the core formula is the same. It's the dividend figure you plug into it that changes the entire story.

Understanding Trailing Dividend Yield

The trailing dividend yield looks backward. It’s calculated using the actual dividends a company paid out over the previous 12 months.

Because it’s based on real, confirmed payments, it’s a concrete historical fact. You can count on it. The downside? The past doesn’t always predict the future. A company might have had a stellar year and paid a juicy dividend, but if market conditions sour, that payout might not be sustainable.

What Is Forward Dividend Yield?

The forward dividend yield, on the other hand, is a projection. It takes the company’s most recently announced dividend and annualizes it, giving you an estimate of what the payout will be over the next 12 months.

This makes it a much more current, forward-looking metric.

Think about a Canadian energy company. Its trailing yield might look amazing after a year of high oil prices. But if analysts expect prices to drop, the company might signal a lower dividend ahead. The forward yield would reflect that change, painting a more realistic picture of your potential income.

A forward yield is an educated guess about future income, making it a valuable tool for assessing a stock's immediate potential and associated risks.

You can see this play out with some of the current TSX leaders. Labrador Iron Ore Royalty (LIF), for example, has a forward dividend yield of 6.94%, which is based on its expected annual payout. Likewise, National Bank of Canada (NA) is showing a 5.98% forward yield, signalling its projected income for shareholders. You can explore more high-dividend Canadian stocks to see how these numbers work in the real world.

By comparing both yields, you get a much richer story. If the forward yield is higher than the trailing one, it could be a sign of the company's confidence. If it's lower, that’s your cue to dig a little deeper and find out why.

Putting the Formula to Work in Your Portfolio

Knowing the dividend yield formula is one thing, but actually using it to make sense of your own portfolio is where the magic happens. Let's move past the theory and see how this simple calculation can sharpen your investment decisions, whether you're chasing income in a TFSA or compounding growth in an RRSP.

The formula gives us a common yardstick to compare the income potential of totally different companies. A big, stable Canadian bank will naturally have a different yield than a growing utility or a real estate investment trust (REIT). That's not just okay; it's expected. Your job is to figure out what those numbers mean for your financial strategy.

Comparing Stocks in a Canadian Context

Let's say you're sizing up three different Canadian stocks, each with a specific job to do in your portfolio. The dividend yield helps bring their roles into focus.

Scenario 1: The Stable Bank in Your TFSA

You're looking at a major Canadian bank, like TD Bank (TD), for your Tax-Free Savings Account. The goal here is simple: reliable, tax-free income.

- Annual Dividend: $4.08 per share

- Share Price: $76.50

Plugging that into the formula gives us: ($4.08 / $76.50) x 100 = 5.33% Yield

That 5.33% yield is a steady stream of cash you get to keep, tax-free. It’s not going to set the world on fire, but it’s dependable—exactly what you want for a TFSA income strategy.

Scenario 2: The Growing Utility in Your RRSP

Next up, a utility company like Fortis Inc. (FTS) for your Registered Retirement Savings Plan. In this account, you're playing the long game with dividend reinvestment and growth.

- Annual Dividend: $2.36 per share

- Share Price: $53.00

The math works out to: ($2.36 / $53.00) x 100 = 4.45% Yield

A slightly lower yield of 4.45% isn’t a red flag. For a company like Fortis, known for hiking its dividend every single year, the real power comes from reinvesting those payouts to fuel compound growth over decades. It's less about the cash today and more about building a bigger nest egg for tomorrow.

Scenario 3: The REIT for Monthly Cash Flow

Finally, you check out a Real Estate Investment Trust (REIT) like RioCan (REI.UN) for a non-registered account, where you want to generate monthly cash flow.

- Annual Dividend: $1.08 per share

- Share Price: $17.50

And the calculation: ($1.08 / $17.50) x 100 = 6.17% Yield

That higher 6.17% yield is pretty standard for REITs. They're built to pass most of their rental income straight to shareholders, making them a great fit for investors who want regular, predictable payments hitting their bank account.

What Makes a Good Dividend Yield?

So, what’s the verdict—what’s a "good" yield? Honestly, the answer changes depending on the company's industry and what you're trying to achieve.

A good dividend yield isn't just the highest number you can find. It's one that is sustainable, supported by strong company financials, and aligns perfectly with your investment objectives.

Think about the companies on the S&P/TSX Canadian Dividend Aristocrats Index. They are famous for their long track records of increasing dividend payouts. Their yields might not always be the highest on the market, but their reliability is what makes them so attractive to long-term investors. You can discover more about the historical performance of these consistent dividend payers to see for yourself why their yields are considered so solid.

Juggling all these different yields across your entire portfolio can get messy fast. This is where NeoSpend helps people manage money smarter. By linking all your accounts—TFSA, RRSP, and non-registered—it gives you one simple dashboard to see your portfolio's total yield and automatically track how your passive income is growing.

Avoiding the High-Yield Trap

When you're hunting for good investments, a stock with a sky-high dividend yield can feel like you've just struck gold. But hold on. Before you get too excited, you need to know that if a yield looks too good to be true, it probably is. This is such a common pitfall that it has its own name: the high-yield trap.

So, how does this trap work? It happens when a company's dividend yield gets artificially pumped up—not because the company is feeling generous, but because its share price has taken a serious nosedive.

Think back to the dividend yield formula. Share price is the denominator. So, when that number plummets, the yield percentage automatically shoots up, even if the actual dividend payment hasn't changed a bit. It’s simple math, but it creates a dangerous illusion of a fantastic income opportunity.

In reality, it's often a massive red flag signalling a company in deep financial trouble. The market has lost faith, investors are jumping ship, and that juicy yield might be the last thing to go before the company is forced to announce a dividend cut.

Spotting the Red Flags

Protecting your money means learning to look past that flashy yield number. You have to do a little digging into the company's financial health to make sure that dividend is actually sustainable.

Here are a few key warning signs that you might be walking into a yield trap:

- Unsustainable Payout Ratio: This tells you what percentage of a company’s earnings is being paid out to shareholders. If that ratio creeps over 100%, the company is paying out more than it’s making. That’s a huge problem.

- Declining Revenues or Profits: A healthy business should be growing its sales and profits over time. If you see those numbers consistently falling, it’s a clear sign the company is struggling and might not be able to support its dividend for long.

- High Levels of Debt: A company drowning in debt often has to choose between paying its lenders and paying its shareholders. Guess who usually wins? The lenders. That puts your dividend payment directly at risk.

The goal isn't just to find the highest yield. It's to find strong companies that can comfortably afford to pay you, not just this quarter, but for years to come. A slightly lower, rock-solid yield is always a better bet than a high one sitting on shaky ground.

By doing this extra bit of homework, you can sidestep one of the most common investing mistakes. It's all about building a resilient, income-generating portfolio based on financial stability, not just an attractive—but misleading—number. Using a tool like NeoSpend can help you see all your investments in one place, making it easier to monitor your portfolio's health and spot potential issues before they become major problems.

How Dividends Are Taxed in Canada

Figuring out the dividend yield formula is a great first step, but it’s only half the story. To really see what you’ll pocket, you need to understand how dividends are taxed here in Canada. Where you hold your investments makes a huge difference in your actual, take-home returns.

If you’re holding dividend stocks in a non-registered account, that income is taxable. But here’s the good news: the Canada Revenue Agency (CRA) doesn't treat all investment income the same. Thanks to a neat little mechanism, dividends from eligible Canadian companies are way more tax-friendly than interest income or even your regular paycheque.

The Canadian Dividend Tax Credit

The secret sauce is something called the Canadian Dividend Tax Credit. It’s basically a non-refundable credit designed to prevent double taxation—once when the company pays tax on its profits, and again when you get paid a dividend from those same profits.

In practice, this credit seriously lowers the personal tax rate you pay on dividend income. Let's say you earned $1,000 in interest; you'd be taxed on the whole amount. But if you earned that same $1,000 from eligible Canadian dividends, the tax credit kicks in to shrink the final tax bill, letting you keep more of your money.

Using Tax-Advantaged Accounts

For most Canadian investors, the smartest move is to sidestep the taxman altogether by using registered accounts. This is where a little bit of planning can have a massive impact on your long-term growth.

- Tax-Free Savings Account (TFSA): Any dividend income you earn inside a TFSA is 100% tax-free. This makes it the perfect home for your best dividend-paying stocks because every single cent they generate is yours, period.

- Registered Retirement Savings Plan (RRSP): Dividends earned inside an RRSP are tax-deferred. You won't pay a dime of tax on that income as it rolls in, which lets your investments compound much faster. You only pay tax when you start taking the money out in retirement.

By placing your dividend stocks in the right accounts, you’re not just investing—you’re being strategic. It’s about making your investment strategy and your tax planning work together.

This is where NeoSpend helps you manage money smarter by letting you see all your accounts—TFSA, RRSP, non-registered—in one spot. Having that bird's-eye view makes it so much easier to track your dividend income and make sure your portfolio is set up in the most tax-efficient way possible.

Got Questions About Dividend Yield? We've Got Answers.

Let's wrap up by tackling some of the most common questions Canadian investors have about dividend yield. Think of this as a quick-fire round to make sure everything we've covered is crystal clear.

What Is a Good Dividend Yield in Canada?

There’s no magic number here, because “good” really depends on the industry you’re looking at and what you’re trying to achieve with your investments.

That said, a yield between 2% and 6% is generally seen as a healthy, sustainable sweet spot for those solid, blue-chip Canadian companies we all know.

Be wary of anything that looks too good to be true. An unusually high yield (think 7% or more) can sometimes be a red flag. It might mean the company’s stock price has taken a nosedive, which could put future dividend payments in jeopardy. Always dig deeper into the company’s financial health instead of just chasing a high percentage.

How Often Do Companies Pay Dividends?

Here in Canada, the most common setup is a quarterly payout. That means you get a little cash deposit into your account every three months.

But it’s not the only way. Some companies, especially Real Estate Investment Trusts (REITs) and certain income funds, pay out every single month. A few others might pay semi-annually or just once a year.

Can a Dividend Yield Ever Be Negative?

Nope, it’s impossible for a dividend yield to be negative. The formula is built on two things that can't be negative: the annual dividend and the share price. The absolute lowest a yield can go is 0%, and that's for companies that don't pay a dividend at all.

Here’s a crucial point, though: while the yield can't be negative, your total return absolutely can be. If a stock’s price drops more than what you earn in dividends, you’re still in the red. A healthy dividend is great, but it’s only one part of the bigger investment picture.

Key Takeaway: The dividend yield formula is more than just math; it's a powerful lens that gives you a clear, simple way to assess an investment's income potential. By understanding how to calculate and interpret it in a Canadian context—from your TFSA to tax credits—you can build a more strategic and effective investment portfolio.

Ready to see how all these pieces fit together in your own portfolio? NeoSpend pulls all your Canadian investment accounts—TFSAs, RRSPs, you name it—into one clean dashboard. You can track your dividend income, see your portfolio's overall yield, and get the clarity you need to build wealth with confidence. Try NeoSpend today and see your money in a whole new light.