Ever feel like your money has a mind of its own? One minute your account is healthy, and the next you're wondering where it all went. You're not alone. The key to taking back control isn't complicated spreadsheets or restrictive diets for your wallet; it's finding the right financial partner. That's where modern Canadian budgeting tools come in. They aren't just expense trackers; they’re smart guides built to navigate our unique financial landscape—from TFSAs and RRSPs to everyday spending at Loblaws or Tim Hortons.

Why Canadian-Specific Budgeting Tools Are a Game-Changer

Managing money in Canada has its own set of rules. We have unique savings vehicles like the Tax-Free Savings Account (TFSA) and the Registered Retirement Savings Plan (RRSP), and our financial strategies need to account for them. This is where most generic, international budgeting apps fall short, leaving you to piece together the full picture yourself.

A budgeting tool built for Canadians understands this from the ground up. Think of it as a financial guide that speaks your language. It connects securely to Canadian banks like RBC, TD, and Scotiabank, and it automatically recognizes transactions you’d make every day—like your weekly grocery run or topping up your Presto card.

The Shift from Manual Spreadsheets to Smart Apps

For years, spreadsheets were the go-to for anyone trying to manage their money. While they can work, they require constant manual updates, are prone to errors, and offer zero real-time feedback. Forget to log a few coffees or an online purchase, and your entire budget is thrown off.

Today’s smart budgeting tools eliminate that manual labour. They sync directly with your accounts to provide a live, accurate picture of your finances. This isn’t just about convenience; it’s about getting an honest look at your money and saving valuable time. A tool like NeoSpend, for example, consolidates everything into one simple, clear dashboard, so you can see your entire financial life in seconds, not hours.

It's no surprise that millions of Canadians are embracing these tools. As our comfort with mobile banking grows and interest in personal finance skyrockets, fintech apps have become essential. You can read more about the growing use of these fintech tools and see the full analysis.

Key Benefits of a Dedicated Canadian Tool

Choosing a tool designed with Canadians in mind offers powerful advantages that can transform how you manage your money.

- Effortless Tracking: See exactly where every dollar goes without manually entering a single transaction. For example, your monthly Rogers bill and weekly Sobeys shop are automatically categorized for you.

- Canadian-Specific Insights: Get a clear, consolidated view of your TFSA and RRSP contributions alongside your daily spending.

- Reduced Financial Stress: Eliminate the guesswork and anxiety that comes from not knowing where your money is going.

- Smarter Goal Setting: Set and track realistic goals that feel achievable, whether it’s saving for a down payment in Calgary or a vacation to the Maritimes.

By using a tool that truly understands our financial system, you’re not just tracking expenses—you're building a smarter, more confident relationship with your money.

What to Look for in a Top Canadian Budgeting Tool

So, what separates a basic app from a tool that genuinely improves your financial life? It comes down to features designed for the way we live and bank in Canada. While many apps can track spending, the best Canadian budgeting tools go deeper. They understand our banking system, our unique savings accounts, and our everyday spending habits.

The most critical feature is a secure, reliable connection to Canadian banks. This means seamless integration with major institutions like RBC, TD, and BMO, as well as credit unions like Vancity or Meridian. This direct link is the engine that powers the tool, automatically importing your transactions so you’re not stuck manually entering data from receipts.

This automation is what turns budgeting from a dreaded chore into a simple, effortless habit. When your app syncs daily, you get a real-time, honest view of your financial health.

Track More Than Just Your Chequing Account

To get a true handle on your finances, you need to see the whole picture—not just your chequing account balance. This is where Canada-specific features are essential. A generic app built for the U.S. market likely won't understand a Tax-Free Savings Account (TFSA) or a Registered Retirement Savings Plan (RRSP).

A great Canadian tool is designed to track these accounts properly. It will help you monitor your contribution room, see how your investments are performing, and understand how these long-term savings contribute to your overall net worth.

A powerful tool like NeoSpend doesn’t just show your TFSA balance. It visualizes how close you are to maxing it out for the year, turning a large, intimidating goal into a clear, actionable plan.

This level of detail is crucial for serious long-term financial planning in Canada.

Smart Categories That Understand Canadian Life

An effective budgeting tool should understand what it means to live in Canada. While automated transaction categorization is a standard feature, its intelligence can vary significantly. A top-tier app will recognize uniquely Canadian merchants and bills, sorting them correctly without any manual intervention.

- Recurring Bills: It knows that payments to Bell, Rogers, or Telus are for phone and internet, and it properly identifies your hydro bills.

- Transit Costs: It recognizes a charge from Presto or Compass and automatically categorizes it as "Transportation."

- Common Retailers: It doesn't get confused by your weekend trip to Canadian Tire or Shoppers Drug Mart.

This local intelligence saves you a significant amount of time you'd otherwise spend manually sorting every purchase. With a tool like NeoSpend, the AI even learns from your habits. If you consistently tag your Tim Hortons runs as "Coffee," it will start doing it for you automatically.

Go Beyond Budgeting with Advanced Insights and Goals

Once you have the basics covered, the best Canadian budgeting tools help you build wealth and achieve your biggest life goals. This is where the app transforms from a simple expense tracker into a true financial partner.

Here are a few game-changing features to look for:

- Net Worth Tracking: This is your ultimate financial report card. It aggregates all your assets (bank accounts, investments) and subtracts your liabilities (credit cards, loans, mortgage). Watching this single number grow month after month is one of the most powerful motivators available.

- Custom Goal Setting: Saving for a down payment on a home or a trip to Banff? The app should let you create specific, time-based goals. It can then show you exactly how much to set aside each month and celebrate your progress along the way.

- Bill and Subscription Management: This is an underrated feature. A good tool will identify all your recurring payments, from Netflix to car insurance. It helps you avoid late fees and, more importantly, flags "subscription creep"—those forgotten free trials that are quietly draining your account.

These features don't just provide data; they offer actionable insights. They help you answer important questions like, "Am I on track for retirement?" or "Can we afford a kitchen renovation next year?" By connecting all the dots, the right tool gives you the confidence to make smarter financial decisions.

How to Choose the Right Budgeting Tool for You

With so many budgeting apps available, choosing the right one can feel overwhelming. It’s easy to be distracted by flashy features, but the key is to focus on what you actually need to achieve your financial goals.

A tool that’s perfect for a freelance designer with a fluctuating income won't be the best fit for a family coordinating household expenses. The goal isn't just to download another app you'll forget in a week; it's to find a long-term financial partner that grows with you.

Think of it like choosing a gym. The fanciest one isn't necessarily the best; the best one is the one you'll actually use consistently. Let’s create a simple framework to help you find the right tool for your financial journey.

Start With Your Personal Finance Goals

Before you download anything, ask yourself a simple question: "What am I trying to achieve with my money?"

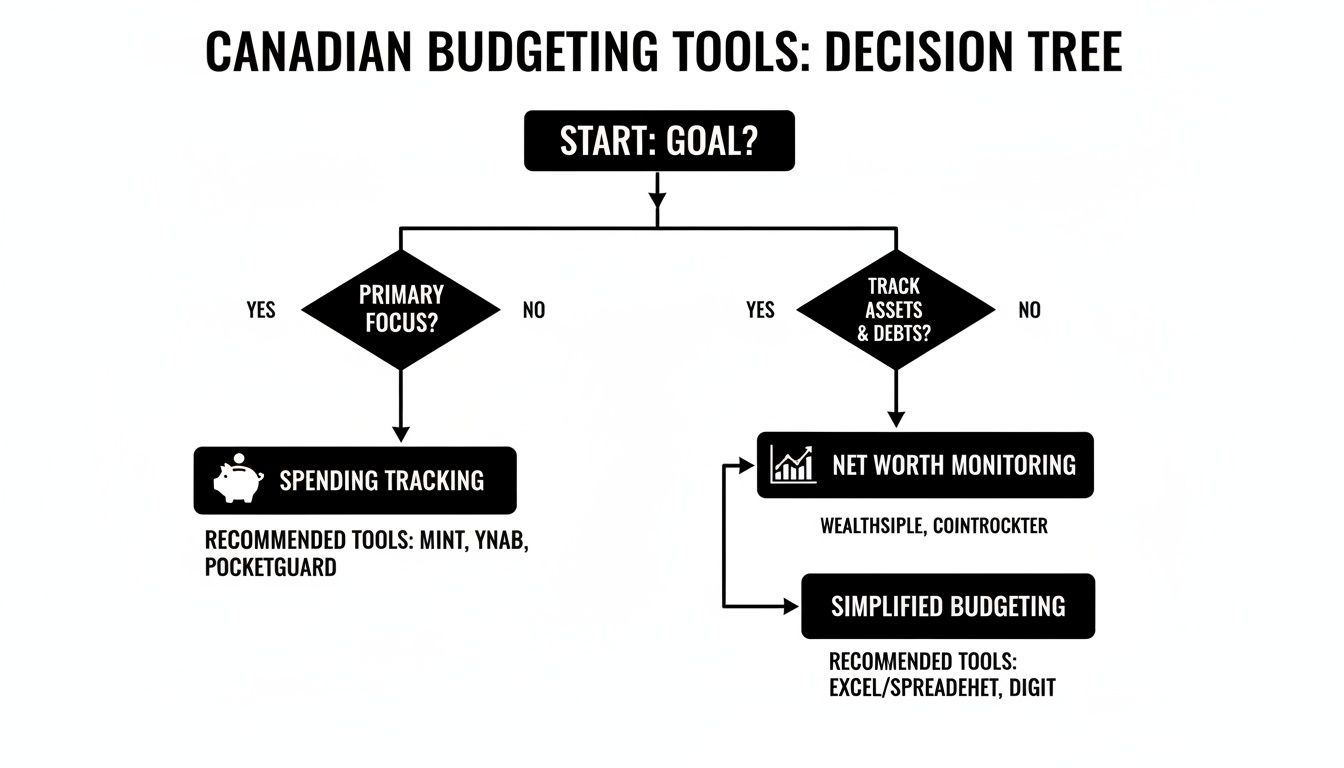

Your answer is the most important factor in this decision. Are you trying to aggressively pay down student debt? Or is your focus on building your net worth for retirement? Maybe you just want to figure out where your money is going each month.

Different goals require different tools. If your main objective is tracking daily spending, a straightforward expense tracker might suffice. But if you're juggling a mortgage, TFSAs, and RRSPs, you’ll need a more robust tool that can consolidate everything and provide a complete financial picture.

This decision tree illustrates how your primary goal can guide you toward the right type of Canadian budgeting tool.

The key takeaway is that your "why" should always determine your "what." Define your objective first, and the selection process becomes much clearer.

Create Your Evaluation Checklist

Once you’ve defined your goals, create a personal checklist to compare different apps. Don't get overwhelmed by evaluating every single feature. Instead, focus on the criteria that will make the biggest impact on your financial life.

Here are some non-negotiable items to look for:

- Security: Does the app use bank-level encryption (like 256-bit AES encryption) and offer two-factor authentication (2FA)? Look for a transparent privacy policy that clearly states they won't sell your data.

- Ease of Use: Is the interface intuitive, or does it feel complicated? A confusing setup is a surefire way to make you abandon the tool. A great tool should feel empowering, not frustrating.

- Canadian Bank Connections: Can it securely and reliably connect to all your Canadian financial institutions, including major banks, online banks, and local credit unions?

- Features for Your Life Stage: Look for tools that match your current needs. A student might want features for tracking student loans, while a growing family might need a way to collaborate on a household budget.

- Cost vs. Value: What are you getting for your money? Many excellent tools offer a free version for basic needs, with paid tiers unlocking more advanced features.

A powerful platform like NeoSpend is designed to meet these criteria, delivering robust security, a user-friendly experience, and features tailored to different Canadian life stages, ensuring you get real, lasting value.

Understanding the Cost of Canadian Budgeting Tools

Pricing for personal finance apps in Canada varies, but you can get a surprising amount of value for free. Most consumer apps offer capable free tiers or affordable premium plans.

A premium subscription typically costs between CAD $10 to $15 per month, often with a discount for an annual plan. More important than the price, however, is ensuring the app is truly built for Canadians. Look for features like support for Canadian tax-advantaged accounts and bilingual customer service, as these details often make the biggest difference. You can learn more about the budgeting app market in Canada to see how different options compare.

Ultimately, the best Canadian budgeting tools are the ones that align with your goals, feel effortless to use, and give you the confidence to take control of your finances.

Getting Your Budgeting App Set Up for Success

The first hour you spend with a new budgeting app is crucial. It’s the moment you turn a good intention into a sustainable habit. A smooth setup process builds the momentum you need to stick with it for the long haul.

Think of it like assembling new furniture. When the instructions are clear and the pieces fit together easily, you feel a sense of accomplishment. But if it's a confusing mess, you're more likely to give up.

Let’s walk through the right way to get set up for success from day one.

The First Step: Securely Connecting Your Accounts

The core feature of any modern budgeting tool is its ability to sync with your banks, freeing you from manual data entry forever. Reputable Canadian budgeting tools use secure, read-only connections, which means they can see your transactions but cannot move or access your money.

Your first task is to link your main accounts. This usually involves selecting your bank from a list and logging in through a secure portal.

What to Connect First:

- Your main chequing account: This is where your paycheque lands and most daily spending occurs.

- Your primary credit card(s): Linking these is essential for capturing the majority of your spending.

- Your main savings account: This gives you a clear picture of what you’re setting aside.

In apps like NeoSpend, this process is designed to be quick and painless, often taking just a few minutes. Once connected, the app will import your recent transaction history, giving you an immediate snapshot of your spending habits.

Customizing Categories for Your Canadian Life

With your transactions flowing in, it's time to make sense of them. Most apps do a decent job of automatically sorting your spending, but personalizing your categories is key to creating a budget that truly reflects your life.

Generic categories are a good starting point, but a Canadian budget needs specifics. Don't hesitate to create custom categories that match your actual spending.

Examples of Custom Canadian Categories:

- Groceries: Loblaws, Sobeys, Metro

- Transit: Presto, Compass Card, TTC

- Coffee: Tim Hortons, Second Cup

- Takeout: SkipTheDishes, DoorDash

- Bills: Rogers, BC Hydro, Enbridge

A personalized budget is a powerful budget. Seeing a category named "Kids' Hockey" instead of a vague "Entertainment" makes your spending more tangible and easier to manage.

This level of detail is where the real insights emerge. You might realize that your daily Tims run adds up to over $100 a month—a detail a generic "Food" category would completely miss.

Setting Up Your First Savings Goal

With your spending organized, it’s time to give your money a mission. Setting a clear, achievable savings goal is one of the most motivating things you can do. It transforms budgeting from a restrictive exercise into a powerful plan for your future.

Start with one meaningful goal, whether it's big or small.

- Define the Goal: What are you saving for? (e.g., "Trip to Whistler," "Emergency Fund," "New Laptop")

- Set the Amount: How much do you need? (e.g., $1,500)

- Give It a Deadline: When do you need it by? (e.g., in 10 months)

A good Canadian budgeting tool will do the math for you—in this case, $150 per month. Platforms like NeoSpend allow you to create dedicated goal pockets, watch your progress with visual trackers, and even automate transfers to make saving effortless. This simple step turns a vague wish into a concrete, actionable plan.

Advanced Budgeting Strategies for Canadians

You’ve linked your accounts and customized your categories. Now it's time to move beyond simple tracking and start telling your money where to go. This is where advanced budgeting strategies come in, transforming your tool from a passive observer into an active command centre for your financial life.

This shift from reactive to proactive is the secret to achieving your goals, whether that’s getting out of debt or building long-term wealth.

Implement a Proven Budgeting Method

Moving past basic tracking often means adopting a formal budgeting system. These frameworks provide rules and a clear structure that simplify financial decisions. The best Canadian budgeting tools, like NeoSpend, are flexible enough to support whichever method works best for you.

Here are two of the most popular and effective strategies:

The 50/30/20 Rule: This is a great starting point. It provides a simple guideline for allocating your after-tax income: 50% for "Needs" (rent, groceries, transit), 30% for "Wants" (dining out, hobbies, streaming services), and 20% for "Savings & Debt Repayment" (RRSP contributions, extra credit card payments). It offers control without overwhelming detail.

Zero-Based Budgeting: This method is more hands-on but incredibly precise. The goal is to make your income minus all your expenses, savings, and debt payments equal zero. Every dollar is assigned a job before the month begins. It’s the ultimate method for anyone who wants complete control over their cash flow.

Choosing a method turns vague financial hopes into a concrete plan you can execute every month.

Master Canadian-Specific Tactics

In addition to these frameworks, certain tactics are especially powerful for navigating our unique financial landscape.

One of the most effective is creating sinking funds. These are dedicated savings buckets for large, predictable expenses that don't occur monthly. For example, instead of scrambling to pay a $2,400 property tax bill in July, you can create a sinking fund and save $200 a month for it.

This simple strategy smooths out your cash flow and eliminates the stress of large, irregular bills. You can set up sinking funds for anything: annual car insurance premiums, holiday gifts, or new winter tires.

Another game-changer is the debt snowball method, particularly for tackling high-interest credit card debt. List your debts from the smallest balance to the largest. Continue making minimum payments on all of them, but direct any extra money toward the smallest debt. Once it's paid off, roll that payment amount over to the next-smallest debt. This creates a "snowball" of momentum that makes paying off debt feel motivating and achievable.

Conduct a Monthly Financial Review

Your budgeting tool contains a wealth of data about your financial habits. The final, critical step is to use it. A monthly financial review should be a non-negotiable ritual. This isn't about criticizing past spending; it's about learning from it to make smarter decisions next month.

Block off 30 minutes at the end of each month and ask yourself four simple questions:

- Where did I overspend? Identify the categories where you went over budget and understand why.

- Where did I underspend? Look for areas where you spent less than planned. This is extra money you can redirect to a savings goal or debt repayment.

- What trends are emerging? Use your app’s reports to spot patterns. Is your grocery bill slowly increasing? Is your "Subscriptions" category growing?

- How is my progress towards goals? Check in on your savings and debt repayment goals. Are you on track? Seeing your progress is the best motivation.

This monthly check-in is where your tool truly proves its value. With platforms like NeoSpend, you can generate spending reports and visualize your progress in seconds, turning raw data into actionable insights.

Your Top Questions, Answered

Starting with a new money management tool is a significant step, and it's natural to have questions. When it comes to your finances, you deserve clarity. Here are the answers to the most common questions Canadians have about budgeting tools.

Are These Budgeting Tools Actually Safe?

This is often the first and most important question. The answer is yes—reputable Canadian budgeting tools are built with robust security measures to protect your information. They use the same heavy-duty security as major banks.

Top apps like NeoSpend connect to your accounts using a secure, read-only link. This means the app can view your transaction data to help you budget, but it has no ability to move money or make changes to your accounts. Always look for tools that use industry-standard security like 256-bit encryption.

What’s the Real Difference Between Free and Paid Apps?

The choice between a free and a paid app depends on how detailed you want to get with your finances.

Free versions are perfect for mastering the fundamentals. They are excellent for tracking daily spending and creating a basic monthly budget. If you're just starting, a free tool can be a game-changer.

Paid versions unlock more powerful features, such as linking all your bank and investment accounts, tracking your complete net worth, smart forecasting, and access to customer support. If you're managing multiple goals or want a comprehensive 360-degree view of your finances, the small monthly fee is often a worthwhile investment.

Can a Budgeting App Really Help With My Investments?

Absolutely. This is where a good budgeting tool becomes essential. Many of the top apps for Canadians can securely sync with your investment accounts, including your RRSPs and TFSAs.

Having all your financial information in one place is a significant advantage. Instead of logging into multiple websites to check your chequing, credit, and investment accounts, you can see everything on a single dashboard. You can monitor your progress toward retirement, track investment performance, and understand how all your accounts work together to build your net worth.

Take Control of Your Financial Future

Gaining control over your finances isn't about luck; it's about taking small, deliberate steps. The best Canadian budgeting tools are more than just apps—they are personal financial co-pilots designed to help you navigate your unique money situation.

When you choose a tool that securely syncs with Canadian banks and helps you track your real-life goals, you're not just crunching numbers. You're gaining the clarity you need to build wealth, reduce stress, and feel confident in your financial decisions. The most challenging part is simply getting started.

Your Turn to Get Ahead

The idea of using smart tools for financial health is gaining traction everywhere. The federal government’s Budget 2025 aims to use digital tools to achieve $13 billion in annual savings. If the government can leverage technology to manage its finances, so can you. You can dig into the details of the federal government's financial modernization plans to learn more.

By choosing a tool that gives you a clear, real-time view of your spending, saving, and investing, you are taking charge of your money, not the other way around.

Takeaway: Financial clarity isn’t a one-time fix; it’s a daily habit. Consistently using a budgeting tool turns complex data into simple, actionable insights. This is how you trade financial stress for financial strength and build a future you can count on.

Ready to experience that "aha" moment with your own money? See what a clear financial picture can do for you. It’s time to take control and build a more secure future.