A credit card minimum payment calculator does one thing, and it does it brilliantly: it pulls back the curtain on the true cost of just scraping by. It shows you, in clear dollars and cents, exactly how many years and how much extra money you'll pay in interest if you only make minimum payments. This gives you the hard data you need to build a real payoff plan.

The Real Cost of Making Only Minimum Payments in Canada

We’ve all been there. The credit card statement arrives, and that tiny minimum payment looks tempting, especially when your budget is stretched thin. It’s an easy option that keeps your account in good standing.

But here’s the tough truth: that seemingly harmless choice is one of the most expensive financial traps you can fall into. It's a system designed to keep you in debt for years—sometimes even decades—by accumulating interest.

In Canada, credit card issuers typically calculate your minimum payment as a small percentage of your balance, plus any interest and fees for that month. The problem? This payment is so small it barely makes a dent in the interest charges, let alone the actual money you borrowed (the principal).

Why the Minimum Is a Maximum Problem

Picture this: you're trying to empty a bathtub with the tap still running. Paying only the minimum is like using a teaspoon to bail out the water—you're putting in effort, but you’re not making any real headway against the flood of incoming interest.

Worse, the interest compounds. That means you start paying interest on your interest, digging the hole deeper every single month.

This isn't a niche problem. A recent report found the average credit card balance for a Canadian was sitting around $4,499. For people stuck in the habit of making only minimum payments, their payoff timeline can stretch from a few years to well over a decade.

You can dig into more data on Canadian credit card trends to see the full scope of the issue. A credit card minimum payment calculator is built to show you this exact scenario with your own numbers.

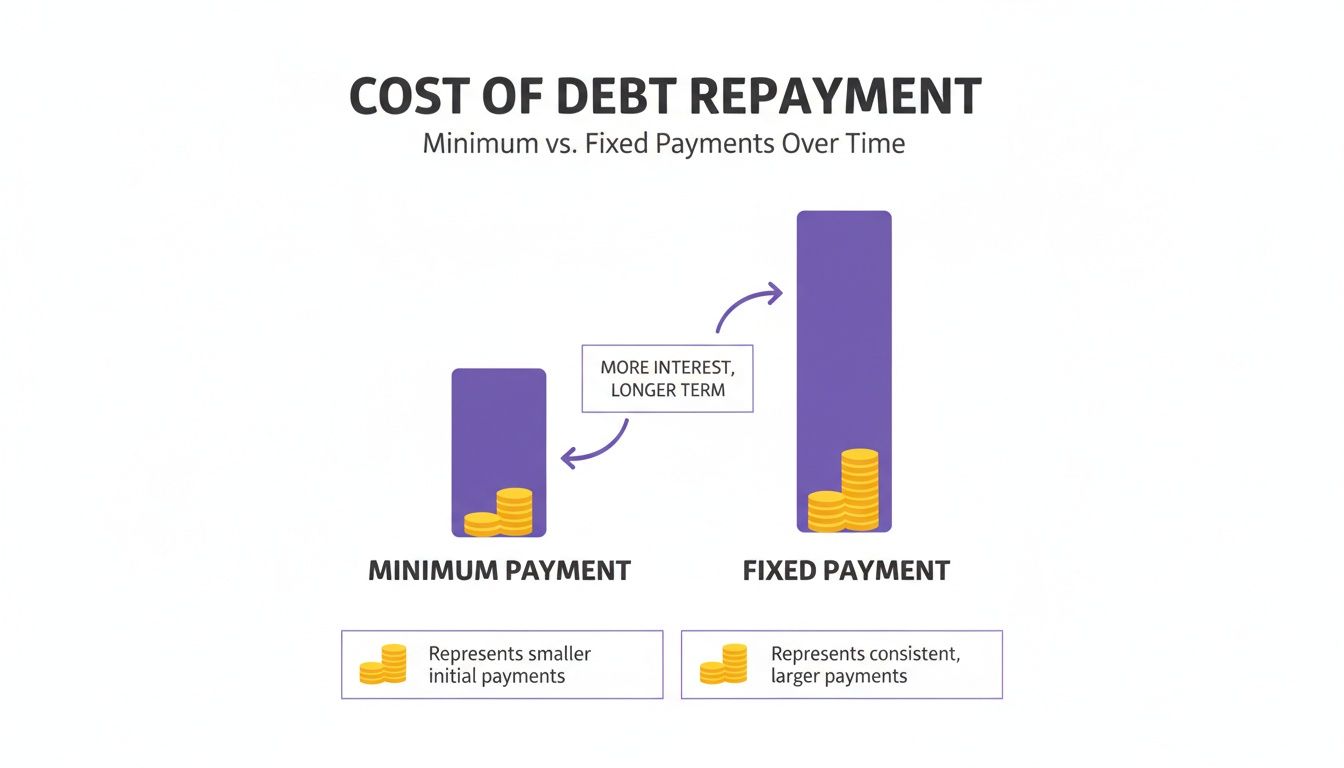

This chart drives the point home, showing the massive difference between sticking to the minimum versus paying a little more each month.

The visual contrast is stark. Even a small increase in your monthly payment can save you thousands of dollars and get you out of debt years sooner.

Minimum Payment vs Fixed Payment: An Everyday Canadian Example

Let's look at what this means for a typical Canadian with a $4,499 balance on a card with a 20.99% interest rate. This table breaks down the two approaches.

| Payment Strategy | Monthly Payment | Time to Pay Off | Total Interest Paid |

|---|---|---|---|

| Minimum Payment | Starts at ~$135, decreases over time | 16 years and 10 months | $4,932 |

| Fixed Payment | $150 (just a bit more) | 3 years and 2 months | $1,623 |

By paying just a little more than the minimum with a fixed $150 payment, you would save $3,309 in interest and be debt-free 13.5 years earlier. It's a game-changer.

The most powerful step toward financial freedom is understanding exactly what your debt is costing you. A minimum payment hides this cost, while a calculator reveals it in stark detail.

Ultimately, you want to shift your mindset from, "What's the least I have to pay?" to "What's the most I can afford to pay to eliminate this debt?"

That's where smart tools help you manage money smarter. For example, an app like NeoSpend lets you see exactly where your money is going, find places to cut back, and redirect that cash to your credit card balances. It helps you break the cycle for good.

How to Use a Minimum Payment Calculator Like a Pro

Ready to face your debt head-on? A credit card minimum payment calculator is more than just a numbers game—it's a tool that shows you your financial future. Using one is simple, but truly understanding the results is where you find the motivation to take back control.

First, grab your latest credit card statement. You'll need three key pieces of information, which are usually easy to spot.

- Current Balance: This is the total amount you owe right now.

- Annual Percentage Rate (APR): This is the interest rate you’re being charged on your balance.

- Minimum Payment Rule: This is the formula your bank uses. It’s often a percentage of your balance (like 2% or 3%) plus interest and fees, or a flat amount like $10, whichever is higher.

Once you have those details, you’re ready to plug them into a calculator and see the hard truth about just scraping by.

A Realistic Canadian Credit Card Scenario

Let's use an example that hits close to home for many Canadians. Imagine you have a $5,000 balance on a department store credit card with a common 19.99% APR. Your card issuer calculates your minimum payment as 2% of the balance plus interest.

When you enter those numbers into a calculator, it will give you two key figures. Prepare yourself.

- Time to Pay Off: This tells you how many months—and years—it will take to be free of this debt if you only ever make the minimum payment.

- Total Interest Paid: This is the shocker. It shows you the extra money you’ll give the bank on top of the original $5,000 you spent.

For this scenario, the results are staggering. It would take over 23 years to clear the debt. Even worse? You'd end up paying roughly $8,100 in interest alone. That's significantly more than the original debt itself.

Turning Those Numbers Into Actionable Insights

Seeing figures like that isn't meant to discourage you. It's meant to empower you. A calculator's real job is to turn that vague, nagging stress about debt into a concrete problem with a measurable cost.

This is your wake-up call. It’s the moment you stop passively letting debt linger and start actively planning its elimination. The goal is simple: make those numbers—the payoff time and total interest—as small as possible.

Now the fun begins. Start playing with the numbers. What if you paid a fixed $200 a month instead of the minimum? The calculator will instantly show your payoff time plummeting and your interest savings soaring into the thousands.

This is where smart tools can really help you manage your money smarter. An app like NeoSpend can track your spending habits and highlight where you might be able to cut back, freeing up that extra cash to throw at your balance. When you can see your entire financial picture in one place, you can turn that feeling of urgency into a powerful, effective payoff plan.

Why Are So Many Canadians Stuck in the Minimum Payment Trap?

If you feel like you're running on a treadmill trying to pay down your credit card, you’re not alone. Many people across Canada are caught in that same frustrating cycle, where paying more than the minimum feels out of reach. It's a huge challenge, fuelled by very real financial pressures.

Let's be honest: the rising cost of living has squeezed household budgets. When essentials like groceries, rent, and gas eat up more of your paycheque, extra debt payments are often the first thing to get cut. For many, this means there's no choice but to pay the bare minimum just to stay afloat.

Add to that stubbornly high interest rates, and even a small balance can feel impossible to pay down. This isn’t just a feeling; it’s a trend backed by data.

The Big Picture on Canadian Credit Card Debt

Recent financial reports paint a clear picture of how Canadians are handling credit card debt. In mid-2023, the average payment rate on bank cards was a relatively healthy 55% of the outstanding balance. By early 2024, that number dropped sharply to between 48% and 49%.

That shift shows that people are being forced to pay down less of what they owe. This kind of financial pressure makes tools like a credit card minimum payments calculator more critical than ever for seeing the real, long-term impact. You can explore more of these Canadian bankcard industry trends to see the full story.

Understanding this context is key. It confirms that falling into the minimum payment trap isn’t a personal failing—it’s often a direct result of a tough economic climate. Knowing this helps you shift from feeling stuck to making a strategic plan.

Your Actionable Escape Plan

The first step to regaining control is visibility. You can’t fight an enemy you can’t see. This is where you pivot from understanding the broader problem to tackling your own financial situation head-on.

The first step to breaking the cycle isn't about earning more money—it's about truly understanding where your money is going right now. Small, strategic tweaks can free up more cash than you think.

This is exactly where a tool like NeoSpend comes in to help you manage your money smarter. By linking your accounts, you get a crystal-clear picture of your spending habits. NeoSpend’s smart AI analyzes your transactions and flags areas where you could potentially cut back, often without making drastic sacrifices.

Think of it like this:

- Spot Your Habits: See if you’re consistently overspending on things like daily coffees or forgotten subscriptions.

- Find Hidden Savings: Pinpoint subscriptions you don't use anymore or find other areas to trim your budget.

- Free Up Cash: Take the money you save and redirect it straight toward that high-interest credit card debt.

By automating this process, you can stop guessing and start confidently planning. Bit by bit, you can begin chipping away at that balance and finally break free from the minimum payment trap.

How to Break the Minimum Payment Cycle for Good

Seeing how much minimum payments cost you is a real eye-opener. But knowing is only half the battle. To actually break free, you need an actionable game plan. The good news is there are proven methods to tackle your debt head-on, save a ton of money, and finally feel in control of your finances.

And you're not alone in this. A recent study found that 36% of Canadian cardholders now carry a balance from month-to-month. Even more telling is that 58% of credit card users are considered "financially unhealthy." This is a widespread issue. You can dig into their full findings on Canadian credit card satisfaction for more context.

Choose Your Debt Payoff Strategy

When it comes to paying down debt, two methods stand out: the Debt Avalanche and the Debt Snowball. There's no single "best" choice—the right one is the one you'll actually stick with.

The Debt Avalanche (The Financial Logic Method)

This strategy is for the numbers-oriented person. You focus on paying off your highest-interest debt first while making minimum payments on everything else. It’s the fastest way to save the most money on interest.

- An Everyday Canadian Example: Let's say you have a $3,000 balance on a store credit card at 22.99% APR, plus a $5,000 line of credit at 12.99% APR. With the avalanche method, you'd throw every spare dollar at that high-interest store card first.

The Debt Snowball (The Motivational Method)

This strategy is all about psychology. You attack your smallest debt first, regardless of the interest rate. The goal is to score a quick, satisfying win that builds momentum and keeps you motivated.

- The Same Scenario: With the same two debts, the snowball method has you focusing all extra payments on the $3,000 store card because it's the smaller balance. Getting that "paid in full" notification gives you a huge mental boost to roll that payment over to the next debt.

Whichever plan you choose, the core idea is identical: focus your firepower. Pay the minimum on all debts except one, and then attack that target with everything you’ve got.

Find Extra Cash in Your Budget

You don’t need a sudden windfall to make a real dent in your debt. Small, smart tweaks to your spending can free up a surprising amount of cash.

- Audit Your Subscriptions: Go through your last few credit card statements line by line. Are you still paying for a streaming service you forgot about? A gym membership you haven't used? Cancelling just two or three can easily put $30-$50 back in your budget each month.

- Round Up Your Payments: This is a simple trick that works wonders. If your payment is $187, round it up to an even $200. That extra $13 feels small, but it adds up to an extra $156 a year going straight to your principal balance.

- Try Bi-Weekly Payments: Instead of one payment per month, split it in half and pay every two weeks. Since there are 26 bi-weekly periods in a year, you'll make the equivalent of one extra monthly payment without even feeling it.

Making these changes is much easier when you have a clear picture of where your money is going. This is where an app like NeoSpend can make a huge difference. It automatically sorts your spending, so you can easily spot those forgotten subscriptions or find other areas to trim. When you know exactly what’s happening with your cash, you can confidently redirect it to what matters most—getting out of debt.

Automate Your Debt Payoff Plan for Good

Let's be real: manually tracking multiple credit card balances, due dates, and spending categories feels like a stressful second job. When life gets busy, it’s all too easy for those carefully crafted debt-free plans to fall by the wayside.

This is where the right technology can completely change the game, turning your goals into a simple, automated system that works for you.

Imagine having one clear view of your entire financial world. That's the power of an app like NeoSpend. It’s designed to streamline the process of getting out of debt so you can get back to living your life.

By connecting your Canadian bank accounts and credit cards, the guesswork is gone. All your balances, due dates, and transactions are in one organized place. No more juggling multiple apps and websites just to know where you stand.

Put Your Savings on Autopilot

One of the biggest hurdles in any debt payoff journey is finding the extra cash to make larger payments. This is where a smart tool becomes your secret weapon.

NeoSpend digs into your spending habits, automatically categorizing everything to show you exactly where your money goes. It’s like having a personal financial assistant pointing out opportunities you might have missed.

- Flags Recurring Charges: It spots all your subscriptions, making it easy to see which ones you've forgotten about so you can cancel them and free up cash.

- Analyzes Spending Patterns: The app learns your habits and suggests practical areas to cut back without making you feel deprived.

- Finds Hidden Money: By getting the full picture, you can spot the small leaks in your budget that, once plugged, add up to real money you can throw at your debt.

This takes the emotion and tedious manual labour out of budgeting. Instead of wrestling with spreadsheets, you get clear, actionable insights that help you find that extra $50 or $100 a month to accelerate your payoff plan.

Your journey to becoming debt-free doesn't have to be a constant struggle. Automating your financial tracking gives you the clarity and consistency you need to stick with it for the long haul.

Never Miss a Payment Again

Late fees are the worst. They inflate your balance, rack up more interest, and only dig you deeper into a hole. A single missed payment can undo weeks of hard work.

That’s why automatic bill tracking is such a crucial feature. NeoSpend keeps an eye on your upcoming due dates and sends you timely reminders, so you never get hit with an unnecessary late fee again. It's about building a safety net that protects your progress and keeps you moving forward, turning an ambitious plan into a simple, sustainable routine.

Your Questions About Credit Card Payments Answered

It's completely normal to have questions when you're navigating credit card debt. Let's tackle some of the most common ones we hear from Canadians to give you a clear path forward.

Does paying only the minimum hurt my credit score in Canada?

This is a tricky one. While making the minimum payment on time keeps your account in good standing and avoids a late payment on your credit report, it can indirectly harm your score.

The key factor is your credit utilization ratio—the percentage of your available credit that you're currently using. Lenders in Canada like to see this number stay below 30%.

When you only pay the minimum, your balance stays high. This keeps your utilization ratio elevated, which can signal to lenders that you're financially stretched. Over time, this can drag your credit score down.

What happens if I miss a minimum payment entirely?

Missing a payment, even by one day, triggers several negative consequences. First, your card issuer will likely charge you a late fee, adding to your balance.

Then, they'll report the missed payment to Canada’s main credit bureaus, Equifax and TransUnion, which will cause an immediate dip in your credit score. To make matters worse, you could also lose any promotional interest rate you have, causing your APR to jump to a much higher penalty rate.

Is it better to pay off one card or pay extra on all of them?

This is a classic personal finance debate. The "best" method is simply the one you’ll stick with.

The Debt Avalanche method is the most efficient on paper. You direct every extra dollar at the card with the highest interest rate, which saves you the most money in the long run.

However, many people get a huge motivational boost from the Debt Snowball method. With this strategy, you focus on paying off your smallest balance first, regardless of the interest rate. Scoring that first win can give you the momentum to keep going.

The best strategy is the one you will actually stick with. Both the Avalanche and Snowball methods are excellent choices for taking control of your debt; choose the one that aligns with your motivation style.

How is my next minimum payment calculated after an extra payment?

Your minimum payment is always calculated based on your statement balance at the end of each billing cycle. When you make an extra payment, you lower your overall balance.

This means your next minimum payment will actually be a little bit lower. This is why you need to stay disciplined! Avoid the temptation to just pay the new, smaller minimum. Commit to paying that same, higher amount every month to maintain your momentum and eliminate that debt faster.

Your Takeaway: Understanding the true cost of minimum payments is the first step toward financial freedom. Use a credit card minimum payments calculator to see your own numbers, then create a realistic plan using strategies like the Debt Avalanche or Snowball. By finding small savings and staying consistent, you can break the cycle and pay off your debt years sooner.

Ready to stop guessing and start planning? Let NeoSpend give you the clarity you need to take control of your finances. See all your accounts in one place, find hidden savings with AI insights, and build a debt payoff plan you can actually stick to. Try NeoSpend today by visiting https://neospend.com and take the first step toward your debt-free future.