Ever wondered where you stand financially? A great place to start is your credit score. Think of it as your financial report card—a quick, three-digit summary of how you’ve handled borrowing money in the past. It’s a key piece of your financial identity here in Canada.

Right now, the credit score average in Canada is around 760, according to the latest data from FICO. This single number plays a huge role in your life, influencing everything from getting a mortgage for a condo in Toronto or a car loan for a truck in Calgary to signing up for a new mobile phone plan.

Your Credit Score is Your Financial Report Card

Remember your GPA back in school? A high one told teachers you were a dependable student. A low one? Well, that might have meant you needed a bit of extra help. Your credit score works in a very similar way with lenders.

A high score signals to lenders that you're a responsible borrower, making them much more comfortable offering you loans, often with better interest rates. For example, a great score could mean a lower interest rate on your mortgage, saving you thousands over the life of the loan. On the other hand, a lower score might make them hesitant or offer you higher rates.

Scores in Canada typically run on a scale from 300 to 900. The higher your number, the healthier your credit looks. It’s the go-to metric banks use to quickly figure out the risk of lending you money. A strong score can literally save you thousands of dollars over the years by unlocking lower interest payments on big-ticket items like a home or car.

Why The Average Score Matters

Knowing the national average gives you a powerful benchmark. It’s a simple way to see how your financial habits stack up against other Canadians. If you’re scoring above the average, you’re in great shape. If you’re below it, that’s not a failing grade—it’s just a clear sign that it’s time to focus on improving.

Lately, economic headwinds have been putting a squeeze on everyone's finances, and the numbers show it. FICO noted that the average score recently slipped to 760, down just a bit from its pandemic-era high. This isn't just a random fluctuation; it reflects the real-world impact of rising living costs and tough mortgage renewals hitting hundreds of thousands of Canadians. You can learn more about these Canadian credit score trends to get a feel for how the economic climate is shifting.

Your credit score isn't just a number—it’s a reflection of your financial habits and a key that unlocks future opportunities. Understanding it is the first step toward building a stronger financial future.

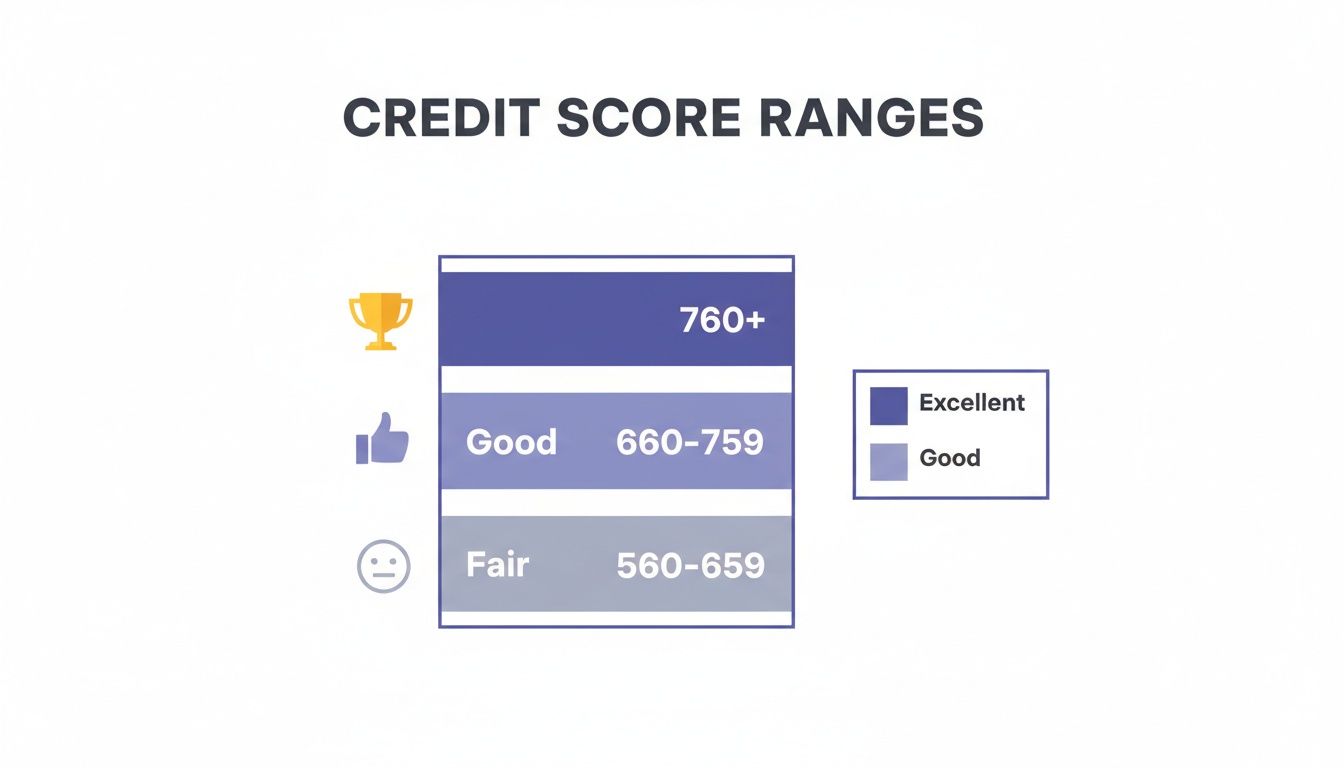

Decoding the Credit Score Ranges

So, what does your specific number actually mean? To make sense of it, it helps to know the different tiers. While the exact goalposts might shift slightly between Canada’s two main credit bureaus—Equifax and TransUnion—the breakdown generally looks like this. It's helpful to see where your score falls to understand what lenders see when they look at your profile.

Canadian Credit Score Ranges At a Glance

| Credit Score Range | Rating | What It Means For You |

|---|---|---|

| 760 and above | Excellent | You're a top-tier borrower. You'll get the best rates and premium products with ease. |

| 725-759 | Very Good | Lenders see you as a safe bet. You should get approved for most loans at competitive rates. |

| 660-724 | Good | You're in a solid spot. Most lenders will view you positively for standard loans and mortgages. |

| 560-659 | Fair | You might face some hurdles. Approvals can be tougher, and you'll likely see higher interest rates. |

| Below 560 | Poor | Getting new credit will be a challenge. This often signals a history of missed payments or defaults. |

Once you know where you stand, you can set clear, achievable goals to climb to the next level. Think of it as levelling up your financial life. By understanding these ranges, you can pinpoint exactly where you are and what you need to work on. That's where a tool like NeoSpend helps. By consolidating your finances, it gives you a clear view of your spending so you can build the habits needed to move into a higher credit score tier.

How Credit Scores Vary Across Canadian Provinces

It’s no secret that life is different from one coast to another, and the same goes for our financial lives. The local job market, the cost of a two-bedroom apartment in Montreal, and the overall economic vibe of a place all play a role in shaping the average credit score.

Think about it: someone navigating the high-octane housing market of Toronto has a completely different set of financial pressures than a person living in a quiet Maritime town. These regional numbers aren't just interesting facts; they're a benchmark, giving you a sense of where you stand compared to your neighbours.

As you can see, hitting that 660 mark gets you into the "Good" zone. That's a great target to aim for if you want lenders to start offering you better rates.

A Look at City-Specific Averages

When you zoom in from the provincial level to specific cities, the picture gets even clearer. British Columbia, for example, often has some of the highest averages in the country, while cities in Alberta can see their scores shift with the boom-and-bust cycles of the energy sector.

The numbers tell a fascinating story. In B.C., Vancouverites have an average score of 703, with Victoria not far behind at 691. Hop over to Alberta, and you’ll find Calgary at 665 and Edmonton at 645. Ontario’s a mixed bag—Markham leads with a strong 715 and Toronto sits at 694, but Hamilton's average is a more modest 653. Meanwhile, Montreal comes in at 690, and Winnipeg holds an average of 657. You can dig deeper into how Canadian cities stack up to get the full picture.

Here’s the key takeaway: where you live matters. Things like sky-high housing costs or local job security have a real, tangible impact on how people in your community manage their debt, and that shows up in the average credit score.

Why Do These Regional Differences Exist?

So, what’s driving these variations? It boils down to a few core factors.

- Economic Health: Provinces with strong, diverse economies tend to have higher average incomes and more stable jobs. That stability makes it easier for people to build and maintain good credit.

- Cost of Living: In cities like Vancouver and Toronto, massive mortgages and high rents mean people are often carrying more debt. Managing that bigger debt load without a stumble is a tougher balancing act.

- Debt Levels: The amount of consumer debt people carry—from credit card balances to car loans—directly influences a region's average score.

No matter where you are in Canada, using a smart money management app can give you a clear view of your spending and bills, making it way easier to build a strong score that opens doors.

The Five Ingredients of Your Credit Score

Your credit score isn’t just some random number pulled out of thin air. Think of it more like a recipe, where five key ingredients tell lenders how you handle your money. Once you understand what they are and how much weight each one carries, you're on your way to mastering your score.

While the exact formulas used by Equifax and TransUnion are kept under wraps, the general breakdown is pretty well-known. Each piece of the puzzle contributes a different percentage to your final score.

Payment History (35%)

This is the big one. Your payment history is the single most important ingredient, making up a massive 35% of your score. It’s a straightforward record of whether you pay your bills on time.

Every missed payment—on a credit card, car loan, or even a hydro bill that gets sent to collections—can leave a negative mark that sticks around for years. Consistently paying on time is the best thing you can do for your credit. Even one late payment can have a real impact, so setting up reminders or automatic payments is a smart move. This is where an app like NeoSpend can be a total game-changer, helping you track due dates so nothing falls through the cracks.

Credit Utilization (30%)

Your credit utilization ratio sounds a bit technical, but it’s really just the amount of credit you're using compared to the total amount you have available. It’s the second-biggest piece of the pie. Here's how it works: if you have a credit card with a $10,000 limit and you've got a $5,000 balance, your utilization is 50%. When lenders see high utilization, they get a little nervous because it might signal that you're stretched thin financially.

A good rule of thumb is to keep your credit utilization below 30% on each of your credit cards and lines of credit. Honestly, the lower, the better.

Imagine you're doing a big home reno in Calgary and you charge $8,000 in materials to a card with a $10,000 limit. That 80% utilization could temporarily ding your score, even if you plan on paying it all off next month.

Length of Credit History (15%)

This ingredient is all about how long you’ve been using credit. It looks at the age of your oldest account, your newest account, and the average age of all your accounts combined. A longer credit history gives lenders more data to see how reliable you are over time. This is exactly why it’s often a good idea to keep old, no-fee credit cards open, even if you don’t use them much. Closing that card could shorten your credit history and potentially drop your score.

New Credit (10%)

Whenever you apply for new credit—like a credit card, a mortgage, or a car loan—it triggers what's called a hard inquiry on your credit report. Each hard inquiry can cause a small, temporary dip in your score. If you apply for a bunch of new credit products in a short time, it can look like a red flag to lenders. It might suggest you're in some kind of financial trouble or just taking on way too much debt at once. It’s always best to space out your applications.

Credit Mix (10%)

Finally, lenders like to see that you can responsibly manage a few different types of credit. A healthy credit mix might include a combination of:

- Revolving Credit: Things like credit cards and lines of credit, where you can borrow and repay over and over.

- Installment Loans: Loans with fixed payments and a set end date, like a mortgage, car loan, or student loan.

Having a mix shows you’re a versatile and trustworthy borrower. But—and this is a big but—you should never take on debt you don’t need just to try and improve your credit mix. This factor is much less important than paying on time and keeping your balances low.

Actionable Steps to Boost Your Credit Score

Knowing where the credit score average sits is one thing, but the real power comes from taking action. The good news is that improving your credit score isn't about some drastic financial overhaul. It’s all about building small, consistent habits that pay off big time.

Think of it like getting in shape—each good decision strengthens your financial muscle. These are the practical, down-to-earth strategies that will actually move the needle on your credit health, opening up doors to better rates and more opportunities across Canada.

Master Your Payment History

If there’s one golden rule in the credit game, it’s this: always pay your bills on time. This isn't just a suggestion; it's the absolute foundation of a healthy score. Your payment history is the single biggest piece of the credit score pie, so it’s where you need to focus first. A single late payment can stick to your credit report for years, dragging your score down.

The easiest way to nail this? Set up automatic payments for your recurring bills—credit cards, your phone plan, car loans, you name it. It takes the "oops, I forgot" factor completely out of the equation and builds a perfect track record for you. Tools like NeoSpend are built for exactly this. The app helps you keep tabs on bills and subscriptions, sending reminders before the due dates. It’s a simple safety net that helps you protect the most important part of your score.

Keep Your Credit Utilization Low

Next up is managing how much of your available credit you're actually using. This is your credit utilization ratio, and trust me, lenders are watching it closely. They want to see a healthy amount of breathing room on your accounts.

In Canada, the rule of thumb is to keep your balance on each credit card and line of credit below 30% of its limit. So, on a card with a $5,000 limit, you'd want to keep the balance under $1,500.

Staying below that 30% threshold sends a clear signal: you're not overextended and you know how to manage your credit responsibly. If your balances are creeping up, make paying them down your top priority. You'd be surprised how quickly this one move can boost your score.

Protect Your Credit History

Building a solid credit history is a marathon, not a sprint. Once you've put in the time, you want to protect it. It might feel like good housekeeping to close that old credit card you never use, but that move can sometimes backfire. When you close an old account, especially one you’ve had for a decade, you can shorten the average age of your credit history. Since a longer history is a good thing for your score, it’s often smarter to keep that no-fee card open. Just use it for a small purchase every few months to keep it active and preserve that hard-earned history.

Here are a few more quick wins to get you on the right track:

- Check for Errors: Pull your credit reports from Equifax and TransUnion regularly and scan them for mistakes. Finding and disputing an error can be a fast way to fix a score that’s being unfairly held back.

- Limit New Applications: Try not to apply for a bunch of new credit cards or loans in a short time frame. Every application triggers a "hard inquiry," which can temporarily ding your score. Space them out.

- Become an Authorized User: If you have a parent or partner with a stellar credit history, ask them to add you as an authorized user on one of their cards. Their on-time payments and long history could give your score a helpful nudge.

By weaving these tips into your regular financial routine, you'll be well on your way to building a score that shows lenders you’re a great person to do business with—and leaving "average" in the dust.

How NeoSpend Helps You Build Better Credit

Knowing what goes into the average credit score is one thing, but actually doing something about it? That’s what really moves the needle. This is where NeoSpend steps in to act as your financial co-pilot. It’s designed to help you build the kind of habits that lead to a stronger credit profile, giving you the tools to change the numbers, not just look at them.

NeoSpend pulls all your Canadian financial accounts into one simple dashboard, giving you a 360-degree view of your money in minutes. Seeing everything in one place makes it so much easier to track where your money is going, tackle your budget, and start chipping away at debt.

See Your Financial Health at a Glance

One of the fastest ways to see your score drop is letting your credit card balances climb. NeoSpend’s dashboard makes it dead simple to keep an eye on your credit utilization. You can see your balances across all your cards in real time, which is a huge help for staying under that crucial 30% threshold.

This isn't just about spending trends. The dashboard also shows you what bills are coming up, giving you the heads-up you need to manage your money proactively. When you keep these key numbers front and centre, you can’t help but make smarter decisions that directly support your credit-building goals.

Never Miss a Payment Again

Your payment history is the single biggest ingredient in your credit score. Seriously, just one late payment can undo months of hard work. NeoSpend’s automatic bill and subscription tracker is like a personal safety net, making sure nothing slips through the cracks.

The app keeps you on top of your financial commitments in a few key ways:

- Upcoming Due Dates: It flags all your upcoming payments—from your phone bill to your Netflix subscription—so you always know what’s around the corner.

- Renewal Reminders: You’ll get a heads-up before annual subscriptions renew, giving you a chance to decide if you still want to keep them.

- Smart Alerts: Get notifications for due dates and any unusual activity, helping you dodge those painful late fees and protect your credit.

With NeoSpend, you're not just tracking your money; you're building a system for success. It’s all about making on-time payments feel effortless, and that's the absolute cornerstone of an excellent credit score.

Get Proactive Insights with Neo AI

What if you had a financial assistant that could spot trouble before it becomes a problem? That’s the magic of Neo AI. It quietly analyzes your spending patterns and serves up practical insights to help you stay on the right path. For example, Neo AI can let you know if you're spending more than usual in one category, which could make it harder to pay off your credit card bill in full. It can even help you plan for bigger purchases by showing you how they might affect your budget and your credit utilization. This isn’t just another app; it’s a smart partner dedicated to helping you build a healthier financial future.

Got More Questions About Canadian Credit Scores?

Even after digging into what goes into your credit score and where the national credit score average sits, it's totally normal to have a few more things on your mind. Getting your credit right is a journey, not a destination. Having clear answers makes that journey a whole lot smoother.

Here are some straightforward answers to the questions we hear all the time from Canadians just like you.

How Long Does It Take to Improve My Credit Score?

You’ll need some patience, but the good news is you don’t have to wait forever to see things moving in the right direction. While a major credit turnaround takes time, you can start seeing positive changes pop up on your credit report within a few months of building consistent, healthy habits. For example, if you focus on making all your payments on time and bringing down your credit card balances, you could see a nudge in your score in as little as 30 to 60 days. On the flip side, bouncing back from a big financial hit like a bankruptcy will be a multi-year process. The real key? Consistency. It's your most powerful tool for long-term credit health.

Will Checking My Own Credit Score Lower It?

This is a huge myth, so let's put it to rest once and for all: No, checking your own credit score will never, ever lower it. When you check your score through a service like Borrowell or even your bank's app, it’s what’s known as a "soft inquiry." Think of it as a personal check-in. These have zero impact on your score. A "hard inquiry" is different. That only happens when a lender pulls your credit report because you’ve formally applied for new credit, like a mortgage or a credit card. A bunch of hard inquiries in a short time can cause a small, temporary dip in your score, but a soft inquiry is harmless.

Checking your own score is just like looking in the mirror—it shows you where you stand. It's actually a smart financial habit that helps you track your progress and spot any trouble early on.

What's a Good Credit Score in Canada, Really?

It helps to know what you're aiming for. In Canada, a credit score of 660 or higher is generally considered good. Once you hit that mark, you should have a solid chance of getting approved for most standard loans and credit cards.

But why stop there? Here’s a quick look at the upper levels:

- Very Good (725-759): Now you’re talking. Lenders see you as a very reliable borrower and will start offering you more competitive interest rates.

- Excellent (760+): You're in the top tier. Lenders will roll out the red carpet, offering you their very best products and the lowest interest rates possible. This can literally save you thousands of dollars over the life of a mortgage or car loan.

Is It Bad to Have No Credit History?

Having no credit history isn't quite the same as having bad credit, but it presents its own unique challenge. Lenders rely on your financial past to predict how you'll handle debt in the future. If you have no history, they have no data—it's like trying to hire someone with a blank resume. This can make it tough to get your first credit card, be approved to rent an apartment, or even sign up for certain mobile phone plans. For young adults and newcomers to Canada, building that initial credit history is a crucial first step. Starting with something simple like a secured credit card or a credit-builder loan is a great way to establish that positive track record you'll need for your bigger financial goals.

Takeaway: Your credit score is more than just a number; it's a powerful tool that reflects your financial habits and opens doors to future opportunities. By understanding the key factors that influence it—like paying bills on time and keeping balances low—you can take practical steps to build a score that's well above the Canadian average.

Managing your credit doesn't have to feel like a mystery. With the right information and tools like NeoSpend, you can get a clear picture of your finances, track your bills effortlessly, and build the habits that lead to a stronger credit score. Ready to take control? Try NeoSpend today and get a clear picture of your financial health.