Think of the Canadian taxation year as your financial report card. For most Canadians, this report card covers the same period every year: January 1 to December 31. It’s the official 12-month window the Canada Revenue Agency (CRA) uses to tally up your income, review your deductions, and figure out what you owe.

What is the Canadian Taxation Year?

It’s easy to gloss over the term, but your taxation year is the foundation of your entire financial life in Canada. It dictates which T4 slips you need, which expenses you can write off, and even the deadline for your RRSP contributions. Understanding this concept is the first step to getting a handle on your taxes instead of letting them handle you.

For example, when you file your 2023 taxes, you are reporting all the income you earned between January 1, 2023, and December 31, 2023. This fixed timeline ensures you’re not just reacting to tax season—you’re planning for it.

Why Does This 12-Month Window Matter So Much?

Having everyone on the same January-to-December schedule creates a level playing field. It’s a simple, consistent system that ensures millions of Canadians are measured by the same financial yardstick each year, which is essential for a fair tax system.

For the 2023 tax year, for example, the CRA's federal brackets started at 15% for income up to $53,359 and climbed to 33% for anyone earning over $235,675. Every dollar you earn within that January-to-December window counts, which is why understanding your bracket is so important. You can dig into the details on Canada's tax bracket statistics to see exactly how your income stacks up.

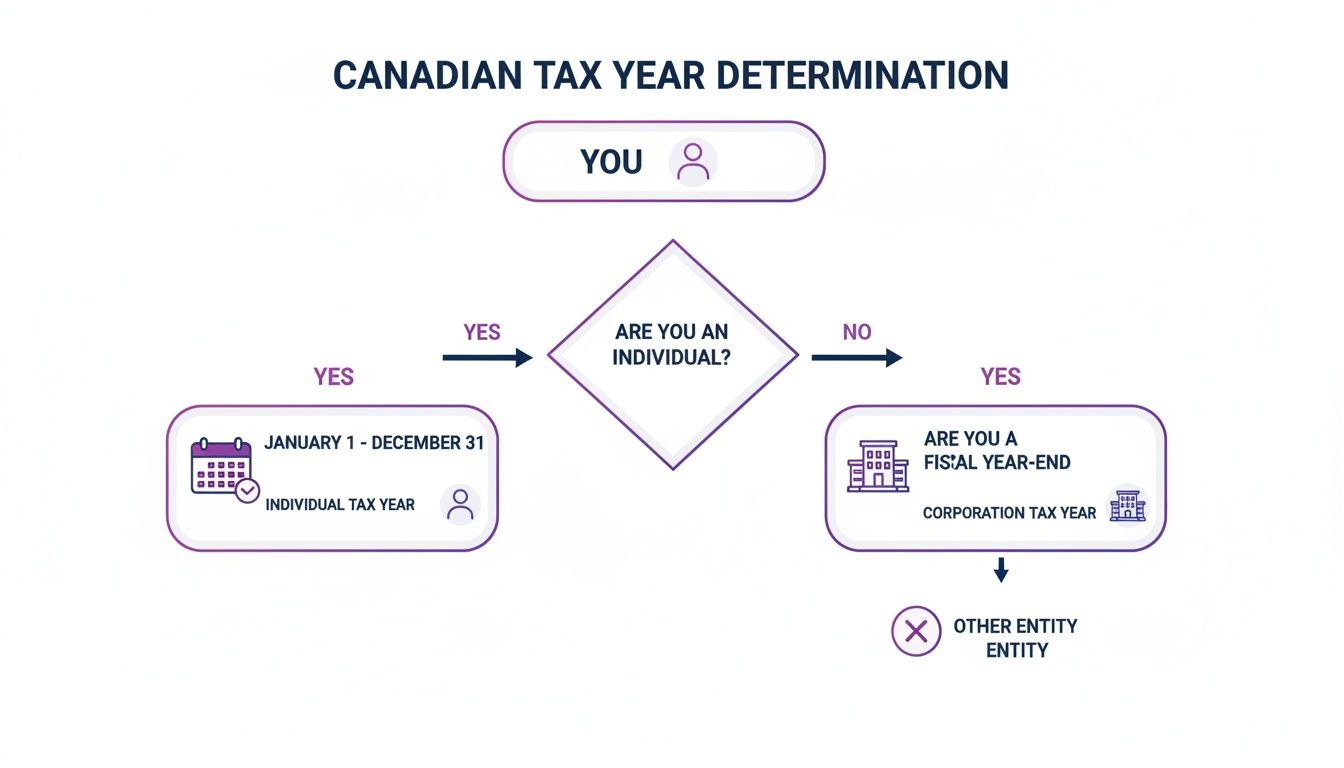

This simple decision tree breaks it down: as an individual, your path is set. For businesses, it’s a different story.

As you can see, the path for individuals is straightforward. This fixed timeline makes tracking your finances much less of a headache than it is for corporations, who have a bit more flexibility.

How It Shapes Your Financial Habits

Once you truly get that your financial year is January to December, you can stop being reactive and start being proactive. Instead of scrambling to find receipts and slips in April, you can track your income and expenses as they happen, giving you a much clearer picture of where you stand.

The secret to a stress-free tax season isn't finding a magic loophole in April; it's staying organized from January to December.

This is where a tool like NeoSpend helps people manage money smarter. It automatically sorts your spending as it happens, so you can see a real-time snapshot of your financial life within the current taxation year. You can tag deductible expenses on the fly, keep an eye on your income, and head into tax season feeling prepared and in control.

The Difference Between a Fiscal Year and a Calendar Year

One of the biggest head-scratchers in Canadian taxes is the “fiscal year vs. calendar year” concept. If you’re an employee or sole proprietor, your financial world runs from January to December—a calendar year. But for incorporated businesses, the rules are more flexible, allowing them to choose a fiscal year for better financial planning.

For individuals, sole proprietors, and partnerships, the taxation year is set in stone. It always runs from January 1 to December 31. This keeps things straightforward for personal tax filing, making sure everyone reports their income and expenses over the same 12-month stretch.

Why Incorporated Businesses Get to Choose a Fiscal Year

Incorporated businesses get a special perk: they can choose their own 12-month reporting period, known as a fiscal year (or fiscal period). It can start on the first day of any month and end on the last day of the month right before it in the following year. This is a strategic move that lets a company sync its tax reporting with its natural business rhythm.

A fiscal year is a strategic tool that allows a corporation to match its tax obligations to the rhythm of its revenue stream, not the other way around.

Consider a ski resort in Whistler. Its prime money-making season is from November to March. If it used a calendar year, its peak season would be split between two tax years, making it difficult to analyze performance. By choosing a fiscal year that ends after the snow melts—say, April 1 to March 31—the company gets a clean, complete picture of a single season's success.

Understanding the Key Differences: Calendar Year vs. Fiscal Year

It all boils down to your business structure. Knowing which timeline applies to you is absolutely critical for getting your taxes right.

| Feature | Calendar Year | Fiscal Year |

|---|---|---|

| Who Uses It | Individuals, sole proprietors, and partnerships. | Incorporated businesses only. |

| Timeline | Always January 1 to December 31. | Any consecutive 12-month period chosen by the corporation. |

| Flexibility | None. The timeline is fixed by the CRA. | High. Can be aligned with seasonal business cycles. |

| Deadline Impact | Personal filing deadline is April 30. | Corporate filing deadline is six months after the fiscal year-end. |

This flexibility for corporations is a core part of Canada's approach to business taxation. For instance, Canada's corporate tax rate has come down significantly from a high of 50.90% in 1981 to a much more stable 26.50% in recent years. That rate is applied to a corporation's fiscal period, which can have a real impact on financial reporting. You can explore more historical data on Canadian corporate tax rates on TradingEconomics.com.

Why Freelancers Must Use the Calendar Year

If you're a freelancer or running a side hustle as a sole proprietor, you might be wondering why you don't get to pick a fiscal year. The answer is simple: your business income is reported directly on your personal T1 income tax return.

Since your personal taxes are strictly based on the calendar year, your business income has to follow suit. This keeps everything aligned and avoids the headache of trying to merge two different reporting periods onto a single tax form. It's a crucial distinction for the millions of self-employed Canadians navigating their tax obligations.

No matter which tax year you use, staying organized is non-negotiable. Using a tool like NeoSpend helps you track every dollar, tag business expenses on the fly, and get a clear financial picture that lines up perfectly with your calendar year. It turns tax prep from a frantic annual scramble into a simple, year-round habit.

Tax Rules for Self-Employed Canadians and Freelancers

Jumping into the world of self-employment is a huge milestone, but it also means navigating a different set of tax rules. While your Canadian taxation year is the same as everyone else's—January 1 to December 31—the deadlines and your responsibilities look a little different. Getting these details right is the key to keeping the CRA happy and your business finances in good shape.

The first major difference you'll notice is in the deadlines. As a self-employed person, the CRA gives you until June 15 to file your tax return.

But here’s the catch that trips up so many new freelancers: while you get more time to file, you don’t get more time to pay. Any tax you owe for the previous year is still due on April 30. If you miss that payment date, the CRA starts charging compound daily interest on whatever you owe, even if you file your return on time in June.

The World of Tax Instalments

Once your freelance business takes off, paying taxes might become more than just a once-a-year event. If your net tax owing climbs above $3,000 for the current year (and in either of the two previous years), the CRA will ask you to pay your income tax in quarterly instalments.

Think of it as a pay-as-you-go plan for your taxes. Instead of facing a massive bill every spring, you prepay an estimated amount throughout the year. For example, if you expect to owe $4,000 in taxes for the year, you would pay $1,000 each quarter. The CRA will even send you instalment reminders with suggested amounts based on your past income.

"Tax instalments are the CRA's way of levelling the playing field. They ensure self-employed individuals contribute throughout the year, just like employees do through payroll deductions."

The payment dates are the same every year, making them easy to plan for:

March 15

June 15

September 15

December 15

Missing these payments can lead to interest and penalties, so it’s smart to build them right into your business budget.

Master Your Income and Expense Tracking

The secret to a stress-free tax season? Meticulous record-keeping. Every dollar you earn and every eligible business expense you incur needs to be tracked. This is where modern financial tools can be a game-changer. Forget the shoebox stuffed with crumpled receipts.

For instance, using a tool like NeoSpend to manage your personal finances can make tax prep almost automatic. You can link your business bank account and credit cards, and the app starts sorting your transactions for you. You can add custom tags like "Business Travel," "Office Supplies," or "Client Lunch" to a purchase the second you make it.

Come tax time, you can skip the weeks of painful admin. Just generate a report of your tagged business expenses, and you’ll have a clean, accurate summary of your deductions for the Canadian taxation year. This kind of proactive tracking doesn't just save time and stress—it ensures you claim every deduction you’re entitled to.

Beyond the Basics: Other Tax Timelines You Need to Know

While the main Canadian taxation year sets the pace for your financial life, a few other important timelines run on their own schedule. Getting a handle on these is a game-changer for smart tax planning. Think of them as opportunities to lower your tax bill and stay on the CRA’s good side.

If your main tax year is the highway, these other periods are the strategic off-ramps. They have their own rules and deadlines, and knowing how to navigate them means you won't miss out on some serious financial advantages.

The Famous RRSP Contribution Window

This is probably the one most Canadians have heard of. The deadline to contribute to your Registered Retirement Savings Plan (RRSP) for a specific tax year isn't December 31. It’s actually 60 days into the following year, which usually means March 1 (or February 29 in a leap year).

This 60-day grace period is an incredibly powerful tool. It gives you breathing room after the year ends to look at your final income numbers and figure out how much you want to contribute to shrink your tax bill.

For instance, any contribution you make in January or February of 2024 can be claimed on your 2023 tax return. It’s a fantastic last-minute play to lower your taxable income for the year that just wrapped up.

Making the 60-Day RRSP Window Work for You

So, what does this look like in a real-world Canadian scenario? Let’s break it down.

Scenario: Meet Chloe, a freelance graphic designer in Toronto. When she’s wrapping up her books in January 2024, she realizes her 2023 income was higher than she expected, bumping her into a higher tax bracket.

Action: She still has contribution room in her RRSP. So, in February 2024, she moves $5,000 into her RRSP account.

Result: Because she made that deposit within the first 60 days of the new year, she can claim that $5,000 as a deduction on her 2023 return. This lowers her taxable income for the previous year and cuts down her tax bill.

This simple move can save you hundreds, if not thousands, of dollars. This is where tools like NeoSpend really shine. They give you a clean, year-end summary of your income, making it easy to see if a last-minute RRSP top-up makes sense for you.

GST/HST Reporting Periods for Businesses

If you're self-employed or run a small business, the Goods and Services Tax (GST) or Harmonized Sales Tax (HST) reporting period is another critical timeline to watch. This cycle operates completely separately from your income tax filing and is tied directly to your business’s annual revenue.

When you register for a GST/HST account, the CRA will assign you a reporting frequency. It usually falls into one of three buckets:

Annually: For smaller businesses with sales of $1.5 million or less. Your return and payment are generally due three months after your fiscal year ends.

Quarterly: For businesses with sales between $1.5 million and $6 million. Returns and payments are due one month after the end of each fiscal quarter.

Monthly: For businesses with sales over $6 million. You’ll need to file and pay one month after the end of each month.

Staying on top of your GST/HST isn't just good practice—it's non-negotiable. Missing these deadlines can trigger penalties and interest charges that chip away at your hard-earned profit.

Juggling these separate deadlines demands solid organization. A smart expense tracking app like NeoSpend can help you monitor your revenue in real-time. By tagging your sales, you can easily watch your income grow and know exactly when you might need to change your GST/HST reporting frequency, keeping you compliant and stress-free.

Common Tax Year Mistakes and How to Avoid Them

Figuring out the Canadian taxation year can feel like a maze, but most of the costly mistakes boil down to a few common, and totally avoidable, slip-ups. Every year, people get hit with unnecessary penalties and stress just from overlooking a few key details.

Getting a handle on these common pitfalls is the first step to making your tax season smoother. It usually comes down to two things: timing and organization. From freelancers missing a crucial payment deadline to investors getting their contribution windows mixed up, simple errors can have a big financial impact. The good news? With a little planning and the right tools, you can sidestep them completely.

The Self-Employed Deadline Trap

This is a big one. If you're self-employed, you know you get until June 15 to file your tax return. But here’s the catch that trips so many people up: your tax payment is still due on April 30. If you miss that payment date, even if you file on time in June, the CRA will start charging compound daily interest on whatever you owe.

And in the current economic climate, you can bet they’re paying close attention. With government deficits in the billions, as highlighted in reports like this one on Canada's fiscal outlook from RBC Economics, making sure revenue comes in on time is a top priority.

The fix is simple: set a reminder for mid-April. Use that time to get a good estimate of your taxes and send the payment off, long before your filing deadline.

Misunderstanding the 60-Day RRSP Rule

The 60-day RRSP contribution window is a fantastic tax-planning tool, but it's also a source of major confusion. When you contribute to your RRSP in January or February, you have the option to claim that deduction on the tax return for the year that just ended. The mistake happens when people either forget to claim it at all or accidentally claim it on the current year's return instead.

Forgetting to properly claim a contribution made in the first 60 days of the year is like leaving free money on the table. You miss out on a tax deduction that could have lowered your bill for the year that just ended.

To stay on top of this, always check your RRSP slips carefully. Your financial institution will issue a specific slip for any contributions made between January 1 and March 1. Make sure that amount gets entered on the correct line of your prior-year tax return.

Poor Record Keeping

Let’s be honest, this is probably the most common and damaging mistake of all: not keeping your records organized. It doesn't matter if you're a freelancer trying to track down every last business expense or someone hoping to claim medical costs—a messy paper trail can mean missed deductions and a massive headache if the CRA comes knocking.

This is exactly where having a dedicated financial tool changes the game. Instead of digging through a shoebox full of crumpled receipts in April, an app like NeoSpend lets you categorize transactions and tag deductible expenses as you go. By turning financial organization into a year-round habit, you make sure every single eligible deduction is captured. Tax prep suddenly goes from a frantic scramble to a simple, straightforward review.

To help you stay ahead, we've put together a quick reference table of these common slip-ups and how to handle them.

Common Taxation Year Mistakes and Solutions

| Common Mistake | Why It Happens | How to Avoid It |

|---|---|---|

| Missing the Self-Employed Payment Deadline | Confusing the June 15 filing deadline with the April 30 payment deadline. | Set a calendar alert for mid-April to calculate and pay your estimated tax liability. Treat the two deadlines as separate events. |

| Incorrectly Claiming RRSP Contributions | Forgetting that contributions in the first 60 days of the year can be claimed on the previous year's return. | Carefully review your RRSP contribution slips. Ensure amounts from Jan 1 - Mar 1 are applied to the correct tax year. |

| Disorganized Expense Records | Leaving all receipt and invoice organization until tax season, leading to missed deductions or incomplete documentation. | Use a digital tool like NeoSpend to track and categorize expenses in real-time throughout the year. |

| Forgetting GST/HST Deadlines | Treating GST/HST reporting periods and deadlines the same as income tax deadlines, which they are not. | Check your specific GST/HST reporting period (monthly, quarterly, or annually) and mark all filing and payment dates in your calendar. |

Remembering these key points can save you a lot of time, money, and stress when tax season rolls around. A little organization goes a long way.

Your Year-Round Tax Prep Checklist

Knowing how the Canadian tax year works is one thing. Putting that knowledge into action is how you really take control of your money. Instead of getting blindsided by tax season every spring, a year-round approach turns that mad dash into a calm, organized process. This breaks down a huge task into small, manageable chunks, quarter by quarter.

This simple checklist helps you build a habit of staying on top of your finances all year long. When you're always a few steps ahead, you won't have to worry about missing a deadline or a valuable deduction.

Quarter 1 (January to March): The Final Push

The first three months of the year are a balancing act. You're closing the books on last year's taxes while also getting things in order for the new year. This is your last chance to make moves that will lower the tax bill you're about to file.

Gather Your Slips: Your T4s, T5s, and RRSP contribution slips will start showing up. Get a dedicated folder—physical or digital—and pop them in as they arrive.

Make Last-Minute RRSP Contributions: The clock is ticking! You have until 60 days into the new year (usually March 1st) to contribute to your RRSP and still get the deduction on last year's return.

Organize Your Receipts: If you're claiming business expenses, medical costs, or charitable donations, now's the time to get them all together and add them up.

Quarter 2 (April to June): File and Plan

This quarter is all about the big deadlines. It's when you finally file your return and settle up with the CRA for last year. But just as importantly, it's the perfect moment to start fresh for the current year.

File and Pay by April 30: For most Canadians, this is the big one. It's the last day to file your return and pay any taxes you owe without getting hit with penalties.

Self-Employed Filing Deadline: If you or your spouse work for yourselves, you get until June 15 to file. But remember, your payment is still due on April 30.

Start the New Year's Records: Once last year's return is out the door, wipe the slate clean. Start a new system for the current year and begin tracking your income and expenses right away.

Quarter 3 (July to September): The Mid-Year Check-In

With the filing chaos behind you, summer is the perfect time for a quick financial check-in. It's your chance to see how the current tax year is shaping up and make any course corrections to avoid a nasty surprise next spring.

A mid-year financial review is your early warning system. It helps you spot potential tax issues while you still have plenty of time to fix them.

The main thing to look at here is your income. If you're self-employed and you've had a better year than you expected, you might need to start making quarterly tax instalments. This breaks up a huge tax bill into smaller payments and helps you avoid penalties. The next instalment is due September 15.

Quarter 4 (October to December): Strategic Year-End Moves

The final stretch of the year is your last chance to make some smart moves and optimize your tax situation before everything is locked in on December 31. The decisions you make now can have a real impact on the return you'll be filing in a few months.

Tax-Loss Selling: Look at your non-registered investment accounts. If you have some investments that have lost value, selling them can create a capital loss. You can use that loss to cancel out capital gains from your winning investments.

Make Charitable Donations: Any donation you make by December 31 can be claimed as a tax credit for that year.

Review Your Pay Stub: Got a bonus or a raise this year? It’s a good idea to double-check your pay stubs and make sure your employer has been taking off enough tax.

Keeping this rhythm all year is so much easier with tools like NeoSpend. It can automatically categorize your transactions and give you a clean dashboard to see where your money is going. It helps turn tax prep from a once-a-year headache into a simple, continuous habit.

Got Questions? We've Got Answers

Even after you get the hang of things, specific situations can throw you a curveball. Let's tackle some of the most common questions that pop up about the Canadian taxation year.

I Moved to Canada Mid-Year. Do I File for the Whole Year?

No, you only report income for the part of the year you were officially a resident for tax purposes.

Let's say you landed in Calgary and became a resident on August 1. Your first Canadian tax year would run from August 1 to December 31. You'll report any worldwide income you earned during that five-month window to the CRA. For the income you earned before your move, you'll handle that with the tax authorities in your previous country.

Can I Pick a Fiscal Year for My Side Hustle?

This one trips a lot of people up. If your side gig is set up as a sole proprietorship or a partnership, the answer is no. You’re required to use the standard January 1 to December 31 calendar year.

Why? Because the CRA wants your business income reporting to line up perfectly with your personal T1 tax return, keeping things simple. The only way to get the flexibility of choosing a different 12-month fiscal period is to officially incorporate your business.

What Happens If I Miss the April 30 Payment Deadline?

This is a big one for freelancers and the self-employed. You might get until June 15 to file your paperwork, but your tax payment is still due on April 30. No exceptions.

Missing that payment deadline hurts. Starting on May 1, the CRA begins charging compound daily interest on whatever you owe. That interest piles up every single day until you’ve paid off the entire balance, turning a manageable tax bill into a much bigger problem.

The best defence here is a good offence. When you track your income and expenses all year, you have a much better idea of what you’ll owe. That way, you can set money aside and avoid any nasty surprises come springtime.

Key Takeaway

Understanding the Canadian taxation year is the first step toward financial empowerment. For most individuals, it's a simple January to December calendar, but knowing the key deadlines for RRSPs, self-employment, and GST/HST can save you significant money and stress. By adopting a year-round approach to financial tracking, you can transform tax season from a dreaded chore into a confident, organized process.

Staying on top of your finances is easier with the right tools. With NeoSpend, you get a clear view of your money, making it simple to track every dollar, budget effectively, and walk into tax season feeling prepared and in control. Explore more financial tips on our blog to keep learning.