If you're looking for the best online banks in Canada, you'll quickly notice a few names popping up again and again: Tangerine, Simplii Financial, and EQ Bank. They've become the go-to choices for a reason. These digital-first banks are shaking up the old way of doing things by offering no-fee chequing, savings accounts that actually earn decent interest, and the freedom to manage it all from your phone.

Why Are So Many Canadians Switching to Online Banks?

The shift away from traditional brick-and-mortar branches isn't just a trend; it's a fundamental change in how Canadians handle their money. Online banks don't have the massive overhead costs of physical locations, and they pass those savings directly on to you in the form of better rates and fewer (or zero) fees. This is practical, smart banking.

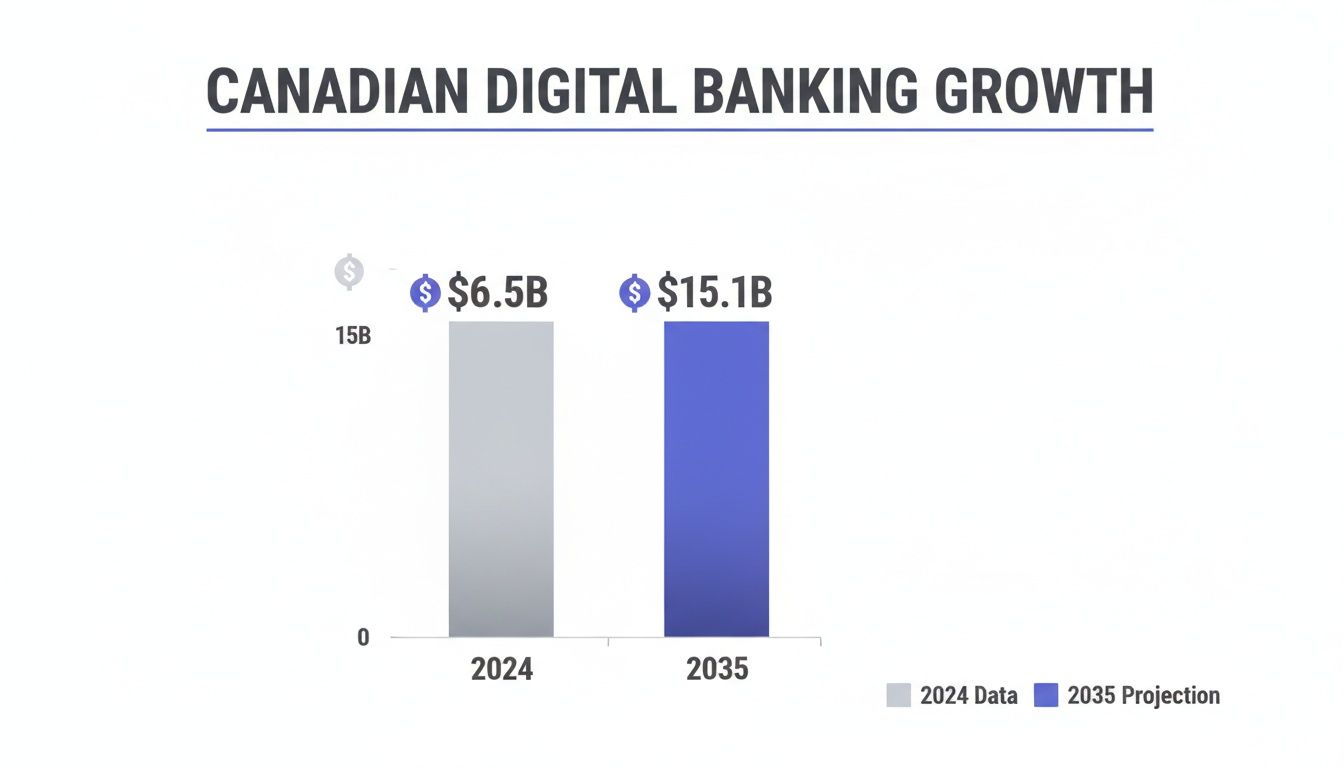

The proof is in the numbers. The digital banking scene in Canada hit $6.5 billion USD in 2024 and is expected to balloon to $15.1 billion USD by 2035. That kind of growth shows just how many of us are realizing the perks of banking online. You can learn more about this growth in Canada's digital banking market here.

So, what's driving the switch? It really boils down to a few key advantages:

- No More Monthly Fees: Most online banks offer chequing and savings accounts without those annoying monthly "maintenance" fees. For example, if you pay $15 a month now, switching could save you $180 a year.

- Higher Interest on Your Savings: Because their costs are lower, online banks can afford to pay you more interest on your savings. It’s a simple way to make your money work harder for you.

- Bank on Your Own Terms: Pay bills, deposit a cheque by snapping a photo, send an Interac e-Transfer®—it’s all done right from an app, whenever and wherever you are. No more rushing to a branch before it closes.

Take a look at Tangerine's interface. It’s clean, simple, and designed to make your life easier. No clutter, no confusion—just the information you need, right where you expect it.

Top Canadian Online Banks at a Glance

To help you get started, here's a quick rundown of what makes each of the top online banks stand out. This table cuts through the noise to show you what each one does best, so you can find a good match for your own financial style.

| Bank | Best For | Monthly Fee (Chequing) | Savings Interest Rate (Standard) | Unique Feature |

|---|---|---|---|---|

| Tangerine | All-in-one banking with great promotional rates. | $0 | 1.00% (often higher with promos) | Free access to Scotiabank's huge ATM network. |

| Simplii Financial | Seamless integration with CIBC's ATM network. | $0 | 0.40% (often higher with promos) | Offers a full suite of banking, including mortgages and loans. |

| EQ Bank | Consistently high interest rates on savings. | N/A (Offers a hybrid savings/chequing account) | 2.50% (often up to 4.00%) | High non-promotional interest rates and free e-Transfers. |

| Neo Financial | High cashback rewards and integrated spending. | $0 | 2.25% | A heavy focus on credit card rewards and retail partnerships. |

| Koho | Budgeting tools and credit-building features. | $0 - $19/month | Up to 5.00% (plan-dependent) | A prepaid Mastercard with options to help build your credit history. |

Once you've picked a bank, pair it with a smart money app like NeoSpend. Hooking up your new no-fee account gives you a single, clear view of your entire financial picture. NeoSpend helps you see where every dollar is going, making it the perfect combination for taking control of your money right from the start.

Comparing Canada's Top Online Banks in Detail

Picking the right online bank in Canada goes way beyond chasing the flashiest sign-up bonus. To make a smart choice, you have to look at the details that impact your money day-to-day. Let’s break down the big players—Tangerine, Simplii Financial, and EQ Bank—and see how they stack up on what really matters: fees, rates, app experience, and customer support. This is a practical guide to figure out which bank actually fits your life.

And it's clear Canadians are embracing this shift. The digital banking market is growing fast, and it's not slowing down anytime soon.

The market is expected to more than double by 2035, which tells you one thing: digital-first banking is here to stay because it just makes sense for a lot of people.

Tangerine: The All-Rounder with Big Bank DNA

Tangerine is Scotiabank’s digital-only offspring, and it inherited the best traits from both sides of the family. You get the scrappy, no-fee approach of an online bank with the safety net and ATM network of a "Big Five" bank. That free access to Scotiabank’s ATMs is a huge perk for anyone who hasn’t gone completely cashless.

Their main draw? Killer promotional interest rates for new clients. For the first five months, you can often earn a much higher interest rate, which is a fantastic way to kickstart a savings goal. After that, the rate drops back to a standard level, but that initial boost is hard to beat. Their app is clean and genuinely useful, with built-in tools for setting and tracking financial goals. It helps you actually see your progress, whether you’re saving for a down payment on a place in Calgary or just a weekend trip.

It's no surprise they're a top performer in customer satisfaction. The 2025 J.D. Power Canada Retail Banking Satisfaction Study put Tangerine right at the top alongside RBC Royal Bank, which says a lot. People love them because they deliver a smooth, no-fuss experience. You can read the full J.D. Power study here.

Simplii Financial: The Full-Service Digital Branch

Simplii Financial is CIBC’s answer to online banking, and it’s designed to be a one-stop shop. Just like Tangerine, you get free access to the parent company’s ATM network—in this case, CIBC machines all across the country.

Where Simplii really shines is its sheer range of products. They don’t just do chequing and savings. You can get mortgages, lines of credit, GICs, and even mutual funds. This makes Simplii an amazing option if you want to ditch monthly fees but keep all your financial accounts under one digital roof.

The trade-off is that their everyday savings rates aren’t usually the highest on the market. They lean on welcome offers to stay competitive, so it’s a better fit for someone who values the convenience of an all-in-one platform over squeezing every last drop of interest from their savings.

The bottom line: If you want a digital bank that can handle everything from your morning coffee purchase to your mortgage application without charging a monthly fee, Simplii Financial is a powerhouse. It’s the closest you’ll get to a traditional full-service bank, just without the physical branches.

EQ Bank: The High-Interest Savings Machine

EQ Bank didn't try to compete on every front. Instead, they focused on one thing and became the best at it: offering consistently high interest rates. No temporary "teaser" rates here—their everyday rate is almost always one of the best you can find in Canada.

They did this by rethinking the whole chequing vs. savings account model. Their Savings Plus Account is a hybrid that pays you high interest on every dollar, but you can still use it to pay bills and send unlimited free Interac e-Transfers®. It’s a simple, brilliant move that means you don't have to constantly shuffle money between accounts to maximize your earnings. Your everyday cash works just as hard as your long-term savings.

This focus makes EQ Bank a favourite for serious savers and anyone building an emergency fund.

So, what's the catch? EQ Bank doesn't have its own debit card or ATM access. If you need cash, you have to e-Transfer money to an account at another bank first. For the growing number of Canadians who rarely handle cash, it’s a tiny inconvenience that’s easily worth the extra interest.

Mobile App Usability and User Experience

With an online bank, the mobile app isn't just a feature—it is the bank. A clunky app can be a dealbreaker.

- Tangerine: Their app is widely praised for its clean design and intuitive navigation. The goal-setting features are fantastic for making saving feel less like a chore and more like a game you can win.

- Simplii: The app is solid and reliable, much like its parent, CIBC. It does everything you need it to do efficiently, without any unnecessary bells and whistles.

- EQ Bank: Their app is beautifully minimalist. It’s built to do two things perfectly: show you how much interest you're earning and make it dead simple to move your money. It nails both.

How to Connect to Your Other Financial Tools

Here’s something people often forget to check: does the bank play nice with other apps? The best online banks understand that your financial life doesn’t exist in a silo. You need the full picture.

The good news is that all three—Tangerine, Simplii, and EQ Bank—integrate securely with budgeting tools. This lets an app like NeoSpend pull in your transaction data through a secure, read-only connection. This is key for security; NeoSpend can see your spending to help you budget, but it has zero ability to actually touch or move your money. For example, a freelancer in Toronto could link their Simplii account (for business expenses) and their EQ Bank savings (for taxes) to NeoSpend. The app automatically categorizes everything, giving them one clear dashboard to see exactly where their money is going and growing. This kind of connection turns a simple bank account into a central piece of a much smarter financial system.

How to Find the Right Online Bank for Your Lifestyle

Your financial life isn’t one-size-fits-all, so your bank shouldn't be either. The goal isn’t to find the single “best” online bank in Canada, but to find the one that clicks with your specific habits and goals. What works for a student is totally different from what a freelancer needs, and a super-saver is playing a different game than a long-term investor. Let's look at some real-world Canadian scenarios to find your perfect fit.

For the Student Managing a Tight Budget

When you're a student, every dollar counts. You need a bank that eliminates fees, makes saving easier, and lets you access your cash without hassle.

- Top Recommendation: You can’t go wrong with Tangerine or Simplii Financial. Both offer genuinely no-fee chequing accounts, meaning your student loan or part-time job earnings won’t be eroded by monthly charges.

- Why It Works: The biggest win here is free access to a massive ATM network (Scotiabank for Tangerine, CIBC for Simplii). This is a lifesaver for students who need to grab cash on or near campus without paying those annoying out-of-network fees.

- Practical Example: You need cash to buy a used textbook from another student. With Tangerine, you can just walk to the nearest Scotiabank ATM and pull out what you need. No fees, no hassle. It’s that simple.

For the Freelancer with Variable Income

Freelancers and gig economy workers constantly juggle fluctuating income and need to separate business expenses for tax time. The right bank account brings order to that chaos.

- Top Recommendation: EQ Bank is a clear winner for freelancers. Their Savings Plus Account is a hybrid that earns high interest but acts like a chequing account, giving you unlimited free Interac e-Transfers®. This is a huge deal when you’re getting paid by different clients and paying out business expenses all month long.

- Why It Works: Not having to pay $1.50 per e-Transfer adds up to real savings over a year. Plus, earning a solid interest rate on the money you've set aside for taxes means it’s actually working for you instead of just sitting there.

Pro Tip for Freelancers: Connect your EQ Bank account to a money management app like NeoSpend. Its secure, read-only sync automatically organizes your transactions, giving you a clear picture of your income and spending. This is how NeoSpend helps you manage money smarter, especially when tax season rolls around.

For the Dedicated Saver Maximizing Every Dollar

If your main goal is to grow your money as fast as possible, then only one thing really matters: the interest rate. You need a bank that consistently offers the best returns without relying on short-term promotional offers.

- Top Recommendation: EQ Bank is the champion in this category. They’ve built their reputation on offering one of the best non-promotional high-interest savings rates in Canada, year after year.

- Why It Works: With EQ Bank, you’re not constantly chasing the next welcome bonus. Whether it’s your emergency fund or a down payment fund, your money is always earning a top-tier rate. That means it compounds faster, helping you hit your goals sooner.

- Real-World Scenario: Let's say you're saving $10,000 for a down payment. At a 4.00% interest rate with EQ Bank, you’d earn $400 in a year. With a more typical 1.00% rate from another bank, you'd only get $100. That $300 difference is the power of a consistently high rate.

For the Investor Focused on Long-Term Growth

For investors, a basic savings account isn't enough. You need an online bank that provides easy access to registered accounts like TFSAs and RRSPs on a platform that doesn’t drain your returns with high fees.

- Top Recommendation: Tangerine and Simplii Financial are both strong choices here. They give you a straightforward way to open and manage GICs, mutual funds, and self-directed TFSA and RRSP accounts.

- Why It Works: They offer a convenient all-in-one experience. You can handle your daily banking and keep an eye on your long-term investments with a single login, which really simplifies things. Their investment products are also designed to be approachable, even for beginners.

- Smart Integration: By linking your Tangerine investment and chequing accounts to NeoSpend, you get a full, unified view of your entire financial picture. NeoSpend lets you see your daily spending right next to your TFSA growth, giving you the clarity needed to make smarter decisions.

How Online Banks and Budgeting Tools Create a Power Couple

Picking one of Canada's best online banks is a great start, but the real magic happens when you connect it to a smart budgeting tool. Your bank account is the engine, but a budgeting app is the dashboard—it shows you where you're headed, how fast you're going, and how much fuel is left. That connection gives you a truly complete picture of your financial health.

This is all possible through interoperability, a fancy word that means different financial apps can talk to each other securely. Modern apps like NeoSpend are built to link with all your accounts—chequing, savings, credit cards, and investments—to pull everything into one place. Suddenly, you have a bird's-eye view of your money that a single bank account could never offer on its own.

The Power of a Single Financial Dashboard

Trying to manage your money across multiple accounts can feel like building a puzzle with pieces from different boxes. A good budgeting tool puts all those pieces on one table so you can finally see how they fit. When you link your online bank to NeoSpend, it automatically sorts your transactions. That morning Tim Hortons coffee, your monthly Netflix bill, and that weekly grocery haul at Loblaws? All categorized without you lifting a finger.

This is where actionable insights come from. You start to see spending patterns you’d otherwise miss, making it easier to spot areas to cut back and make smart decisions instead of just guessing.

How Secure Connections Keep Your Data Safe

One of the first questions people ask is, "Is it actually safe to connect my bank account to an app?" The answer is a firm yes, thanks to serious security technology. Reputable apps like NeoSpend use a secure, read-only connection to sync with your bank. "Read-only" means the app can see your transaction history to help you budget, but it has zero power to move, withdraw, or do anything with your money.

This technology is protected by bank-level 256-bit encryption, the same heavy-duty security that all major financial institutions use. Your login details are never stored in a readable format, and your data is protected every step of the way.

Canadian banks are rock-solid, which allows them to pour resources into making these digital integrations as safe as possible. With total loans in the sector projected to hit C$4.34 trillion by late 2025 (a 3.2% year-over-year climb), they have the resources to invest in top-tier security. You can read more about the strong outlook for Canadian banks and their digital growth.

A Real-World Canadian Example

Let's make this practical. Imagine a couple in Vancouver who uses Tangerine for their joint chequing and EQ Bank for their high-interest savings. By connecting both accounts to NeoSpend, here’s what they can do:

- Track Shared Bills: They see all upcoming payments—rent, hydro, internet—in a single calendar. No more missed due dates.

- Monitor Spending Together: NeoSpend pulls transactions from both accounts, giving them a clear picture of their combined monthly spending on groceries and nights out.

- Crush Their Savings Goals: They're saving for a trip to Banff. With everything in one place, they can see in real-time how their spending choices affect that goal, making it easier to stay motivated and on track. This is exactly how NeoSpend helps you manage money smarter.

How to Make Your Final Choice: A Simple Checklist

Alright, we've covered a lot. Now it's time to zero in on the one bank that's the right fit for you. Choosing an online bank comes down to knowing yourself and how you handle your money. To help, here's a simple checklist to filter your options and make a confident choice.

Your Decision-Making Checklist

Run through these questions. Your answers will clearly point you toward the bank that best suits your needs.

- How often do you use cash? If you still deal with cash, free ATM access through a bank like Tangerine or Simplii is essential. If you’re fully digital, EQ Bank’s no-ATM model might be a non-issue.

- Which fees annoy you the most? Take a real look at the fee schedules. Focus on services you actually use, like Interac e-Transfers® or sending money internationally, and choose the bank that eliminates those costs.

- What’s your main savings goal right now? If your top priority is squeezing every last bit of interest from your savings, EQ Bank is tough to beat. If you prefer the convenience of having everything—including solid TFSA and RRSP options—under one roof, Tangerine and Simplii are great bets.

- What are your deal-breaker features? Do you need built-in investing? A credit card with great rewards? Line up your must-haves with what each bank actually delivers.

The most important thing here is honesty. A bank with the highest interest rate is only the "best" if its features don't clash with how you actually live your financial life.

Once you’ve settled on a bank, there’s one last step to level up your money management: connect your new accounts to NeoSpend. This is how you get that full, clear picture of everything you own and owe, all in one place. It’s the perfect way to make the most of your new no-fee setup. Check out how NeoSpend can get you started on the right foot today.

Common Questions About Online Banking in Canada

Switching banks is a big move, so it’s normal to have questions. We’ve answered some of the most common things Canadians ask when considering a digital bank.

Is my money safe in an online bank?

Yes, absolutely. Your money is just as secure with a reputable online bank as it is with a big five bank. They are members of the Canada Deposit Insurance Corporation (CDIC), a federal Crown corporation. This means your eligible deposits are protected for up to $100,000 per insured category. So, in the very unlikely event the bank has a problem, your money is safe. They also use bank-level encryption and fraud monitoring to keep your accounts locked down.

How do I deposit cash or a cheque without a branch?

This is easier than you think. For cheques, all online banks have mobile cheque deposit in their app. You just snap a picture of the cheque to deposit it. For cash, online banks partner with major traditional banks, giving you free access to their ATM network for deposits.

- Tangerine uses Scotiabank's ATM network.

- Simplii Financial uses CIBC's ATM network.

Can I get mortgages and investments from an online bank?

Yes. The best online banks offer more than just basic accounts. You can often get competitive rates on mortgages, GICs, Tax-Free Savings Accounts (TFSAs), and Registered Retirement Savings Plans (RRSPs). While their investment options might not be as vast as a specialized brokerage, they are more than enough for the average Canadian’s goals. To see how these accounts fit into your overall financial picture, an app like NeoSpend can sync everything into one simple view.

What if I need to talk to a real person?

Just because there’s no branch doesn’t mean you’re on your own. Online banks have robust customer support through secure in-app chat, dedicated phone lines (often with flexible hours), and detailed online help centres for quick answers.

Your Takeaway: Choosing the best online bank in Canada is about matching its features to your lifestyle. Whether you prioritize high interest with EQ Bank, all-in-one convenience with Simplii, or a great all-around experience with Tangerine, switching can save you money and simplify your finances.

Ready to see your new online bank account in a whole new light? Connecting it to NeoSpend gives you the complete picture of your finances, with AI-powered insights to help you budget smarter and save more. Explore how NeoSpend can help you achieve your financial goals today.