Ever sold something—like stocks, a piece of art, or a small business—for more than you paid for it? That profit is a capital gain, and in Canada, it's usually taxable. But before you worry about the tax bill, there's good news. The Canadian government offers powerful tax breaks, or exemptions, designed to reduce what you owe and encourage investment in our economy.

Understanding these rules is key to smart financial management. One of the most valuable tax breaks for entrepreneurs, farmers, and fishers is the Lifetime Capital Gains Exemption (LCGE). This guide will break down how it works in simple, practical terms for Canadians.

Selling an asset for a profit is a major financial milestone, but it usually means the Canada Revenue Agency (CRA) will expect a share. Thankfully, the Canadian tax system includes special exemptions that can shrink, or even completely eliminate, the tax you owe on those profits.

For any Canadian who owns assets, mastering these exemptions is a game-changer. Whether you’re a homeowner, an investor, or a small business owner, knowing what you qualify for can save you thousands. Two of the most significant exemptions are the Principal Residence Exemption and the Lifetime Capital Gains Exemption (LCGE).

Principal Residence vs. Lifetime Exemption

If you’ve heard of any capital gains exemption, it’s likely the Principal Residence Exemption. This is the rule that lets most Canadians sell their main home without paying a cent of tax on the profit. It’s a cornerstone of our tax system, designed to ensure families aren't penalized for moving or downsizing.

The Lifetime Capital Gains Exemption (LCGE), on the other hand, is more specialized but incredibly valuable. It’s a major perk aimed directly at entrepreneurs and owners of Canadian farm and fishing businesses. Think of it as a reward for building a business from the ground up. This guide will focus on the LCGE, providing a clear roadmap to its rules.

The LCGE is a cumulative limit, not a one-time deal. You can use it across several sales of qualifying assets during your lifetime until you hit the maximum amount. This makes long-term strategic planning absolutely essential.

Why This Exemption Matters to You

For many Canadian entrepreneurs, their business isn't just a job—it's their life's work and largest asset. The LCGE acknowledges this commitment by allowing you to shelter a massive portion of your profit from tax when you sell your business.

Specifically, it applies to the sale of:

- Qualified Small Business Corporation (QSBC) shares: These are shares in a private, Canadian-controlled company that meets specific asset criteria.

- Qualified farm or fishing property: This includes assets like land, buildings, equipment, or licenses used in a farming or fishing business.

This guide will demystify the LCGE rules, breaking them down into simple, practical steps. We'll cover who qualifies, how to calculate your exemption, and how tools like NeoSpend help you manage your finances smarter. By the end, you'll be able to make informed decisions that protect your financial future.

Diving Into the Lifetime Capital Gains Exemption

The Lifetime Capital Gains Exemption (LCGE) is one of the most powerful tax-saving tools available to Canadian entrepreneurs. It’s the government’s way of rewarding the hard work that goes into building a small business, farm, or fishing operation—the very backbone of our economy.

So, what is it? The LCGE lets you sell specific types of assets and keep a huge portion of the profit, completely tax-free. For someone who has spent their life building a family business in Canada, the LCGE could mean hundreds of thousands of dollars stay in your pocket for retirement or your next venture.

What Kinds of Assets Actually Qualify?

This exemption doesn't apply to every investment. Unlike the Principal Residence Exemption that covers your family home, the LCGE is laser-focused on encouraging entrepreneurship in a few key sectors.

To qualify, you need to be selling one of two types of assets:

- Qualified Small Business Corporation (QSBC) Shares: These are shares in a private, Canadian-controlled company that must pass specific tests regarding its assets and business activities. This is the most common path for entrepreneurs.

- Qualified Farm or Fishing Property: This covers assets like land and buildings, but also specific items like fishing licenses or shares in a family farm corporation.

Understanding which assets qualify is the first step in smart tax planning. It allows you to structure your business in a way that keeps the door open for this massive tax break down the road.

It’s a “Lifetime” Limit for a Reason

A crucial detail is that the LCGE is a cumulative, lifetime limit. Think of it like a running total of exemptions you've claimed. You can use it across different sales over many years until you hit your personal maximum. This is great for serial entrepreneurs or anyone who might sell off parts of their business over time.

For example, imagine you sell the small marketing firm you started in Halifax. As of June 25, 2024, the LCGE limit increased from just over $1 million to $1.25 million.

This boost allows owners of a qualified small business corporation (QSBC) to shield up to $1.25 million in capital gains when they sell their shares. The same rule applies to qualified family farms and fishing properties. To understand how the new inclusion rate impacts your total gains, you can get more details from experts at Skyline Wealth Management.

Heads Up: Since the LCGE is a lifetime maximum, you must track how much you use. Every dollar you claim on one sale reduces the amount available for future sales.

This is where a financial tool like NeoSpend proves its worth. By consolidating all your accounts in one place, you can tag transactions related to your business investments. This builds a clear history, making it easier to track your costs, calculate potential gains, and ensure you’re ready to maximize your capital gains exemption when you sell.

For a quick overview, here are the key details you need to know about the LCGE.

LCGE at a Glance Key Details

| Attribute | Details |

|---|---|

| Exemption Limit | $1.25 million of capital gains (as of June 25, 2024). |

| Nature of Limit | Cumulative; can be used across multiple sales over your lifetime. |

| Eligible Assets | Qualified Small Business Corporation (QSBC) shares. |

| Qualified farm or fishing property. | |

| Purpose | To encourage and reward entrepreneurship in Canada. |

| Claimant | An individual Canadian resident (not a corporation or trust). |

This table provides a high-level view, but the details matter. Understanding these rules is the first step toward a plan that could save you a fortune in taxes.

Meeting the Eligibility Rules for Your Business

Claiming the Lifetime Capital Gains Exemption (LCGE) isn’t automatic. The Canada Revenue Agency (CRA) has a specific set of tests your business must pass to qualify for this valuable tax break. Successfully navigating them requires careful planning, especially when it comes to your company’s shares.

Let’s follow the story of Maya, a Toronto-based tech founder getting ready to sell her software startup. She knows that claiming a $1.25 million capital gains exemption would be life-changing. But her accountant has made it clear: everything depends on her company meeting the definition of a Qualified Small Business Corporation (QSBC).

For the shares she plans to sell, there are three critical tests to pass. If she fails even one, the entire exemption could be lost.

The 24-Month Holding Period Test

First, Maya must satisfy the holding period. This rule is simple: for the entire 24 months right before she sells her shares, only she or a related person could have owned them.

This test is designed to reward long-term business builders, not short-term speculators looking to flip shares and claim the exemption. Since Maya founded her company and has held her shares for over five years, she easily passes this first test.

The 50% Asset Use Test

The next test is more complex. It examines what the company has been doing with its assets over that same 24-month period. For Maya’s shares to qualify, more than 50% of the fair market value of her company's assets had to be used in an active business, primarily in Canada.

This rule is a big one. It’s the CRA’s way of ensuring the exemption goes to genuine operating businesses, not holding companies that just sit on passive investments like stocks, bonds, or rental properties unrelated to the main business.

If a company is hoarding too much cash or has significant investments not tied to its core operations, it could fail this test. This is a common pitfall for successful businesses, so it’s something to monitor closely.

The 90% Test at the Time of Sale

Finally, there’s the test at the moment of sale. At this specific point, 90% or more of the fair market value of the company’s assets must be used in an active business. This is often called the "all or substantially all" test.

This is the strictest of the three rules. A company could meet the 50% test for two years, but if it takes on a large passive investment right before the sale, it could fail this final test and be disqualified. That’s why pre-sale financial "purification" to clean up the balance sheet is so important.

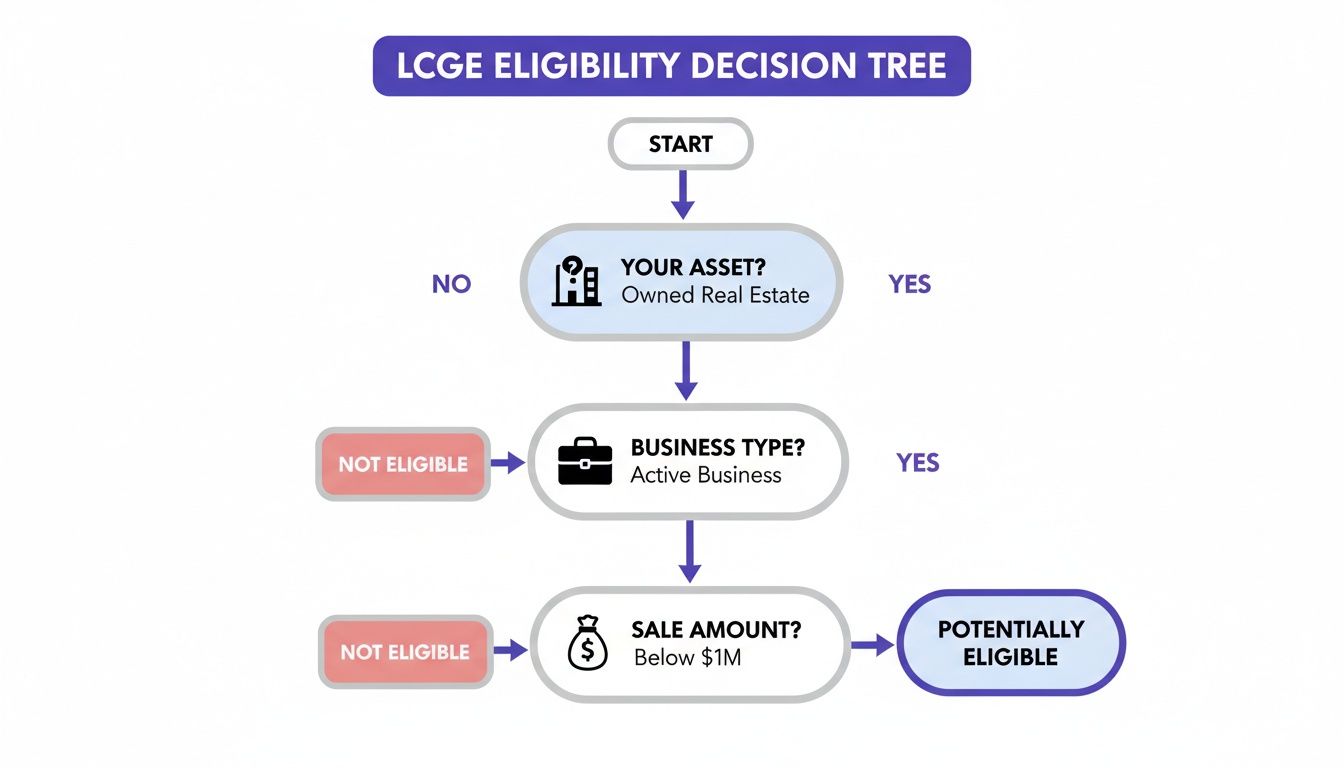

This decision tree gives you a quick visual guide to see if you're on the right track for LCGE eligibility.

As the flowchart shows, qualifying for the capital gains exemption depends on meeting a sequence of conditions related to your asset type, business structure, and sale details. Being proactive is essential.

For business owners like Maya, these rules highlight how critical meticulous record-keeping and smart financial management are. Using a tool like NeoSpend can be a game-changer. By linking your business accounts, you get a real-time view of your company’s financial health, making it much simpler to monitor your asset mix and stay ready for a future sale.

How to Calculate and Claim the Exemption

Understanding the theory behind the Lifetime Capital Gains Exemption (LCGE) is one thing, but applying it to your finances is what really matters. Let’s walk through the steps of calculating your capital gain and claiming this powerful tax break. It’s more straightforward than you might think if your records are in order.

A capital gain calculation is simple math. You take the proceeds of disposition (what you sold the asset for) and subtract your Adjusted Cost Base (ACB) plus any selling expenses. The ACB is your total cost to acquire the asset, including the original price and related fees.

For example, say you sell your qualifying small business shares for $900,000. Your initial investment was $100,000, and you paid $10,000 in legal fees to close the deal.

Your capital gain is: $900,000 (Sale Price) - $110,000 (ACB + Expenses) = $790,000.

Applying the Exemption to Your Gain

Once you have your capital gain, you can apply your available LCGE. Since your $790,000 gain is well under the $1.25 million lifetime limit, you can use the exemption to eliminate your taxable capital gain entirely, saving you from a massive tax bill.

But what if your gain is bigger than the limit? Let’s imagine you sold those same shares for $1.5 million.

- Calculate the Total Capital Gain: $1,500,000 - $110,000 = $1,390,000

- Apply Your LCGE Deduction: You claim your maximum lifetime limit of $1.25 million against that gain.

- Find the Remaining Gain: $1,390,000 - $1,250,000 = $140,000

That leftover $140,000 is your capital gain. The capital gains inclusion rate then determines how much gets added to your taxable income for the year.

Reporting on Your Tax Return

When tax time comes, you need to report the sale and claim the exemption on specific Canada Revenue Agency (CRA) forms. The main ones are:

- Schedule 3, Capital Gains (or Losses): This is where you report the details of the sale, including the proceeds and your adjusted cost base.

- Form T657, Calculation of Capital Gains Exemption: On this form, you calculate the exact LCGE deduction you're claiming for the year.

This is why tracking your ACB and every related expense is so important. Accurate records are your best defence in a CRA audit and ensure you don’t overpay tax. You can learn more about how these rules affect small businesses from the CFIB.

Pro Tip: Your Adjusted Cost Base isn’t static. It can increase over time with capital improvements or further investments. Keeping meticulous records ensures you’re not overpaying on your taxes.

An app like NeoSpend is a must-have for any entrepreneur. Instead of digging through old bank statements, you can tag investment and business transactions as they happen. You’ll build a clear record of your ACB, making the final calculation simple for you and your accountant. With NeoSpend, you turn a major tax-time headache into a smart, ongoing habit.

Common Mistakes and Smart Tax Strategies

Claiming the Lifetime Capital Gains Exemption (LCGE) can be a massive financial win, but the path is lined with tricky Canada Revenue Agency (CRA) rules. One wrong move could cost you hundreds of thousands in tax savings.

Let's review the most common pitfalls and the smart strategies that savvy Canadian business owners use to maximize their capital gains exemption.

The Passive Asset Trap

One of the biggest hurdles is the asset test. As a business succeeds, it’s natural to build up a cash reserve or invest profits in things like stocks or real estate.

The problem? If these passive investments grow too large, the CRA may decide your company’s shares are no longer “Qualified Small Business Corporation” (QSBC) shares, making you ineligible for the LCGE. This is why proactive financial management is essential for tax planning.

How to "Purify" Your Corporation and Stay Compliant

So, how do you solve this? To avoid failing the critical asset tests (the 50% test over 24 months and the 90% test at the time of sale), you may need to "purify" your corporation. This means removing non-qualifying passive assets from your company's balance sheet before the sale.

Common purification tactics include:

- Pay out dividends: Distribute excess cash to shareholders.

- Pay down company debt: Use idle cash to clear business loans.

- Reinvest in the business: Buy new equipment or expand operations.

- Restructure your company: A tax professional might suggest a corporate reorganization to move passive assets into a separate holding company.

The goal of purification is to make your balance sheet clearly reflect an active, operating business. This should be planned well in advance of any potential sale.

Playing the Long Game: Timing and Family Coordination

When it comes to the LCGE, timing is critical. Rushing a sale without proper planning can lead to disqualification.

Family-owned businesses have a unique advantage. Every individual Canadian gets their own $1.25 million lifetime limit, meaning families can multiply their tax savings. If you, your spouse, and your adult children all own qualifying shares, each person can claim their own LCGE. For instance, a couple from Calgary who each own 50% of a qualifying business could potentially shelter up to $2.5 million in capital gains. This requires careful structuring of share ownership long before a sale is on the horizon.

Putting Capital Losses to Work

What happens if your gain exceeds your exemption limit? This is where capital losses become a useful tool. If you have other investments that have lost value, you can sell them to "realize" that loss.

You can use capital losses to cancel out capital gains in the same year. If you have more losses than gains, you can carry them back three years or forward indefinitely to offset future gains. This is a powerful way to neutralize any taxable gains that the LCGE doesn't cover. For a deeper dive, explore guides on how capital gains are taxed in Canada from sources like Taxes for Expats.

Common LCGE Mistakes vs. Smart Solutions

Here’s a quick look at common tripwires and how to sidestep them.

| Common Pitfall | Strategic Solution |

|---|---|

| Holding too many passive assets | Purify the corporation by paying dividends, clearing debt, or reinvesting in active assets well before a sale. |

| Last-minute planning | Start planning your exit strategy and LCGE claim at least two years before you intend to sell. |

| Ignoring family members' exemptions | Structure share ownership (e.g., via a family trust) to allow multiple family members to claim their individual LCGEs. |

| Forgetting to track the 24-month holding period | Keep meticulous records to ensure you’ve held the shares for the required period before the sale. |

| Not using capital losses effectively | Review your entire portfolio to identify and realize losses that can offset gains exceeding the LCGE limit. |

Juggling asset purity, sale timing, and loss harvesting is where a tool like NeoSpend can be your co-pilot. It helps you monitor your business and investment accounts, giving you the insights to know when it’s time to call your advisor. By keeping your financial picture organized, NeoSpend helps you stay on track to maximize your capital gains exemption.

What This All Means for Your Wallet

The key takeaway from this guide is that the $1.25 million Lifetime Capital Gains Exemption (LCGE) is a massive opportunity for Canadian entrepreneurs. It's not just a line on a tax form; it's a cornerstone of smart financial planning that can shape your journey from startup to a successful exit.

The main principles are simple: understand the rules early, prioritize long-term planning, and be diligent about record-keeping. Waiting until a buyer comes along is often too late. You need to be proactive about managing your company's assets and share structure today.

Think of Planning as an Opportunity, Not a Chore

This is where a modern tool like NeoSpend can make a real difference. Instead of wrestling with spreadsheets, you can use it to automatically categorize transactions and tag business expenses as they happen. This helps you build an accurate, real-time record of your adjusted cost base without the headache.

Tax planning isn't a burden—it's an opportunity to maximize the wealth you've worked so hard to build. A clear financial picture is the first step toward confident decision-making.

When you have a single, clear view of your finances, you are in a position of power. A simple dashboard can help you spot potential red flags—like a growing balance of passive assets—long before they threaten your LCGE eligibility.

Your Next Move Towards Financial Clarity

Successfully claiming the LCGE comes down to diligence and foresight. It means treating your business not just as a job, but as a financial asset that needs careful management to maintain its tax-advantaged status.

So, what's the first step? Get a complete picture of your money. Connect your accounts to NeoSpend to see where your money is going, monitor your business’s financial health, and start mapping out your future with confidence.

Explore how NeoSpend helps Canadians get smarter with their money and prepare for their biggest financial goals.

Got Questions? We've Got Answers

Digging into the capital gains exemption often brings up more questions. It’s a complex topic, so to provide clarity, here are plain-language answers to the questions we hear most often from Canadian entrepreneurs and investors.

Can I Use the LCGE for My Publicly Traded Stocks?

Many Canadians wonder if profits from selling shares in public companies like Shopify or RBC can be sheltered by the Lifetime Capital Gains Exemption (LCGE).

The answer is a clear no. The LCGE is specifically designed to reward those building Canada's small businesses. It only applies to gains from selling Qualified Small Business Corporation (QSBC) shares—shares in a private, Canadian-controlled company that meets strict asset tests.

What if My Gain Is Bigger Than the Exemption Limit?

First, congratulations—that’s a great problem to have. If your capital gain is more than the $1.25 million LCGE limit, you don't lose the benefit; you simply pay tax on the excess amount.

For example, if you sell your qualifying business with a $1.4 million capital gain, you can use your full $1.25 million exemption to make that portion of the profit tax-free. The remaining $150,000 is a taxable capital gain, and the standard inclusion rate determines how much of that is added to your income for the year.

Is the Principal Residence Exemption the Same as the LCGE?

It's easy to confuse these two, but they are completely different tools for different assets.

- The Principal Residence Exemption allows you to sell your main home without paying tax on the profit. It applies only to the property you live in.

- The Lifetime Capital Gains Exemption is for selling specific business, farm, or fishing assets.

They operate independently with their own rules and limits. You can't use the LCGE on your house, and you can't use the principal residence exemption on your business shares.

Can My Spouse and I Both Claim the Exemption?

Absolutely, and this is where smart family tax planning is key. The LCGE is an individual exemption, meaning every Canadian resident has their own personal $1.25 million lifetime limit.

If you and your spouse both own qualifying shares in the same business, you can each claim your own LCGE when you sell. This could potentially shield up to $2.5 million in capital gains for your family. The catch is that share ownership must be structured correctly long before a sale is considered.

Key Takeaway: The Lifetime Capital Gains Exemption is a powerful tool, but qualifying requires careful, long-term planning. Start by understanding the rules, keeping meticulous records, and actively managing your business assets to ensure they remain "active." A proactive approach is the best way to secure this valuable tax benefit.

Ready to get organized for a future sale? With NeoSpend, you can track your business investments and expenses in one place, ensuring you have the crystal-clear financial records needed to maximize your capital gains exemption. Take control of your financial future with NeoSpend today.