Picture your yearly Canada Pension Plan (CPP) contributions as filling up a bucket for your retirement. The CPP max contribution is simply the point where that bucket is considered full for the year. It's the absolute highest amount you (and your employer, if you have one) need to contribute based on your annual earnings.

Once you hit that limit, you're done contributing to CPP for the rest of the year. The best part? That money that was being deducted goes right back into your pocket on every paycheque until the new year starts.

So, What Exactly Is the CPP Max Contribution?

The Canada Pension Plan is a cornerstone of retirement planning for most working Canadians, but you don't contribute indefinitely. There’s a ceiling on how much you pay in each year, and that ceiling is what we call the CPP max contribution. It's a key number to understand on your pay stub.

This limit exists to keep the system fair. It ensures your contributions are tied to a reasonable portion of your income. The government sets an annual income cap, known as the Year's Maximum Pensionable Earnings (YMPE). You only contribute on the income you make up to this cap. As soon as your earnings surpass the YMPE, your CPP deductions simply stop for the rest of the year.

This system achieves two important things:

- It caps your payments: This prevents you from paying CPP on every single dollar you earn, which is a big relief for higher-income earners.

- It shapes your future benefits: The amount you put in is directly linked to the pension you’ll receive down the road. Consistently hitting the maximum contribution is how you qualify for the largest possible pension payout in retirement.

For many Canadians, hitting the annual CPP max feels like getting a surprise raise partway through the year. Suddenly, your take-home pay gets a nice bump because that CPP deduction vanishes from your paycheque until January 1st.

Understanding this concept is a solid first step in mastering your money. It helps you anticipate changes in your pay and plan accordingly. For instance, a smart spending and savings tool like NeoSpend helps you track your deductions throughout the year. You'll see exactly how much you've contributed, giving you a clear idea of when you might hit the cpp max contribution and allowing you to budget smarter for when that extra cash starts flowing your way.

How Your CPP Contribution Is Calculated

Ever look at your pay stub and wonder where that "CPP deduction" number comes from? It's not a random amount; it’s calculated using a precise formula set by the federal government. Once you understand the key ingredients, it's actually quite straightforward.

Knowing how it works empowers you to read your paycheque with confidence and even forecast how your take-home pay might change throughout the year.

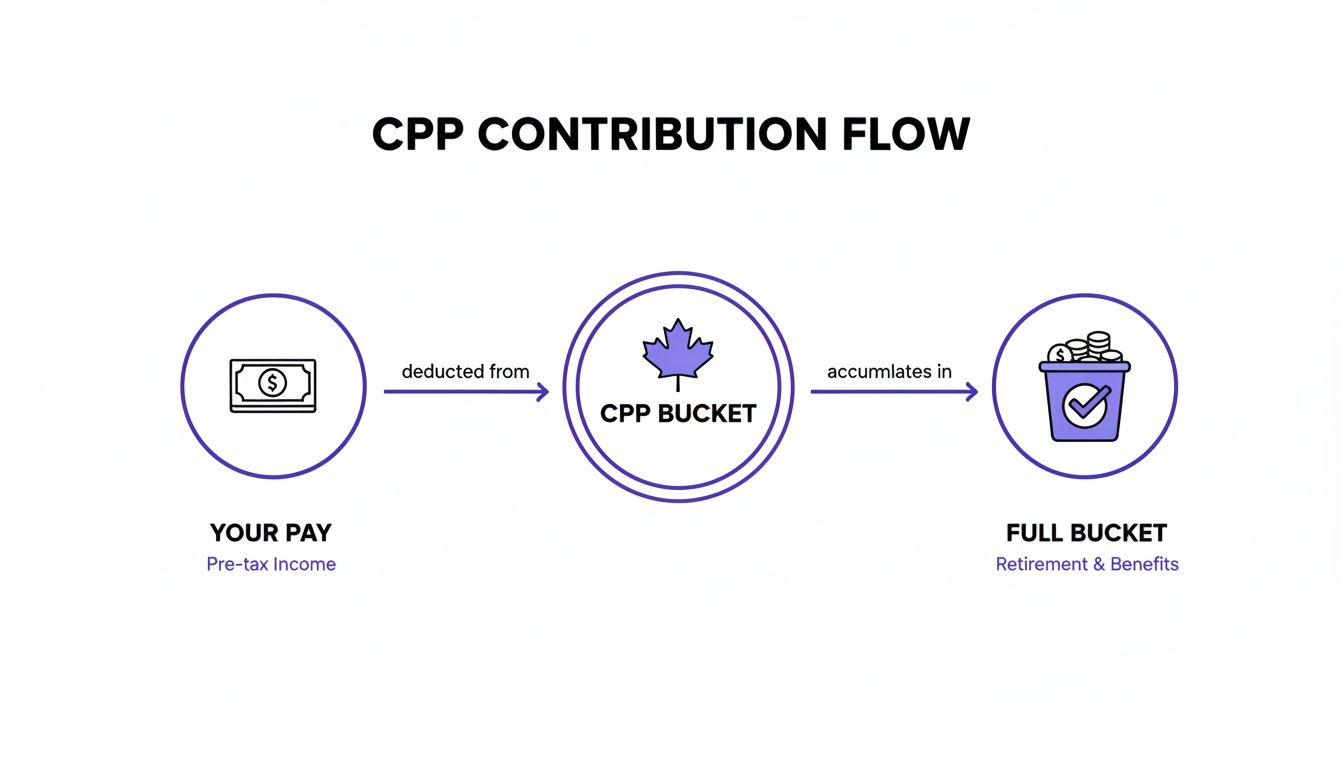

This flowchart gives you a simple picture of how your contributions flow from your paycheque into your future retirement fund.

Essentially, a piece of every paycheque goes into your CPP "bucket." This continues until you hit the annual limit. Then—poof!—the deductions stop, and your paycheque gets a little bigger for the rest of the year.

The Core Ingredients of Your CPP Payment

To calculate your exact contribution, there are three key numbers you need to know. The government updates these annually, but they work together to determine your payment.

Before we dive into the math, here's a quick cheat sheet for the terms you'll see.

Key Terms in CPP Calculations

This table is a quick reference guide to the essential terms used to calculate your annual CPP contribution.

| Term | Simple Explanation | What It Means For You |

|---|---|---|

| YMPE (First Earnings Ceiling) | The maximum income you pay base CPP contributions on each year. | Once your income hits this number, your base CPP deductions stop for the rest of the year. |

| Basic Exemption Amount | The first chunk of your income that is exempt from CPP contributions. | You don't pay any CPP on this initial amount, giving everyone a small break. |

| Contribution Rate | The percentage of your eligible income that gets deducted for CPP. | This percentage is applied to your earnings between the basic exemption and the ceiling. |

| YAMPE (Second Earnings Ceiling) | A new, higher income ceiling for those who earn more than the YMPE. | If you earn above the YMPE, you'll pay an additional contribution on income up to this cap. |

Think of these terms as the building blocks for your contribution. Now, let's see how they fit together.

Putting the Numbers to Work

Year's Maximum Pensionable Earnings (YMPE): This is the official earnings ceiling for base CPP contributions. For 2024, the YMPE is set at $68,500. Any dollar you earn above this amount is not subject to the first tier of CPP deductions.

Basic Exemption Amount: Every Canadian gets a break on the first slice of their income. You don’t pay a cent of CPP on the first $3,500 you earn in a year. The calculation only starts after this amount.

Contribution Rate: This is the magic percentage. For 2024, both employees and employers contribute 5.95% each on pensionable earnings. (If you’re self-employed, you cover both halves).

So, the basic formula looks like this: (Your Income - $3,500) x 5.95% = Your Contribution... up to the max, of course.

A New Layer for Higher Earners

Starting in 2024, a second tier of CPP contributions was introduced, often called "CPP2." This only impacts Canadians who earn more than the YMPE.

Think of it like this: Your main CPP contributions fill up a big bucket. If your income is high enough to fill that one, you now start pouring a little extra into a second, smaller bucket. This extra contribution is designed to lead to a bigger CPP payout when you retire.

This second tier comes with its own ceiling, the Year's Additional Maximum Pensionable Earnings (YAMPE). For 2024, the YAMPE is $73,200.

If your income falls between the YMPE ($68,500) and the YAMPE ($73,200), you'll contribute an additional 4.0% on just that portion of your earnings.

Keeping track of these two tiers and when you'll hit the max can be a headache. That’s where a smart money management tool like NeoSpend becomes a game-changer. It helps you visualize your income and deductions, giving you a clear, real-time view of how close you are to reaching the cpp max contribution without needing to pull out a calculator after every payday.

Employee vs Self-Employed CPP Contributions

How you contribute to the Canada Pension Plan looks very different depending on whether you're an employee or self-employed. For employees, it’s a shared cost; for the self-employed, it’s a solo responsibility. Understanding this difference is crucial for managing your money and avoiding surprises at tax time.

For most employees in Canada, contributing to CPP is a team effort. You pay your share through automatic deductions from each paycheque, and your employer matches it, dollar for dollar. It’s a clean 50/50 split. This matching contribution is a significant benefit, as it doubles the amount going toward your future retirement pension without you having to foot the entire bill.

The Self-Employed Responsibility

If you're self-employed—whether you’re a freelancer, contractor, or small business owner—the situation changes. You are responsible for covering both the employee and the employer portions of the CPP contributions. This means you pay the full rate on your net self-employment income when you file your annual tax return.

Essentially, being your own boss means you're also your own employer in the eyes of the Canada Revenue Agency (CRA). This demands a more hands-on approach to your finances, as you must proactively set aside cash to cover this larger contribution.

This double duty can lead to a significant tax bill if you haven't planned for it. It's one of the biggest financial adjustments for people transitioning from traditional employment to entrepreneurship. This is where modern financial tools can make a world of difference. The Canadian fintech scene is growing rapidly, providing tools to help people manage these challenges. While major banks are still dominant, innovative companies are gaining ground as Canadians seek smarter ways to handle their money. You can learn more about this trend on fintech.global.

A Real-World Comparison

To see the financial impact clearly, let’s compare two Canadians, each earning $60,000 in pensionable income.

- The Employee in an Office: Contributes 5.95% of their pensionable earnings. Their employer matches that amount. The employee’s direct contribution is manageable and spread out over the year.

- The Self-Employed Freelancer: Must contribute the full 11.9% (5.95% + 5.95%). Their total contribution is double that of the employee and is typically paid when they file their taxes.

This stark difference highlights why proactive budgeting is non-negotiable for freelancers and entrepreneurs. A good rule of thumb is to set aside a percentage of every payment you receive for taxes and CPP.

For self-employed Canadians, NeoSpend can be a lifesaver. The app’s smart features can help you set up a dedicated savings goal for your tax bill, track your income, and set reminders for quarterly instalment payments. By helping to automate this process, NeoSpend helps you budget for the full cpp max contribution so you can manage these larger payments smoothly and focus on what you do best—running your business.

Real-World Examples of CPP Contributions

Theory is great, but seeing the numbers in action makes it all click. Let's walk through a few common scenarios for Canadian workers to see how the Canada Pension Plan math plays out on a paycheque.

For these examples, we'll use the official 2024 numbers: a first earnings ceiling (YMPE) of $68,500 and a basic exemption of $3,500.

Example 1: Salaried Employee Earning Below the Max

Meet Aisha, a marketing coordinator in Toronto earning a $60,000 salary. Her income is below the maximum threshold (the YMPE), which means she'll see CPP deductions on every paycheque all year long.

Here’s the breakdown of her annual contribution:

- Calculate Pensionable Earnings: First, we subtract the basic exemption from her salary.

- $60,000 (Income) - $3,500 (Exemption) = $56,500 (This is the amount she pays CPP on).

- Apply the Contribution Rate: Now, we apply the employee rate of 5.95%.

- $56,500 x 5.95% = $3,361.75

Aisha’s total contribution for the year is $3,361.75. Her employer matches that amount, meaning a total of $6,723.50 goes into her CPP account for the year.

Example 2: High-Income Employee Earning Above the Max

Now, let's look at David, a software developer in Vancouver making $95,000 a year. Since his salary is well above the $68,500 YMPE, he will hit the cpp max contribution limit before the year is over.

His calculation is based on the maximum pensionable earnings, not his entire salary.

- Calculate Maximum Pensionable Earnings (Tier 1): We find the portion of income that the base CPP rate applies to.

- $68,500 (YMPE) - $3,500 (Exemption) = $65,000

- Apply the Contribution Rate (Tier 1): David contributes 5.95% on that amount.

- $65,000 x 5.95% = $3,867.50

But because David's income is also above the second earnings ceiling (the YAMPE, at $73,200), he also contributes to "CPP2." This is calculated on the income between the two ceilings ($73,200 - $68,500 = $4,700).

- $4,700 x 4.0% = $188.00

Adding it all up, David's total annual CPP contribution is $4,055.50 ($3,867.50 + $188.00). Once he's paid that full amount, the CPP deductions stop, and he gets a nice bump in his take-home pay for the rest of the year.

Pro Tip: Tracking these deductions manually can be tricky. A tool like NeoSpend gives you a real-time view of your earnings and deductions, making it easy to see when you’re getting close to hitting that annual max.

Example 3: Self-Employed Professional

Finally, let’s look at Maria, a freelance graphic designer in Montreal with a net self-employment income of $80,000. As a freelancer, she is responsible for paying both the employee and employer portions of CPP.

- Calculate Maximum Pensionable Earnings (Tier 1): The math starts the same as David's.

- $68,500 (YMPE) - $3,500 (Exemption) = $65,000

- Apply the Full Contribution Rate (Tier 1): Maria pays the combined rate of 11.9% (5.95% x 2).

- $65,000 x 11.9% = $7,735.00

Since her income is also above the second ceiling, she also pays both sides of the CPP2 contribution.

- $4,700 x 8.0% (4.0% x 2) = $376.00

Maria’s total annual contribution is a hefty $8,111.00. This is a powerful reminder of why careful financial planning is essential when you're your own boss.

To put it all into perspective, here's a quick comparison of how CPP contributions look at different income levels.

Sample CPP Contribution Scenarios (2024)

| Scenario | Annual Income | Annual CPP Contribution |

|---|---|---|

| Part-Time Retail Worker | $30,000 | $1,576.75 |

| Mid-Range Salaried (Aisha) | $60,000 | $3,361.75 |

| High-Income Salaried (David) | $95,000 | $4,055.50 |

| Self-Employed (Maria) | $80,000 | $8,111.00 |

As you can see, your contribution varies significantly based not just on how much you make, but also on how you make it.

How Hitting the CPP Max Affects Your Paycheque

For many higher-earning Canadians, a welcome moment arrives sometime in the fall or winter: the day the CPP deduction disappears from their pay stub. Hitting your CPP max contribution for the year brings an immediate and noticeable perk—a bigger paycheque.

Once you've paid the maximum amount required for the year, you're done. From that point until December 31st, the money that was going to the Canada Pension Plan now goes directly into your bank account. It feels like getting a temporary raise.

From Short-Term Gain to Long-Term Security

While that extra cash feels great in the moment, hitting the max has a more important long-term impact. Consistently reaching the maximum contribution year after year is how you qualify for the highest possible CPP retirement pension when you eventually stop working.

Think of it this way: each year you hit the maximum, you’re maximizing your future retirement income potential from this program. It underscores how valuable the CPP is for building a secure retirement in Canada.

The extra take-home pay you get after maxing out your CPP is a golden opportunity. Instead of just letting it get absorbed into daily spending, you can use it to accelerate your other financial goals.

A bit of smart planning can make a huge difference here. Canada's fintech sector is booming—valued at USD 4.38 billion in 2024 and projected to hit USD 18.84 billion by 2033—giving us incredible tools to manage our money better than ever. You can read more about Canada's fintech growth on imarcgroup.com.

Capitalize on Your Extra Income with NeoSpend

So, what should you do with that extra money? This is the perfect chance to turn a temporary pay bump into lasting financial progress.

With a tool like NeoSpend, you can automate your financial strategy so you don't even have to think about it. Here are a few smart moves to consider:

- Boost Your Savings: Set up a recurring transfer to move that extra amount straight into your Tax-Free Savings Account (TFSA) or Registered Retirement Savings Plan (RRSP).

- Pay Down Debt: Schedule an extra payment toward high-interest debt like a credit card balance. You'll become debt-free faster.

- Build Your Emergency Fund: If your emergency savings are looking a little thin, this is the perfect time to build a solid cash cushion for life's unexpected events.

NeoSpend helps you see the bigger picture. By keeping an eye on your deductions, the app helps you anticipate when you’ll hit the cpp max contribution. That way, you can plan ahead and make sure every dollar from your boosted paycheque is working toward a stronger financial future.

Putting Your CPP Knowledge to Work

Now that you understand the nuts and bolts of the CPP max contribution, it’s time to turn that knowledge into a real-world strategy. A little planning can help you make the most of the shifts in your paycheque and, crucially, avoid any surprises when you file your taxes.

For high-income employees, there's a great opportunity each year when you hit the CPP maximum. When your take-home pay gets that boost, be intentional. A simple yet powerful move is to set up an automatic transfer for the amount your CPP deduction used to be, sending it straight into a TFSA, RRSP, or high-interest savings account.

If you’re self-employed, you're playing a different game. Since you're responsible for both the employee and employer portions, financial discipline is key. A proven tactic is to open a separate bank account just for your taxes and CPP payments. Every time a client pays you, immediately move a set percentage—often between 15-20%, depending on your income—into that account. Don't touch it. Your future self will thank you.

Let Tech Handle the Heavy Lifting

Manually tracking deductions and planning for tax instalments can feel like a part-time job. Thankfully, we don't have to do it alone. Modern financial tools are designed to take the headache out of managing money.

It’s clear Canadians are embracing them. Calgary’s own Neo Financial saw its revenue grow by an incredible 38,000% in just three years, signaling a huge shift in how we approach our finances. You can get the full story on how fintech is shaking things up for Canadians over at fintech.ca.

This trend highlights just how valuable apps like NeoSpend can be, turning what used to be a chore into something you barely have to think about.

Think of a smart budgeting app as putting your financial plan on autopilot. The right tool gives you a crystal-clear picture of your money, keeps you on track with your goals, and helps you put every single dollar to work.

This is exactly what NeoSpend was built for. It offers features that help you get ahead of your CPP contributions and other financial obligations:

- Savings Goals: Create a specific goal for your self-employed tax bill and automatically track your progress.

- Bill Tracking: Get reminders for those quarterly tax instalments so you never get hit with a late penalty.

- AI Insights: NeoSpend can analyze your spending habits and point out where you can save, freeing up more cash for what truly matters.

By combining smart strategies with the right tools, you can stop reacting to your CPP obligations and start proactively managing them—a small shift that makes a huge difference in building a solid financial foundation.

Your Top CPP Questions, Answered

Once you get the hang of how the Canada Pension Plan works, a few practical "what-if" questions usually pop up. Let's tackle some of the most common ones we hear from Canadians.

Can I Top Up My CPP Contributions Voluntarily?

It's a great question, but the short answer is no. Unlike an RRSP where you can voluntarily add more funds, your CPP contributions are mandatory and fixed.

They’re tied directly to your employment income each year, up to the maximum limit set by the government. Think of it less like a savings account and more like an insurance premium—it's calculated for you, not chosen by you.

I Think I Overpaid My CPP. What Happens Now?

This happens frequently, especially if you had more than one job in a single year. Each employer deducts CPP as if they are your only one, so it's easy to contribute more than the annual cpp max contribution limit.

Don't worry—that money isn't lost. When you file your income tax return, the Canada Revenue Agency (CRA) automatically calculates any overpayment and issues it back to you as a refund. It’s a seamless process.

Do My CPP Contributions Reduce My RRSP Contribution Room?

Nope, these are two separate pillars of your retirement plan. Your RRSP contribution room is calculated based on 18% of your earned income from the previous year (up to a set maximum) and is not affected by CPP.

While they both help you build a solid retirement, how much you pay into CPP has zero impact on how much you're allowed to save in your RRSP. They work in parallel to support your financial future.

Takeaway: Understanding your CPP max contribution is a key part of smart financial planning in Canada. For employees, it means a paycheque boost late in the year, and for the self-employed, it’s a crucial number for tax planning. By knowing your numbers and using tools like NeoSpend, you can turn this knowledge into actionable steps toward building a stronger financial future. Explore more financial topics or try NeoSpend to start managing your money smarter today.