When you break it down, the difference between a chequing and a savings account is simple. Your chequing account is for spending money day-to-day. Your savings account is for growing your money for the future. This guide will help you, as a Canadian, master both.

Think of your chequing account as your financial hub for daily life. It’s where your paycheque lands and where you pull money from for bills, groceries, and your morning Tim Hortons run. A savings account, on the other hand, is where your money goes to work for you, quietly building up for your bigger goals. Using them together correctly is the key to smart money management.

Chequing vs. Savings Account: What's the Difference for Canadians?

To get a handle on your finances, you need the right tool for the right job. A chequing account is built for a high volume of transactions—it’s designed for money to flow in and out without a fuss. Savings accounts are the opposite; they’re meant for your money to stay put and grow, rewarding you with interest for your patience.

Understanding this core difference is the first step to building a smarter financial system. You wouldn't use a hammer to turn a screw, right? In the same way, using a savings account for daily spending just doesn't make sense. Stick to each account's purpose, and you'll sidestep needless fees and actually let your money grow.

For Canadians, getting this right is key to everything from paying rent in a pricey city like Toronto to saving for that down payment in Calgary. This table lays out the key differences so you can see exactly where each account shines.

Key Differences Between Chequing and Savings Accounts

Here’s a quick side-by-side look at what sets these two essential bank accounts apart, with practical Canadian examples.

| Feature | Chequing Account | Savings Account |

|---|---|---|

| Primary Purpose | Daily transactions and bill payments | Long-term savings and wealth building |

| Transaction Frequency | High (often unlimited) | Low (often with limited free withdrawals) |

| Interest Rates | Very low or none | Higher, designed to grow your money |

| Common Fees | Monthly maintenance, overdraft fees | Excess withdrawal fees |

| Typical Use Cases | Paying bills, Interac e-Transfers, direct deposits from your employer | Emergency fund, vacation savings, down payment on a home |

Understanding these distinctions helps you use each account strategically to manage your cash flow and build for the future. A tool like NeoSpend simplifies this by giving you a clear, single view of both, helping you track spending and move money to hit your goals faster.

The biggest mistake people make is treating their chequing account like a savings account. Letting big sums of cash just sit there means you're missing out on growth. A smart financial strategy uses both accounts together.

Your Chequing Account: The Hub for Daily Spending

Think of your chequing account as your financial command centre. It’s where your money is constantly on the move, flowing in and out to handle all your daily transactions. Your paycheque lands here, and it's from here you pay for everything from your monthly rent to that morning double-double.

Unlike a savings account, which is designed to hold and grow your money, a chequing account is built for action. It’s set up to handle frequent debits, bill payments, and transfers, making it the go-to tool for managing your everyday cash flow without getting hit with penalties.

How Chequing Accounts Work in Canada

In Canada, chequing accounts are the real workhorses of personal finance. They're specifically designed for the high volume of transactions that define modern life. Whether you're paying a Telus bill online, firing off an Interac e-Transfer after brunch in Toronto, or just tapping your debit card at the grocery store, your chequing account is what makes it happen.

Because they’re built for spending, these accounts typically offer very low interest, if any at all. Their value isn’t in making you money, but in giving you easy access to it when you need it. This is the core of the chequing vs savings account debate: one is for spending, the other is for stashing.

Your chequing account’s main job is to provide liquidity—the ability to access your cash whenever you need it for day-to-day life. It prioritizes access over growth.

Navigating Common Chequing Account Fees in Canada

That convenience can sometimes come at a price. Many Canadians are all too familiar with monthly maintenance fees, which can run anywhere from a few dollars to over $30 for premium accounts. You might also get dinged for exceeding transaction limits, using another bank's ATM, or for non-sufficient funds (NSF).

To keep those costs in check, you have a few options:

- Maintain a Minimum Balance: Many banks will waive their monthly fee if you keep a certain amount of cash in your account, often somewhere between $3,000 and $5,000.

- Choose a No-Fee Account: Digital banks and credit unions across Canada are changing the game with chequing accounts that have no monthly fees and unlimited transactions.

- Bundle Your Services: Some institutions will cut you a break on fees if you have other products with them, like a mortgage or an investment account.

Juggling all this activity can get complicated, but that’s where NeoSpend can make all the difference. It connects directly to your chequing account to give you a crystal-clear view of your cash flow. It automatically sorts your spending and sends you timely reminders for upcoming bills, helping you steer clear of overdrafts and late fees. When you know exactly where your money is going, you can start making better decisions and keep more of it for yourself.

Your Savings Account: The Engine for Your Financial Goals

If your chequing account is for the day-to-day grind, your savings account has a much bigger, more exciting job: it's the engine that powers your future. This isn't just a place to stash whatever cash is left over at the end of the month. It's a strategic tool you can use to turn big dreams into real, achievable goals.

Changing how you think about your savings account is the first step. Stop seeing it as a simple storage unit and start thinking of it as a launchpad. It’s for major life milestones—that down payment on a home in Vancouver, a dream trip, or just building a solid financial safety net so you can sleep better at night. Unlike a chequing account, its whole purpose is to sit there, accumulate, and earn interest.

Supercharge Your Savings with the Right Canadian Accounts

In Canada, not all savings accounts are created equal. To really get things moving, you need to look past a basic savings account and find options that give you a real advantage.

- High-Interest Savings Accounts (HISAs): These are a fantastic starting point. HISAs offer much better interest rates than you'd get from a standard savings or chequing account, making them perfect for your emergency fund or other short-term goals.

- Tax-Free Savings Accounts (TFSAs): A TFSA is a must-have for Canadian savers. It’s a registered account where any interest or investment growth you make is completely tax-free. Pro tip: holding a HISA inside a TFSA is a powerful one-two punch for maximizing your returns without giving the government a piece of the action.

- Registered Retirement Savings Plans (RRSPs): These are specifically for retirement. Any money you contribute to an RRSP is tax-deductible, which lowers your taxable income for the year. Your investments then grow tax-deferred until you pull them out in retirement.

Picking the right account is a huge part of your chequing vs. savings strategy. A standard savings account is fine, but a TFSA or RRSP is where you actually start building wealth.

A savings account is more than just a bank feature; it's a commitment to your future self. Every dollar you put in is a vote for your long-term well-being over short-term wants.

Unfortunately, making that commitment isn’t always easy. Canadians have historically found it tough to build up savings, with the national household saving rate fluctuating over the years. You can explore more on Canadian saving trends to see how this plays out in personal finance. This is where automation and clear goals become your secret weapons. By setting up an automatic transfer from your chequing to your TFSA every payday, you're consistently building your nest egg. NeoSpend helps you do this, with goal-tracking features that let you see your progress, making it easier to stay motivated and hit your targets faster.

Choosing the Right Account: Practical Canadian Scenarios

Knowing the theory behind a chequing vs. savings account is one thing. Actually putting them to work together is how you start building real financial momentum. The trick is to stop thinking of them as separate and start seeing them as a team, where each one has a specific job based on your immediate needs and future goals.

Take payday, for example. The second that money hits your account, you've got a choice to make. How much stays in your chequing to cover the bills and life for the next month, and how much gets shipped off to savings to build for the future? It's a constant balancing act between having cash on hand for today and growing your money for tomorrow.

The Payday Split Strategy: A Canadian Example

A solid way to start is by tallying up your fixed monthly expenses. We're talking rent or mortgage, utilities, car payments, insurance—all the predictable bills. Then, add a bit of a buffer for the things that change, like groceries, gas, and whatever you do for fun. That final number is the absolute minimum you should keep in your chequing account.

Let's say your fixed costs in Calgary come out to $2,800. A smart move would be to keep about $3,200 in your chequing account to handle everything with a little wiggle room. Any dollar over that amount should be immediately swept into a savings account so it can get to work earning interest.

NeoSpend Pro Tip: The app's AI can actually look at your spending habits and suggest a personalized payday split for you. It might send you a notification like, "Your average monthly spend is $3,150. We recommend keeping $3,500 in chequing and moving the leftover $950 to your 'Vacation Fund' goal."

This one simple habit fights off "cash drag"—that thing that happens when too much money sits doing nothing in a low-interest chequing account. It feels like a small move, but it adds up big time. This hands-on approach to saving is also part of a bigger picture in Canada, where household savings rates show a major split between generations. You can learn more about these Canadian savings trends to see where you fit in.

Managing a Side Hustle in Canada

The chequing vs. savings account decision gets even more critical if you're juggling a side hustle or freelance work. Mixing your business and personal cash in a single chequing account is a surefire way to create a mess, especially when tax season rolls around.

Here’s a much cleaner way to handle it:

- Open a separate chequing account just for your side gig. All your business income goes in, and every business expense (think software, supplies, ads) comes out of it.

- Pay yourself a "salary." Transfer a fixed amount from your business chequing to your personal chequing on a regular schedule, just like a real payday.

- Stash your profits in a dedicated savings account to cover income taxes. A good rule of thumb is to set aside 25-30% of every single payment you receive.

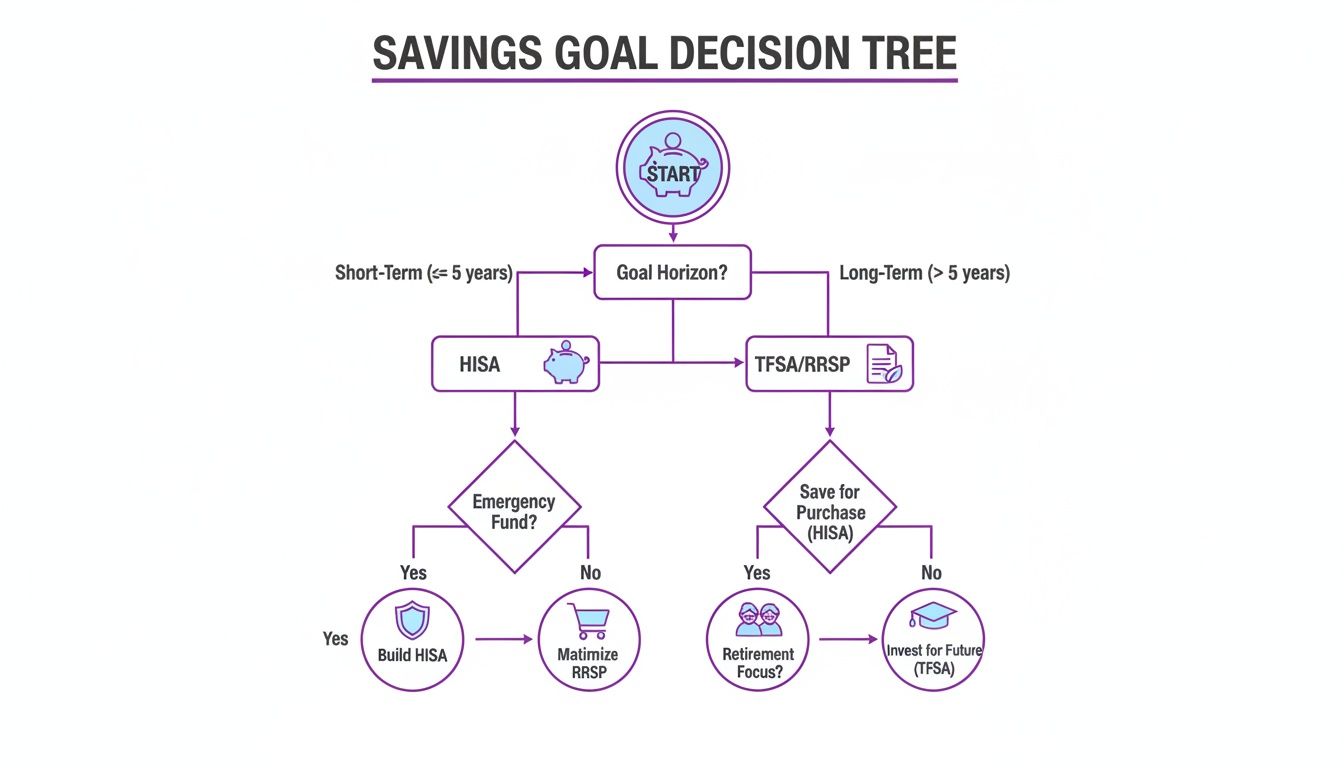

This flowchart helps visualize how to match your savings account to what you’re trying to achieve, whether it’s a short-term goal or a long-term dream.

As you can see, short-term goals are perfect for accounts you can access easily, like a HISA. On the other hand, bigger ambitions like retirement are better off in accounts that offer tax advantages, like a TFSA or RRSP.

How to Build Your Emergency Fund with a Savings Account

A savings account’s most critical job? Building your financial safety net. Think of this emergency fund as your personal buffer against life's curveballs—a sudden job loss, a leaky roof, you name it. It's tempting to keep all your money in one pot, but your chequing account is simply the wrong tool for this job.

An emergency fund has to be easy to get to, but not so easy that you dip into it for non-emergencies. This is where a High-Interest Savings Account (HISA) really pulls its weight. It hits that sweet spot between liquidity and growth, letting your money earn real interest while staying ready for when you actually need it.

Calculating Your Emergency Fund Goal

The classic rule of thumb is to have three to six months' worth of essential living expenses tucked away. This isn't your total income; it’s the bare-bones amount you need to cover the absolute must-haves if your paycheques stopped coming.

To figure out your target, just add up your non-negotiable monthly bills:

- Rent or mortgage payments

- Utilities (hydro, heat, internet)

- Groceries and transportation

- Insurance premiums and any debt payments

Got your monthly total? Multiply it by three to get a solid starting goal. For instance, if your essential expenses run about $3,000 a month, your first target for an emergency fund should be $9,000.

Building this safety net is non-negotiable. A chequing account offers zero growth for this crucial fund. A savings account, on the other hand, puts your money to work, compounding over time and giving you a much better defence against inflation.

This is where the chequing vs savings account debate becomes crystal clear. Shockingly, recent data shows that only 52% of Canadians have enough cash saved to cover three months of expenses, leaving almost half the country in a tough spot. You can discover more insights about Canadian financial preparedness in this report from the Financial Consumer Agency of Canada.

Automate Your Way to Financial Security

Staring at that goal number can feel overwhelming, but modern tools make it much easier. NeoSpend can help you build this buffer automatically. Just set up recurring transfers from your chequing to your savings account every payday.

This "set it and forget it" method means you're consistently building your safety net without having to think about it. NeoSpend even sends you little nudges and alerts when you hit milestones, turning what feels like a huge task into a series of small wins. That’s how you get the peace of mind that comes with real financial security.

Common Questions Canadians Ask About Chequing vs. Savings Accounts

When you're figuring out the best way to handle your money, a few questions always seem to pop up. Let's clear the air on some of the most common ones Canadians ask about chequing and savings accounts. Getting these details right is the first step to building a solid financial system that actually works for you.

Can I use a savings account for daily spending in Canada?

You could, but you really, really shouldn't. Think of it this way: you wouldn't use a screwdriver to hammer a nail. It’s the wrong tool for the job.

Savings accounts in Canada are built to hold and grow money, not for a flurry of daily activity. They typically give you maybe one or two free withdrawals a month. Go over that, and you’ll get hit with hefty fees that can completely erase whatever interest you've earned. For your daily coffee run, bill payments, and Interac e-Transfers, your chequing account is your best friend.

How many bank accounts do I really need?

For most Canadians, the magic number is two: at least one chequing account and one savings account. This is your foundational setup. The chequing account is your financial command centre for money coming in and going out, while your savings account is where you park cash for the future.

Pro Tip: Open multiple savings accounts and give them nicknames like 'Emergency Fund,' 'Vacation to Bali,' or 'Future Car Down Payment.' This little trick makes your goals feel more real and helps you track your progress without getting everything mixed up.

An app like NeoSpend simplifies this by pulling all your different accounts into one clean view, so you get the full picture of your finances without having to jump between multiple banking apps.

Is a TFSA the same as a savings account?

This is a big one, and it's easy to get them confused. A Tax-Free Savings Account (TFSA) isn't a type of account, but rather a registration with special tax benefits. A TFSA's superpower is that any money it earns—from interest or investments—is 100% tax-free.

You can absolutely hold a High-Interest Savings Account (HISA) inside a TFSA. This is one of the smartest ways to turbocharge your savings for big goals because you get to keep every penny of the interest, no questions asked by the CRA. With a normal savings account, any interest you make is considered taxable income.

What’s the best way to avoid chequing account fees?

Nobody likes paying fees. A common way to get monthly chequing fees waived at many Canadian banks is by keeping a minimum balance, which is often a hefty $4,000 or more. Some banks also offer fee-free accounts for students or seniors.

Honestly, the easiest route is often to go with a digital bank that offers no-fee chequing as a standard feature. On top of that, NeoSpend can act as your personal fee watchdog. It can track your transactions and ping you if you’re about to exceed the limits on a basic chequing plan, saving you from those annoying extra charges.

Key Takeaway: The secret to smart banking is using a chequing account for daily spending and a savings account for future goals. By automating transfers and choosing the right accounts (like a HISA within a TFSA), you can avoid fees and make your money work harder for you.

Ready to make your chequing and savings accounts work smarter, together? NeoSpend brings everything into focus so you can master your daily spending and hit your savings goals faster. Start managing your money with clarity today.